Medical Affairs Outsourcing Market Report Scope & Overview:

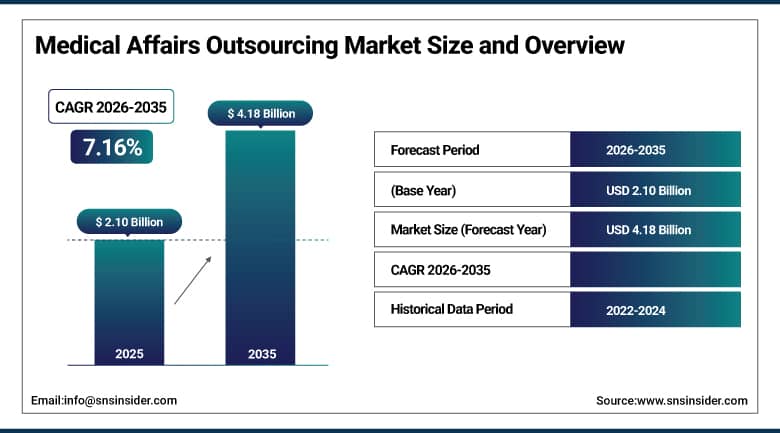

The Medical Affairs Outsourcing Market was valued at USD 2.10 billion in 2025 and is expected to reach USD 4.18 billion by 2035, growing at a CAGR of 7.16% from 2026–2035.

The medical affairs outsourcing market is witnessing strong growth in the global market owing to increasing complexity in drug development processes. Rising demand for regulatory compliance and scientific communication is supporting market expansion. Pharmaceutical and biotechnology firms are increasingly outsourcing medical affairs functions. Growing clinical trial activities and global research collaborations are creating new opportunities. Advancements in digital health platforms and real-world evidence generation are improving service efficiency. Increasing focus on cost optimization and faster product approvals is further accelerating adoption of medical affairs outsourcing services.

According to the U.S. Food and Drug Administration & Drug and Biologics approval database and the European Medicines Agency regulatory activity 2025, over 50% of global clinical trials now involve multi-regional trial designs requiring coordinated medical affairs support across jurisdictions.

According to the OECD’s health workforce statistics and WHO’s assessment on regulatory capacity, more than 70% of nations use external technical experts for pharmacovigilance and regulatory compliance due to low internal capacity. Moreover, according to FDA inspection reports, more than 60% of post-marketing safety reporting systems use external or hybrid medical affairs departments.

Market Size and Forecast:

-

Market Size 2026E: USD 2.24 billion

-

Market Size 2035: USD 4.18 billion

-

CAGR (2026 - 2035): 7.16%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Medical Affairs Outsourcing Market - Request Free Sample Report

Medical Affairs Outsourcing Market Trends:

-

Increasing adoption of outsourcing in medical affairs due to rising complexity of clinical trials and regulatory documentation requirements globally.

-

Growing reliance on biotechnology companies outsourcing regulatory affairs, pharmacovigilance, and medical writing for faster drug development processes.

-

Expanding demand for specialized outsourcing partners supporting rare disease research and orphan drug development across global pharmaceutical industries.

-

Rising use of digital medical affairs platforms improving efficiency in real world evidence generation and scientific communication services.

-

Increasing multi region clinical trials driving higher documentation workload and encouraging end to end medical affairs outsourcing adoption.

-

Strong focus on cost optimization and operational efficiency pushing pharmaceutical companies toward flexible project based outsourcing models worldwide.

U.S. Medical Affairs Outsourcing Market Outlook:

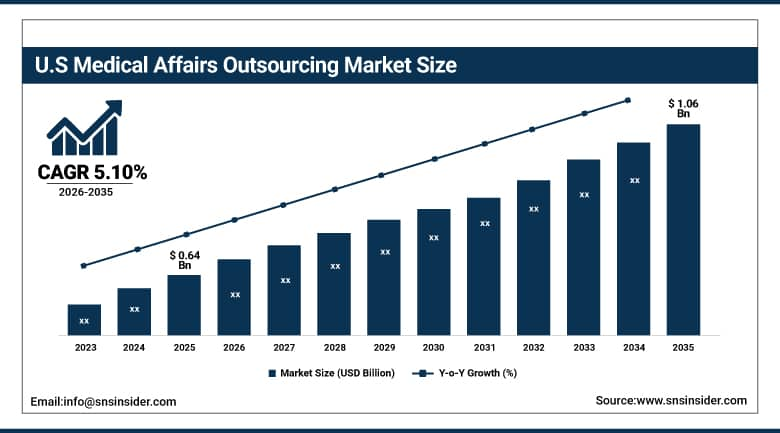

The U.S. Medical Affairs Outsourcing Market was valued at USD 0.64 billion in 2025 and is expected to reach around USD 1.06 billion by 2035, growing at a CAGR of 5.10% from 2026–2035.

