Instrument Transformer Market Report Scope & Overview:

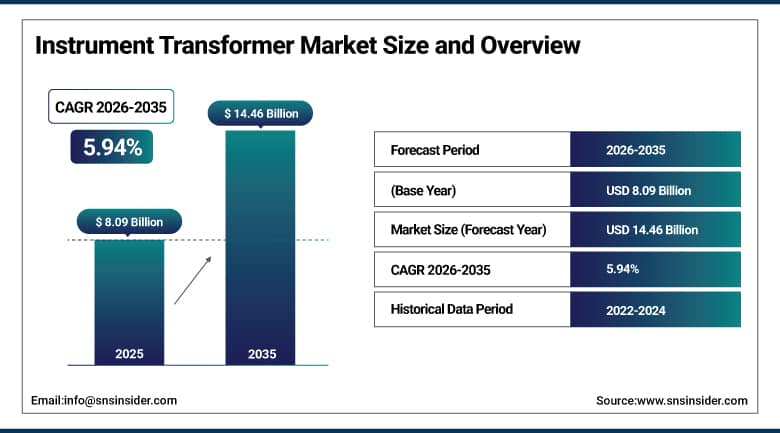

The Instrument Transformer Market was valued at USD 8.09 billion in 2025 and is expected to reach USD 14.46 billion by 2035, growing at a CAGR of 5.94% from 2026-2035.

The growth of the Instrument Transformer Market is being fueled by the increased development of power transmission and distribution networks, rising demand for electricity, and grid modernization efforts. The increasing penetration of renewable energy sources is increasing the demand for precise measuring and protecting equipment. Moreover, developments in smart grids, digital substations, and infrastructure upgrades within utilities and industrial organizations are contributing towards driving market growth.

The U.S. Department of Energy's Grid Deployment Office has committed USD 20 billion from the Bipartisan Infrastructure Law for transmission infrastructure projects that include substation upgrades where instrument transformers are essential components. The International Energy Agency projects global electricity grid investment must reach USD 800 billion annually by 2030 to support the energy transition a level of investment that sustains growing demand for all substation equipment including instrument transformers.

Instrument Transformer Market Size and Forecast

-

Market Size in 2025: USD 8.09 Billion

-

Market Size by 2035: USD 14.46 Billion

-

CAGR: 5.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Instrument Transformer Market - Request Free Sample Report

Instrument Transformer Market Trends

-

Rising demand for accurate measurement and protection in power transmission and distribution is driving the instrument transformer market.

-

Growing adoption across utilities, industrial facilities, and renewable energy projects is boosting market growth.

-

Expansion of smart grids and grid modernization initiatives is fueling deployment.

-

Increasing focus on voltage and current monitoring, fault detection, and system reliability is shaping adoption trends.

-

Advancements in digital and optical instrument transformers are enhancing precision and safety.

-

Rising investments in high-voltage infrastructure and substation automation are supporting market expansion.

-

Collaborations between transformer manufacturers, utilities, and EPC contractors are accelerating innovation and global adoption.

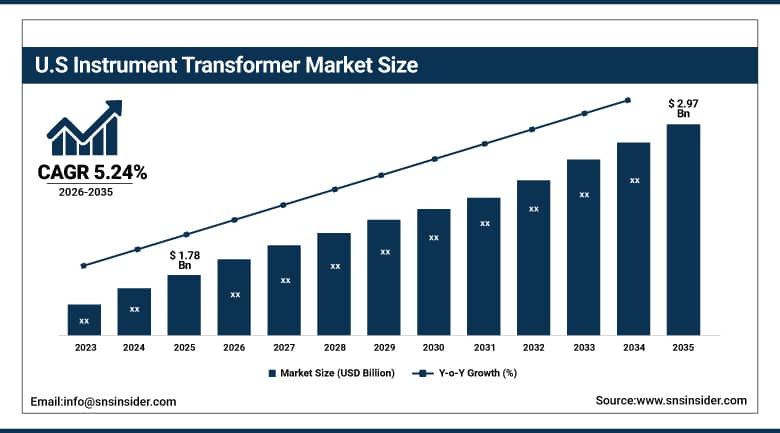

U.S. Instrument Transformer Market was valued at USD 1.78 billion in 2025 and is expected to reach USD 2.97 billion by 2035, growing at a CAGR of 5.24% from 2026-2035.

The U.S. Instrument Transformer Market is propelled by grid modernization initiatives, upgrades in existing infrastructures, and growing electricity demand. Investments made in renewable energy deployment and smart grid systems have fueled adoption rates. Transmission system expansion and reliable electricity supply considerations are additional factors contributing to the growth of the market.

