Liquid Metal Thermal Interface Material Market Report Scope & Overview:

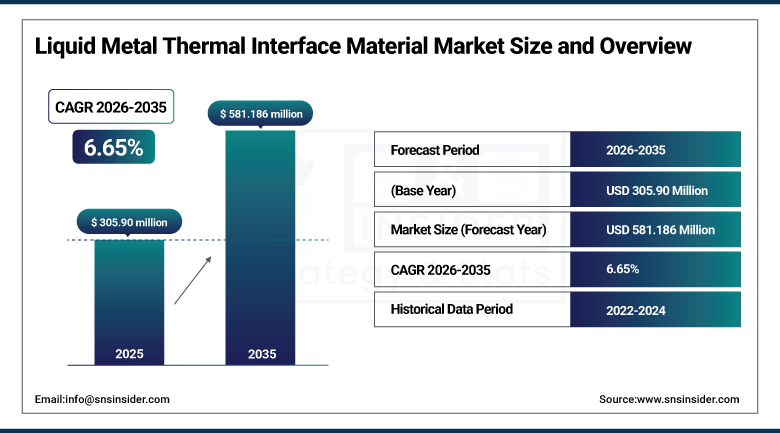

The Liquid Metal Thermal Interface Material Market was valued at USD 305.90 million in 2025 and is expected to reach USD 581.18 million by 2035, growing at a CAGR of 6.65% from 2026–2035.

The liquid metal thermal interface material market is witnessing strong growth in the global market owing to the increasing demand for high-performance thermal management solutions, advanced cooling systems, and miniaturized electronic devices. The rising need for efficient heat dissipation in semiconductor devices, CPUs, GPUs, and power electronics is promoting the usage of liquid metal TIMs in various sectors. Investments made by organizations in data centers, electric vehicles, and high-performance computing infrastructure are contributing to market growth. Increasing developments in AI computing, next-generation electronics, and advanced alloy formulations are playing a major role in driving the demand for liquid metal TIMs. Growth in electronics manufacturing activities and stringent performance requirements are fueling the demand for market.

According to the U.S. Department of Energy and International Energy Agency on high-performance computing infrastructure trends, global data center electricity consumption accounts for approximately 2–3% of total electricity demand in 2025, with cooling systems contributing nearly 30–40% of facility energy use.

As stated by the U.S. National Renewable Energy Laboratory, advanced semiconductor packaging and AI workloads have increased chip heat flux beyond 500 W/cm² in high-density processors, driving measurable adoption of ultra-high-conductivity thermal interface solutions.

Market Size and Forecast

-

Market Size 2026E: USD 325.63 million

-

Market Size 2035: USD 581.18 million

-

CAGR (2026 - 2035): 6.65%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Liquid Metal Thermal Interface Material Market - Request Free Sample Report

Liquid Metal Thermal Interface Material Market Trends

-

Rapid expansion of AI infrastructure is increasing demand for high efficiency liquid metal thermal interface materials globally.

-

Growing data center deployments are driving adoption of advanced cooling solutions for high density computing systems.

-

Increasing GPU and CPU heat loads are boosting requirement for superior thermal conductivity materials in electronics.

-

Shift toward miniaturized and high-power density electronics is accelerating use of advanced thermal interface solutions.

-

Continuous semiconductor innovation is improving chip performance, increasing need for effective heat dissipation technologies.

-

Rising cloud computing and edge computing adoption is strengthening demand for high performance thermal management materials.

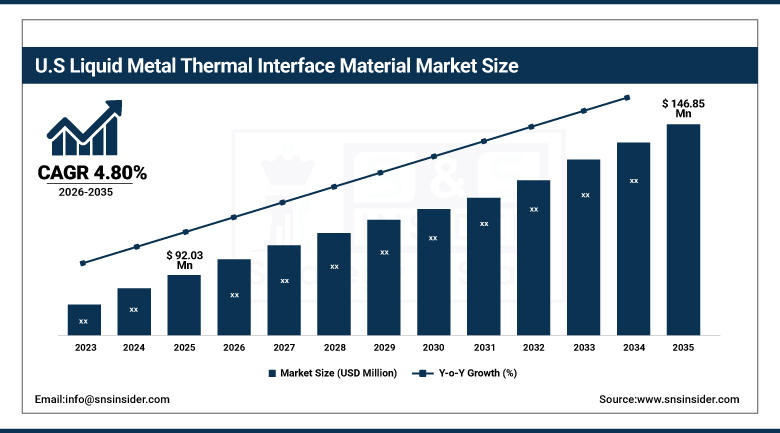

U.S. Liquid Metal Thermal Interface Material Market Size Outlook.

