Invasive Ductal Carcinoma Treatment Market Report Scope & Overview:

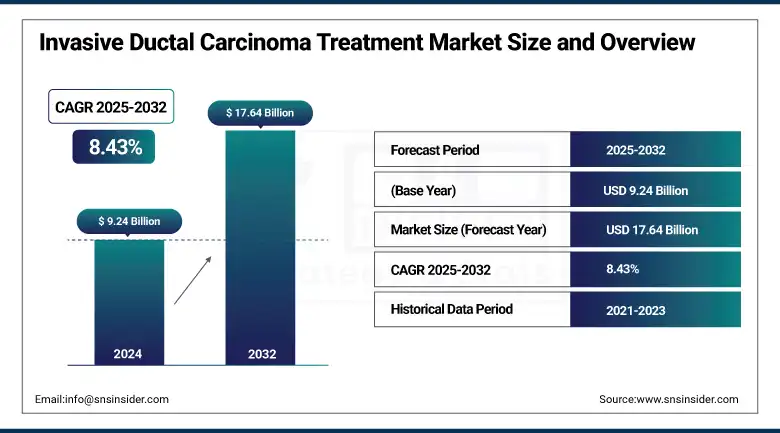

Invasive ductal carcinoma treatment market size was valued at USD 9.24 billion in 2024 and is expected to reach USD 17.64 billion by 2032, growing at a CAGR of 8.43% over the forecast period of 2025-2032.

Rising breast cancer prevalence, government initiatives, and significant therapeutic discoveries are driving the invasive ductal carcinoma treatment market growth.

For instance, with 310,720 women and 2,800 men diagnosed with invasive breast cancer in the U.S. in 2024, the National Breast Cancer Foundation notes that invasive ductal carcinoma (IDC) accounts for nearly 80% of all breast cancer diagnosis.

To Get more information On Invasive Ductal Carcinoma Treatment Market - Request Free Sample Report

Early identification and developments in targeted therapy for invasive cancer, including HER2 inhibitors and CDK4/6 inhibitors, have greatly raised patient survival rates and quality of life. As national health budgets are progressively giving cancer care infrastructure and access top priority, government bodies, such as the U.S. FDA and the European Medicines Agency continue to speed approvals for creative IDC therapy choices.

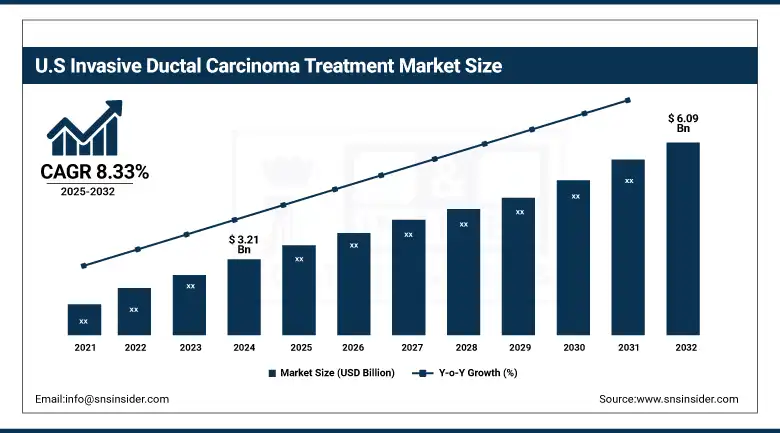

Reflecting strong investment in breast oncology therapeutics and a strong regulatory environment, the U.S. held a significant invasive ductal carcinoma treatment market share, generating USD 3.21 billion in 2024 and is projected to reach USD 6.09 billion by 2032 with a CAGR of 8.33% over 2025–2032. Rising use of customized medicine, increased access to diagnostics, and the development of new oncology pipeline medications help to further highlight these invasive ductal carcinoma treatment market trends.

The invasive ductal carcinoma treatment market growth has been significantly driven by government regulatory bodies. A significant milestone for HER2-positive breast cancer treatment and evidence of the government's will to increase IDC treatment options, the U.S. FDA authorized Enhertu, in April 2024, for HER2-positive metastatic solid tumors. In March 2024, AstraZeneca's Truqap got approval in Japan for hormone receptor-positive, HER2-negative breast cancer with particular genetic changes, therefore highlighting the global drive for precision medicine in breast cancer treatment.

Market Dynamics:

Drivers:

-

Rising Incidence of Global Breast Cancer and Early Detection Initiatives Propel Treatment Demand

A major driver of the invasive ductal carcinoma treatment market is the increasing global frequency of breast cancer, especially invasive ductal carcinoma (IDC). Early detection programs, including mammography exams backed by groups, such as the American Cancer Society, have raised diagnosis rates, further facilitating quick interventions. For instance, the 5-year survival rate for localized IDC is 99%, incentivizing early treatment adoption. By increasing available treatment options, regulatory approvals for innovative medications as Japan's 2024 supplementary New Drug Application for ENHERTU (trastuzumab deruxtecan) targeting HER2-low breast cancer, intensify demand. This increase in diagnosed instances, together with developments in precision diagnostics, guarantees continuous market expansion since healthcare systems provide top priority on lowering IDC mortality rates.