The North American Electric Reliability Corporation (NERC) requires instrument transformer accuracy and calibration standards across the bulk electric system to ensure protection and metering reliability. The U.S. Federal Energy Regulatory Commission's Order 2023 on large generator interconnection is accelerating transmission system upgrades that include new substation construction requiring complete instrument transformer populations.

Instrument Transformer Market Segment Analysis

-

By Type, Current segment dominated the Instrument Transformer Market in 2025 with 58% share; Potential segment fastest growing (CAGR).

-

By Dielectric Medium, SF6 segment dominated the Instrument Transformer Market in 2025 with 46% share; Solid segment fastest growing (CAGR).

-

By Enclosure, Outdoor segment dominated the Instrument Transformer Market in 2025 with 62% share; Indoor segment fastest growing (CAGR).

-

By Voltage, High Voltage Transmission segment dominated the Instrument Transformer Market in 2025 with 34% share; Ultra-High Voltage Transmission segment fastest growing (CAGR).

-

By Application, Transformer & Circuit Breaker Busing segment dominated the Instrument Transformer Market in 2025 with 39% share; Relaying, Metering & Protection segment fastest growing (CAGR).

-

By End Use, Power Utilities segment dominated the Instrument Transformer Market in 2025 with 55% share; Railway & Metros segment fastest growing (CAGR).

By Type, Current segment dominates the Instrument Transformer Market, Potential segment expected to grow fastest.

Current segment captured the highest market share of around 58% in the Instrument Transformer Market due to its extensive use for current measurement, protection, and control purposes in transmission and distribution grids in 2025. Due to its significance in providing grid stability and monitoring functions, the demand for this segment will stay consistent among various utility and industrial companies.

Potential segment is forecasted to record the fastest-growing CAGR from 2026-2035 owing to increasing need for measuring voltage in HV grids, advancements in grid modernization programs, and growth of renewable energy sources. With the increased deployment of smart grids, digital substations, and other advanced monitoring technologies, the uptake of potential segment will be faster.

By Dielectric Medium, SF6 segment dominates the Instrument Transformer Market, Solid segment expected to grow fastest.

The SF6 segment accounted for the largest share in the global Instrument Transformer Market with an approximate market share of 46% during 2025 due to its superior dielectric nature, higher insulation level, and reliability. The ability of the SF6 segment to offer effective performance along with smaller sized equipment design has been contributing to its popularity in substations and transmission grids.

The solid segment will record the highest growth rate with a CAGR in the period 2026-2035. It will be attributed to the growing concern regarding the environmental sustainability of various products in substations. The advantages such as safety, lower maintenance needs, and higher durability of the solid segment have been driving its popularity in recent times.

By Enclosure, Outdoor segment dominates the Instrument Transformer Market, Indoor segment expected to grow fastest.

Outdoor segment captured the largest share of about 62% of the total market revenue in the year 2025 due to the operation of most of the power transmission and distribution systems being performed outdoors, thus making it essential to invest in weatherproof and sturdy instruments transformers to avoid any malfunction in performance due to the changing environmental conditions.

The indoor segment is anticipated to be the fastest-growing segment in terms of CAGR from 2026 to 2035 owing to the installation of compact substations and switchgear systems in residential complexes and other industries. The rising requirement for effective power transmission systems is encouraging players to install their substations indoors as it ensures maximum operational efficiency and provides a safer working environment for employees.

By Voltage, High Voltage Transmission segment dominates the Instrument Transformer Market, Ultra-High Voltage Transmission segment expected to grow fastest.

The High Voltage Transmission category held the major market share of nearly 34% in the year 2025 based on the highest revenue generated owing to the importance of the category for long-distance transmission of electrical energy. The requirement for proper measurement, monitoring, and control of electricity at high voltages ensures that there is no loss of power in the process, thus making such systems important for the global economy.

Ultra-High Voltage Transmission category is anticipated to expand at the fastest rate of growth from 2026-2035 due to increased investment in long distance power transmission infrastructure and interconnection of grids in different regions. The growing demand for electricity coupled with increased generation from renewable energy sources is contributing to the growth of this particular segment.

By Application, Transformer & Circuit Breaker Busing segment dominates the Instrument Transformer Market, Relaying, Metering & Protection segment expected to grow fastest.

Transformer & Circuit Breaker Busing segment held the largest market share, generating approximately 39% of revenue in the Instrument Transformer Market in 2025, due to its critical role in ensuring smooth current and voltage transfer in substations and switchgear facilities. The segment's extensive application in the power infrastructure network facilitates the efficient functioning of these systems.

The Relaying, Metering & Protection segment is projected to exhibit the fastest CAGR between 2026 and 2035, owing to the rising implementation of digital substations and smart grids. The growing importance of monitoring and automation techniques is creating a high demand for accurate measurement instruments in power grids, contributing significantly to their reliability and energy management processes.

