CT/NG Testing Market Size & Trends

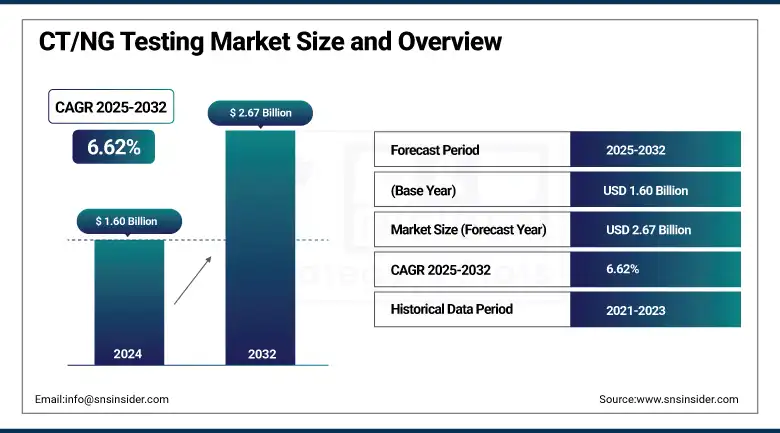

The CT/NG Testing Market size was valued at USD 1.60 billion in 2024 and is expected to reach USD 2.67 billion by 2032 and grow at a CAGR of 6.62% over the forecast period of 2025-2032.

The CT/NG testing market is growing steadily because of the increasing prevalence of sexually transmitted infections (STIs), growing awareness among patients, and expanding screening programs. Nucleic acid amplification tests (NAATs) have been found to improve the early identification and treatment of these cases, along with the increasing use of point-of-care diagnostics. Rising Self-Testing and Government-Supported Screening Programs Increasing CT/NG testing market growth.

To Get more information On CT NG Testing Market - Request Free Sample Report

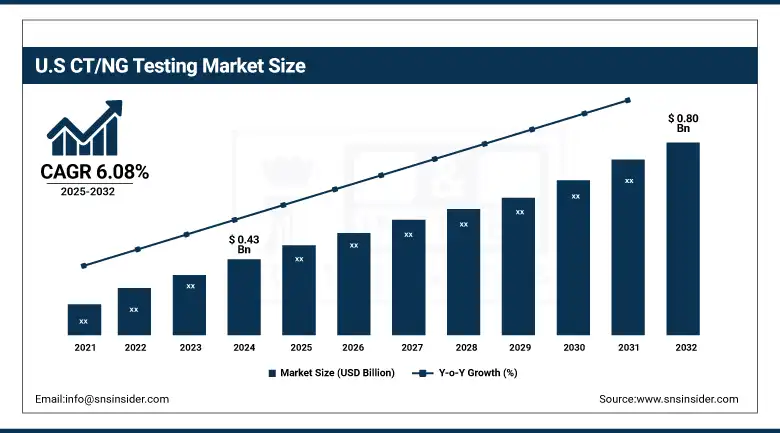

The U.S. CT/NG testing market size was valued at USD 0.43 billion in 2024 and is expected to reach USD 0.80 billion by 2032, growing at a CAGR of 6.08% over the forecast period of 2025-2032. North America CT/NG testing market share for the U.S. is high owing to high volume testing, a well-developed diagnostic infrastructure, along public health programs. Active STI surveillance and national screening programs are contributing to an increase in early detection and diffusion of testing within medical practice.

Chlamydia and gonorrhea are also the first and second most commonly reported STIs in the US, with approximately 1.6 million cases of chlamydia and 601,319 cases of gonorrhea in 2023, respectively.

CT/NG Testing Market Dynamics

Drivers

-

The Growing Incidence of STIs is Boosting the Market Expansion

Increased incidence rates of sexually transmitted infections globally, particularly for Chlamydia trachomatis (CT) and Neisseria gonorrhoeae (NG), are a key factor fueling demand in the CT/NG testing market. Due to many shifting sexual practices, ignorance, and inadequate preventive measures, they all add up to a higher incidence of disease. Many cases of these infections remain undiagnosed because they often do not cause any symptoms, or the symptoms are mild; however, these infections can lead to serious complications, such as infertility, pelvic inflammatory disease, and increased risk of human immunodeficiency virus (HIV) acquisition and transmission. The increasing burden of these diseases results in high demand for accurate, early diagnostic testing to allow treatment before the wider spread of the disease.

