Interventional Cardiology Devices Market Report Scope & Overview:

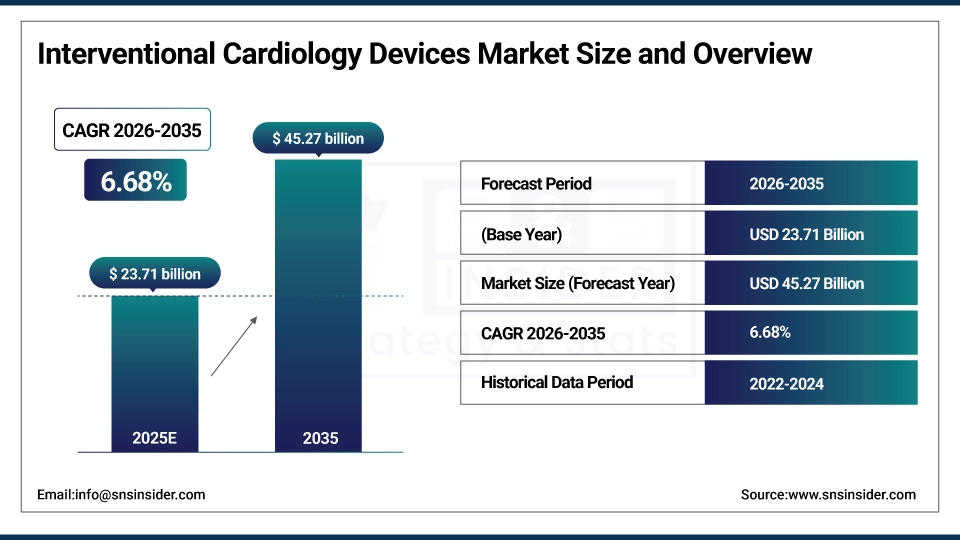

The Interventional Cardiology Devices Market Size was valued at USD 23.71 billion in 2025 and is expected to reach USD 45.27 billion by 2035, growing at a CAGR of 6.68% during 2026-2035.

The global Interventional Cardiology Devices Market is growing, as people age, the risk for developing cardiovascular diseases, including coronary artery disease, heart failure, and the aging process of the cardiovascular system, including stiffened arteries and the narrowing of blood vessels, also increases. Heart-related illnesses are particularly common in those aged 65 and older, making them ideal TAVR candidates. This has led to an increasing need for minimally invasive, catheter-based therapies with shorter recovery times and lower procedural risk.

For instance, in February 2025, according to the WHO, Cardiovascular diseases (CVDs) are the leading cause of death globally, taking an estimated 17.9 million lives each year.

Interventional Cardiology Devices Market Size and Forecast:

-

Market Size in 2025: USD 23.71 Billion

-

Market Size by 2035: USD 45.27 Billion

-

CAGR: 6.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Interventional Cardiology Devices Market - Request Free Sample Report

Key Interventional Cardiology Devices Market Trends

-

Growing adoption of minimally invasive PCI and peripheral interventions for faster recovery and reduced hospital stays.

-

Drug-eluting and bioresorbable stents dominate innovation, improving safety and long-term outcomes.

-

Embolic protection and atherectomy devices are increasingly used in complex and high-risk interventions.

-

Rising prevalence of CAD and PAD globally, especially in aging and diabetic populations, is fueling procedure volumes.

-

Expansion of cardiac cath labs in Asia-Pacific and Latin America to meet rising interventional cardiology demand.

-

Shift toward precision-guided, imaging-assisted, and robotic interventions for safer, more efficient procedures.