The U.S. Liquid Metal Thermal Interface Material Market was valued at USD 92.03 million in 2025 and is expected to reach around USD 146.85 million by 2035, growing at a CAGR of 4.80% from 2026–2035.

The U.S. liquid metal thermal interface material market is growing consistently owing to increased demand in data centers, semiconductor cooling, and high-performance computing applications. The usage of liquid metal thermal interface materials in CPUs, GPUs, EV battery systems, and advanced electronics has contributed to market growth in a consistent manner. Increased spending in the development of AI infrastructure and advanced chip design has generated an increase in demand for high-efficiency thermal management materials. Development of electronics manufacturing, automotive electrification, and next-generation computing systems is further driving the demand for this product.

As per the U.S. National Science Foundation SBIR-supported research and the U.S. Department of Energy–aligned semiconductor thermal management studies, liquid metal thermal interface materials are being advanced to achieve ultra-low thermal resistance below 1 mm²K/W in experimental systems. NSF-funded prototypes demonstrate stretchable liquid metal–polymer composites enabling heat dissipation improvements exceeding 250% strain tolerance for advanced electronics cooling.

Additionally, the U.S. electronics thermal management applications account for over 26% of thermal interface material demand in 2025 computer systems, reflecting measurable adoption in high-density computing and semiconductor packaging applications.

Liquid Metal Thermal Interface Material Market Segment Analysis

-

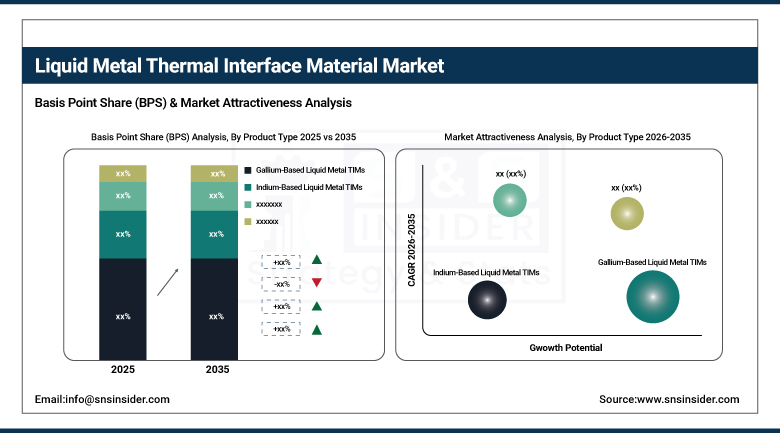

By Product Type, gallium-based liquid metal TIMS dominated the market with 55.40% share in 2025; while eutectic alloy liquid metal TIMS are the fastest growing segment with CAGR of 11.39% during 2026 to 2035.

-

By Application, consumer electronics dominated the market with 46.80% share in 2025; while data centers & high-performance computing are the fastest growing segment with CAGR of 10.50% during 2026 to 2035.

-

By End User, electronics manufacturers dominated the market with 52.60% share in 2025; while data center operators are the fastest growing segment with CAGR of 11.15% during 2026 to 2035.

-

By Distribution Channel, direct sales dominated the market with 50.20% share in 2025; while OEM/contract supply agreements are the fastest growing segment with CAGR of 11.26% during 2026 to 2035.

By Product Type, gallium-based liquid metal TIMS dominated the liquid metal thermal interface material market, while eutectic alloy liquid metal TIMS are the fastest growing segment.

The Gallium-based liquid metal TIMs sub-segment held the dominated revenue share in the Liquid Metal Thermal Interface Materials market in 2025. The reason behind this is that it is highly efficient when compared with other liquid metals because it exhibits better thermal conductivity along with having a low melting point. This segment is used in consumer electronics and high-performance computers. The existing process and economic feasibility have contributed to the massive utilization of this segment in semiconductor cooling and advanced electronic devices.

The Eutectic alloy liquid metal TIMs segment is projected to register the fastest CAGR over the forecast period, i.e., from 2026 to 2035. The increasing requirement of advanced cooling technology for AI computing and EVs has driven the growth of this segment. The growing innovation in materials engineering and rising application in data centers and automotive electronics will fuel the growth of this segment globally.

By Application, consumer electronics dominated the liquid metal thermal interface material market, while data centers & high-performance computing are the fastest growing segment.