Globally in 2020, among people aged 15 to 49 years, more than 374 million new infections with curable sexually transmitted infections (STIs) were recorded each year, with Chlamydia trachomatis and Neisseria gonorrhoeae as two examples.

Based on data from 188 studies, a global meta-analysis published in 2024 estimated the pooled prevalence of gonorrhea among adults aged 15 to 49 was 7.2% and chlamydia at 9.9%.

-

Government Initiatives and Screening Programs are Benefiting the Market to Grow

Public health organisations and governments are currently working on strategies to initiate control over the transmission of STIs by introducing routine screening and early diagnosis. For instance, the CDC's National Chlamydia Screening Program in the United States offers grants and guidelines for testing and campaigns to promote testing among high-risk populations, including sexually active young adults. Hence, these efforts supplement the volume of tests and offer new technologies for adoption in diagnosis, thereby contributing to the growth of the CT/NG testing market. The public health policies emphasizing STI control also allow for optimal resource utilization and infrastructure at all levels for the provision of testing facilities.

CDC advocates for STI prevention funding and guidelines, including the National Chlamydia Screening Program, which has been especially effective in increasing the proportion of young people tested.

According to the National Committee for Quality Assurance (NCQA), annual chlamydia screening rates for women ages 16–24 who are sexually active have increased dramatically among commercial HMOs since 2001, growing by 111% by 2023.

Restraint

-

Fewer Awareness and Stigma are Hampering the Market Expansion

The stigma surrounding STIs (sexually transmitted infections diagnostics) discourages many people from being tested for CT and NG infections. STIs are taboo in many cultures, which creates stigma, embarrassment, and in some cases, fear of being judged. Such stigma prevents people from getting tested and treated, even when they have symptoms or are knowingly at high risk of infection. Moreover, poor sexual health education contributes to not knowing about screening in the first place, which this valid in young adults and the present high-risk population. All of these factors lead to underdiagnosis and underreporting, and combined, they limit the growth factors of the market as they reduce the overall demand for the CT/NG testing services.

CT/NG Testing Market Segmentation Analysis

By Product Type

The Assays & Kits segment dominated the CT/NG testing market share with an 84.11% market share in 2024, owing to their importance in the accurate and rapid detection of infections. Since the kits offer high sensitivity and specificity, they are the most common type of kit that is used in various kinds of healthcare settings, otherwise diagnostic laboratories otherwise applied point-of-care sites. Molecular diagnostics have paved new avenues with their rapidity, ability to interface with various testing platforms, and multiplex assay systems for simultaneous diagnosis of both Chlamydia trachomatis and Neisseria gonorrhoeae, thus establishing them as the gold standards for large-scale screening programs and routine diagnostics globally.

The Instruments/Analyzers segment is expected to register the fastest growth throughout the forecasting period, due to the technological innovations and increased use of automated and high-throughput testing platforms. Modern analyzers increase the efficiency of testing by reducing the overall turnaround time and decreasing the chances of human error, playing a key role in handling rising volumes of tests. In addition, the high demand for POC and decentralized testing solutions is further stimulating the investments for miniaturized, portable instruments that can gain rapid and reliable results, thus propelling this segment's growth.

By Test Type

The laboratory testing segment dominated the CT/NG testing market with an 89.5% market share in 2024, due to accuracy, reliability, and sample volume handling. Although such methods are more demanding and require trained personnel, modern NAATs, which have become the mainstream in centralized laboratories, provide very sensitive and specific results and, due to their advantages of more reliable detection, are generally considered key for confirmatory diagnosis and applicable in routine screening programs. It also ensures quality control and full reporting through already established infrastructure and trained manpower in laboratories to facilitate its widespread application in hospitals and diagnostic centers.

The fastest-growing segment is predicted to be Point-of-Care (POC) Testing, owing to the rising need for rapid on-site diagnostics. POC tests have the benefit of rapid turnaround times, leading to early clinical decision-making and antimicrobial initiation, particularly valuable in resource-limited and remote locations. POC tests adoption is driven by increasing awareness towards sexual health, convenience, and decentralization of healthcare models, and growing advancements in technology, making POC tests more accurate for ease of use, in turn fueling market growth.

By Technology

The PCR segment dominated the CT/NG testing market with a 68.06% market share in 2024 due to the high sensitivity, specificity, and high adoption rate of PCR-based tests as a gold standard for Chlamydia trachomatis and Neisseria gonorrhoeae infections. The PCR technology, being highly specific, can amplify even in small quantities the genetic material that is specific for a particular organism, and thus, early and almost accurate diagnosis can be made for very low bacterial load, having the same genetic material for amplification. PCR's established role in clinical laboratories, multiplex testing options, and strong regulatory approvals have positioned it as the global preferred method for large-scale screening and confirmatory testing.