Interventional Cardiology Devices Market Report Highlights

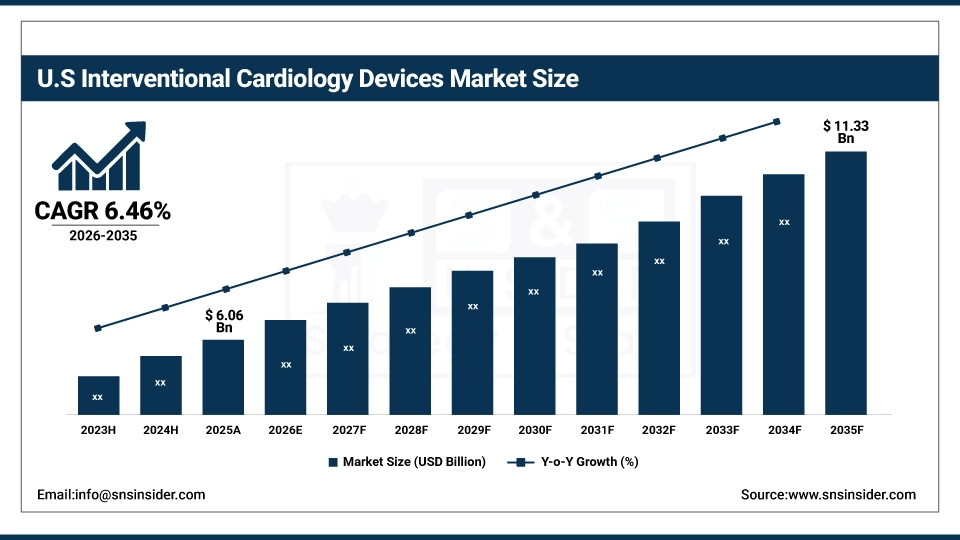

The U.S. interventional cardiology devices market size was valued at USD 6.06 billion in 2025 and is projected to reach USD 11.33 billion by 2035, growing at a CAGR of 6.46% over the analysis period 2026-2035. The US is the leading market in the global interventional cardiology devices market, with a large number of patients suffering from cardiovascular diseases and a huge demand for minimally invasive technologies in their treatment in the region. The presence of leading device manufacturers and ongoing R&D expenditures also contribute to the U.S. dominance, being able to sustain a high level of pace of innovation, high procedure volume, and market share.

Us image

Interventional cardiology devices market trends are attributed to escalating burden of cardiovascular diseases, growing utilization of minimally invasive and transcatheter cardiovascular procedures, rapid uptake of next-generation imaging technologies, and continuous technological advancements, underpinned by enhancement in global healthcare infrastructure and affirmative reimbursement policies.

Key Interventional Cardiology Devices Market Segment Analysis

-

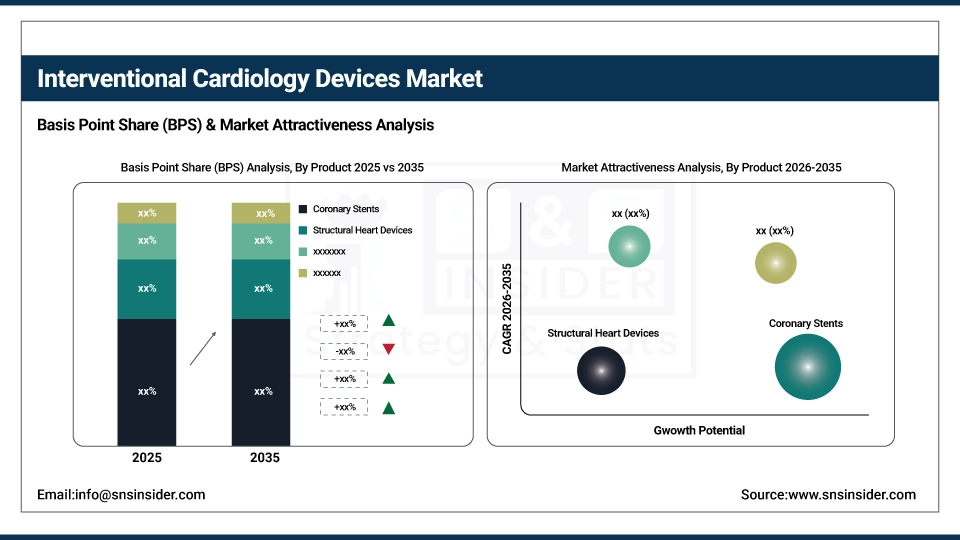

By Product, Coronary stents held the largest share of around 35.32% in 2025, and the structural heart devices segment is expected to register the highest growth with a CAGR of 7.41%.