The U.S. medical affairs outsourcing market is growing consistently owing to rising complexity in regulatory and clinical communication needs. Strong presence of pharmaceutical and biotechnology companies is supporting steady growth across healthcare industries. The use of outsourced medical writing, pharmacovigilance, and regulatory services has contributed to market expansion. Increasing focus on faster drug approvals and compliance efficiency has generated higher demand. Development of digital medical affairs platforms, real world evidence generation, and advanced outsourcing models is further driving market expansion.

According to the U.S. Food and Drug Administration & Drug Trials Snapshot program, over 60% of the U.S.-registered clinical trials in 2025 involve industry sponsors collaborating with external service providers for regulatory, clinical, or medical communications functions.

As per the U.S. Department of Health and Human Services and NIH clinical research reporting standards, more than 4,000 active interventional studies are currently ongoing in the United States, with oncology accounting for approximately 35% of all registered trials. Additionally, FDA guidance updates emphasize increased reliance on outsourced pharmacovigilance and real-world evidence generation in post-market surveillance activities.

Medical Affairs Outsourcing Market Segment Analysis:

-

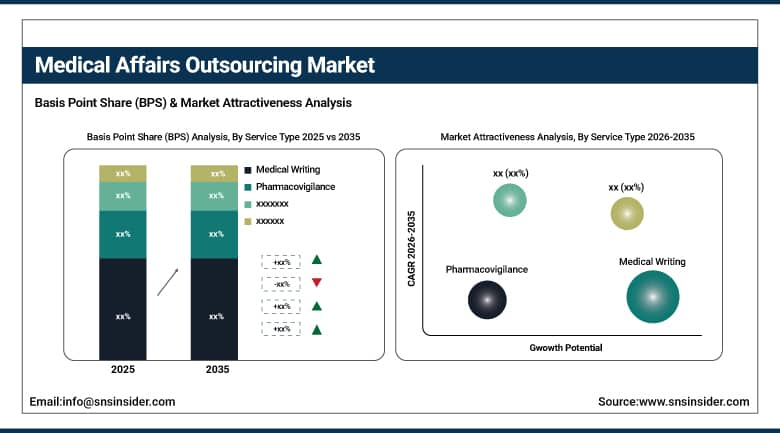

By Service Type, medical writing dominated the market with 31.45% share in 2025; while pharmacovigilance is the fastest growing segment with CAGR of 11.55% during 2026 to 2035.

-

By Therapeutic Area, oncology dominated the market with 33.87% share in 2025; while neurology is the fastest growing segment with CAGR of 10.99% during 2026 to 2035.

-

By Client Type, pharmaceutical companies dominated the market with 49.68% share in 2025; while biotechnology firms are the fastest growing segment with CAGR of 12.10% during 2026 to 2035.

-

By Engagement Model, full-service outsourcing dominated the market with 54.73% share in 2025; while project-based outsourcing is the fastest growing segment with CAGR of 12.23% during 2026 to 2035.

By Service Type, medical writing dominated the medical affairs outsourcing market, while pharmacovigilance is the fastest growing segment.

Medical writing segment has gained the dominated revenue share of the medical affairs outsourcing market in 2025 owing to the increase in the demand for regulatory submission and clinical documentation. Scientific writing plays an important role for pharmaceuticals and biotechnological companies to meet their requirements. The increase in the difficulty level of the clinical trials and the stringent regulations also support the growth of this segment. Standardization, high dependency, and increase in research publications will contribute to the dominance of this segment in the market.

Pharmacovigilance segment is likely to gain the fastest CAGR during the forecast period 2026 to 2035 owing to the increase in the focus of the market players on the drug safety monitoring and adverse event reporting in the global market. The increase in the regulatory pressure and post-marketing surveillance requirements also support the growth of this segment. Expansion in the clinical trials and the development of biologics leads to the increase in the safety information.

By Therapeutic Area, oncology dominated the medical affairs outsourcing market, while neurology is the fastest growing segment.