By End Use, Power Utilities segment dominates the Instrument Transformer Market, Railway & Metros segment expected to grow fastest.

The Power Utilities accounted for the major market share revenue of around 55% in 2025 owing to the fact that utilities are the key players in the operation of transmission & distribution grids that require the installation of instrument transformers. Growing efforts toward the expansion, upgrading, and maintenance of the power grid are fueling high growth in instrument transformer demand.

The Railways & Metros segment will witness significant growth during 2026-2035 on account of the fast-growing electrification of railway lines and development of urban rail systems. Increasing investment in metro rails and high-speed railways will drive the growth of instrument transformer demand due to their necessity in the power distribution system.

Instrument Transformer Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

52% |

|

North America |

United States |

85% |

|

Europe |

Germany |

26% |

|

Middle East & Africa |

Saudi Arabia |

42% |

|

Latin America |

Brazil |

48% |

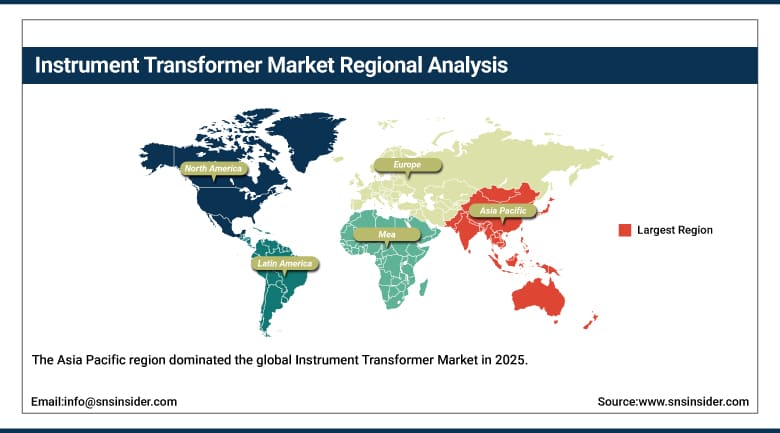

Asia Pacific Instrument Transformer Market Insights

The Asia Pacific region dominated the global Instrument Transformer Market in 2025 in terms of revenue share of around 42% due to widespread expansion of grids in China and India, fast industrialization in the southeast Asia region, and renewable energy incorporation. There is an increase in large investment in ultra-high voltage grids, which is increasing the demand for high-quality instrument transformers. Furthermore, upgrading of the substation infrastructure and enhancing the efficiency of the grid are supporting the market's expansion.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Instrument Transformer Market Insights

North America Power Transformer Market is distinguished by significant spending in terms of upgrading the electric grid and replacing old electrical infrastructure. Digital substation technology and improved monitoring systems have gained more traction due to the rising trend among utilities toward making the electric grid reliable and efficient. Another major factor contributing to market growth is the increasing adoption of renewable energy resources.

Europe Instrument Transformer Market Insights

Europe Instrument Transformer Market is propelled by the shift towards sustainable energy systems along with the rising use of renewable energy sources like wind energy and solar energy. The development of old grids and adoption of smart grids is among the main concerns for different countries. Moreover, effective regulatory policies emphasizing energy efficiency and sustainability have been encouraging the use of instrument transformers. Other factors like cross-border electricity transmission systems are also helping in sustaining demand for instrument transformers.

Middle East & Africa and Latin America Instrument Transformer Market Insights

The Middle East & Africa and Latin America Instrument Transformer Market is growing at a moderate rate owing to the rapid increase in the installation of power infrastructure, growing demand for electricity, and rising investment in power transmission and distribution systems. The focus of countries within these regions is on the expansion of power grids, rural electrification programs, and the incorporation of renewable energy sources. Moreover, the growth of industries, urbanization trends, and the modernization of substations are further driving demand.

Instrument Transformer Market Growth Drivers:

-

Grid modernization investment and renewable energy integration driving sustained global instrument transformer market growth

The growth of the instrument transformers industry is directly correlated with the rate at which investments into building up and upgrading electrical grids happen worldwide, and those investments are presently at all-time highs because of structural and persistent reasons. The shift towards cleaner energy resources demands not only additional capacity to transport the generated power to consumption nodes, which are located quite far away from each other, but also the installation of substations, where the power flows can be managed due to the two-way nature of distributed power generation. The digital substation transformation projects are generating an additional need for instrument transformers as utilities update their protection and metering systems from electromechanical to digital ones.

The IEA's Net Zero by 2050 scenario requires tripling of global electricity grid investment from current levels, implying average annual grid spending exceeding USD 800 billion by 2030. The European Commission's REPowerEU plan has allocated EUR 86 billion to grid modernization across EU member states specifically to support renewable energy integration and cross-border power trading.