-

By Procedure Type, the PCI segment dominated the market with approximately 55.76% share in 2025, while PVI is expected to register the highest growth with a CAGR of 7.33%.

-

By Technology, drug-eluting accounted for the leading share of nearly 60.52% in 2025, whereas biodegradable is expected to register the highest growth with a CAGR of 7.75%.

-

By End User, the Hospitals & ASCs segment led the market with about 60.22% share in 2025, and is forecasted to grow the fastest at a CAGR of 6.85%.

By Product, Coronary Stents Lead Market and Structural Heart Devices Register Fastest Growth

In 2025, the coronary stents segment held a demanding revenue of around 35.32% in the interventional cardiology devices market share and is expected to continue its dominance, owing to their large application in PCI, the great power of inhibiting restenosis, and the huge acceptance of drug-eluting stents. Increasing incidence of cardiovascular diseases, advancements in technology, and rising demand for minimally invasive procedures contribute to the dominance of this segment in the market. The structural heart devices segment is projected to experience the fastest CAGR growth of around 7.41%, due to increasing uptake of TAVR and MitraClip, growing aging-valve population, demand for less invasive modalities, and technological advancements enhancing patient outcomes and procedural safety.

By Procedure Type, Interventional Cardiology Dominates and Shows Rapid Growth Over the Forecast Period

The interventional cardiology devices industry was dominated by the percutaneous coronary intervention (PCI) segment with a revenue share of over 55.76% in 2025, driven by its efficacy for coronary artery disease, high global volumes, and high usage of stents and balloons. Growing cardiovascular load, inclination towards minimal invasive procedures, and ongoing device developments are among the key factors fuelling the dominance. On the peripheral vascular intervention (PVI) hand, it is anticipated to record the fastest CAGR of 7.33% during the forecast period (2026-2035), due to increasing peripheral artery disease population, diabetes, and geriatric population, increasing penetration of minimally invasive procedures, advanced stents, and improving healthcare facilities globally.

By Technology, Drug-Eluting Lead, Whereas It Registers the Fastest Growth

The drug-eluting segment led the interventional cardiology devices industry with the highest revenue market share of about 60.52% in 2025, owing to its demonstrable potential for lowering rates of restenosis and enhancing long-term results. Their successful use in the context of percutaneous coronary intervention (PCI), strong adoption, and ongoing development of drug-polymer combinations. The biodegradable segment is likely to register the fastest CAGR of approximately 7.75% over the forecast years 2026-2035, due to greater use of provisional scaffolding, bioresorbable material progress, and lower long-term complications, together with a growing clinical confidence in safer novelty temporary metallic stent alternatives in the field of interventional cardiology.

By End User, Hospitals & ASCs Lead, and Grow the Fastest

The hospitals & clinics segment of the interventional cardiology devices industry was estimated as the highest earning segment with a revenue share of around 60.22% in 2025, owing to developed healthcare infrastructure, trained cardiologists, a large number of procedures, a favorable reimbursement scenario, and the adoption of integrated imaging devices to expedite patient care and lead the market. And projected to attain the highest CAGR of approximately 6.85% throughout the forecast period (2026-2035), owing to the growing number of outpatient cardiac procedures, growing adoption of ASCs, introduction of minimally invasive procedures, and the rising number of cath lab installations and increasing healthcare expenditure in emerging countries.

