Medical Device Contract Manufacturing Market Report Scope & Overview:

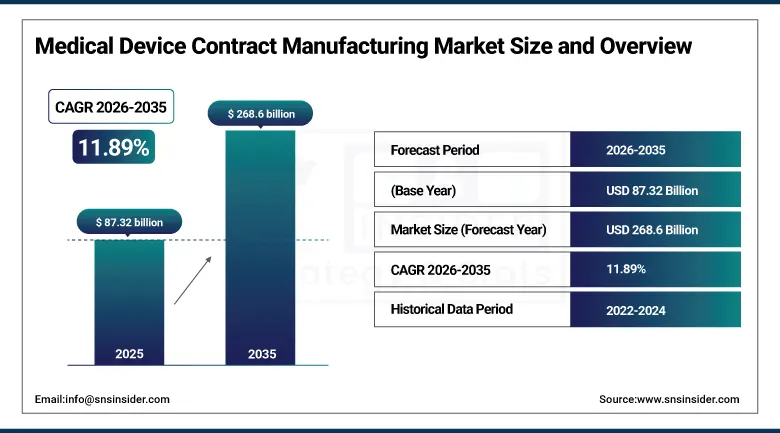

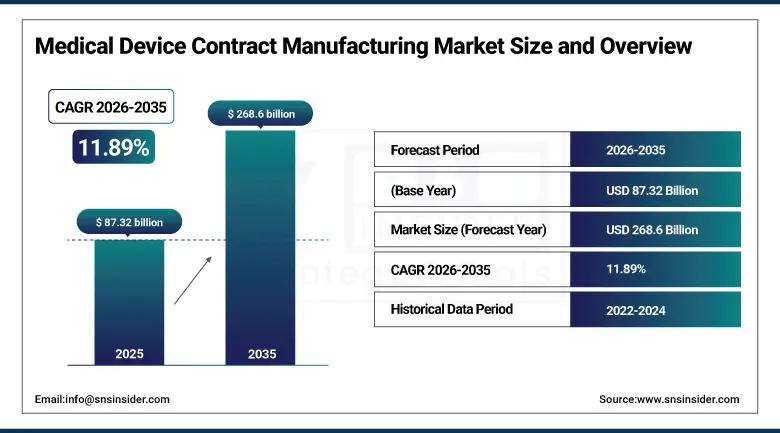

The Medical Device Contract Manufacturing Market was valued at USD 87.32 Billion in 2025 and is expected to reach USD 268.6 Billion by 2035, growing at a CAGR of 11.89% from 2026–2035.

The global medical device contract manufacturing market is advancing as original equipment manufacturers progressively outsource production to specialized contract manufacturers whose precision engineering capabilities, regulatory expertise, automated assembly infrastructure, and economies of scale create quality and cost outcomes that in-house manufacturing cannot replicate efficiently. Contract manufacturing enables device OEMs to accelerate time-to-market by leveraging established cleanroom manufacturing infrastructure, pre-qualified sterilization services, and regulatory compliance frameworks rather than investing capital in dedicated manufacturing facilities whose fixed cost base creates competitive disadvantage at lower production volumes. Contract manufacturers’ integration of automation, robotics, AI-driven quality monitoring, and 3D printing creates manufacturing sophistication that sustains above-average market growth.

In February 2025, Arterex acquired Phoenix S.r.l., a leading Italian medical device solution provider, expanding its presence in Europe and enhancing capabilities in medical device development, finished device assembly, and packaging. The acquisition reflected the consolidation trend among top-tier medical device contract manufacturers seeking European market presence to serve the growing EU MDR compliance-driven outsourcing demand from OEMs whose European market access requires manufacturer certification that established European CMOs can efficiently provide without duplicate facility qualification investment.

