Flexible Endoscopes Market Report Scope & Overview:

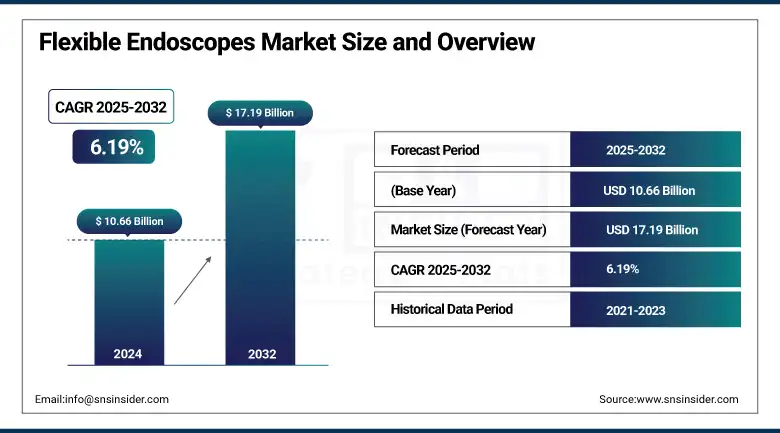

The Flexible Endoscopes Market size was valued at USD 10.66 billion in 2024 and is expected to reach USD 17.19 billion by 2032, growing at a CAGR of 6.19% over the forecast period of 2025-2032.

The global flexible endoscopes market is forecasted to witness a steady increase in revenue as the demand for innovative techniques for minimally invasive diagnostic and surgical procedures for gastrointestinal, respiratory, and urological applications rises. Market growth is also being driven by the developments in imaging technology, rising preference toward outpatient procedures, and increasing awareness of early disease detection. In a related development, the transition amongst healthcare providers for single-use/disposable endoscopes, to minimize the risk of cross-contamination, coupled with the increasing number of endoscopic surgeries globally, is becoming a key driving force for innovation and adoption in developed and emerging healthcare environments.

To Get more information On Flexible Endoscopes Market - Request Free Sample Report

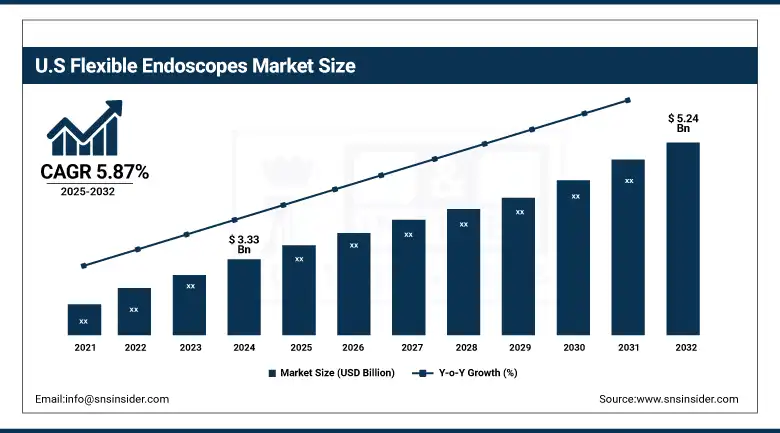

The U.S. flexible endoscopes market size was valued at USD 3.33 billion in 2024 and is expected to reach USD 5.24 billion by 2032, growing at a CAGR of 5.87% over the forecast period of 2025-2032.

North America, driven by a highly advanced healthcare infrastructure, the presence of major market players, and the early adoption of minimally invasive procedures, has cemented the position of the U.S. as the most lucrative market. Coupled with high procedural volumes (gastrointestinal and pulmonary endoscopy) and favorable reimbursement policies, this entrenched position is further indicated by the large market in the U.S.

Flexible Endoscopes Market Dynamics:

Drivers:

- Increasing Incidences of Chronic Gastrointestinal and Respiratory Conditions are Accelerating the Market Growth

Chronic diseases, such as colorectal cancer, inflammatory bowel disease (IBD), ulcers, and chronic obstructive pulmonary disease (COPD) continue to gain a global footprint. These conditions frequently demand that a diagnostic procedure be performed quickly and accurately, a context in which flexible endoscopes are essential. Flexible endoscopes, as in the case of colonoscopies, are crucial components of colorectal cancer screening programs, for example. Likewise, bronchoscopes serve for the detection and monitoring of lung disorders. With the prevalence of these disorders increasing, particularly among aging patient populations, the need for flexible endoscopic procedures is expected to grow significantly.

