Leather Chemicals Market Analysis & Overview

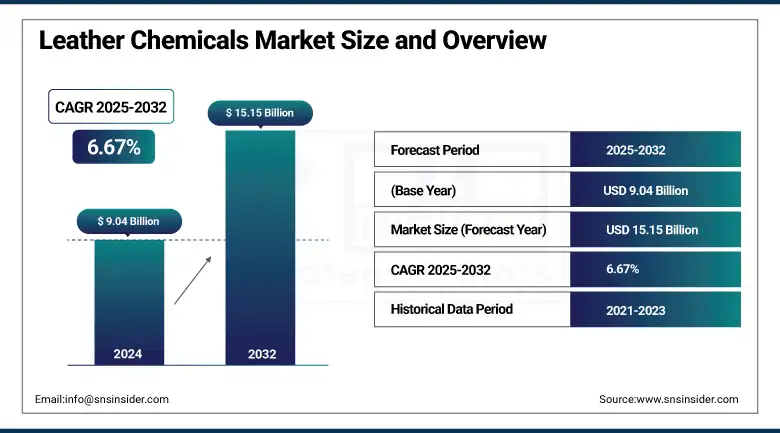

The Leather Chemicals Market size was USD 9.04 billion in 2024 and is expected to reach USD 15.15 billion by 2032, growing at a CAGR of 6.67% over the forecast period of 2025-2032.

The Leather Chemicals Market Analysis highlights the increasing influence of the expanding fashion and luxury goods sector. It is due to the increased demand among consumers for carrying high-fashion, premium, and high-value, uniquely manufactured leather goods, such as luxury handbags, shoes, belts, and apparel, which impact the demand for high-quality leather market and it is booming and is witnessing unprecedented growth. It is impacting communities, especially in urban areas, where younger individuals with more disposable income are dining out. Modern leather chemicals play a pivotal role in satisfying consumer demand for aesthetics, durability, and less environmentally harmful leather goods by aiding in tanning, dyeing, finishing, and surface treatment of leather. Besides, the increasing focus of major fashion brands on sustainability is supported by the sustainable leather processing chemicals.

According to the Bureau of Labor Statistics (BLS), American households on average spent USD 655 on women's clothing, USD 406 on men's clothing, and USD 87 on girls' clothing in 2023. These numbers highlight significant consumer spending on fashion and the importance of the sector in the economy.

Leather Chemicals Market Size and Forecast

-

Market Size in 2024: USD 9.04 Billion

-

Market Size by 2032: USD 15.15 Billion

-

CAGR: 6.67% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2023

To Get more information On Leather Chemicals Market - Request Free Sample Report

Leather Chemicals Market Trends:

-

Rising demand from the footwear and automotive upholstery sectors is driving leather chemical consumption, with global leather footwear production accounting for over 55% of total leather usage.

-

Growing preference for eco-friendly and bio-based chemicals is accelerating market transformation, with sustainable leather processing chemicals witnessing over 8–10% annual growth.

-

Increasing production of automotive interiors is boosting demand for finishing and coating chemicals, as automotive leather applications contribute to nearly 30% of premium leather consumption.

-

Rapid expansion of leather manufacturing in Asia-Pacific is strengthening regional dominance, with the region accounting for over 40% of global leather production.

-

Adoption of advanced tanning technologies and water-efficient processing solutions is reducing chemical and water consumption by 20–25%, improving compliance with environmental regulations.

Moreover, in 2021, the U.S. Textile and Apparel Exports show that the U.S. exports of textiles and apparel rose by USD 2.7 billion (18.5%) to reach USD 17.4 billion in 2021. It indicates a growing demand for U.S.-made fashion products in international markets.