North America Interventional Cardiology Devices Market Insights

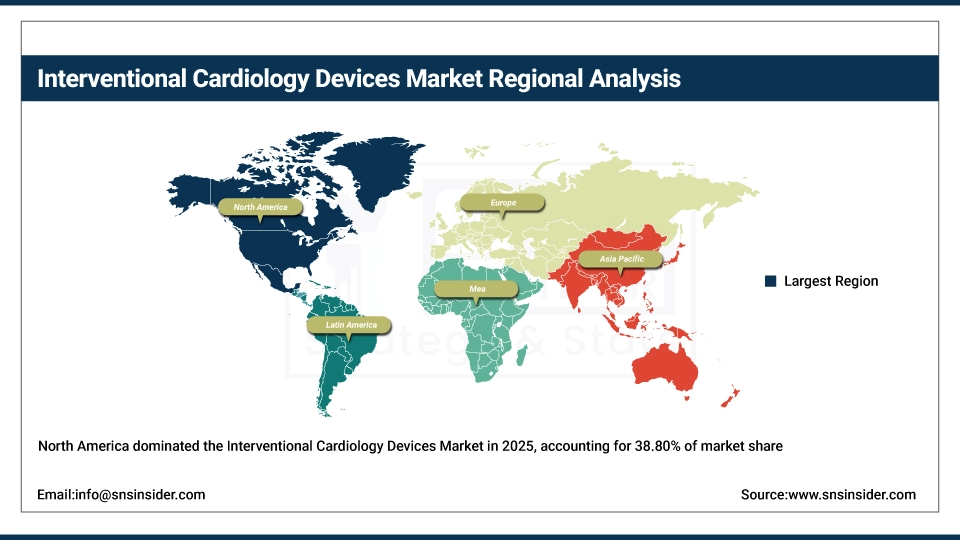

North America accounted for the highest revenue share of approximately 38.80% in 2025 of the interventional cardiology devices Market, owing to the well-established medical facilities, high incidence of CVDs, and heavy uptake of non-invasive techniques, comprising connections among PCI and TAVR. The presence of top global device manufacturers, huge R&D investments, and robust reimbursement systems will add to the market leadership. Furthermore, the strong awareness, presence of experienced cardiologists, and easy accessibility to advanced cardiac centers have further ensured that North America continues to lead the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Interventional Cardiology Devices Market Insights

The Asia Pacific segment is projected to witness the fastest CAGR of 7.07% during the forecast period of 202562035, as there is an increasing prevalence of cardiovascular diseases, a geriatric population, and the incidence of diabetes and obesity. Increased healthcare infrastructure, government initiatives, and growing awareness regarding minimally invasive cardiac procedures further boost the adoption. Moreover, the growing spending by global device manufacturers, favourable reimbursement policies, and rapid expansion of catheterization labs in countries including China, India, and Japan further bolster the regional outlook.

Europe Interventional Cardiology Devices Market Insights

The Europe Interventional Cardiology Devices Market is growing steadily due to the increasing incidence of cardiovascular diseases, the growing geriatric population, and high penetration of minimally invasive procedures, including PCI and structural heart procedures. The market is driven by robust healthcare infrastructure, positive reimbursement policies, and established R&D efforts by key device manufacturers. Moreover, increased awareness, a rising number of cardiac centers, and early adoption of advanced technologies, including bioresorbable and drug-eluting stents, are also contributing to the large market share of Europe.

Latin America (LATAM) and Middle East & Africa (MEA) Interventional Cardiology Devices Market Insights

The Middle East & Africa and Latin America markets are also increasing, owing to a higher risk of cardiovascular diseases, favorable government healthcare reforms, along with a growing number of low- and middle-income countries (LMICs) with a growing number of cardiac centers in the regions. The Middle East & Africa are a growing market, with a healthy cardiovascular disease patient pool, healthcare investments, a rise in dedicated cardiac centers, and greater use of PCI, TAVR, and other interventional devices.

Interventional Cardiology Devices Market Growth Drivers:

-

Rising Prevalence of Cardiovascular Diseases is Driving the Interventional Cardiology Devices Market Growth

Rise in awareness of animal health is also one of the key factors for the growth of the Interventional Cardiology Devices Market. Growth in pet owners’ concern regarding healthy nutrition, weight monitoring, and pets' well-being is driving the demand for automated feeders. With accurate portion control, purring schedules, and any monitoring, they are designed to allow owners to take care of their pets' health and obesity while also sharing their diets.

For instance, in April 2025, the increasing elderly population globally, especially in North America, Europe, and the Asia-Pacific, drives higher demand for interventional cardiology procedures.

Interventional Cardiology Devices Market Restraints:

-

Stringent Regulatory Approvals are Hampering the Interventional Cardiology Devices Market Growth

The Interventional Cardiology Devices Market is heavily dependent on the regularity clearance of the products, and due to its complex and time-consuming process across countries, the market faces some challenges to handle. For devices including drug-eluting stents (DES), bioresorbable scaffolds, and structural heart implants, extensive clinical trials and regulatory approval by the FDA, EMA, PMDA, among others, are required, which may cause long launch waits, high development costs, and market unavailability on time.

