Incident Response Market Report Scope & Overview:

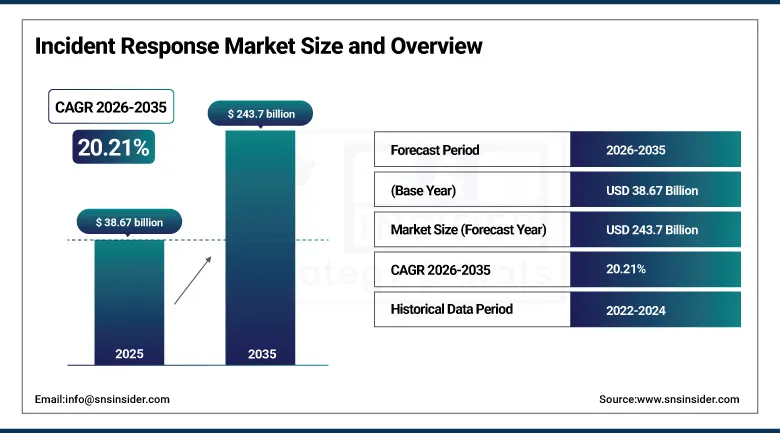

The Incident Response Market was valued at USD 38.67 Billion in 2025 and is expected to reach USD 243.7 Billion by 2035, growing at a CAGR of 20.21% from 2026–2035.

The Incident Response Market is experiencing substantial growth because of the rising number and complexity of attacks against corporations, governments, and critical infrastructure. The growing popularity of cloud computing and digital transformations is increasing the number of possible vulnerabilities, which makes real-time detection and response capabilities a must-have. Another factor that contributes to the Incident Response Market growth is regulatory compliance, which creates the need for proper security measures. Finally, artificial intelligence (AI), automation, and SOAR platforms can improve efficiency, reduce downtime, and mitigate losses, thus, fostering market growth.

According to the International Telecommunication Union (ITU), global cybercrime losses are expected to reach USD 10.5 trillion annually by 2025, reflecting the escalating scale and financial impact of cyber incidents worldwide.The World Economic Forum (WEF) reports that 72% of organizations have experienced an increase in cyber risks due to digital transformation and cloud adoption, highlighting the expanding threat landscape for enterprises.

Market Size and Forecast

- Market Size in 2026E: USD 46.49 Billion

- Market Size by 2035: USD 243.7 Billion

- CAGR: 20.21% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

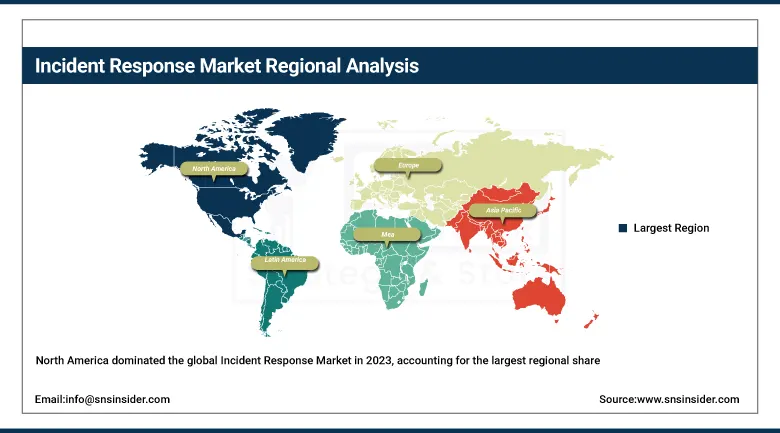

- Largest Region: North America

To Get more information on Incident Response Market - Request Free Sample Report

Incident Response Market Trends

-

Rising frequency and sophistication of cyberattacks driving strong demand for advanced incident response solutions and rapid threat mitigation capabilities

-

Increasing adoption of AI and machine learning for automated threat detection, faster incident analysis, and real-time security response

-

Growing regulatory compliance requirements and data protection laws compelling organizations to implement structured incident response frameworks

-

Expanding integration of cloud-based security platforms enabling scalable, centralized, and faster incident response across distributed IT environments

-

Rising focus on cybersecurity resilience among enterprises, especially in BFSI, healthcare, and IT sectors, boosting adoption of proactive incident response strategies