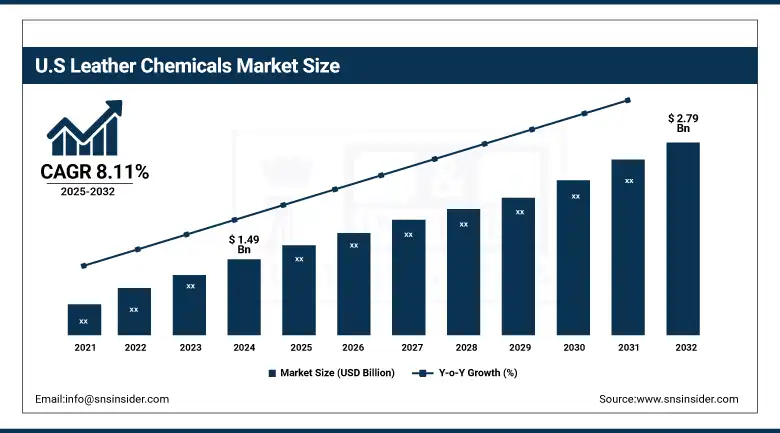

The U.S Leather Chemicals market size was USD 1.49 billion in 2024 and is expected to reach USD 2.79 billion by 2032 and grow at a CAGR of 8.11% over the forecast period of 2025-2032. The country’s expansion is driven by the robust industrial base, high domestic demand for luxury and automotive leather products, and the presence of major manufacturers of leather goods. The demand for specialty leather chemicals is primarily driven by the country's strong automotive industry, where leather is used extensively for interiors. In addition, the U.S. fashion and furniture industries are still looking for raw materials, quality leather, and leather that would sustain the durability process, thus driving the chemical content processed.

Leather Chemicals Market Drivers:

-

Growing Automotive Sector Using Leather Interiors Drives Market Growth

A major factor steering the leather chemicals market is the automotive sector, the growing usage of leather interiors. As buyers pursue ever-more plush, comfortable, attractive cars, they are also finding the highest-grade leather upholstery creeping into car seats, dashboards, and door panels. This is particularly evident in the premium and luxury vehicle segments. In order to meet the stringent requirements for durability, softness, colorfastness, and abrasion resistance, the manufacturers need to use specialty leather chemicals during tanning, dyeing, and finishing processes. This not only gives leather a better look and feel but also better durability and performance in a variety of weather conditions. Also, for the automotive sector, the implementation of green chemistry and eco-friendly leather chemicals in compliance with environmental policies of automotive industries and sustainability goals is driving innovation and therefore increasing the leather chemicals market growth.

According to the Bureau of Economic Analysis (BEA) estimates the value of the motor vehicle seating and interior trim manufacturing industry was about USD 98.845 billion in 2023. Included in this sector is the manufacturing of automotive interior components, which consist of leather upholstery, among others, with leather being such a prime material for automotive interiors.

Leather Chemicals Market Restraints:

-

High Operational and Treatment Costs may hamper the market growth.

The leather chemicals market is restrained by high operational and treatment costs. Tanning is one of the major chemical processes that turns animal skins into leather and produces considerable effluents and solid waste, requiring treatment before discharge to comply with environmental regulations. It costs a lot of money to establish and operate wastewater treatment plants, buy pollution control gear, and meet local and global environmental regulations. For small and medium-sized tanneries, these costs can be extremely prohibitive, squeezing them for profitability and prohibiting them from investing in more advanced or environmentally-friendly leather chemical solutions.

Leather Chemicals Market Opportunities:

-

Technological Advancements in Leather Processing Create Opportunities in the Market

Innovation is disrupting traditional processes with radically new approaches, such as enzyme-based tanning, waterless processing, and digital leather finishing, that can be more efficient, more sustainable, and cheaper. Such technologies contribute to the minimization of water use, chemical waste, and energy consumption, a convergence with the increasing demand for environmentally friendly manufacturing. Moreover, it has some technological advancements in chemical formulations that help leather achieve its properties in better ways, including improved softness, brightness, and durability, such as cleaner tanning technology. Those kinds of innovations are especially helpful for manufacturers who need to stay ahead of the changing quality needs of industries, such as the automotive, fashion, or furniture sectors, which drive the leather chemicals market trends.

The government of India allocated around USD 220 million under the Indian Footwear and Leather Development Programme (IFLDP) during 2021–2026. Much of this funding goes to the Integrated Development of Leather Sector (IDLS) and the Sustainable Technology and Environmental Promotion (STEP) sub-schemes. These schemes extend financial support for the upgradation, addition of capacity, and technological development of existing plant & machinery of leather sector units, such as tanneries, leather goods, and saddlery footwear.