Market Size and Forecast

-

Market Size in 2026E: USD 97.72 Billion

-

Market Size by 2035: USD 268.6 Billion

-

CAGR: 11.89% from 2026 to 2035

-

Fastest Growing Region: North America

-

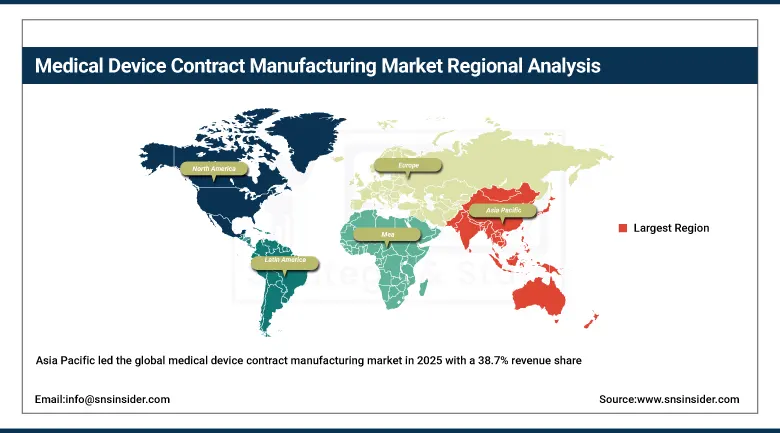

Largest Region: Asia Pacific

To Get more information on Medical Device Contract Manufacturing Market - Request Free Sample Report

Medical Device Contract Manufacturing Market Trends

-

AI-driven quality control and real-time production monitoring are reducing defect rates and enabling predictive maintenance in high-volume device assembly.

-

3D printing adoption in contract manufacturing is enabling rapid prototyping and small-batch production of complex implant and surgical device geometries.

-

EU MDR and US FDA regulatory compliance complexity is driving OEM outsourcing to CMOs with established quality management system infrastructure.

-

Robotic automation integration in precision component assembly is improving throughput consistency while reducing per-unit labour cost across high-volume device categories.

-

Near-shoring of medical device manufacturing from Asia to North America and Eastern Europe is creating new CMO capacity investment in proximity to major OEM headquarters.

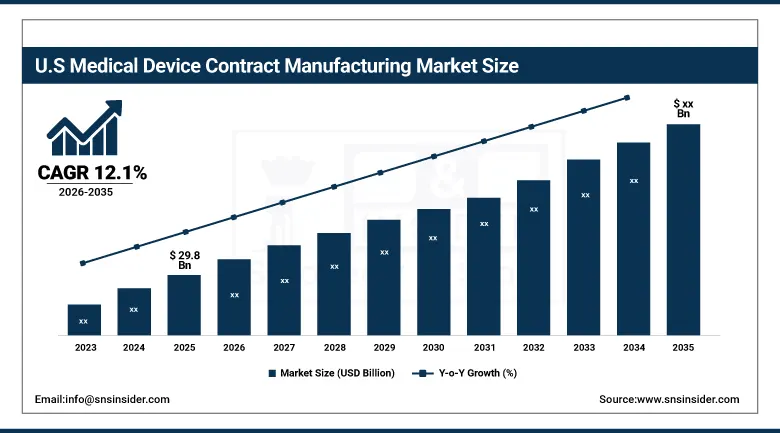

The U.S. Medical Device Contract Manufacturing Market Outlook

The U.S. Medical Device Contract Manufacturing Market was valued at approximately USD 29.8 Billion in 2025 and is expected to grow significantly through 2035, expanding at a CAGR of approximately 12.1% from 2026–2035.

The United States leads North American medical device contract manufacturing through its world-leading OEM customer base including Medtronic, Abbott, Boston Scientific, and Becton Dickinson whose outsourcing programmes create the most commercially significant CMO procurement in the global market. FDA’s stringent 21 CFR Part 820 Quality System Regulation requirements and the transition to ISO 13485:2016-aligned Device Quality Regulation create compliance investment that sustains premium contract manufacturer engagement. Jabil Healthcare, Flex Medical, and Plexus Corp sustain U.S. CMO market leadership through FDA-registered facilities and established design transfer expertise.

In January 2025, Integer Holdings acquired Pulse Technologies for USD 140 million, enhancing its precision machining and coating offerings for cardiovascular and other implantable device applications. The acquisition demonstrated the strategic value of precision manufacturing capability in the medical device CMO sector, where specialized machining, surface treatment, and coating expertise for implantable components creates commercial differentiation that justifies acquisition premium above commodity assembly capability valuations in the consolidating contract manufacturing landscape.

Medical Device Contract Manufacturing Market Segment Analysis

-

By Service Type, device development & manufacturing segment dominated the medical device contract manufacturing market with approximately 54.3% share in 2025, while quality management & testing is the fastest growing service with a CAGR of approximately 14.4%.

-

By Device Type, diagnostic & in-vitro diagnostic devices segment dominated the medical device contract manufacturing market with approximately 28.2% share in 2025, while drug delivery devices is the fastest growing device type with a CAGR of approximately 12.4%.