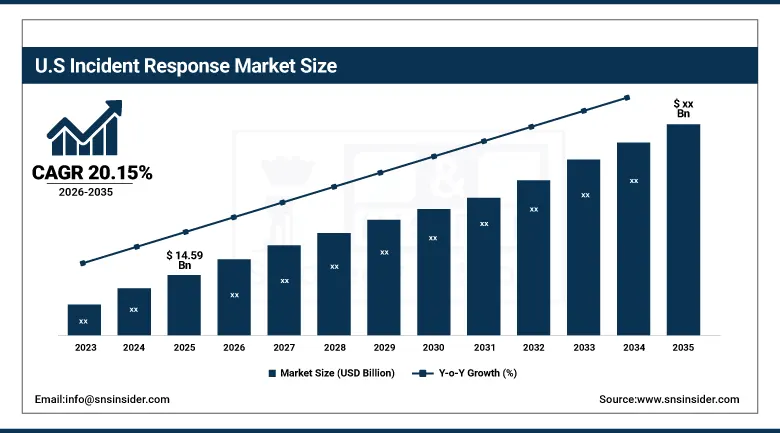

The U.S. Incident Response Market Outlook

The U.S. Incident Response Market was valued at USD 14.59 Billion in 2025 and is expected to reach USD 91.47 Billion by 2035, growing at a CAGR of 20.15% from 2026 to 2035.

The United States leads North American revenues through the world’s most mature enterprise cybersecurity investment culture, the SEC’s cybersecurity disclosure rules requiring material incident reporting within four business days, and the concentration of leading incident response service providers including IBM X-Force, CrowdStrike Falcon Complete, Palo Alto Networks Unit 42, and Mandiant whose U.S. headquarters sustain global service delivery capabilities. Federal government incident response investment under CISA’s cybersecurity programmes and critical infrastructure protection mandates creates a substantial government-funded demand parallel to commercial enterprise market growth.

According to the Federal Bureau of Investigation (FBI) Internet Crime Complaint Center (IC3), cybercrime losses in the United States reached approximately USD 20.9 billion in 2025, underscoring the escalating financial impact of cyber incidents and strengthening the demand for advanced incident response capabilities.

Incident Response Market Segment Analysis

-

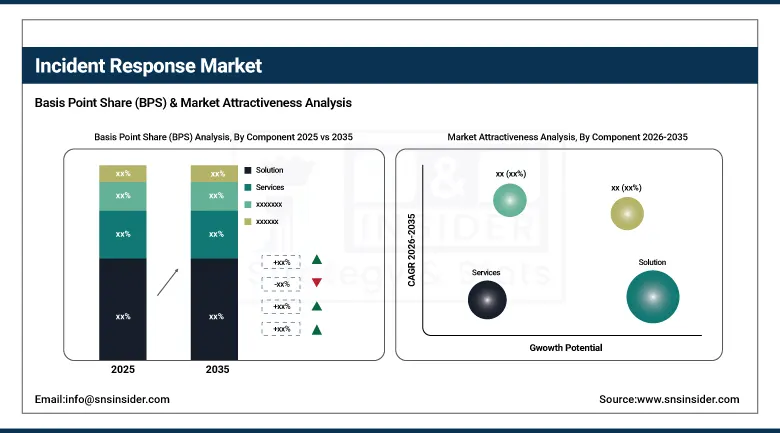

By Component, Solution segment dominated the Incident Response Market in 2025 with 64% share; Services segment is the fastest growing segment.

-

By Service Type, Assessment and Response segment dominated the market in 2025 with 38% share; Advanced Threat Hunting segment is the fastest growing segment.

-

By Security Type, Endpoint Security segment dominated the market in 2025 with 41% share; Cloud Security segment is the fastest growing segment.

-

By Organization Size, Large Enterprises segment dominated the market in 2025 with 67% share; SMEs segment is the fastest growing segment.

-

By Vertical, BFSI segment dominated the market in 2025 with 29% share; Healthcare & Life Sciences segment is the fastest growing segment.

By Component, solution segment dominates the incident response market, while services segment is the fastest-growing segment

The Solution segment dominated the Incident Response Market owing to high usage rates of cyber security platforms providing real-time detection of threats and responses and centralization of incidents. Enterprises look for solution-driven platforms that help them reduce the response time, limit the extent of the damage, and enhance operational effectiveness. The surge in the number of cyber security risks and the demand for compliance have also helped Solution consolidate its position in the market.