Interventional Cardiology Devices Market Opportunities:

-

Emerging Markets Expansion is a Significant Growth Opportunity in the Interventional Cardiology Devices Market

The use of AI and machine learning in Interventional Cardiology Devices offers major potential, improving diagnostic accuracy, predictive analytics, and workflow. The firms’ institutions and care centers will gain an edge over competitors when they choose AI-driven imaging, as control over the Interventional Cardiology Devices Market affects profit margins and hastens technology upgrades globally.

For instance, in March 2025, rising cardiovascular disease and expanding cardiac centers in the Asia-Pacific are driving increased adoption of interventional cardiology procedures.

Competitive Landscape for Interventional Cardiology Devices Market:

Boston Scientific Corporation (est. 1979, Massachusetts, USA): A global leader in coronary and peripheral stents, balloons, and structural heart devices, with a focus on innovative solutions for minimally invasive heart and vascular interventions.

-

In February 2025, Boston Scientific launched the SYNERGY XD drug-eluting stent in Europe and expanded TAVR/MitraClip structural heart devices in the Asia-Pacific, enhancing coronary and minimally invasive procedure outcomes.

Medtronic plc (est. 1949, USA, Minnesota) Multi-national medical device company that designs, manufactures, and sells coronary and peripheral stents, guidewires, and catheter systems for endovascular therapy, and other cardiovascular devices, including heart valve systems.

-

In March 2025, Medtronic introduced the IN. PACT Admiral drug-coated balloon in the U.S. and expanded robotic-assisted PCI systems across Europe and Latin America for precise cardiovascular interventions.

Abbott Laboratories (est. 1888, Illinois, USA) Integrated healthcare company, focused on drug-eluting stents, vascular closure systems, and diagnostics, with leadership positions in interventional cardiology, and a commitment to continued innovation in the market.

-

In January 2025, Abbott Laboratories received FDA approval for the XIENCE Skypoint DES for complex coronary lesions and launched new coronary and peripheral devices in emerging markets, improving global interventional cardiology access.

Interventional Cardiology Devices Market Key Players:

Some of the Interventional Cardiology Devices Market Companies

-

Boston Scientific Corporation

-

Medtronic plc

-

Abbott Laboratories

-

Edwards Lifesciences Corporation

-

Terumo Corporation

-

Siemens Healthineers

-

Philips Healthcare

-

Johnson & Johnson

-

Cook Medical

-

Becton Dickinson

-

Cardinal Health

-

MicroPort Scientific Corporation

-

LivaNova PLC

-

Merit Medical Systems, Inc.

-

Sorin Group

-

ABIOMED, Inc.

-

Terumo Interventional Systems

-

Claret Medical, Inc.

-

Neovasc Inc.

-

Boston Scientific

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.71 billion |

| Market Size by 2035 | USD 45.27 billion |

| CAGR | CAGR of 6.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

• By Product (Coronary Stents, Structural Heart Devices, Angioplasty Balloons, Catheters, Embolic Protection Devices, PTCA Balloon Catheters, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Edwards Lifesciences Corporation, Terumo Corporation, Siemens Healthineers, Philips Healthcare, Johnson & Johnson, Cook Medical, Becton Dickinson, Cardinal Health, MicroPort Scientific Corporation, LivaNova PLC, Merit Medical Systems, Inc., Sorin Group, Terumo Interventional Systems, Claret Medical, Inc., Neovasc Inc., Boston Scientific and other players. |

Frequently Asked Questions

North America dominated the Interventional Cardiology Devices Market in 2025.

The Coronary Stents segment dominated the Interventional Cardiology Devices Market in 2025.

Rise in awareness of animal health is also one of the key factors for the growth of the Interventional Cardiology Devices Market.

The Interventional Cardiology Devices Market size was USD 23.71 billion in 2025 and is expected to reach USD 45.27 billion by 2035.

The Interventional Cardiology Devices Market is expected to grow at a CAGR of 6.68% from 2026-2035.

Get in Touch