Indium Phosphide Wafer Market Report Scope & Overview:

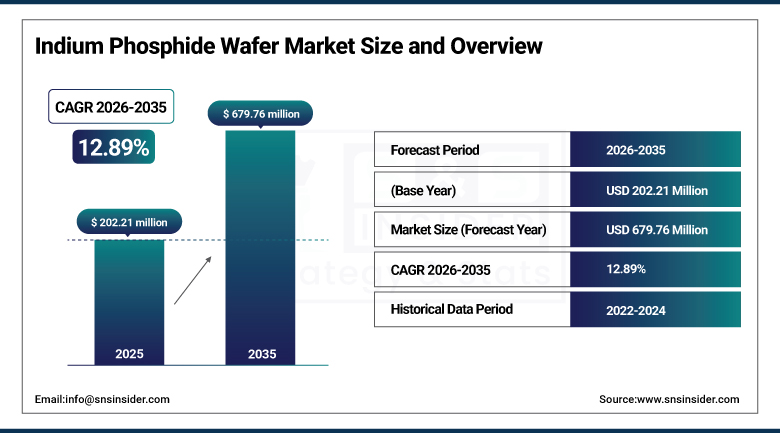

The Indium Phosphide Wafer Market size was valued at USD 202.21 Million in 2025 and is expected to reach USD 679.76 Million by 2035, growing at a CAGR of 12.89% from 2026–2035.

Indium phosphide is a compound semiconductor material prized for its superior electron mobility that make it the material of choice for high-speed, low-power optoelectronic devices. Growth in this market is closely tied to the buildout of data centers, AI infrastructure, telecommunications networks, and sensing technologies, all of which depend on the kind of high-frequency, energy-efficient photonic components that only InP can reliably deliver at scale. One of the key reasons for growing InP wafers demand is the further implementation of 5G technology and future data transmission technologies, which is becoming even more evident as the companies increase wafer sizes to cut down cost per device and increase manufacturing volumes for transceivers based on artificial intelligence and coherent optical communications.

On March 25, 2024, Coherent Corp. announced it had established the world's first capability for 6-inch indium phosphide wafer fabrication, at its Sherman, Texas, and Järfälla, Sweden facilities. The milestone increases production capacity fourfold per wafer and reduces die costs by more than 60% for InP optoelectronic devices used in coherent optical communications, datacom transceivers, AI interconnects, and future 6G wireless applications, positioning Coherent to meet surging demand from AI infrastructure and next-generation network buildouts.

InP Wafers Market Size and Forecast

-

Market Size in 2026E: USD 228.27 Million

-

Market Size by 2035: USD 679.76 Million

-

CAGR: 12.89% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Indium Phosphide Wafer Market - Request Free Sample Report

Indium Phosphide Wafer Market Trends

-

Increasing adoption of 6-inch indium phosphide wafers is improving manufacturing efficiency, production yields, and cost competitiveness for advanced photonic devices.

-

Rising AI data center investments are driving demand for InP-based lasers and photodetectors used in high-speed optical interconnects and coherent communications.

-

Advancements in InP-based multi-junction solar cells are expanding applications in high-efficiency photovoltaic and aerospace energy systems.

-

Expansion of 5G infrastructure and emerging 6G research is increasing demand for indium phosphide optical components in next-generation telecommunications networks.

-

Government semiconductor incentive programs are accelerating investments in compound semiconductor manufacturing, strengthening global indium phosphide wafer production capacity.

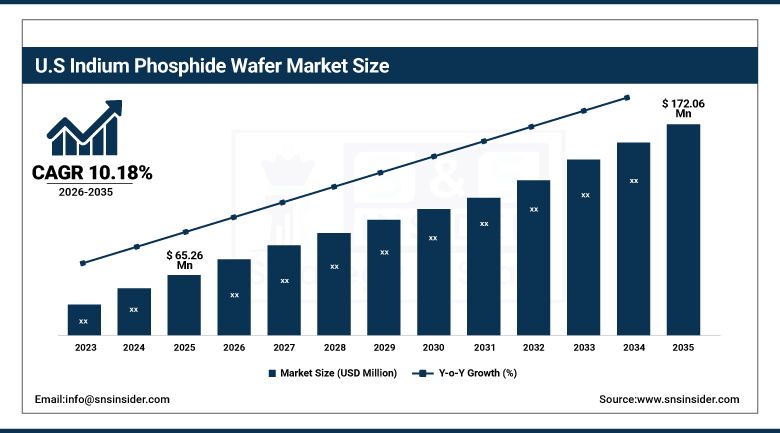

U.S. Indium Phosphide Wafer Market Size Outlook

The U.S. indium phosphide wafer market was valued at approximately USD 65.26 Million in 2025 and is expected to reach approximately USD 172.06 Million by 2035, growing at a CAGR of approximately 10.18%.