Consumer Electronics emerged as the leading segment for liquid metal thermal interface material market with the largest revenue share in 2025 owing to high demand for high-performance smartphones, gaming equipment, laptops, and computing devices. Fast shrinking electronics necessitates better thermal management for better performance, and liquid metal thermal interface materials offer improved thermal conductivity and hence performance improvements. Growth in manufacturing consumer electronics around the world has increased the use of liquid metal TIMs in advanced semiconductor cooling solutions.

The Data Center & High-Performance Computing is anticipated to grow at the fastest CAGR during the forecast period 2026-2035 due to growing AI workloads, growth of cloud computing technologies, and installation of high-density servers. Growing demand for thermal dissipation of heat generated by GPU and processors needs more efficient cooling techniques. Liquid metal TIMs provide an effective solution for heat dissipation and system performance. Investments in hyperscale data center installations have been fueling adoption worldwide.

By End User, electronics manufacturers dominated the liquid metal thermal interface material market, while data center operators are the fastest growing segment.

The Electronics Manufacturers segment was observed as the leading player in terms of generating the dominated revenues in the liquid metal thermal interface material market in 2025 owing to effective utilization of modern thermal solutions across the semiconductor fabrication process and electronic device assembly applications. High demand for top-quality CPUs, GPUs, and small-sized consumer electronics has been a key contributing factor. Additionally, well-established supply chains, constant innovations within the semiconductor industry, and rising requirement for thermal management have propelled the dominance of this segment within market.

The Data Center Operators segment will hold the most significant CAGR between 2026 and 2035 owing to the surging demand for AI computing, cloud computing, and expansion of hyperscale data center networks. Rising amount of heat generated by powerful servers and advanced GPUs has boosted the adoption rate of liquid metal thermal interface solutions. Additionally, investments towards developing energy-efficient cooling solutions have accelerated the segment growth within market.

By Distribution Channel, direct sales dominated the liquid metal thermal interface material market, while OEM/contract supply agreements are the fastest growing segment.

The Direct Sales business channel accounted for the leading market share in terms of revenue in the liquid metal thermal interface material market in 2025. This channel was favored due to greater preference for customized solutions, along with technical collaboration between the supplier companies and their clients. The high-performance computing, semiconductor, and EV industries require materials to be specified according to requirements. Thus, direct procurement guarantees higher quality and optimal performance of the electronic systems.

The OEM/Contract Supply Agreement business channel will experience significant CAGR during the period from 2026 to 2035. This is mainly attributed to rising contracts between material suppliers and OEMs from various industries. The increased demand for integrated thermal solutions for CPUs, GPUs, and EV modules will favor this channel. Such contracts will enable the OEMs to benefit from cost-effective procurement and innovations within the domain.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.35% |

|

Europe |

Germany |

27.10% |

|

Asia Pacific |

China |

38.60% |

|

Middle East & Africa |

UAE |

17.80% |

|

Latin America |

Brazil |

44.30% |

North America Liquid Metal Thermal Interface Material Market Insights.

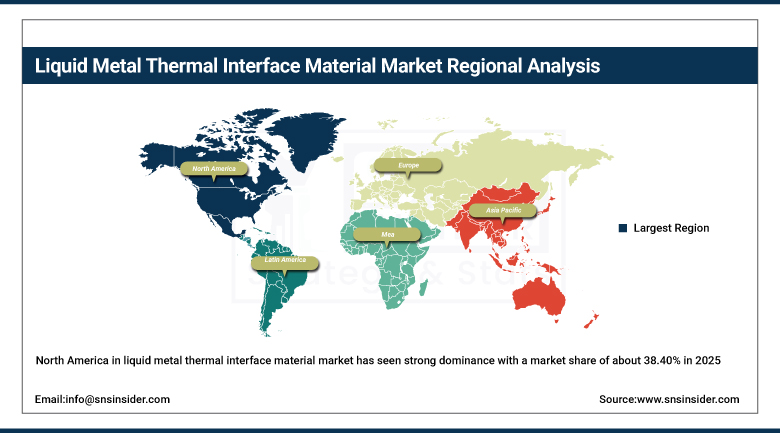

North America in liquid metal thermal interface material market has seen strong dominance with a market share of about 38.40% in 2025 due to advanced semiconductor manufacturing and data center infrastructure. The region benefits from strong demand in high-performance computing, EV thermal management, and AI driven hardware systems. Increasing demand for efficient heat dissipation, advanced cooling solutions, and miniaturized electronics is driving market expansion across the United States and Canada. Rising adoption in cloud computing and automotive electronics is further supporting market leadership. Strong R&D investments are strengthening thermal innovation capabilities.