For instance, according to NCBI, Chronic obstructive pulmonary disease (COPD) is one of the most common chronic respiratory diseases. The gold standard for its diagnosis is less than a post-bronchodilator forced expiratory volume in one second to forced vital capacity (FEV1/FVC) ratio of 70%. Overall, COPD affects about 544.9 million people globally and has remained the third leading cause of death since the earliest years of record-keeping, accounting for about 7% of all global deaths (GBD Chronic Respiratory Disease Collaborators, 2020).

- Improvements in Endoscopic Services are Propelling the Market Growth

Advances in flexible endoscopy have significantly improved the precision and effectiveness of these diagnoses and procedures. HD, NBI, and the incorporation of AI-enabled systems enhance mucosal visualization and detection of abnormalities. Furthermore, with the miniaturization of components and enhanced maneuverability, procedures are also less invasive and more comfortable for patients. Such technological improvements have been fueling adoption across primary care settings, due to their role in facilitating earlier detection, enhanced accuracy of diagnoses, and improved clinical outcomes.

In March 2024, Medtronic launched the HemoClear system, a new flexible endoscope for the diagnosis of gastrointestinal bleeding. It applies AI to real-time hemorrhage detection and tracking, with the goal of improving procedural speed and patient safety. This product is one of a wave of AI-enabled endoscopic care aimed at enhancing outcomes.

Restraints:

- Burden of Expenses on Endoscopic Tools and Treatments is Restraining the Market from Growing

The high cost of purchase and maintenance of flexible endoscopes is one of the major restraints of the flexible endoscopes market. Sophisticated, flexible endoscopes, particularly ones that use little to no consumables, high-definition imaging, and are integrated with robotic control and AI-enhanced diagnostics, can be cost-prohibitive. In addition to these costs, hospitals and clinics pay for regular upkeep reprocessing systems (for sterilization), and replacement elements. On top of that, training employees on how to use this complex equipment in a safe manner also brings with it its own significant costs.

For smaller health facilities and centers in upper-middle and lower-income countries, the cumulative costs often outweigh the benefits, limiting adoption and providing a barrier to market uptake of such devices, especially in healthcare budget-constrained regions.

Flexible Endoscopes Market Segmentation Analysis:

By Product

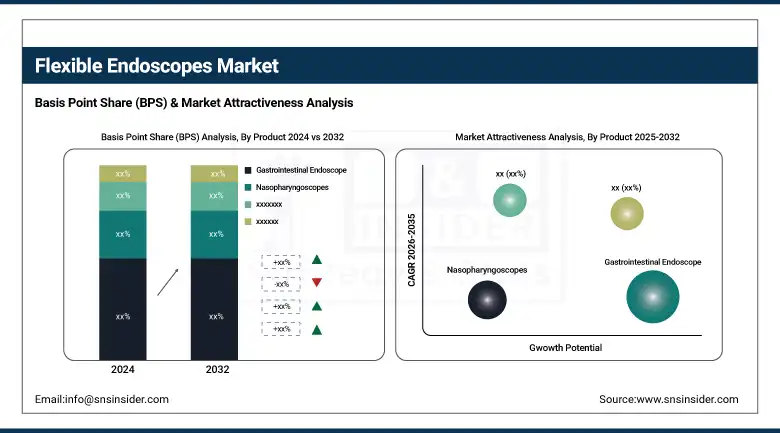

The gastrointestinal endoscopes segment dominated the flexible endoscopes market share in 2024, with a 54.23% share due to the increasing prevalence of GI conditions, such as colorectal cancer, ulcer, and Crohn's disease. High demand for non-invasive and lingering diagnostic techniques is making GI endoscopes famous among hospitals and ambulatory centers. Furthermore, favorable measures, including national screening programs, increased awareness among patients, and global technological advances in GI endoscopy, including high-definition imaging and disposable endoscopes, have reinforced the growth of these procedures.

During the forecast period, the laparoscopes segment is expected to achieve the fastest growth, fueled by the global paradigm toward minimally invasive surgeries (MIS) as an alternative to conventional open surgeries with regard to general, bariatric, and gynecologic procedures. Improvements in surgical outcomes, recovery time, and adoption in health care facilities are driven by advances in camera technologies, 3D, and robotic-assisted laparoscopy, and improved ergonomics. In addition, the increase in lifestyle-related diseases and disorders that necessitate surgical procedures, including gallbladder disease and endometriosis, also fosters the growth of the global laparoscope market.