Instrument Transformer Market Restraints:

-

Digital substation technology transition costs and supply chain constraints limiting instrument transformer market deployment pace

The shift to using digital instrument transformers instead of the traditional electromagnetic types, although technologically more advanced, faces issues related to compatibility with existing protection relay and measuring equipment that were developed for output of the analog types. For utilities seeking to implement the use of digital instrument transformers in their IEC 61850-9 process bus, an additional step involving the upgrade of the protection relay and metering system would be required at the same time, thus becoming a case of mutual investment and resulting in increased project costs. Lead times of instrument transformers have been affected due to shortages of electrical steel, copper, and specialty insulation materials.

Instrument Transformer Market Opportunities:

-

Digital substation adoption and smart grid investment creating significant instrument transformer market growth opportunities globally

The development of digital substation software constitutes the most lucrative prospect in terms of the application of premium instrument transformers. The substitution of oil-based electromagnetic instrument transformers through optical current transformers, electronic instrument transformers, and integrated digital measurement devices is the technological prerequisite for implementing the complete digital substation structure according to the IEC 61850-9 process bus standard. Notable examples of such protection devices are the ABB Relion line of relays, the Siemens SICAM ACS6080 series, and the high-end protection systems by GE.

Recent Developments:

-

2026: ABB launched its next-generation electronic instrument transformer series for 765kV UHV transmission applications, featuring optical current measurement and hybrid insulation technology that achieves 0.1% accuracy class performance at ultra-high voltage ratings while reducing weight by 35% compared to equivalent oil-filled designs.

-

2025: Siemens Energy introduced its SENTINAL digital instrument transformer with integrated condition monitoring capability, using embedded sensors to continuously monitor insulation condition, temperature, and vibration parameters and transmit health status via IEC 61850 communication to substation management systems.

-

2025: BHEL (Bharat Heavy Electricals Ltd.) received a major order from India's Power Grid Corporation for instrument transformers for the 765kV national grid expansion program, representing one of the largest single instrument transformer procurement orders in Indian power sector history and reflecting India's rapid UHV grid development pace.

Instrument Transformer Market Key Players

Some of the Instrument Transformer Market Companies

-

ABB Ltd.

-

Siemens AG

-

General Electric Company (GE Vernova)

-

Schneider Electric SE

-

Hitachi Energy Ltd.

-

Mitsubishi Electric Corporation

-

Toshiba Corporation

-

Arteche Group

-

Pfiffner Group

-

SEFAG AG

-

Prolec-GE Waukesha Inc.

-

RITZ Instrument Transformers GmbH

-

MESA Labs

-

Trench Group (Siemens Energy)

-

Bender Inc.

-

Ritz Messwandler GmbH

-

Koncar Instrument Transformers

-

TBEA Co. Ltd.

-

BHEL (Bharat Heavy Electricals Ltd.)

-

Nippon Chemi-Con Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.09 Billion |

| Market Size by 2035 | USD 14.46 Billion |

| CAGR | CAGR of 5.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Current, Potential, Combined) • By Dielectric Medium (Liquid, SF6, Solid) • By Enclosure (Indoor, Outdoor) • By Voltage (Distribution Voltage, Sub-transmission Voltage, High Voltage Transmission, Extra High Voltage Transmission, Ultra-High Voltage Transmission) • By Application (Transformer & Circuit Breaker Busing, Switchgear Assemblies, Relaying, Metering & Protection, Primary Metering Units) • By End Use (Power Utilities, Power Generation, Railway & Metros, Industries & OEM) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles |

ABB Ltd., Siemens AG, General Electric Company (GE Vernova), Schneider Electric SE, Hitachi Energy Ltd., Mitsubishi Electric Corporation, Toshiba Corporation, Arteche Group, Pfiffner Group, SEFAG AG, Prolec-GE Waukesha Inc., RITZ Instrument Transformers GmbH, MESA Labs, Trench Group (Siemens Energy), Bender Inc., Ritz Messwandler GmbH, Koncar Instrument Transformers, TBEA Co. Ltd., BHEL (Bharat Heavy Electricals Ltd.), Nippon Chemi-Con Corporation |

Frequently Asked Questions

Asia Pacific dominated the Instrument Transformer Market in 2025.

Power Utilities dominated with approximately 48.7% market share in 2025.

The Current Transformer segment dominated the Instrument Transformer Market in 2025.

The Instrument Transformer Market was valued at USD 8.09 billion in 2025.

The Instrument Transformer Market is expected to grow at a CAGR of 5.94% from 2026 to 2035.

Get in Touch