The Services segment is growing rapidly fueled by growing preference for managed services and incident response specialists. Enterprises lack resources and skills for handling complex attacks and hence outsource monitoring, forensics, and incident response to specialized service providers. Growing complexity of attacks and the necessity of round-the-clock security services are further fueling their demand. Services offer enterprises flexibility and continuous coverage of their security needs.

By Service Type, assessment and response segment dominates the incident response market, while advanced threat hunting segment is the fastest-growing segment

The Assessment and Response segment dominated the market as companies preferred assessing their weaknesses and carrying out immediate remedial action when cyber attacks occur. This segment is vital for ensuring low downtime, reduced costs, and data breaches. Businesses need well-planned frameworks for response to ensure business continuity and compliance. With increasing rates of cyberattacks and increasing awareness about risk management techniques, the significance of assessment and response services has gained momentum.

Advanced Threat Hunting is the fastest-growing segment owing to the emergence of the concept of proactive cybersecurity measures. There is increasing emphasis on continuous monitoring and behavior analytics in order to identify any threats that might go undetected and be more sophisticated in nature. The number of occurrences of advanced persistent threats, ransomware attacks, and zero-day attacks has been increasing the demand for advanced threat hunting solutions.

By Security Type, endpoint security segment dominates the incident response market, while cloud security segment is the fastest-growing segment

Endpoint Security dominated the market owing to the growing number of connected devices and remote working conditions. Many companies rely on endpoint security solutions as they ensure security from different types of cyber threats such as viruses, ransomware, and phishing attempts. The growing number of vulnerabilities, coupled with regulations and frequent attacks, has resulted in the leading position of this cybersecurity category. Companies consider endpoint security a priority layer for implementing incident response plans worldwide.

Cloud Security is the fastest-growing segment owing to the widespread use of cloud computing solutions and migration of workloads to digital infrastructure. Clouds have become key areas for hackers as there is valuable data stored in the clouds. The need to secure corporate data requires advanced approaches to incident response and protection of cloud resources. Cloud adoption is becoming more prevalent which will lead to higher revenues generated from sales of cloud security solutions.

By Organization Size, large enterprises segment dominates the incident response market, while SMEs segment is the fastest-growing segment

Large Enterprises dominated the market owing to their robust digital infrastructure, sensitive information, and susceptibility to more advanced cyberattacks. They deploy cutting-edge security operations centers and incident response systems for comprehensive cybersecurity. Their stringent regulatory compliance needs and higher risk of financial losses due to breaches encourage the use of advanced incident response solutions. The size of their budget and IT operations ensure continuous investment in such solutions.

SMEs are the fastest-growing segment as increase in cyberattacks targeting small businesses without adequate security measures. Increased awareness about cybersecurity and availability of affordable cloud computing solutions are major factors contributing to adoption. The growing digital transformation among SMEs has also increased the need to deploy incident response solutions. Small Medium Enterprises are quickly adopting incident response solutions for their cost-effectiveness and ease of use.

By Vertical, BFSI segment dominates the incident response market, while healthcare & life sciences segment is the fastest-growing segment

The BFSI segment dominated the market due to the frequent occurrence of cyber-attacks and the utmost need to secure financial information and transactions. The BFSI segment is prone to many cyber threats and cyber-attacks because of the massive volume of sensitive financial information that it holds. Due to regulatory requirements and the necessity to secure data and transactions, the BFSI segment makes continuous efforts for upgrading its incident response systems.

Healthcare & Life Sciences is the fastest-growing segment due to high digitization rates and increased adoption of connected medical devices. The rapid digitization has increased the vulnerabilities of the segment towards many cyber attacks including ransomware attacks and data breaches. Increased adoption of telemedicine and the necessity to comply with new regulations is driving demand.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Incident Response Market Insights

North America dominated the global Incident Response Market in 2025, accounting for the largest regional share through its mature enterprise cybersecurity investment culture, stringent regulatory compliance framework, and concentration of leading incident response platform and service providers. The United States accounts for approximately 82.5% of North American revenues through IBM X-Force, CrowdStrike, Palo Alto Networks Unit 42, Mandiant, and Secureworks whose combined platform and service capability defines global incident response market standards.

The Cybersecurity and Infrastructure Security Agency (CISA) reports that ransomware remains a major and persistent threat to U.S. critical infrastructure, with incidents increasingly impacting sectors such as healthcare, energy, and government systems, reflecting the growing need for advanced incident response capabilities.