Due to the steady increase in the R&D as well as the investments, the United States of America InP Wafers Market is on an expansion path and will see continued growth thanks to the availability of semiconductor manufacturing plants, which help develop innovative devices based on the use of InP for applications such as telecommunication, AI, and photonics. Due to the continuous advancements being made in quantum computing and high-performance computing, the demand for high quality InP Wafers remains strong in the country.

Ortel's C-Band InP laser diode wafer production technology transition for Photonics Foundries was performed in January 2025 from Emcore to the Canadian Photonics Fabrication Facility to expand capacity and ensure continuity of supply. This is following the acquisition of EMCORE's optical core technology segment by HieFo Corporation, involving an InP wafer fabrication facility in North America, and the participation of HieFo Corporation at the LD Micro Main Event in October 2024 that highlights its importance in AI and data centers' connectivity using InP photonic components.

Indium Phosphide Wafer Market Segment Analysis

-

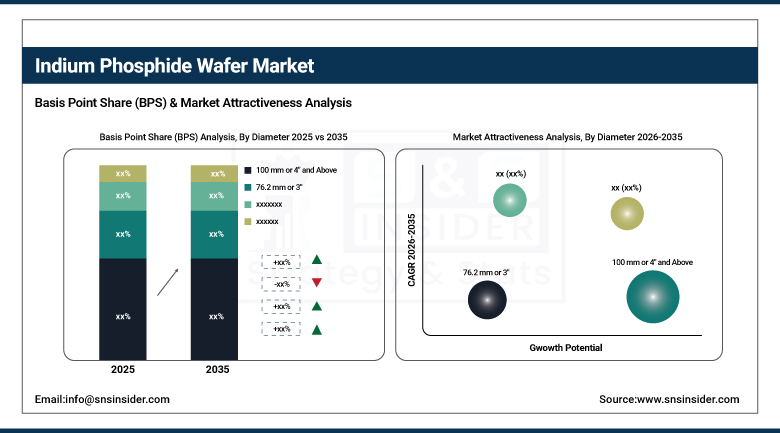

By Diameter, the 100 mm (4 inch) and above segment dominated the indium phosphide wafer market with more than 56% value share in 2025, while the 76.2 mm (3 inch) segment is the fastest growing.

-

By Wafer Doping Type, the N-type (S / Sn-doped) segment dominated the indium phosphide wafer market with approximately 48.6% value share in 2025, while the semi-insulating (Fe-doped) segment is the fastest growing during the forecast period.

-

By Manufacturing Technology, the VGF-grown bulk wafers segment dominated the indium phosphide wafer market with around 51.8% value share in 2025, while the epitaxial InP-on-Si (Hybrid) segment is the fastest growing during the forecast period.

-

By End User, the telecommunications segment dominated the indium phosphide wafer market with approximately 44% share in 2025, while the consumer electronics segment is the fastest growing.

By Diameter, 100mm and above dominates, 3-inch grows fastest

Segment of 100 mm (4 inch) and above captured more than 56% of the market share in 2025 owing to increased application of high voltage optoelectronics such as lasers, photodetectors, and transmitters in telecommunication, data center, and artificial intelligence industries. Large wafer size not only allows higher number of devices to be processed on a single wafer but also increases the production efficiency.

The 76.2 mm (3-inch) segment is the fastest-growing diameter category, fueled by demand for smaller, lower-cost wafers that power applications including sensors, high-speed communications, and medical devices. These 3-inch wafers fill an important gap between price and performance in the development of high-end optoelectronic components supporting emerging technologies like 5G, automotive connectors, and IoT devices where cost sensitivity still matters.

By End User, telecommunications dominate, consumer electronics grows fastest

The telecommunication industry had a market share of about 44% in 2025 because of the rising demand for reliable and fast communication technologies due to the continued deployment of 5G technology across the globe and the start of developing 6G technology. InP wafers are required to make optoelectronic devices such as lasers, photodetectors, and transceivers for the development of optical communication systems.