-

By End Use, original equipment manufacturers (OEMs) segment dominated the medical device contract manufacturing market with approximately 67% market share in 2025, While pharmaceutical & biopharmaceutical companies segment is projected to register the fastest CAGR of around 11.8% during 2026–2035

By Service Type, device development & manufacturing dominates, quality management grows fastest

Device development and manufacturing retained the dominant service position with approximately 54.3% of the medical device contract manufacturing market in 2025. Its commercial primacy reflects the comprehensive scope of end-to-end manufacturing services that OEMs require when outsourcing production, where a single CMO relationship spanning design transfer, process validation, pilot production, and commercial-scale manufacturing creates a turnkey manufacturing solution whose integrated accountability reduces the coordination complexity and quality risk of multi-vendor production arrangements. Full-service contract manufacturers including Jabil, Flex, and Celestica whose cleanroom assembly, precision component machining, finished device assembly, and regulatory documentation capabilities span the complete manufacturing scope from component procurement to finished device release create the most commercially valued CMO relationships in the market, commanding premium pricing through their comprehensive capability coverage.

Quality management and testing services are growing fastest at approximately 14.4% CAGR because the progressive tightening of medical device regulatory requirements under EU MDR, FDA’s enhanced inspection programmes, and the expansion of quality management system requirements across global medical device markets creates non-discretionary outsourcing demand for specialized testing, validation, and compliance documentation services. Each new regulatory requirement whose compliance demands specialized analytical equipment, validated testing protocols, and expert regulatory documentation creates CMO quality service procurement that OEMs without in-house capability must source from qualified contract service providers.

By Device Type, IVD devices dominate, drug delivery devices grow fastest

Diagnostic and in-vitro diagnostic devices retained the dominant device type position with approximately 28.2% of the medical device contract manufacturing market in 2025. The extraordinary scale of global IVD test consumption, whose COVID-19 pandemic acceleration created lasting installed base expansion across lateral flow, PCR, and clinical chemistry diagnostic platforms, sustains the largest aggregate medical device contract manufacturing volume in the sector. IVD device contract manufacturing encompasses the precision automated assembly of cartridge and cassette formats, the calibrated dispensing of biological reagents, the quality-controlled packaging in humidity-controlled environments, and the lot release testing whose combined requirements create complex manufacturing programmes that specialized CMOs serve more efficiently than OEM captive facilities.

Drug delivery devices are growing fastest at approximately 12.4% CAGR because the biologics and biosimilar market’s expansion creates growing demand for the auto-injectors, pen injectors, pre-fillable syringes, and inhalation delivery devices whose manufacturing precision, material biocompatibility requirements, and regulatory drug-device combination product classification create specialized CMO capability demand. Each new biologic therapy approved requiring a primary container closure system or drug delivery device creates a long-term CMO supply relationship whose sustained commercial value scales with the therapy’s patient population.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

52.4% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

43.8% |

Asia Pacific Medical Device Contract Manufacturing Market Insights

Asia Pacific led the global medical device contract manufacturing market in 2025 with a 38.7% revenue share through its cost-effective manufacturing infrastructure, highly skilled precision engineering workforce, and sophisticated cleanroom assembly capability in China, Singapore, Malaysia, Thailand, and India. China accounts for approximately 52.4% of Asia Pacific revenues through its scale of medical device manufacturing at global export volumes, the concentration of OEM manufacturing partnerships, and growing domestic medical device consumption creating near-market production motivation.

India is the most commercially dynamic emerging market within Asia Pacific, where growing OEM cost optimization outsourcing, the domestic medical device manufacturing investment under Make in India policy, and the expanding clinical market’s device demand create above-regional-average CMO procurement growth. Singapore and Malaysia’s advanced cleanroom manufacturing infrastructure and regulatory compliance frameworks sustain premium regional CMO capability for high-value precision device manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Medical Device Contract Manufacturing Market Insights

North America is the fastest-growing regional medical device contract manufacturing market, driven by OEM outsourcing expansion among leading U.S. device companies, near-shoring investment driven by supply chain resilience priorities, and the growing complexity of regulatory compliance creating CMO engagement above vertically integrated production capability. The United States accounts for approximately 82.5% of North American revenues through Jabil Healthcare, Flex Medical, Integer Holdings, and Plexus Corp’s dominant CMO market position.