The isothermal nucleic acid amplification technology segment is anticipated to experience the fastest growth through the forecast period, owing to rapid, cheap, and easy alternatives to conventional PCR. Their work isothermally at a constant temperature, thus not requiring expensive thermal cyclers, making them suitable for point-of-care and resource-limited settings. The increasing need for rapid turnaround times, portable devices, and point-of-use testing has helped propel isothermal amplification for significant growth in the CT/NG testing space.

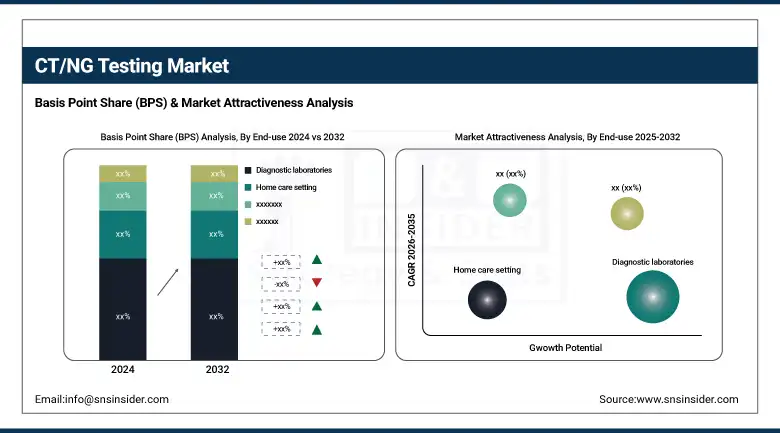

By End-use

The 2024 CT/NG testing market, dominated by the diagnostic laboratories segment with a 56.8% market share in 2024, due to a unique infrastructure that is beneficial when conducting simplex & multiplex CT/NG tests, along with increased capacity for testing and higher expertise in complex molecular diagnostics. Such laboratories are situated in a central configuration and can process thousands of samples by automated nucleic acid amplification tests (NAATs) to yield accurate results. As such, their capacity to underpin population screening programs and liaise with public health authorities renders them a key pillar in the detection and management of CT and NG.

During the forecast period, the hospitals & clinics segment is expected to record the fastest growth due to the rising incorporation of on-site testing & rapid diagnostics in clinical laboratories. It is important in treating STIs that hospitals expand their facilities to offer immediate testing and that patients get immediate results and diagnosis. Moreover, the increasing outpatient clinic population, increasing promotional awareness towards sexual health, and growing expenditures in healthcare infrastructure are making a significant contribution to the adoption of CT/NG testing services in hospitals and clinics, thereby rapidly driving the market growth.

CT/NG Testing Market Regional Insights

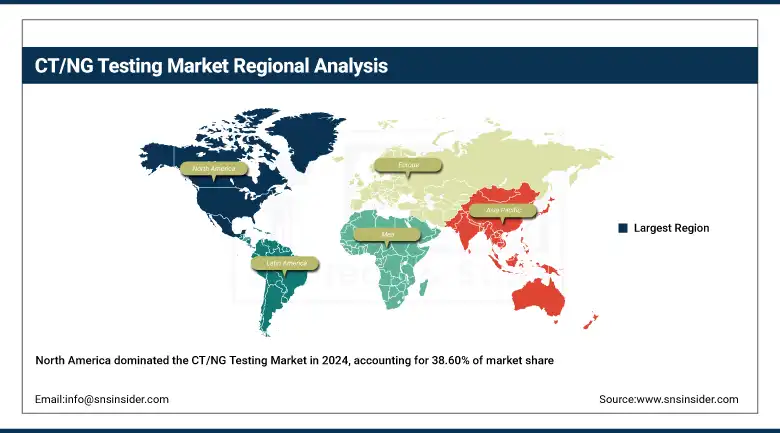

The CT/NG testing market is dominated in North America with a 38.60% market share in 2024, due to strong healthcare systems, higher inclination toward STI awareness, and solid routine screening programs. Some of these emerging trends are also driven by government efforts, including STI prevention strategies promoted by the Centers for Disease Control and Prevention (CDC), which advocate testing and prompt detection, especially among high-risk populations. In addition, the increasingly fast adoption of molecular diagnostic technologies such as nucleic acid amplification tests (NAATs) and the well-established reimbursement policies to ensure patient access to testing also favour the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

The CT/NG testing market in Asia Pacific is projected to be the fastest-growing region with a 7.45% CAGR over the forecast years due to the rising prevalence of STIs, improving access to healthcare, and increasing awareness about sexual health. The increasing disease burden due to urbanization, shifting sexual behavior and poorer early detection has led to governments strengthening diagnostic capabilities. Increasing investments in public health infrastructure and affordability of testing (including rapid point-of-care diagnostics, particularly in China, India, and Southeast Asian countries) will also be seen as positive developments in the region.

