LED Packaging Market Report Scope & Overview:

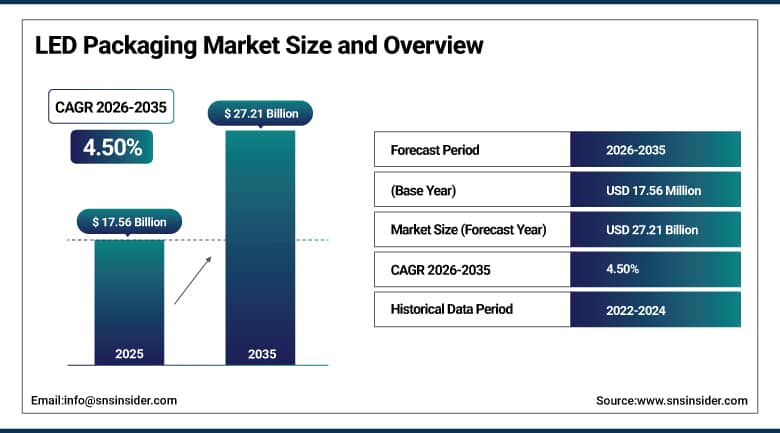

The LED Packaging Market was valued at USD 17.56 billion in 2025 and is expected to reach USD 27.21 billion by 2035, growing at a CAGR of 4.50% from 2026–2035.

The LED packaging market is witnessing significant growth in the global market due to rising demand for energy efficient lighting systems. Increasing adoption of advanced display technologies and mini-LED applications is driving strong market expansion. Growing penetration of automotive LED lighting and smart vehicles is further supporting product deployment. Expansion of smart cities and infrastructure modernization is significantly boosting usage. Rapid advancements in semiconductor packaging and miniaturization are strengthening demand for high performance LED packaging solutions worldwide.

According to Samsung Electronics and ams OSRAM product developments, micro-LED and mini-LED integration is accelerating demand for compact packages. Government energy efficiency programs such as U.S. DOE initiatives support LED adoption. Asia Pacific leads production due to strong semiconductor ecosystems. Nichia Corporation reports continuous innovation in high-brightness LEDs enabling automotive, signage, and smart lighting expansion across global infrastructure applications.

Market Size and Forecast:

-

Market Size 2026E: USD 18.32 billion

-

Market Size 2035: USD 27.21 billion

-

CAGR (2026 - 2035): 4.50%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On LED Packaging Market - Request Free Sample Report

LED Packaging Market Trends:

-

Rapid adoption of mini and micro-LED packaging increases efficiency nearly 30 percent across advanced display applications globally

-

Stringent environmental regulations drive lead-free packaging materials and recyclable substrates reducing hazardous waste by 25 percent globally

-

Advanced thermal management solutions in LED packaging enhance heat dissipation efficiency by 35 percent for high power applications

-

Chip scale and flip chip wafer level packaging technologies reduce production costs nearly 20 percent while improving yields

-

Automotive smart lighting integration with advanced driver assistance systems drives demand growth exceeding 40 percent in packaging units

-

Rising investments in manufacturing capacity expansion across Asia Pacific increase production output by 50 percent improving supply chain resilience

U.S. LED Packaging Market Size Outlook:

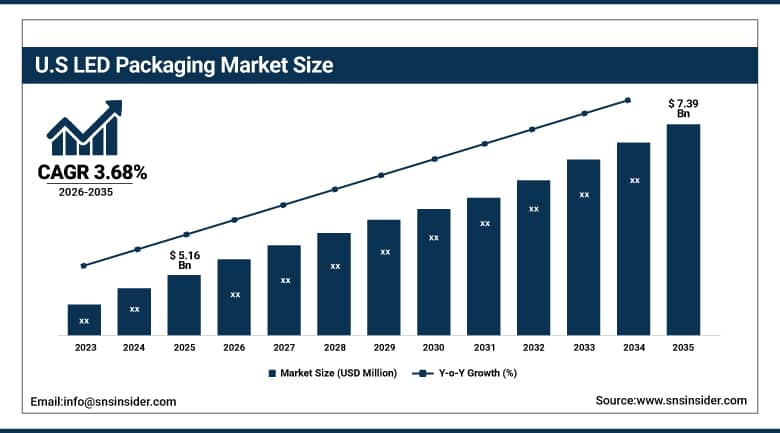

The U.S. LED Packaging Market was valued at USD 5.16 Billion in 2025 and is expected to reach around USD 7.39 Billion by 2035, growing at a CAGR of 3.68% from 2026–2035.