According to the Federal Bureau of Investigation (FBI) Internet Crime Report, reported cybercrime losses exceeded USD 12.5 billion in a recent year, underscoring the rising financial impact of cyber incidents and the critical importance of rapid detection and response mechanisms.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Incident Response Market Insights

Europe is a significant incident response market where GDPR’s 72-hour breach notification requirement creating immediate forensic investigation urgency, the NIS2 Directive’s incident reporting obligations across critical infrastructure operators, and DORA’s financial services ICT incident classification and reporting framework collectively create regulatory compliance-driven incident response investment that sustains structured enterprise procurement. Germany accounts for approximately 22.4% of European revenues through its large enterprise technology sector, the BSI’s cybersecurity framework creating government agency procurement, and the commercial presence of IBM, T-Systems, and European MDR providers.

According to the European Union Agency for Cybersecurity (ENISA), 4,875 cybersecurity incidents were analyzed in the 2025 reporting window, reflecting the growing volume and complexity of cyber threats across the region and the increasing need for structured incident response capabilities.

ENISA’s Threat Landscape report indicates that approximately 60% of intrusion access incidents in Europe originate from phishing attacks, highlighting social engineering as a dominant entry vector and reinforcing the importance of rapid detection, response, and user-awareness strategies in cybersecurity defense frameworks.

Asia Pacific Incident Response Market Insights

Asia Pacific is the fastest-growing regional incident response market, driven by accelerating digital transformation creating expanding attack surface, growing regulatory cybersecurity frameworks including Singapore’s Cybersecurity Act, India’s CERT-In 6-hour reporting mandate, and China’s Multi-Level Protection Scheme mandating enterprise incident response capabilities. China accounts for approximately 38.5% of Asia Pacific revenues through its large enterprise technology sector, government critical infrastructure protection investment, and growing domestic cybersecurity platform development.

India is the most commercially dynamic emerging incident response market, where the CERT-In 6-hour breach reporting mandate’s demanding compliance timeline creates urgent investment in detection and response capabilities that India’s rapidly digitalising economy’s large enterprise population must develop.

The FBI–CISA advisory ecosystem reports that more than 350 healthcare facilities were impacted in a single coordinated ransomware campaign, highlighting the growing scale and sophistication of attacks targeting critical healthcare infrastructure and reinforcing the need for robust incident response mechanisms.

FBI IC3 data and CISA alerts indicate a 400% increase in healthcare ransomware activity in recent multi-region attack waves, including incidents linked to APAC-connected infrastructure, underscoring the accelerating threat landscape and the rising demand for advanced cybersecurity response capabilities.

MEA & Latin America Incident Response Market Insights

The UAE leads MEA revenues at approximately 22.8% through its advanced digital economy’s cybersecurity investment, the Dubai Cybersecurity Strategy’s enterprise and government mandate, and the concentration of MENA regional financial and technology sector organisations whose high-value data creates incident response preparedness motivation. Saudi Arabia’s National Cybersecurity Authority and Vision 2030’s digital infrastructure investment create growing institutional incident response programme procurement.

Brazil leads Latin American revenues at approximately 43.8% through its large financial services sector’s LGPD compliance investment, the growing enterprise technology sector’s cybersecurity incident response programme development, and the Banco Central do Brasil’s cybersecurity circular requirements for financial institution incident response capability documentation. Mexico and Colombia contribute growing secondary demand through their financial services regulation and enterprise digitalisation investment.

Market Dynamics

Growth Drivers: Escalating ransomware frequency and SEC breach disclosure mandates creating non-discretionary incident response investment across regulated industries

The incident response market’s exceptional growth rate is driven by the structural alignment of three compounding commercial forces: ransomware’s evolution into the dominant cyber threat whose average financial impact of USD 4.88 million per breach in 2024 creates the most compelling individual risk management investment case in enterprise cybersecurity, regulatory disclosure mandates whose breach notification timelines require pre-established incident response capability rather than improvised post-breach contractor engagement, and the progressive professionalisation of criminal threat actor organisations whose sophisticated attack tooling and operational security exceeds the detection capability of organisations without purpose-built incident response investment.

Each new regulatory disclosure requirement, SEC cybersecurity rules, DORA, NIS2, or CERT-In 6-hour mandate, creates a new jurisdiction-wide compliance investment event whose commercial scale multiplies with each affected enterprise.