By Application

The flexible endoscopes market for the gastrointestinal endoscopy segment dominated in 2024 with a 32.14% market share, owing to a high global burden of GI disorders, such as colorectal cancer, ulcers, and inflammatory bowel diseases. The Ogilvie et al paper highlights a recent increase in the use of GI endoscopes linked to routine screening colonoscopies in changing demographics (ageing populations) and expansion of public health initiatives to enhance early cancer detection. Finally, the availability and adoption of Advanced Flexible Endoscopes with high-resolution imaging and therapeutic capabilities further establishes GI endoscopy as the primary modality in clinical medicine.

The bronchoscopy segment is anticipated to register the fastest growth over the forecast period, favoring the growth of the bronchoscopy segment, the rising prevalence of respiratory diseases, including chronic obstructive pulmonary disease (COPD), lung cancer, and infections, such as tuberculosis. The global demand is being fueled by factors such as a mounting requirement for early detection of pulmonary diseases, the growing interventional pulmonology space, and the entry of new flexible bronchoscopes having enhanced navigation technologies.

By End-User

The hospitals segment held the largest share of the global market for flexible endoscopes in 2024, with a 66.18% market share, owing to these hospitals' extensive infrastructure, trained staff, and high number of patients lining up for complicated and emergency procedures. The Hospitals have modern endoscopy suites and also a well-integrated imaging base, through which diagnostic and therapeutic endoscopic procedures of all systems, including gastrointestinal, respiratory, and urological, are also possible by procedures. Hospitals also have an increased procurement budget, which allows them to purchase a larger number of advanced flexible endoscopes and adjacent systems in bulk, thereby fueling their flexible endoscopes market growth.

ASCs (ambulatory surgery centers) are expected to grow the fastest due to the increasing number of surgeries that may be performed on the same day. With their streamlined workflows, improved patient turnover, and lower procedural costs, ASCs are becoming an increasingly desirable setting for selected minimally invasive endoscopic procedures. Further bolstered by stable and agile advancements in endoscopic technology and equipment, the trend is creating a foundation to increase the use of flexible endoscopes in the outpatient setting.

Flexible Endoscopes Market Regional Insights:

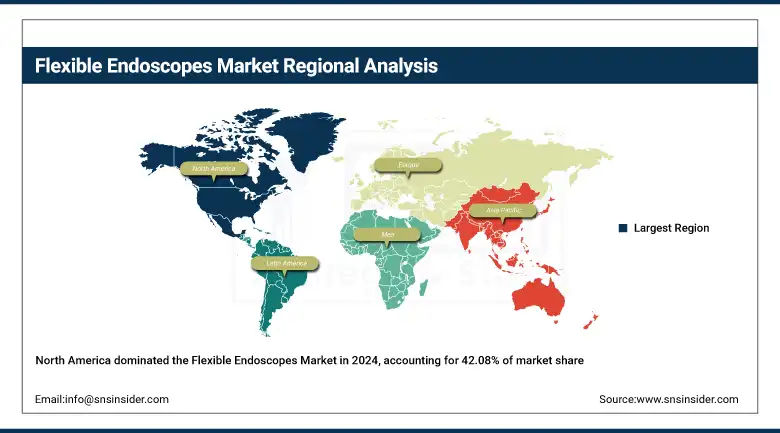

The flexible endoscopes market in North America dominated in 2024 with 42.08% market share, owing to a well-established healthcare infrastructure, rising prevalence of chronic gastrointestinal and respiratory diseases, and growing acceptance of minimally invasive diagnostic procedures. The availability of flexible endoscopes is established in hospitals and ambulatory surgical centers across the region alongside the presence of key market players, established reimbursement frameworks, and hefty investments in R&D by medical device companies. In addition, increased awareness of the advantages of early detection among physicians and patients has led to a rise in the number of these procedures performed in both the U.S. and Canada.

Get Customized Report as per Your Business Requirement - Enquiry Now

The flexible endoscopes market is growing at the fastest rate in Europe, with 6.89% CAGR over the forecast period, owing to the increasing elderly population, rising incidence of colorectal and gastric cancers, and improved government initiatives targeting preventive healthcare services. Germany, France, and the U.K. are heavily investing in the modernization of endoscopy units and public health initiatives to increase access to minimally invasive diagnostics. In addition, the area has regulations that promote innovation and quality, and through training programs, increase the adoption of medical equipment by health professionals. Together, these factors contribute in support for a rapid expansion of the market in Europe.