The U.S. LED packaging market is witnessing steady growth because of rapid adoption of energy efficient lighting solutions. LED packaging usage in automotive lighting, display backlighting, and general illumination has been responsible for strong market expansion. Increasing investment in smart buildings and infrastructure modernization has led to rising demand for advanced LED packages. Expanding semiconductor manufacturing and optoelectronics development is further supporting product adoption. Growing focus on energy efficiency and long lifespan lighting solutions is strengthening market growth.

According to the U.S. Department of Energy (DOE), LED adoption has reached 48% of all installed lighting stock in 2020, driven by efficiency gains of up to 90% energy savings versus incandescent systems, significantly improving lighting performance across residential and commercial sectors. The DOE reports annual U.S. lighting energy savings of 1.3 quads.

LED Packaging Market Segment Analysis:

-

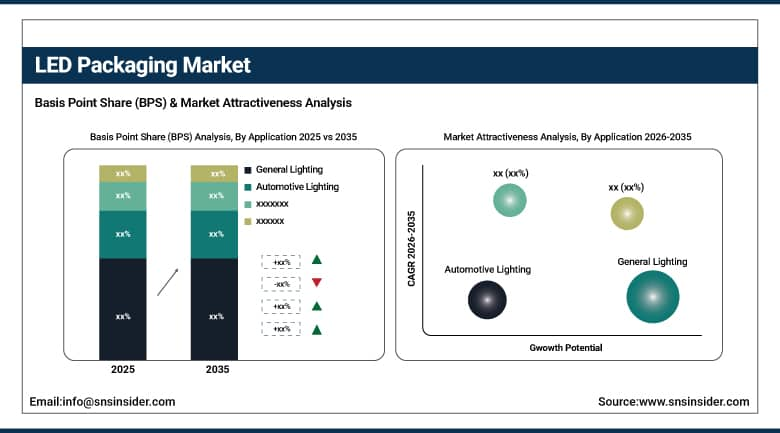

By Application, general lighting dominated the LED packaging market with 35.42% share in 2025; while automotive lighting is the fastest growing segment with CAGR of 8.06% during 2026 to 2035.

-

By Technology, chip-on-board (COB) dominated the LED packaging market with 31.64% share in 2025; while flip chip are the fastest growing segment with CAGR of 8.35% during 2026 to 2035.

-

By End Use, residential dominated the LED packaging market with 42.68% share in 2025; while commercial is the fastest growing segment with CAGR of 5.86% during 2026 to 2035.

-

By Type, discrete LEDs dominated the LED packaging market with 48.36% share in 2025; while integrated led modules are the fastest growing segment with CAGR of 6.36% during 2026 to 2035.

By Application, general lighting dominated the LEDpackaging market, while automotive lighting is the fastest growing segment.

General Lighting segment held the dominated share in the LED packaging market on account of the high revenue generation in 2025. The large-scale adoption of lighting systems based on LEDs in residential, commercial, and industrial infrastructure drives the market's dominance. Increased preference for energy-efficient products along with government policies encouraging low-power consumption lighting systems has aided growth to a great extent. Large-scale adoption of LED technology replacing conventional lighting sources has contributed to the growth.

The Automotive Lighting segment is estimated to capture the fastest CAGR in terms of growth over the forecast period (2026-2035). The rising use of electric cars along with advanced driver-assistance systems, which need advanced lighting technologies, has propelled the growth of this segment. Rising demand for advanced headlamps, ambience lighting, and smart lighting technology in cars is fueling the market growth. Advancements in mini-LED and micro-LED technology have made the lighting more efficient.