Canada contributes supplementary North American revenues through its growing medical device manufacturing sector’s CMO engagement, the pharmaceutical packaging and drug delivery device manufacturing capability of Ontario-based contract manufacturers, and the growing biotechnology sector’s biologic drug delivery device procurement from Canadian CMO partners with Health Canada regulatory expertise.

Europe Medical Device Contract Manufacturing Market Insights

Europe is a technically sophisticated medical device contract manufacturing market where EU MDR’s stringent post-market surveillance, clinical evidence, and quality management system requirements are creating regulatory-driven outsourcing to certified CMOs whose established notified body relationships and EU MDR-compliant quality system infrastructure reduce OEM compliance burden. Germany accounts for approximately 22.4% of European revenues through its large medical device industry’s precision engineering CMO engagement and the commercial presence of Freudenberg Medical and Micro Systems Technologies.

Ireland, Switzerland, and the Czech Republic contribute significant secondary European CMO market revenues through their attractive medical device manufacturing investment environments, established multinational OEM presence creating local CMO demand, and growing precision engineering and cleanroom assembly capability. The EU’s ongoing medical device regulatory harmonization and the gradual expansion of EU MDR compliance deadlines create consistent compliance-driven CMO service procurement.

MEA & Latin America Medical Device Contract Manufacturing Market Insights

Israel leads MEA revenues through its world-class medical technology industry’s precision manufacturing capability, the defense sector’s advanced manufacturing technology transfer into medical device production, and the growing domestic medical device export sector’s CMO engagement. South Africa and the UAE contribute growing regional demand through healthcare infrastructure investment creating domestic device procurement.

Brazil leads Latin American revenues through its large domestic medical device market’s growing CMO engagement, the ANVISA regulatory framework’s compliance requirements creating outsourcing motivation, and the growing pharmaceutical and medical device manufacturing sector’s domestic capacity investment. Mexico’s proximity to U.S. OEM headquarters and the maquiladora manufacturing infrastructure create growing medical device CMO activity.

Market Dynamics

Growth Drivers: OEM outsourcing acceleration driven by regulatory complexity and device technology advancement requiring specialized CMO capabilities

The medical device contract manufacturing market’s growth is driven by OEMs’ systematic evaluation of their manufacturing portfolios whose outcome progressively favors outsourcing to specialized CMOs whose regulatory compliance infrastructure, precision manufacturing capability, and economies of scale create quality and cost outcomes exceeding captive facility performance. Each new medical device regulatory requirement whose compliance demands specialized quality management system elements, validated testing protocols, or documented clinical evidence creates outsourcing motivation for OEMs whose regulatory staff and manufacturing operations cannot efficiently maintain simultaneous competency across multiple regulatory jurisdictions.

Device technology advancement in areas including next-generation implants with electronic function, connected health monitoring devices requiring integrated circuit assembly, and combination drug-device products requiring pharmaceutical manufacturing capability creates CMO engagement beyond conventional assembly expertise into specialized technical domains. Each OEM product line entering technically complex device categories whose manufacturing requirements exceed existing captive production infrastructure creates new CMO relationship formation whose long-term supply agreement value scales with product lifecycle.

Restraints: Intellectual property protection concerns and high quality system qualification investment creating barriers to CMO engagement for proprietary device OEMs

Medical device OEMs’ concern about proprietary design and process intellectual property protection when transferring production to external contract manufacturers creates a significant adoption barrier whose severity is greatest for novel device technologies whose market exclusivity depends on maintaining manufacturing know-how confidentiality. Each OEM whose competitive advantage rests on proprietary manufacturing process rather than purely design IP creates reluctance to transfer production to CMOs whose other customer relationships create potential knowledge transfer exposure across competitive device programmes.

The substantial investment required to qualify medical device contract manufacturing facilities, where FDA 21 CFR Part 820 quality system verification, ISO 13485 audit clearance, and product-specific process validation collectively require months of documentation, testing, and regulatory submission before first commercial lot release, creates switching cost that both constrains new CMO relationship formation and sustains existing relationships beyond their optimal commercial terms. Each qualification investment whose sunk cost accumulates across multiple vendor assessments, process validations, and regulatory submissions creates procurement inertia.