Among the end users, consumer electronics is witnessing the highest growth due to increasing demands for energy-efficient and highly functional electronic gadgets with every launch of new mobile electronics, wearables, and smart home appliances. The optical components such as lasers and photodetectors produced using InP wafers constitute enabling technologies for consumer electronics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.0% |

|

Europe |

Germany |

24.0% |

|

Asia Pacific |

China |

41.0% |

|

Middle East & Africa |

UAE |

28.0% |

|

Latin America |

Brazil |

36.0% |

North America Indium Phosphide Wafer Market Insights

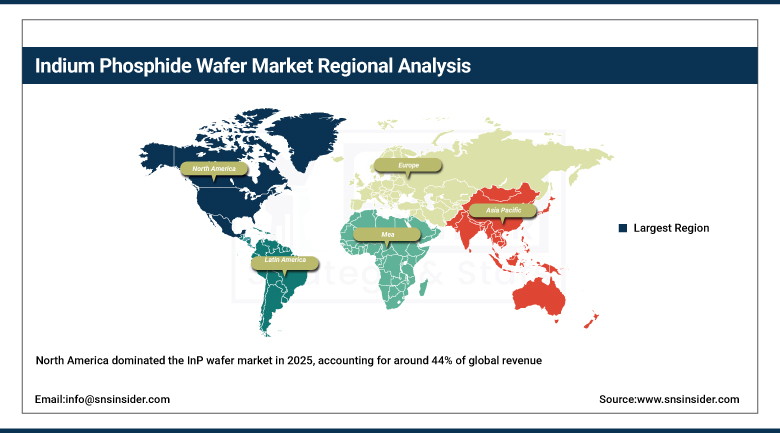

North America dominated the InP wafer market in 2025, accounting for around 44% of global revenue, due to the region's established semiconductor manufacturing ecosystem and a broad network of research centers, especially across the United States. This advantage is due to the high concentration of semiconductor fabrication facilities within the U.S., which help generate innovations in InP-based devices used in fields like telecommunications, AI, and photonics.

The investments being made in advanced technologies such as quantum computing and high performance computing have led to a sustained need for good quality InP wafers. The expansion of the Texas manufacturing facility by Coherent, through federal and state semiconductor incentives, clearly shows the huge amount of capital investment being made in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Indium Phosphide Wafer Market Insights

Europe maintains a moderate but steady growth position in the InP wafer market, supported by its strong foundation in semiconductor research and advanced technologies. Photonic, telecommunication, and data centers utilizing InP devices are seen with considerable investments in the region, where the key nations with expertise in development and processing of optoelectronic technology include Germany, UK, and France.

As more fabrication and research facilities are established, the continent has been making a concerted effort to decrease dependence on outside suppliers through improvement of local chip production capacity. The initiatives by the government to establish a robust semiconductor industry have helped bolster the region’s position despite being less competitive compared to the rapidly growing Asia Pacific market.

Asia Pacific Indium Phosphide Wafer Market Insights

Asia Pacific is projected to be the fastest-growing region in the InP wafer market, with a CAGR of about 14.66% through 2035, driven by increasing investment in 5G infrastructure, expansion of data center networks, and growing consumer electronics production across China, Vietnam, Japan, South Korea, and India. China dominates regional demand, supported by large-scale semiconductor manufacturing investments and robust government backing through policies including Made in China 2025.

A growing number of telecommunications companies across the region, paired with well-established supply chains, favorable government initiatives, and the presence of key semiconductor players adopting InP-based solutions, continues to contribute to regional market growth. Fast-growing telecommunications and consumer electronics industries across the broader region are expected to keep Asia Pacific ahead of other markets in percentage growth terms.

MEA & Latin America Indium Phosphide Wafer Market Insights

The Middle East and Africa InP wafer market remains small compared to other regions but is likely to see steady growth, driven by rising investment in telecommunications, data centers, and emerging technologies. The UAE and Saudi Arabia have been gradually becoming more attuned to sophisticated technologies, and are seeking to construct state-of-the-art infrastructure in terms of both data center and optical network applications.

Latin America is experiencing steady increase in InP wafer demands, though still with less optical communications and AI applications compared to other parts of the world. It is led by Brazil, due to its expanding investments in telecommunications infrastructure, as well as Mexico through its manufacturing capacity supplying to North America.

Market Dynamics

Growth Drivers: Record-breaking solar cell efficiency driving new InP demand

With an increasing demand for efficient solar cells, the special nature of InP makes it an excellent choice for incorporation into future photovoltaics. The capacity of InP to allow high electron mobility and a direct bandgap qualifies it as a significant material in the development of advanced multi-junction solar cells.

A recent breakthrough in silicon solar cell technology involved achieving an efficiency of 36.1% for a multi-junction silicon-based solar cell that uses GaInP and GaAs layers in conjunction with InP. This breakthrough underscores the application of InP in tandem with other materials in order to enhance the efficiency of solar cells.