By Technology, chip-on-board (COB) dominated the LEDpackaging market, while flip chip is the fastest growing segment.

Chip-On-Board (COB) was a dominated segment in the LED packaging market and had accounted for the largest market share in 2025. The high share percentage is attributed to the advantages of superior thermal management capability, increased luminous efficiency and cost-effectiveness when used for large-scale lighting systems. COB offers a small footprint size and allows for the production of more lumens using less number of components. The widespread use of COB is witnessed in general, industrial and high-power LED lighting systems.

The Flip Chip segment is projected to experience the fastest CAGR during the forecast period of 2026-2035 owing to its good thermal characteristics, high current density capacity, and high energy efficiency compared to conventional LED packages. The flip chip method can be used in manufacturing mini and micro-LEDs that enable innovative display systems and LED automotive lighting. The growing requirements for high-resolution displays, smart devices, and advanced automotive LED lights are fueling the popularity of Flip Chip technology.

By End Use, residential dominated the LED packaging market, while commercial is the fastest growing segment.

Residential end-use accounted for the dominated share in the LED Packaging Market. The growing installation of energy-efficient LED lights in homes and offices is driving the use of LEDs in residential segments. With the rise in urbanization and the replacement of traditional lighting systems, increasing popularity among consumers to use energy-efficient lighting that requires lower maintenance is expected to drive market growth.

The Commercial segment is projected to be the fastest-growing end-use segment in the LED Packaging Market during 2026-2035. The rapid increase in office space along with the development of retail centers and hotels is leading to increased commercial activity. Increased adoption of automated and smart lighting is driving the growth in commercial LED packaging. Cost reduction in electricity consumption is adding to the growing demand in commercial settings.

By Type, discrete leds dominated the LED packaging market, while integrated led modules is the fastest growing segment.

Discrete LEDs segment led the LED packaging market by generating dominated revenue share, owing to extensive application in general lighting, automotive indicators, signages, and consumer electronics products. Easy availability, low-cost manufacturing processes, and mature technology base enable their extensive use across applications. Demand for replacement solutions is anticipated to fuel product dominance through 2035. Superior quality standards, standard module designs, and suitability in existing installations contribute to their constant adoption around the world.

Integrated LED Modules category is expected to register the fastest CAGR through the years 2026-2035. This is owing to the growing demand for LEDs that have higher efficiencies than discrete LEDs as well as enhanced performance in terms of heat dissipation properties, improved control on brightness, and easy integration. Increasing applications in automotive lighting fixtures and display screens fuel their growth at a rapid pace.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

84.36% |

|

Europe |

Germany |

26.40% |

|

Asia Pacific |

China |

41.50% |

|

Middle East & Africa |

UAE |

16.80% |

|

Latin America |

Brazil |

45.30% |

Asia Pacific LED Packaging Market Insights.

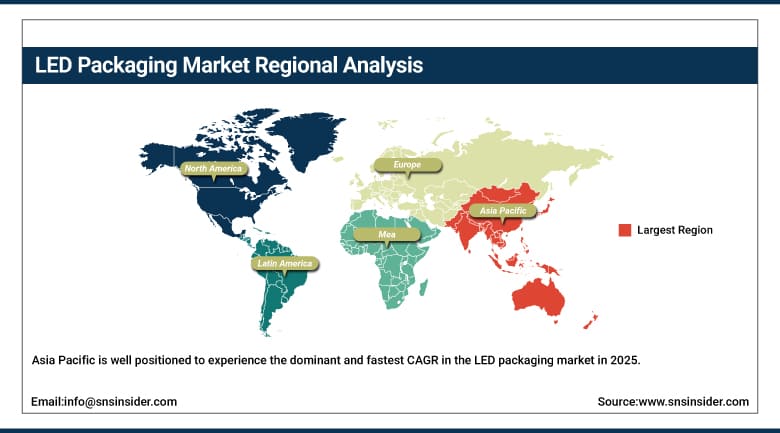

Asia Pacific is well positioned to experience the dominant and fastest CAGR in the LED packaging market in 2025, with a 32.85% market share and a 5.30% CAGR, driven by rapid expansion in electronics manufacturing and LED production dominance. China, India, Japan, and South Korea are key contributors. Rising demand for consumer electronics, automotive lighting, and display technologies is boosting adoption. Expanding semiconductor manufacturing capacity and large-scale LED production hubs are further strengthening market growth across the region.