The oncology segment holds the dominated share of the medical affairs outsourcing market in terms of revenue in 2025. The high share is attributed to the high cancer burden in the world and ongoing oncology drug development pipelines. The growing number of clinical trials and sophisticated therapy protocols require significant support in medical affairs. Stringent regulations and requirement for real world evidence enhance the outsourcing need. High investments made by pharmaceutical companies in oncology research increase the demand for medical writing, pharmacovigilance, and regulatory communication.

The neurology segment has been projected to experience the fastest CAGR between 2026 and 2035 owing to increasing incidences of neurological disorders including Alzheimer’s, Parkinson’s, and Epilepsy. Increasing unmet medical needs along with limited treatment options drive the expansion in research. The growing investment in neurodegenerative diseases pipeline and advanced biologics enhance the outsourcing need.

By Client Type, pharmaceutical companies dominated the medical affairs outsourcing market, while biotechnology firms are the fastest growing segment.

The Pharmaceutical Companies segment held the dominated market share in the medical affairs outsourcing market in 2025 due to the huge number of drugs that undergo developmental processes in pipelines. Such firms have many needs for medical writing, pharmacovigilance, and regulations for global approvals. The high degree of dependence on outsourcing makes their operations efficient. Their high financial power and expansion of clinical trials make them dominate in the market.

The Biotechnology Firms segment is projected to register the fastest CAGR during the forecast period 2026-2035 because of the growing innovations in the areas of biologics and precision medicines. The increased use of outsourcing firms by biotech companies due to the need for cost effective medical affairs support makes this segment grow rapidly. The rapid expansion of pipelines and emphasis on clinical research collaborations increases the adoption rate.

By Engagement Model, full-service outsourcing dominated the medical affairs outsourcing market, while project-based outsourcing is the fastest growing segment.

Full-Service Outsourcing segment held the leading position in terms of the medical affairs outsourcing market share in 2025, owing to the capability of offering end-to-end integrated medical affairs solution packages. The need for companies to outsource their medical affairs activities through one company providing services related to medical writing, regulatory affairs, pharmacovigilance, and clinical communication makes companies choose full-service medical affairs outsourcing companies. Centralized outsourcing partner and cost-effective drug development also support its dominance.

Project-Based Outsourcing segment is expected to be the fastest-growing CAGR of the medical affairs outsourcing market between 2026 and 2035 owing to the increasing need for short-term and flexible medical affairs solutions. The need to outsource specific projects like regulatory submissions, product launches, and clinical documentation provides opportunities for cost control, scalability, and timely execution. The increasing use of project-based medical affairs outsourcing companies among biotech and small pharmaceutical companies drives the growth of project-based outsourcing services.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

73.45% |

|

Europe |

Germany |

28.60% |

|

Asia Pacific |

China |

41.70% |

|

Middle East & Africa |

UAE |

18.30% |

|

Latin America |

Brazil |

46.20% |

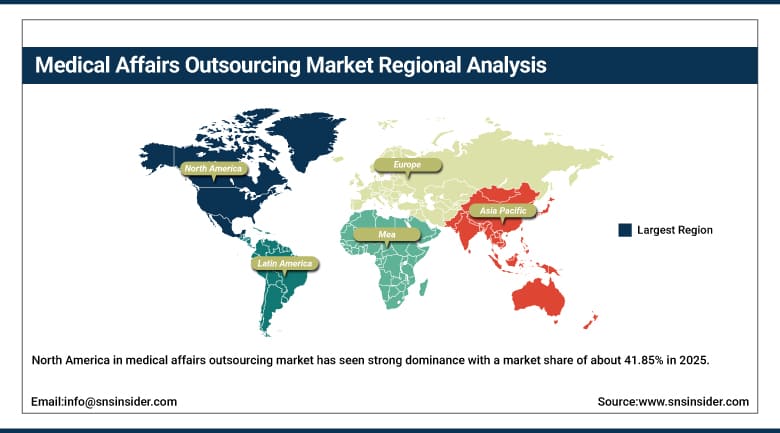

North America Medical Affairs Outsourcing Market Insights.

North America in medical affairs outsourcing market has seen strong dominance with a market share of about 41.85% in 2025 due to advanced pharmaceutical infrastructure and high outsourcing adoption. The region benefits from strong presence of global pharmaceutical and biotechnology companies. Increasing demand for regulatory compliance, medical writing, and pharmacovigilance services is driving expansion across the United States and Canada. Rising clinical trial activity and real-world evidence generation is further supporting market leadership. Strong digital health adoption and outsourcing partnerships are strengthening regional capabilities.