According to the U.S. Geological Survey Mineral Commodity Summaries 2026 and publicly reported industry data on thermal management materials, North America accounts for approximately 24.1% of global liquid metal thermal interface material demand in 2025, reflecting strong adoption in high-performance computing and electronics manufacturing. The U.S. center electricity consumption represents about 4% of national electricity use in 2025, as reported by the U.S. Department of Energy, with continued growth in AI-driven workloads increasing deployment of advanced cooling technologies such as liquid metal TIMs in server and semiconductor applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Liquid Metal Thermal Interface Material Market Insights.

The Europe liquid metal thermal interface material market shows strong presence in 2025 due to strict energy efficiency regulations and growing electronics manufacturing base. Countries like Germany, France, United Kingdom, and Netherlands are key contributors to demand. High focus on automotive electrification, industrial electronics, and advanced computing systems is supporting steady market growth across the region. Increasing adoption in EV battery systems, aerospace electronics, and telecom infrastructure is further strengthening consumption. Expanding sustainability and energy efficiency frameworks are driving advanced thermal material adoption.

According to the European Commission’s 2025 Digital Economy and Society Index indicators and the International Energy Agency on industrial electrification, Europe’s centre workload is expanding with electricity consumption share reaching nearly 3% of total EU demand in 2025, driven by high-performance computing and AI server deployment.

Asia Pacific Liquid Metal Thermal Interface Material Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the liquid metal thermal interface material market during the forecast period with a market share of about 8.70% in 2025. Rapid electronics manufacturing expansion and semiconductor fabrication growth are driving strong demand across China, Japan, South Korea, India, and Taiwan. Expanding consumer electronics production, EV manufacturing, and data center investments are significantly boosting adoption. Rising demand for cost-efficient high-performance cooling solutions is further accelerating market growth across the region. Large scale chip production supports strong regional demand outlook.

In accordance with the TIFM, TIFM was also dominant in the adoption of advanced TIFM in HPC and EV batteries’ thermal systems. 50% of the regional demand in 2025 came from electronics manufacturing. The liquid metal TIFM solution became prevalent for sub-5 nm semiconductor packaging as well as in AI system hardware heat flux dissipation.

Middle East & Africa and Latin America Liquid Metal Thermal Interface Material Market Insights.

The Middle East & Africa and Latin America region is witnessing steady growth due to rising digital infrastructure and industrial modernization. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in data centers, telecommunications, and automotive electronics are supporting market expansion. Growing need for efficient thermal management in industrial electronics and cloud infrastructure is further boosting product adoption. Rising industrialization strengthens long term demand outlook across both regions.

According to the U.S. Department of Energy and National Institute of Standards and Technology, thermal management demand in high-performance electronics is increasing as center workloads grow, with global center electricity consumption estimated at about 1–1.5% of total electricity use in 2025.

Market Dynamics

Growth Drivers: Rising demand for high performance computing and AI driven electronics accelerates liquid metal cooling adoption

Rapid expansion of artificial intelligence workloads and high-performance computing systems is increasing thermal loads in processors. Liquid metal thermal interface materials provide superior heat dissipation compared to conventional greases. Growing use in GPUs, CPUs, and advanced semiconductor chips enhances system efficiency. Data centers and cloud infrastructure expansion further strengthens adoption. Increasing need for miniaturized and high-power density electronics is accelerating demand across multiple industries. Continuous innovation in chip design and processing speed is further boosting requirement for advanced thermal management solutions globally.

According to the IEEE Electronic Packaging Society 2025 technical analysis on AI and HPC thermal design, next-generation accelerators used in AI-driven computing increasingly exceed 700 watts per module, with industry roadmaps targeting 1-kilowatt-class GPUs explicitly designed for liquid-cooled architectures.

As per benchmarking studies published in 2025 on liquid-cooled HGX systems, liquid cooling improves GPU thermal stability from 54–72°C under air cooling to 41–50°C, enabling approximately 17% higher computational throughput. These measurable thermal and performance gains are driving accelerated adoption of liquid metal thermal interface materials in high-density AI server platforms.

Restraints: Reliability concerns and potential leakage risks restrict usage in sensitive electronic and consumer devices

Liquid metal materials pose risks of leakage and corrosion when improperly applied in electronic systems. Interaction with aluminum and other metals may cause degradation over time. Stability under extreme thermal cycling remains a technical challenge in long term applications. Manufacturers require advanced sealing and containment methods to ensure safety. These requirements increase design complexity and system cost. Concerns regarding long term reliability in consumer electronics reduce adoption rates. Strict quality control and engineering precision are essential for broader commercialization of these materials.