According to Asian Development Bank, Asia-Pacific economies are expanding electronics exports and industrial output, strengthening high-tech manufacturing clusters. China’s LED production exceeds 13–14 million tons annually, reflecting strong industrial scale.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America LED Packaging Market Insights.

North America accounts for a significant revenue share in 2025 due to the growing demand for advanced lighting and display technologies. The region benefits from a mature semiconductor industry along with the higher adoption of intelligent lighting and LED applications in the automotive sector. Increasing demand for energy-efficient lighting, OLED and mini-LED displays, and intelligent lighting systems is contributing to market expansion in both the U.S. and Canada.

According to the U.S. Department of Energy, LED lighting reached approximately 48% penetration of the installed lighting stock by 2020, significantly reducing national electricity consumption in buildings. The U.S. Energy Information Administration (EIA) reported that LEDs were present in around 44% of commercial buildings by 2018, indicating rapid adoption across infrastructure.

Europe LED Packaging Market Insights.

The Europe LED packaging market makes an important mark in the year 2025 owing to strong sustainability regulations and energy efficiency mandates. Countries like Germany, France, United Kingdom, and Italy are leading contributors to regional demand. High focus on carbon neutrality, smart lighting systems, and automotive electrification is supporting consistent market expansion. Increasing investments in green buildings and smart infrastructure are strengthening adoption across commercial and industrial sectors.

According to the European Commission under Ecodesign Regulation, Europe’s lighting stock exceeds 10 billion light sources, with LEDs rapidly increasing their share, significantly improving energy efficiency across residential, commercial, and industrial applications.

According to Eurostat and EU energy efficiency assessments, lighting accounts for about 10% of total electricity consumption in the EU, while LED transition policies are projected to deliver around 34 TWh annual energy savings by 2030.

Middle East & Africa and Latin America LED Packaging Market Insights.

The Middle East & Africa, as well as Latin America, regions will see stable growth in the LED packaging market by 2025 on account of infrastructure development and smart lighting adoption. The UAE, Saudi Arabia, South Africa, Brazil, and Mexico will become new additions to these markets. With more smart city projects, urban development, and renewable energy integration, there is likely to be steady growth in LED packaging demand within these economies.

According to UAE Ministry of Energy and Infrastructure and Saudi Energy Efficiency Center, government-led street lighting retrofit programs and mandatory efficiency standards are accelerating LED adoption across infrastructure and commercial sectors in the Middle East & Africa region.

According to Brazil Ministry of Mines and Energy and Mexico Secretariat of Energy, national energy efficiency policies and lighting modernization initiatives are driving increased LED deployment across urban infrastructure in Latin America.

Market Dynamics:

Growth Drivers: Rising demand for energy efficient lighting systems and smart infrastructure modernization accelerating LED adoption

The significant move towards energy-efficient lighting systems is creating huge demand for LED packages. All countries around the world are adopting energy-saving policies and discontinuing inefficient lighting systems. The fast development of smart cities and smart infrastructure is contributing to rising demand for superior LED packages. The increasing substitution of conventional lighting systems with LED systems is leading to the growth of this market. The consistent progress in energy-efficient lighting technologies is enhancing prospects for the industry’s growth in the coming years.

As per the International Energy Agency (IEA), LED adoption is above 75% in India, fueled by government-led schemes and energy efficiency regulations for more than 110 countries. Large scale adoption of LEDs in streetlights has been made possible in India due to their UJALA scheme and smart city scheme, which has helped to reduce energy consumption in some cities by up to 58%.