Restraints: Shortage of skilled incident response professionals and high retainer cost limiting adoption among resource-constrained small and medium enterprises

The global cybersecurity workforce shortage, whose estimated deficit of 3.5 million unfilled positions creates acute scarcity of incident response analysts, forensic investigators, and threat intelligence specialists, constrains the service market’s capacity expansion pace relative to demand growth, creating delivery bottlenecks at established incident response service providers whose analyst hiring and training timelines cannot match the geometric growth of client demand.

The cost of retainer-based incident response service agreements, whose annual fees of USD 50,000 to USD 500,000 for guaranteed response time commitments represent budget allocations that SME information security budgets frequently cannot accommodate, limits managed incident response adoption to larger enterprise organisations whose security programme maturity and budget scale support premium service procurement.

Opportunities: AI-powered autonomous investigation automation and emerging market regulatory mandates creating transformative commercial expansion frontiers for incident response

AI-powered autonomous investigation systems that analyse security telemetry, correlate attack indicators across the kill chain, generate investigation summaries, and recommend containment actions without requiring analyst queues represent the most commercially transformative capability advancement in incident response history, whose successful deployment enables existing analyst teams to handle the growing alert volumes that expanding attack surface generates without proportional headcount investment.

Each incident response platform that demonstrates documented mean-time-to-respond improvement through AI investigation automation creates competitive differentiation that sustains premium pricing and accelerates enterprise adoption. Emerging market regulatory mandates including India’s CERT-In reporting requirement, GCC national cybersecurity strategies, and Southeast Asian digital security regulations collectively create new compliance-driven incident response investment markets whose commercial scale grows with each jurisdiction that formalises enterprise cybersecurity programme requirements.

Recent Developments:

-

2025: CrowdStrike introduced Charlotte AI Investigator within its Falcon platform, providing autonomous AI-powered alert investigation that analyses endpoint telemetry, correlates related events, and generates prioritised investigation summaries, reducing mean time to respond from hours to minutes.

-

2024: IBM introduced a generative AI-powered cybersecurity assistant within IBM X-Force Incident Response, enabling natural language security event queries, contextual threat analysis, and automated incident documentation that accelerates investigation workflows substantially.

-

2024: Palo Alto Networks Unit 42 expanded its AI-driven incident response retainer programme with enhanced threat intelligence integration, providing pre-breach attack surface assessment and post-breach containment acceleration through its Cortex XSOAR automated playbook platform.

Incident Response Market Key Players are:

-

IBM Corporation

-

Microsoft Corporation

-

Cisco Systems, Inc.

-

Palo Alto Networks, Inc.

-

CrowdStrike Holdings, Inc.

-

Rapid7, Inc.

-

Fortinet, Inc.

-

FireEye (Trellix)

-

Check Point Software Technologies Ltd.

-

Splunk Inc.

-

AT&T Cybersecurity

-

Secureworks Inc.

-

McAfee Corp.

-

Trend Micro Incorporated

-

Kaspersky Lab

-

Broadcom Inc. (Symantec Enterprise)

-

Oracle Corporation

-

Amazon Web Services (AWS)

-

Google Cloud (Alphabet Inc.)

-

BAE Systems Applied Intelligence

Incident Response Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.67 Billion |

| Market Size by 2035 | USD 243.7 Billion |

| CAGR | CAGR of 20.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Services) • By Deployment Mode (Cloud-Based, On-Premise) • By Organization Size (Large Enterprises, Small & Medium-Sized Enterprises) • By Security Type (Web Security, Application Security, Endpoint Security, Network Security, Cloud Security) • By End User (BFSI, Healthcare, IT & Telecom, Government, Manufacturing, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Microsoft Corporation, Cisco Systems, Inc., Palo Alto Networks, Inc., CrowdStrike Holdings, Inc., Rapid7, Inc., Fortinet, Inc., FireEye (Trellix), Check Point Software Technologies Ltd., Splunk Inc., AT&T Cybersecurity, Secureworks Inc., McAfee Corp., Trend Micro Incorporated, Kaspersky Lab, Broadcom Inc. (Symantec Enterprise), Oracle Corporation, Amazon Web Services (AWS), Google Cloud (Alphabet Inc.), BAE Systems Applied Intelligence |

Frequently Asked Questions

The Incident Response Market is expected to grow at a CAGR of 20.21% from 2026 to 2035.

The Incident Response Market was valued at USD 38.67 Billion in 2025.

Rising ransomware costs, strict breach disclosure regulations, and AI-driven automation are accelerating incident response market growth.

The Services segment dominated the Incident Response Market in 2025.

North America dominated the Incident Response Market in 2025.

Get in Touch