Restraints:

-

Prohibitive Costs of Targeted Therapies Restrict Equitable Access to Advanced Treatments

The high cost of innovative IDC treatments, including antibody-drug conjugates and HER2 inhibitors, generates major obstacles to global availability. For instance, trastuzumab deruxtecan-approved by the FDA in January 2025 for HR-positive/HER2-low breast cancer-carries annual treatment costs over USD 100,000, which are out of reach for low-income areas and uninsured individuals. Due to strong insurance coverage and healthcare spending, North America dominated the market in 2024, and Asia Pacific and Africa lagged, albeit with growing IDC incidence. Extended treatment cycles and concomitant tests, which tax healthcare resources, aggravate this gap. Affordability problems will continue without structural changes, such as tiered pricing models or subsidies, therefore restricting the availability of life-saving treatments and prolonging survival rate differences between high-and low-income groups.

Segmentation Analysis:

By Therapy

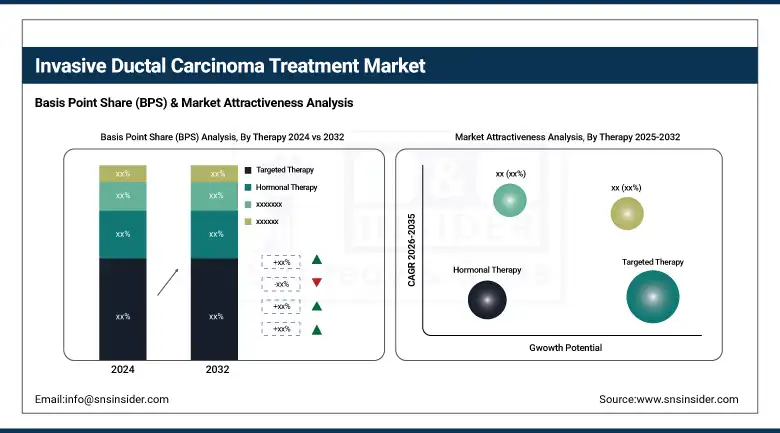

With 64% of global revenue in 2024, targeted therapy for invasive carcinoma is the largest and fastest-growing segment, according to the invasive ductal carcinoma treatment market analysis. The effectiveness of HER2 inhibitors and the increasing application of molecular profiling to direct therapy choice drive this dominance.

For instance, research from Duke University Health System supports the FDA's April 2024 approval of Enhertu for HER2-positive metastatic solid tumors, therefore highlighting the shift toward biomarker-driven IDC therapy choices. Targeted therapy accounted for a notable increase in the U.S. invasive ductal carcinoma treatment market, reflecting the change from conventional chemotherapy for breast cancer toward more exact and less toxic treatments. Immunotherapy is also gaining traction, especially for triple-negative breast cancer, challenging early-stage invasive ductal carcinoma subtype-with recent phase 2 data from Akeso’s ivonescimab showing robust efficacy in combination with chemotherapy for breast cancer.

By Type

The hormone receptor segment held the largest invasive ductal carcinoma treatment market share, reflecting the great frequency of estrogen receptor-positive breast cancer and the efficacy of hormonal treatment for IDC, such as tamoxifen and aromatase inhibitors. The FDA authorized Trodelvy for HR-positive/HER2-negative metastatic breast cancer in February 2023, therefore giving patients who had exhausted hormonal therapy for IDC.

The HER2+ segment is predicted to show the fastest growth driven by fast expansion brought on by the launch of creative medicines, including trastuzumab, pertuzumab, and the antibody-drug combination Enhertu. These medicines have shown notable increases in progression-free and overall survival, which has resulted in more indications and higher acceptance.

For instance, reflecting the move toward precision medicine in hormone receptor and HER2+ subtypes, AstraZeneca's Truqap (capivasertib) was approved in Japan in March 2024 for HR-positive, HER2-negative breast cancer with particular genetic changes.

By Distribution channels

Hospital pharmacies accounted for the largest invasive ductal carcinoma treatment market share, 45% in 2024 with specialized administration and monitoring of chemotherapy, targeted treatments, and immunotherapies often requiring inpatient or outpatient hospital settings. As hospitals offer integrated care, diagnostics, treatment, and follow-up they are the preferred site for complicated IDC management.

Online distribution channels and specialized stores are predicted to expand at the fastest CAGR, driven by the growing availability of oral targeted treatments and hormone drugs that may be safely distributed outside of hospital environments. Growing acceptance of digital health platforms and telemedicine expansion helps to encourage this trend as well.