Leather Chemicals Market Segmentation Analysis:

By Product Type

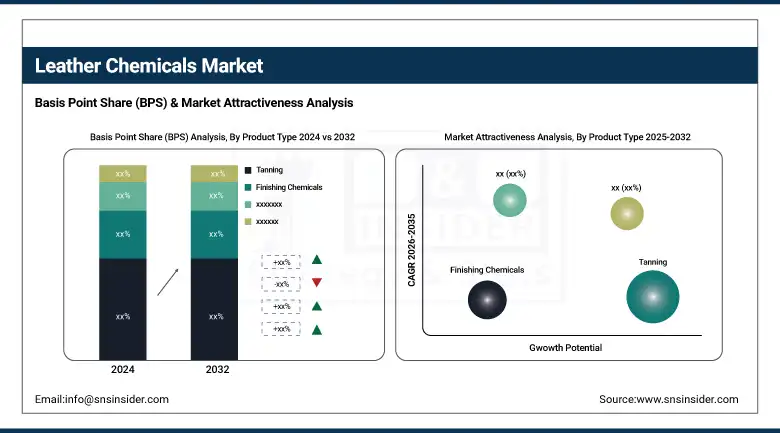

Tanning held the largest Leather Chemicals market share, around 46%, in 2024 as it is an essential process that converts raw hides into leather, which is a multifunctional material that is durable and therefore useful. This process makes animal skins stable by preventing the decay of collagen fibres, thus providing the skins with the required physical features, such as pliability, firmness, and water resistance. Extensive consumption of tanning chemicals, chrome salts, vegetable tannins, and synthetic agents is fueled by high-quality demand for leather for footwear, automotive, fashion, and furniture sectors.

Beamhouse held a significant Leather Chemicals market share, it is due to the fact that Beamhouse covers the important initial steps in manufacturing leather, such as soaking, liming, deliming, and bating. These procedures decontaminate raw hides by doing away with contaminations, hair, and also undesirable healthy proteins, which prepares the leather to be extra acceptable to adhering to tanning and cleaning therapy. Chemicals are applied during the beamhouse stage in order to promote the higher quality and homogeneity of the leather (detergents, enzymes, and degreasing agents). With an increasing emphasis on efficiency, sustainability, and product quality on the part of manufacturers, advanced beamhouse chemicals are gaining traction.

By End-Use Industry

The footwear segment held the largest market share, around 32%, in 2024 owing to the sustained global demand for leather shoes and related products. The footwear manufacturers need a wide category of leather chemicals to ensure durability, comfort, appearance, and resistance to wear and tear, which are the essential properties for shoes that control daily use and multiple environmental conditions. Footwear leather needs to be well tanned, dyed, and finished to satisfy the consumer demand for style and durability. Moreover, the rising middle class and increasing disposable incomes in developing economies have contributed to a surge in footwear consumption, catering further to the growth of leather chemicals.

Automobiles hold a significant market share in the Leather Chemicals market owing to the extensive use of leather in vehicle interiors for a premium touch and comfort, and an ultra-luxury feel. More automakers are using leather in seats, steering wheels, dashboards, and door panels, especially on mid-range to luxury vehicles. There is a fine demand for the leather conditioning agents owing to their durability, best possible colorfastness, softness, and resistance to wear, heat, and UV exposure desired for automotive use, which further bolsters demand for the specialized leather chemicals. Also, the increasing trend for sustainable and eco-friendly manufacturing is driving demand for innovation in advanced leather chemicals that comply with environmental regulations.

Leather Chemicals Market Regional Outlook:

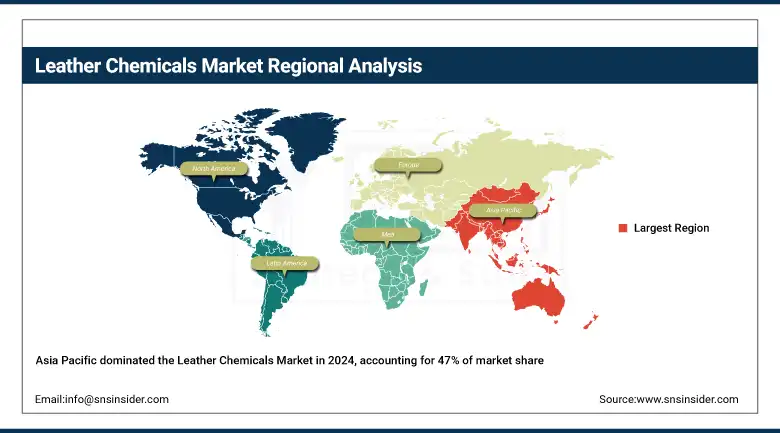

Asia Pacific held the largest market share, around 47%, in 2024. The growth is driven by the rising manufacturing, especially the ones with booming footwear, automotive, and fashion industries in the global center of leather manufacturing and trade. The region is characterized by abundant raw materials, cheap labour, and a growing industrial base, ensuring its competitiveness head-to-head with other global regions in a cluster. Moreover, the significant cost of raw leather, sustainable leather production processes, and growing consumer need for leather chemicals due to their increasing consumption of leather goods (due to rapid urbanization, increase in disposable income, and rising fashion consciousness) fuel demand for leather chemicals used in tanning, dyeing, and finishing.

Get Customized Report as per Your Business Requirement - Enquiry Now

For instance, in January 2024, Pidilite Industries Ltd. formed a strategic partnership with Syn-Bios, a global leader in the leather tanning industry that develops and markets environmentally friendly technologies for high-quality leather processes. This partnership will greatly revolutionize the leather chemical industry in South Asia.

North America Leather Chemicals market held a significant market share and is the fastest-growing segment in the forecast period. It is due to the large-scale leather goods industry in North America and the high demand for high–quality goods in this region. Numerous motor vehicles, fashion, and furniture makers in the region depend on chemically processed leather for vehicle cabin interiors and other upholstery items, in accessories, and apparel. Innovation in leather processing in the U.S. and Canada, driven by leather chemicals companies’ practices, stringent environmental regulations, and growing investment in sustainable chemical technologies. Furthermore, the presence of major chemical companies and continuous research and development to develop biodegradable high technology.

In 2024, TomTex, A U.S.-based start-up, develops bio-based vegan leather from seafood shell waste and mushrooms. A plastic-free alternative to leather, which contributes to more sustainably sourced material innovation in fashion.

Europe held a significant market share in the forecast period. It is owing to the tradition of high-end leather goods, strict regulations regarding environmental protection, and demand for fine leather goods. Italy, Germany, and France are well-known for their luxury fashion, automotive, and upholstery industries, thus, the demand for high-performance leather processing chemicals, performance, visual appeal, and sustainability requirements are inevitable. Responsible for high processing cost, but witnessing the growth of manufacturing plants targeting green chemistry promoted by government policies.

Key Players:

The leading players in the market are Lanxess AG, Stahl Holdings B.V., BASF SE, TFL Ledertechnik GmbH, Sisecam Chemicals, Clariant AG, Schill+Seilacher GmbH, Elementis plc, DyStar Group, and Zschimmer & Schwarz GmbH & Co KG.

Recent Developments:

-

In January 2024, BASF SE introduced a new line of bio-based leather chemicals to reduce the ecological footprint of leather production. It highlights BASF's dedication to sustainability and innovative leather approaches.

-

In October 2023, Trumpler announced, in collaboration with Archroma, a new sustainable and affordable leather tradition process called "DyTan" process this October 2023. This step makes the leather tanning and dyeing process easier and makes leather manufacturing more sustainable, since it consumes less energy and water.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 9.04 Billion |

| Market Size by 2032 | USD 15.15 Billion |

| CAGR | CAGR of 6.67% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Tanning, Dyeing, Beamhouse, Finishing Chemicals) •By Application (Footwear, Leather Goods, Garments, Automobile, Furniture, Glove, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lanxess AG, Stahl Holdings B.V., BASF SE, TFL Ledertechnik GmbH, Sisecam Chemicals, Clariant AG, Schill+Seilacher GmbH, Elementis plc, DyStar Group, Zschimmer & Schwarz GmbH & Co KG. |

Frequently Asked Questions

Asia Pacific led the Leather Chemicals Market in the region with the highest revenue share in 2024.

Growth of the automotive sector using leather interiors drives the market growth.

Tanning will grow rapidly in the Leather Chemicals Market from 2025 to 2032.

The expected CAGR of the global Leather Chemicals Market during the forecast period is 6.67%

The Leather Chemicals Market was valued at USD 9.04 billion in 2024.

Get in Touch