According to the U.S. Food and Drug Administration & Drug Trials Snapshots and clinical research governance updates, over 80% of registered clinical trials in the United States involve industry sponsors utilizing external contract research or outsourced support functions, including medical affairs activities, as of 2025.

According to the U.S. National Institutes of Health clinical research workforce, about 55% of clinical research operations are now carried out through decentralized or hybrid models, utilizing third-party service providers. Moreover, Health Canada regulatory modernization projects highlight that real-world evidence frameworks have been adopted by more than 60% of post-market surveillance systems, resulting in the outsourcing of medical communication and pharmacovigilance services in North America.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Medical Affairs Outsourcing Market Insights.

Europe medical affairs outsourcing market is characterized by steady growth in 2025 owing to strict regulatory frameworks and increasing clinical research activities. The major countries contributing include Germany, France, United Kingdom, and Switzerland. Rising demand for pharmacovigilance and regulatory documentation is fueling market growth. Increasing outsourcing by pharmaceutical companies for cost efficiency and compliance support is further supporting expansion. Strong presence of CROs and research institutions is propelling service adoption.

According to the European Commission eHealth Digital Service Infrastructure and the OECD Health Statistics of 2025, about 90% of the member states of the EU have adopted national electronic health records or health interoperability infrastructures that allow structured clinical research and outsourcing of medical affairs.

According to the U.S. National Institutes of Health, the clinical research workforce in the U.S. shows that about 55% of clinical research operations today rely on a distributed or hybrid system with third-party service vendors. Also, the regulatory modernization efforts at Health Canada show that real-world evidence is increasingly being adopted in more than 60% of the post-market surveillance programs.

Asia Pacific Medical Affairs Outsourcing Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the medical affairs outsourcing market during the forecast period, with an estimated growth rate of 9.70% in 2025. Rapid expansion of pharmaceutical manufacturing and clinical research activities is driving strong demand across China, India, Japan, South Korea, and Southeast Asia. Increasing adoption of cost-effective outsourcing models is further accelerating market growth. Rising biotechnology sector and expanding CRO presence are boosting service penetration. Growing clinical trial outsourcing and regulatory support demand are strengthening regional outlook.

As per WHO & Global Health Observatory 2025 and OECD Health Statistics reports, the share of Asia Pacific nations in the global population is over 60%, and they conduct close to 30% of all global clinical trials, with evidence-based healthcare systems expanding rapidly to support the Medical Affairs function. Per WHO indicators of digital health adoption, over 55% of the member countries of Asia Pacific have adopted national eHealth strategies with real-world evidence frameworks.

Middle East & Africa and Latin America Medical Affairs Outsourcing Market Insights.

The Middle East & Africa along with Latin American regions are experiencing steady growth due to expanding healthcare infrastructure and pharmaceutical development. Key contributing countries include Brazil, Mexico, Argentina, Saudi Arabia, United Arab Emirates, and South Africa. Increasing clinical research activities and growing pharmaceutical investments are supporting market growth. Rising demand for regulatory affairs and medical communication services is driving adoption. Expanding participation in global clinical trials is further enhancing outsourcing penetration across these regions. Limited in-house expertise and cost efficiency needs are also encouraging outsourcing adoption.

As per WHO Global Observatory on Health R&D, clinical trial participation in low- and middle-income regions has expanded by over 20% between recent reporting cycles, supporting outsourcing demand. In addition, FDA and EMA regulatory modernization frameworks show that more than 60% of multinational pharmaceutical sponsors now utilize outsourced medical affairs functions for regulatory communications and evidence generation across emerging markets.

Market Dynamics:

Growth Drivers: Increasing complexity of clinical trials and regulatory requirements driving outsourcing adoption globally

The growing complexity in clinical trials and regulation systems is leading to an increasing need for outsourced medical affairs services worldwide. The pharmaceutical industry is dealing with highly sophisticated treatments that involve biologic drugs and precision medicine. The treatments entail significant amount of writing, regulatory submission, and pharmacovigilance. There are constraints in terms of internal capabilities. There are pressures of increased workload as well. Outsourcing leads to increased efficiencies, precision in compliance, and faster approvals. Global multi-region clinical trials add to the documentation needs.