The CT/NG testing market in Europe is growing at a lucrative rate, due to the presence of strong public health policies and comprehensive screening programs. National programs or initiatives, as seen in the UK, for instance, with a National Chlamydia and Gonorrhea Screening Program, have already significantly increased re-testing and early diagnosis. European governments are also increasing sexual health infrastructure and education to help curb the spread of sexually transmitted infections (STIs). Quality diagnostic standards harmonized at the EU level through effective regulatory frameworks can further facilitate the expansion of this market and the uptake of enhanced testing technologies.

Latin America has boosted investments in STI diagnostics, a trend that continues to grow steadily. The lack of infrastructure and the fragmented regulation between nations prevent rapid growth from occurring, creating constant but slow momentum. Public health campaigns are promoting awareness and demand for testing in urban areas, targeting young and at-risk populations. Access remains a challenge, particularly in funded communities and among rural and high-need communities, where diagnostic access is often out of reach.

MEA is experiencing moderate growth in the CT/NG testing market due to Governments in MEA having been introducing tiered CT/NG screening alongside wider public health initiatives. However, the lack of overall health systems and the delayed adoption of advanced diagnostics are limiting growth to a more regional level compared to other regions. Expansion of testing services in high-prevalence areas is being facilitated by international aid programs and NGO Support. Nevertheless, sociocultural constraints and STI stigma in some countries are limiting the reach of screening and education.

Key Players in the CT/NG Testing Market

Abbott Laboratories, Becton, Dickinson & Company (BD), Danaher Corporation, F. Hoffmann-La Roche Ltd., Hologic, Inc., Thermo Fisher Scientific, Inc., Qiagen N.V., Siemens Healthineers AG, Bio-Rad Laboratories, Inc., Binx Health, and other players.

Recent Developments in the CT/NG Testing Market

-

January 2024 – Qiagen N.V. was FDA cleared for its NeuMoDx CT/NG Assay 2.0, which is intended to enhance sexually transmitted infection (STI) testing, especially Chlamydia trachomatis and Neisseria gonorrhoeae. The assay is for use on Qiagen's NeuMoDx 96 and 288 integrated PCR-based clinical molecular testing systems. It is designed to enhance testing accessibility, cost, and result turnaround time.

-

October 2022 – Bio-Rad Laboratories introduced two new Exact Diagnostics molecular controls: the CT/NG Positive Run Control and the STI Negative Run Control. These quality controls are applied with molecular assays for the detection of Chlamydia trachomatis and Neisseria gonorrhoeae. They aid test accuracy by checking for possible contamination and sample adequacy and are intended to measure intra- and inter-run laboratory performance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.60 Billion |

| Market Size by 2032 | USD 2.67 Billion |

| CAGR | CAGR of 6.62% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Assays & Kits, Instruments/Analyzers) • By Test Type (Laboratory Testing, Point-of-Care (POC) Testing) • By Technology (Isothermal Nucleic Acid Amplification Technology, Polymerase Chain Reaction, Immunodiagnostics, Other Technologies) • By End-use (Hospitals & Clinics, Diagnostic Laboratories, Home Care Setting, Other End-users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Abbott Laboratories, Becton, Dickinson & Company (BD), Danaher Corporation, F. Hoffmann-La Roche Ltd., Hologic, Inc., Thermo Fisher Scientific, Inc., Qiagen N.V., Siemens Healthineers AG, Bio-Rad Laboratories, Inc., Binx Health, and other players. |

Frequently Asked Questions

North America dominated the CT/NG Testing Market in 2024.

The “Assays & kits” segment dominated the CT/NG Testing Market.

Government initiatives and screening programs are benefiting the market, to grow.

The CT/NG Testing Market was USD 1.60 billion in 2024 and is expected to reach USD 2.67 billion by 2032.

The CT/NG Testing Market is expected to grow at a CAGR of 6.62% from 2025 to 2032.

Get in Touch