Opportunities: Rapid expansion of data centers and AI infrastructure creates strong demand for advanced thermal interface materials

Global growth in cloud computing and artificial intelligence infrastructure is increasing deployment of high-density servers. These systems generate extreme heat loads requiring efficient cooling solutions. Liquid metal thermal interface materials provide superior thermal conductivity for next generation processors. Hyperscale data centers are adopting advanced cooling technologies to improve energy efficiency. Increasing investment in edge computing and 5G infrastructure further expands demand. Continuous digital transformation across industries supports long term adoption of high-performance thermal management solutions globally.

According to the International Energy Agency and U.S. Department of Energy center efficiency assessments, global center electricity demand continues to rise with AI workloads increasing server rack power densities above 100 W/cm² in 2025.

As per IEEE Electronics Packaging Society 2025–2026 guidance, over 30% of AI center deployments are adopting liquid cooling systems due to thermal constraints. These measurable indicators of rising compute density and cooling transition strongly support accelerated adoption of liquid metal thermal interface materials in advanced AI infrastructure.

Recent Developments

-

2026: Parker Hannifin Corporation advanced thermal management technologies supporting liquid cooling infrastructure for high-performance computing and semiconductor system.

-

2025: Thermal Grizzly refined Conductonaut liquid metal TIM formulations enhancing thermal conductivity stability for CPU and GPU cooling enthusiasts.

-

2025: Boston Materials partnered with Mitsubishi Chemical Group to co-develop second-generation Liquid Metal ZRT thermal interface materials for AI applications.

-

2024: Henkel AG & Co. KGaA expanded Bergquist thermal management materials portfolio supporting electronics cooling and semiconductor applications globally.

Liquid Metal Thermal Interface Material Market Key Players are:

-

Indium Corporation

-

Thermal Grizzly

-

Coollaboratory

-

Arieca, Inc.

-

Boston Materials, Inc.

-

Boyd Corporation

-

Henkel AG & Co. KGaA

-

KERAFOL Keramische Folien GmbH & Co. KG

-

Parker Hannifin Corporation

-

Shin-Etsu Chemical Co., Ltd.

-

Dow Inc.

-

Gelid Solutions

-

Thermalright Inc.

-

DeepCool Industries Co., Ltd.

-

Cooler Master Technology Inc.

-

Corsair Gaming, Inc.

-

Sino Santech Materials Technology Co., Ltd.

-

Aster Materials

-

Shenzhen Sanhe Tongda Technology Co., Ltd.

-

Dongguan Fortrust New Material Co., Ltd.

Liquid Metal Thermal Interface Material Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 305.90 Million |

| Market Size by 2035 | USD 581.18 Million |

| CAGR | CAGR of 6.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Gallium-Based Liquid Metal TIMs, Indium-Based Liquid Metal TIMs, Eutectic Alloy Liquid Metal TIMs, Other Liquid Metal TIMs) • By Application (Consumer Electronics, Data Centers & High-Performance Computing, Automotive Electronics & EVs, Telecommunications & Networking Equipment) • By End User (Electronics Manufacturers, Automotive OEMs, Data Center Operators, Telecommunications Equipment Manufacturers) • By Distribution Channel (Direct Sales, Distributors & Resellers, Online Sales Channels, OEM/Contract Supply Agreements) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Indium Corporation, Thermal Grizzly, Coollaboratory, Arieca, Inc., Boston Materials, Inc., Boyd Corporation, Henkel AG & Co. KGaA, KERAFOL Keramische Folien GmbH & Co. KG, Parker Hannifin Corporation, Shin-Etsu Chemical Co., Ltd., Dow Inc., Gelid Solutions, Thermalright Inc., DeepCool Industries Co., Ltd., Cooler Master Technology Inc., Corsair Gaming, Inc., Sino Santech Materials Technology Co., Ltd., Aster Materials, Shenzhen Sanhe Tongda Technology Co., Ltd., Dongguan Fortrust New Material Co., Ltd. |

Frequently Asked Questions

The liquid metal thermal interface material market is expected to grow at a CAGR of 6.65% from 2026 to 2035.

The liquid metal thermal interface material market was valued at USD 305.90 million in 2025.

Rising demand for high-performance computing, AI infrastructure, data centers, and semiconductor cooling drives global liquid metal thermal interface materials demand.

Gallium-based liquid metal TIMs dominated in 2025 due to high thermal conductivity, low melting point, and widespread electronics and HPC use.

North America dominated the liquid metal thermal interface material market due to advanced semiconductor manufacturing, strong data centers, and AI computing adoption.

Get in Touch