Regional Analysis:

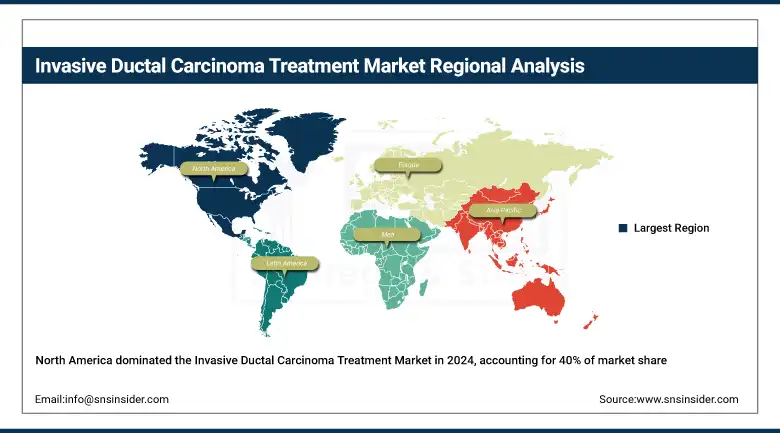

North America continues to dominate the global invasive ductal carcinoma treatment market share 40% in 2024, driven by a robust healthcare infrastructure, high awareness, and significant investment in research and development. The U.S. remains the largest contributor, benefiting from early adoption of targeted therapy, strong reimbursement frameworks, and the presence of leading invasive ductal carcinoma treatment companies. The region’s leadership is further reinforced by high rates of early-stage invasive ductal carcinoma diagnosis and the integration of precision medicine and advanced diagnostics into standard care.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America will continue to lead the global invasive ductal carcinoma treatment market share of 40% in 2024, driven by a strong healthcare infrastructure, great awareness, and large research & development expenditure. Benefiting from early acceptance of targeted therapy, robust reimbursement systems, and the existence of top invasive ductal carcinoma treatment companies, the U.S. remains the biggest contributor. High rates of early-stage invasive ductal carcinoma diagnosis and the inclusion of modern diagnostics and precision medicine into regular treatment support the leadership of the area even further.

Europe is the second-largest market, driven by thorough national screening initiatives, universal healthcare, and strict regulatory control. Germany, the U.K., and France, among others, stress early-stage invasive ductal carcinoma identification and access to sophisticated breast oncology therapeutics. Advanced treatments, including hormone therapy for IDC and new oncology pipeline drugs, have been approved and reimbursed due to the role of the U.K.'s NHS and regulatory authorities, including the MHRA.

Asia Pacific is experiencing the fastest invasive ductal carcinoma treatment market growth, with China and Japan at the forefront. Rising breast cancer incidence, expanding healthcare access, and government investment in cancer care are key drivers. Due to more money for clinical research and the launch of biosimilars, China's market is expected to rise at a notable CAGR. With new approvals for HER2-targeted treatments and increased use of adjuvant therapy and neoadjuvant chemotherapy, Japan is pushing precision medicine.

The LAMEA region is showing steady growth, led by Brazil in Latin America and Saudi Arabia in the Middle East. Government initiatives, such as enhancing access to breast cancer detection, infrastructure for healthcare, and availability of modern treatments such as radiation therapy for IDC and cancer immunotherapy. Particularly, Saudi Arabia is funding research on breast oncology therapies, therefore establishing itself as a regional innovation hub. As the market size is smaller compared to other regions, LAMEA is expected to see accelerated growth as awareness and access to IDC treatment options expand.

Key Players:

The key invasive ductal carcinoma treatment companies are Bristol-Myers Squibb Company, Pfizer Inc., Janssen Pharmaceuticals, Inc., Novartis AG, F. Hoffmann-La Roche Ltd., AstraZeneca, Macrogenics, Inc., Celldex Therapeutics, Merck KGaA, AbbVie Inc., and others.

Recent developments:

-

FDA approval of Enhertu for HER2-positive metastatic solid tumors in April 2024 will increase HER2-positive breast cancer treatment choices.

-

In March 2024, AstraZeneca’s Truqap was approved in Japan for HR-positive, HER2-negative breast cancer with PIK3CA, AKT1, or PTEN alterations.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 9.24 Billion |

| Market Size by 2032 | USD 17.64 Billion |

| CAGR | CAGR of 8.43% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hormone Receptor, and HER2+) • By Therapy (Targeted Therapy, Hormonal Therapy, Immunotherapy, and Chemotherapy) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Bristol-Myers Squibb Company, Pfizer Inc., Janssen Pharmaceuticals, Inc., Novartis AG, F. Hoffmann-La Roche Ltd., AstraZeneca, Macrogenics, Inc., Celldex Therapeutics, Merck KGaA, AbbVie Inc., and others |

Frequently Asked Questions

The Hospital Pharmacies segment dominated the Invasive Ductal Carcinoma Treatment Market.

Prohibitive costs of targeted therapies restrict equitable access to advanced treatments.

The CAGR of the Invasive Ductal Carcinoma Treatment Market is 8.43% during the forecast period of 2025-2032.

The North America region dominated the Invasive Ductal Carcinoma Treatment Market in 2024.

The projected market size for the Invasive Ductal Carcinoma Treatment Market is USD 17.64 billion by 2032.

Get in Touch