As stated by the FDA clinical trial monitoring framework in 2025 and the European Medicines Agency's yearly clinical trials report, over 70% of all worldwide clinical trials are currently being conducted at multiple-country locations owing to the growing complexity involved. As per the WHO International Clinical Trial Registry Platform, over 25,000 interventional studies have been registered throughout the world.

Restraints: High regulatory compliance burden and data complexity limiting outsourcing flexibility and adoption

High regulatory demands throughout global market places outsourced medical affairs in a difficult position to comply with these demands. Variations in regulations in various regions make the process of documentation more complicated and the likelihood of failing to comply higher. There are issues concerning data privacy, adverse event reporting, and audit preparedness. Quality maintenance within outsourced companies is difficult. Frequent regulatory changes demand ongoing compliance and training. All these factors restrain full scale outsourcing. Partial outsourcing is preferred as it ensures control over critical data and compliance with regulatory changes in regions.

Opportunities:Increasing growth of biotechnology sector and rare disease research expanding outsourcing demand globally

The rapid growth in biotechnology companies and studies on rare diseases is creating good outsourcing chances in the field of medical affairs. These organizations do not have a large number of medical affairs teams within them. The advantages of outsourcing include the availability of expertise in areas such as regulatory affairs, clinical communications, and pharmacovigilance. With the emphasis increasing on orphan drugs and personalized medicine, there is an increased need for documentation and regulation at the global level. Biotechnology companies are highly reliant on outsourcing to develop their products rapidly.

According to U.S. Food and Drug Administration & Orphan Drug Designations and Approvals 2025, there have been more than 5,000 orphan drug designations, of which more than 60% are found in biotech drugs. According to WHO global health observatory data, there are more than 7,000 rare diseases impacting 3.5% to 5.9% of the world’s population.

Recent Developments:

-

2026: ICON plc focused on operational restructuring initiatives and leadership-driven efficiency programs amid evolving global clinical outsourcing demand landscape.

-

2025: IQVIA announced strategic collaboration with AWS, naming it preferred agentic cloud provider to accelerate clinical trial automation and healthcare analytics globally.

-

2025: Syneos Health advanced integrated clinical and commercial outsourcing services, focusing on AI-enabled trial optimization and data-driven medical affairs solutions.

-

2024: ICON plc advanced decentralized clinical trial solutions and digital patient engagement technologies across global studies.

Medical Affairs Outsourcing Market Key Players are:

-

IQVIA

-

ICON plc

-

Syneos Health

-

Parexel

-

Fortrea

-

Thermo Fisher Scientific

-

EVERSANA

-

Inizio Medical

-

Adelphi Group

-

OPEN Health

-

Nucleus Global

-

Envision Pharma Group

-

Certara

-

Medpace

-

Real Chemistry

-

IPG Health

-

Publicis Health

-

Havas Health & You

-

Cactus Communications

-

Veeva Systems

Medical Affairs Outsourcing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.10 Billion |

| Market Size by 2035 | USD 4.18 Billion |

| CAGR | CAGR of 7.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Medical Writing, Regulatory Affairs, Pharmacovigilance, Clinical Trial Management, Consulting Services) • By Therapeutic Area (Oncology, Cardiology, Neurology, Infectious Diseases, Diabetes) • By Client Type (Pharmaceutical Companies, Biotechnology Firms, Medical Affairs Outsourcing Market Manufacturers, Contract Research Organizations) • By Engagement Model (Full-Service Outsourcing, Functional Outsourcing, Project-Based Outsourcing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IQVIA, ICON plc, Syneos Health, Parexel, Fortrea, Thermo Fisher Scientific, EVERSANA, Inizio Medical, Adelphi Group, OPEN Health, Nucleus Global, Envision Pharma Group, Certara, Medpace, Real Chemistry, IPG Health, Publicis Health, Havas Health & You, Cactus Communications, Veeva Systems |

Frequently Asked Questions

The medical affairs outsourcing market is expected to grow at a CAGR of 7.16% from 2026 to 2035.

The medical affairs outsourcing market was valued at USD 2.10 billion in 2025.

Major growth factors include increasing clinical trial complexity, regulatory requirements, rising pharmacovigilance and medical writing demand, expansion of multi region studies, real world evidence adoption, and outsourcing for cost efficiency.

Medical Writing dominated in 2025 due to strong demand for regulatory submissions, clinical documentation, and scientific communication supporting drug approvals.

North America dominated in 2025 due to strong pharma biotech presence, clinical trials, outsourcing adoption, and robust regulatory infrastructure.

Get in Touch