The flexible endoscopes market analysis across Asia Pacific is projected to witness significant growth owing to the rapid improvement in healthcare infrastructure, high prevalence of gastrointestinal and respiratory diseases, and the rise in the population seeking access to minimally invasive diagnostics. Favorable government initiatives, the growth of medical tourism, and expansion in hospital capacities and technological capabilities are still driving the region’s growth.

Public and private sector investment in endoscopy units and training for clinicians is one of the key drivers of this growth. Increasing awareness of early screening programs and the availability of disposable endoscopes at economical prices are supporting their adoption in developing countries, such as China, India, Japan, South Korea, and others.

The moderate growth in the flexible endoscopes market can be attributed to the growing accessibility to healthcare and healthcare infrastructure in Latin America. Increasing patient awareness of minimally invasive techniques and fragmented distribution networks allows devices to reach a wider audience. Adoption is improving gradually, but fluctuations in the economy and disparities in regulations may cool the pace of expansion, while public–private partnerships and partnerships with global device manufacturers consistently foster growth.

Moderate growth continues in the Middle East & Africa (MEA) region, bolstered by investments in healthcare infrastructure and increasing demand for minimally invasive endoscopic diagnostics. The endoscopy devices segment consists of the largest product category, which includes flexible endoscopes. Key regional drivers consist of increasing disease burden with chronic diseases, establishment of hospital networks in the UAE, South Africa and Saudi Arabia, and adoption of infection control measures, including disposable endoscopes. However, inequitable access to medical care and a shortage of skilled professionals could hamper the flexible endoscopes market trends.

Flexible Endoscopes Market Key Players:

The key flexible endoscopes market Companies operating in the market are Olympus Corporation, Karl Storz SE & Co. KG, Fujifilm Holdings Corporation, Boston Scientific Corporation, Ambu A/S, HOYA Corporation (Pentax Medical), Richard Wolf GmbH, Smith & Nephew plc, Medtronic plc, ConMed Corporation, and other players.

Recent Developments in the Flexible Endoscopes Market:

-

September 5, 2024 – Olympus Australia, a global MedTech leader, formally launched "Sapphire," its first standalone flexible endoscope sterilisation centre. Situated in Melbourne, the centre is a central element of the newly launched Olympus On-Demand solution.

- May 2025 – FUJIFILM Healthcare Europe launched the ELUXEO EG-840T therapeutic gastroscope and the narrow-design EG-840TP endoscope throughout Europe. The launches represent the most recent developments under the company's 'WELCOME, FUTURE' initiative and come after the success of the ELUXEO 8000 system, demonstrating FUJIFILM's continued dedication to the development of endoscopic treatment technologies.

Flexible Endoscopes Market Report Scope:

Report Attributes Details Market Size in 2024 USD 10.66 Billion Market Size by 2032 USD 17.19 Billion CAGR CAGR of 6.19% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Product (Upper Gastrointestinal Endoscope, Colonoscopes, Bronchoscopes, Sigmoidoscopes, Laryngoscopes, Duodenoscopes, Nasopharyngoscopes, Rhinoscopes, Neuroendoscope, Cystoscopes, Laparoscopes, Other Flexible Endoscope)

• By Application (Gastrointestinal (GI) Endoscopy, Laparoscopy, Arthroscopy, Obstetrics/Gynecology Endoscopy, Urology Endoscopy (Cystoscopy), ENT Endoscopy, Bronchoscopy, Mediastinoscopy, Others)

• By End User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles Olympus Corporation, Karl Storz SE & Co. KG, Fujifilm Holdings Corporation, Boston Scientific Corporation, Ambu A/S, HOYA Corporation (Pentax Medical), Richard Wolf GmbH, Smith & Nephew plc, Medtronic plc, ConMed Corporation, and other players.

Frequently Asked Questions

Ans: North America dominated the Flexible Endoscopes Market in 2024.

Ans: The “Gastrointestinal Endoscope” segment dominated the Flexible Endoscopes Market.

Ans: Growing incidences of chronic gastrointestinal and respiratory conditions are driving the market growth.

Ans: The Flexible Endoscopes Market was USD 10.66 billion in 2024 and is expected to reach USD 17.19 billion by 2032.

Ans: The Flexible Endoscopes Market is expected to grow at a CAGR of 6.19% over 2025-2032.

Get in Touch