Restraints: Intense competition from alternative lighting technologies and pricing pressure restricting market expansion

Availability of alternative sources of lighting such as OLEDs and normal fluorescent lights also forms a potential threat to the adoption of LED packaging. Price sensitivity among people in developing nations renders entry into the market difficult for high-end products. Fast commoditization of LED components leads to low profit margins for manufacturers. Frequent innovations mean that firms have to invest heavily in research and development activities, raising operational costs and slowing down the adoption process.

Opportunities: Growing adoption of micro-LED and smart lighting systems creating high value growth opportunities

The rapid development of micro-LED and smart lighting technologies has created many promising prospects for the development of LED packages. The increasing demand for high-resolution display screens among the consumer electronics and automotive industry has opened up many possibilities in the market. The introduction of IoT-based smart lighting systems has led to an increased acceptance of LED packages. There have been constant developments made in energy-efficient packing technologies, which have led to better performances.

Recent Developments:

-

2026: Nichia expanded microLED and high-efficiency LED R&D, enhancing automotive, display applications, wafer-level stability, and ultra-bright chip development globally.

-

2025: Refond expanded Mini LED packaging and display modules, improving automotive lighting, efficiency, and global supply chain integration for advanced optoelectronics.

-

2025: Samsung advanced MicroLED and Neo QLED LED packaging, improving brightness, efficiency, AI-driven optimization, and large-screen commercialization globally.

-

2024: Seoul Semiconductor expanded WICOP LED packaging adoption, boosting efficiency, thermal performance, and OEM collaborations across automotive and industrial lighting globally.

LED Packaging Market Key Players are:

-

Nichia Corporation

-

ams OSRAM AG

-

Samsung Electronics Co., Ltd.

-

Seoul Semiconductor Co., Ltd.

-

Lumileds Holding B.V.

-

Cree LED

-

Toyoda Gosei Co., Ltd.

-

LG Innotek Co., Ltd.

-

Stanley Electric Co., Ltd.

-

ROHM Co., Ltd.

-

Epistar Corporation

-

Sanan Optoelectronics Co., Ltd.

-

NationStar Optoelectronics Co., Ltd.

-

MLS Co., Ltd.

-

Everlight Electronics Co., Ltd.

-

Unity Opto Technology Co., Ltd.

-

Refond Optoelectronics Co., Ltd.

-

Harvatek Corporation

-

Ennostar Inc.

-

Genesis Photonics Inc.

LED Packaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.56 Billion |

| Market Size by 2035 | USD 27.21 Billion |

| CAGR | CAGR of 4.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (General Lighting, Backlighting, Displays, Automotive Lighting, Signage, Semiconductor & Electronics) • By Technology (Chip-on-Board (COB), Surface Mount Device (SMD), Flip Chip, Package-on-Package (PoP), Silicon-Based) • By End Use (Residential, Commercial, Industrial) • By Type (Discrete LEDs, Integrated LED Modules, LED Arrays) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nichia Corporation, ams OSRAM AG, Samsung Electronics Co., Ltd., Seoul Semiconductor Co., Ltd., Lumileds Holding B.V., Cree LED, Toyoda Gosei Co., Ltd., LG Innotek Co., Ltd., Stanley Electric Co., Ltd., ROHM Co., Ltd., Epistar Corporation, Sanan Optoelectronics Co., Ltd., NationStar Optoelectronics Co., Ltd., MLS Co., Ltd., Everlight Electronics Co., Ltd., Unity Opto Technology Co., Ltd., Refond Optoelectronics Co., Ltd., Harvatek Corporation, Ennostar Inc., Genesis Photonics Inc. |

Frequently Asked Questions

The LED packaging market is expected to grow at a CAGR of 4.50% from 2026 to 2035.

The LED packaging market was valued at USD 17.56 billion in 2025.

Rising energy-efficient lighting demand, smart infrastructure expansion, and automotive LED adoption are driving global market growth.

Chip-on-Board (COB) dominated the market in 2025 due to high efficiency, strong thermal performance, and cost effectiveness.

North America dominated the LED packaging market due to advanced semiconductor ecosystem, smart lighting adoption, and strong automotive LED demand.

Get in Touch