Restraints: Resistance to transitioning from silicon-based systems

Several sectors, including telecommunication companies and data centers, still rely extensively on systems made from silicon. The cost associated with changing to InP technology is very high because it involves developing a new system and training staff members, and hence organizations may shy away from making this change because of the cost implication.

This leads to firms having to balance the short-term difficulty of transition costs versus the efficiency gains to be achieved from implementing InP-based devices. Resistance to change can impede the implementation of InP-based technology despite its performance advantages being known, especially by firms that have a lot of investments in silicon technology.

Opportunities: Scaling to 6-inch wafers unlocking new market potential

The market for InP wafers is undergoing an era of transformation, with the emergence of the first-ever large-scale 6-inch InP wafer production line at Coherent becoming a significant game-changer in the realm of wafer production capacity. This increase in wafer size makes way for better productivity, higher yields, and improved efficiency amid increasing demands for AI-based transceivers, coherent optical communications, and 6G wireless network.

The technology leads to an increase in device density per wafer by up to fourfold, thus ensuring savings of more than 60% in terms of die costs, and opening up considerable business potential for future applications such as 200G/400G electro-absorption modulated lasers, high-speed photodetectors, and Mach-Zehnder modulators.

Recent Developments:

-

2026: Coherent Corp. expanded its indium phosphide epitaxial wafer production capacity to support increasing demand for AI-driven optical interconnects and high-speed data center applications.

-

2026: IQE plc introduced advanced indium phosphide epitaxial wafer technologies optimized for next-generation coherent optical communications and 800G/1.6T transceiver applications.

-

2026: Sumitomo Electric Industries, Ltd. increased investment in compound semiconductor manufacturing to strengthen the supply of indium phosphide substrates for optical communication and photonic integrated circuits.

-

2026: AXT, Inc. expanded production of high-purity indium phosphide substrates to meet growing demand from 5G infrastructure, photonics, and advanced semiconductor device manufacturers.

Indium Phosphide Wafer Companies are:

-

AXT, Inc.

-

IntelliEPI, Inc.

-

Wafer Technology Ltd.

-

JX Advanced Metals Corporation

-

PAM-XIAMEN

-

Beijing JiYa Semiconductor Material Co., Ltd

-

IQE plc

-

Freiberger Compound Materials GmbH

-

Landmark Optoelectronics Corporation

-

Hebei Synlight Crystal Co., Ltd.

-

Yunnan Germanium Co., Ltd.

-

WaferPro LLC

-

Xiamen Powerway Advanced Material Co., Ltd.

-

Visual Photonics Epitaxy Co., Ltd. (VPEC)

-

WIN Semiconductors Corp.

-

Advanced Wireless Semiconductor Company (AWSC)

-

Intelligent Epitaxy Technology, Inc.

-

II-VI Singapore Pte. Ltd.

Indium Phosphide Wafer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 202.21 Million |

| Market Size by 2035 | USD 679.76 Million |

| CAGR | CAGR of 12.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Diameter (50.8 mm or 2 Inch, 76.2 mm or 3 Inch, 100 mm or 4 Inch and Above) • By Wafer Doping Type (Undoped Conductive, N-Type (S / Sn-doped), P-Type (Zn-doped), Semi-insulating (Fe-doped)) • By Manufacturing Technology (VGF-grown Bulk Wafers, LEC/tCZ-grown Bulk Wafers, Epitaxial InP-on-Si (Hybrid), MBE/MOCVD Epi-ready Substrates) • By End User (Consumer Electronics, Telecommunications, Medical, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sumitomo Electric Industries, Ltd., AXT, Inc., IntelliEPI, Inc., Wafer Technology Ltd., JX Advanced Metals Corporation, PAM-XIAMEN, Beijing JiYa Semiconductor Material Co., Ltd., Coherent Corp., IQE plc, Freiberger Compound Materials GmbH, Landmark Optoelectronics Corporation, Hebei Synlight Crystal Co., Ltd., Yunnan Germanium Co., Ltd., WaferPro LLC, Xiamen Powerway Advanced Material Co., Ltd., Visual Photonics Epitaxy Co., Ltd. (VPEC), WIN Semiconductors Corp., Advanced Wireless Semiconductor Company (AWSC), Intelligent Epitaxy Technology, Inc., II-VI Singapore Pte. Ltd. |

Frequently Asked Questions

The 100 mm (4 Inch) and Above segment dominated with more than 56% value share in 2025.

North America dominated the Indium Phosphide Wafer Market in 2025 with approximately 44% market share.

Get in Touch