Opportunities: Near-shoring investment and advanced manufacturing technology integration creating premium medical device CMO capability differentiation

Medical device manufacturing near-shoring represents the most commercially significant new CMO capacity investment trend, where OEMs’ pandemic-era supply chain disruption experience motivates regional production diversification from Asian concentrated manufacturing toward North American and European CMO capacity that offers geographical supply security at acceptable cost premium. Each OEM that establishes a near-shore CMO relationship for its highest-criticality device supply creates a procurement diversification that sustains new CMO facility investment in North American and Eastern European manufacturing locations.

Advanced manufacturing technology integration, including AI-powered vision inspection systems achieving sub-micrometre detection of dimensional defects, collaborative robot assembly enabling flexible production line reconfiguration for changing product mix, and additive manufacturing enabling complex implant geometry production without conventional tooling cost, creates technical differentiation among leading CMOs whose capability investment creates commercial premium above commodity assembly capacity pricing. Each CMO that successfully documents AI quality system performance improvement through validated statistical process control creates customer value justifying premium pricing.

Recent Developments:

-

2025: Arterex acquired Phoenix S.r.l., a leading Italian medical device solution provider, expanding its European presence and enhancing capabilities in device development, finished device assembly, and regulatory packaging for the EU MDR compliance-driven outsourcing market.

-

2025: Integer Holdings acquired Pulse Technologies for USD 140 million, enhancing precision machining and coating capabilities for cardiovascular and implantable device applications and strengthening Integer’s end-to-end development capabilities for high-complexity device programmes.

-

2024: Kimball Electronics received the 2024 Service Excellence Award from CIRCUITS ASSEMBLY for achieving highest customer ratings across manufacturing quality, technology, dependability, and value, demonstrating the commercial differentiation that quality management system excellence creates in medical device CMO customer retention.

Medical Device Contract Manufacturing Market Key Players are:

-

Jabil Inc. (Jabil Healthcare)

-

Flex Ltd. (Flex Medical)

-

Plexus Corp.

-

Integer Holdings Corporation

-

Celestica Inc.

-

Kimball Electronics Inc.

-

Tecomet Inc.

-

Nordson MEDICAL

-

Resonetics LLC

-

Freudenberg Medical GmbH

-

Confluent Medical Technologies

-

Minnetronix Medical Inc.

-

Lake Region Medical (Integer)

-

Tegra Medical LLC

-

Micro Systems Technologies GmbH

-

Arterex Medical Solutions

-

IEC Electronics Corp.

-

SurModics Inc.

-

Phillips-Medisize (Molex)

-

Viant Medical LLC

Medical Device Contract Manufacturing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 87.32 Billion |

| Market Size by 2035 | USD 268.6 Billion |

| CAGR | CAGR of 11.89% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Device Development & Manufacturing, Finished Device Assembly, Precision Components & Sub-Assemblies, Sterilization Services, Quality Management & Testing) • By Device Type (Cardiovascular Devices, Diagnostic & In-Vitro Diagnostic Devices, Drug Delivery Devices, Orthopedic Devices, Surgical Instruments, Others) • By End Use (Original Equipment Manufacturers (OEMs), Pharmaceutical & Biopharmaceutical Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Jabil Inc. (Jabil Healthcare), Flex Ltd. (Flex Medical), Plexus Corp., Integer Holdings Corporation, Celestica Inc., Kimball Electronics Inc., Tecomet Inc., Nordson MEDICAL, Resonetics LLC, Freudenberg Medical GmbH, Confluent Medical Technologies, Minnetronix Medical Inc., Lake Region Medical (Integer), Tegra Medical LLC, Micro Systems Technologies GmbH, Arterex Medical Solutions, IEC Electronics Corp., SurModics Inc., Phillips-Medisize (Molex), and Viant Medical LLC |

Frequently Asked Questions

The Medical Device Contract Manufacturing Market is expected to grow at a CAGR of 11.89% from 2026 to 2035.

The Medical Device Contract Manufacturing Market was valued at USD 87.32 Billion in 2025.

OEM outsourcing acceleration driven by regulatory compliance complexity, device technology advancement requiring specialized CMO capabilities, near-shoring investment for supply chain resilience, and advanced manufacturing technology integration are the primary growth factors.

Device Development & Manufacturing dominated with approximately 54.3% share in 2025, while Quality Management & Testing is the fastest growing service at approximately 14.4% CAGR.

Asia Pacific dominated the Medical Device Contract Manufacturing Market in 2025 with 38.7% revenue share.

Get in Touch