Metal Fabrication Equipment Market Report Scope & Overview:

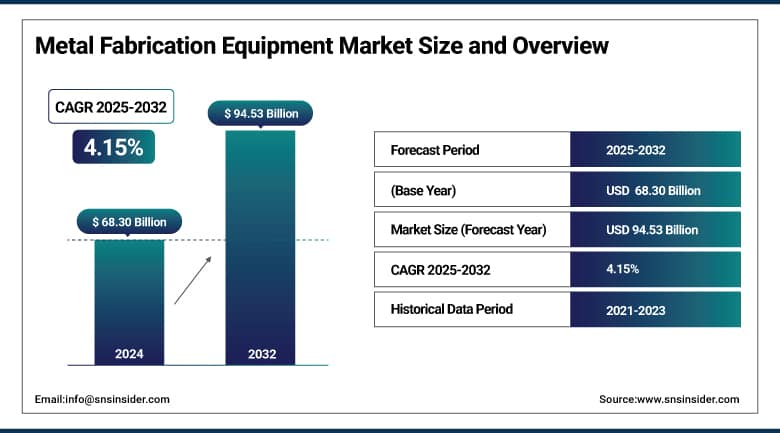

The Metal Fabrication Equipment Market size was valued at USD 68.30 billion in 2024 and is expected to reach USD 94.53 billion by 2032, growing at a CAGR of 4.15% over the forecast period of 2025-2032.

The metal fabrication equipment market is witnessing a gradual expansion, the metal fabrication equipment market is benefiting from an increase in demand within the construction, automotive, aerospace, and heavy machinery industries. The greater availability of metalworking process automation is transforming the industrial sector and is enhancing production efficiency, quality, and reducing labor dependency. Within the same markets, the sheet metal fabrication equipment market is experiencing rapid expansion as its applications extend to consumer electronics and metal part customization.

Innovations such as CNC systems, robotics, and smarter, IoT-enabled machinery are having the greatest impact in their ability to effect smarter, faster, and less costly metalworking. Owing to the introduction of new technologies, the key metal fabrication equipment market trends include an increasing focus on sustainability and digital workflow management. In addition to new technological advancements in the metal fabrication equipment market, growth is driven demand for such products is also supported by the ongoing modernization of the infrastructure in developing countries and increased demand for lightweight, high-strength materials. On the other hand, the metal fabrication equipment market is currently being affected by high initial setup costs and a lack of adequately skilled workers, which might affect their rate of adoption in the short term. Nevertheless, the market is set to achieve widespread expansion in the coming years as manufacturers increasingly focus their efforts on the automated and customized operation of such equipment.

May 2025 – TRUMPF Inc. received a USD 2.5 million grant from Connecticut’s Strategic Supply Chain Initiative to expand its North American Smart Factory in Farmington. The investment supports a new press-brake production line set for 2026, aimed at boosting sheet-metal fabrication. TRUMPF also invested USD 40 million in the now-operational 55,800 sq ft facility equipped with automated laser-cutting and welding systems. The site includes a training center to develop skilled labor, with potential for additional tax incentives if job targets are met.

To Get More Information On Metal Fabrication Equipment Market - Request Free Sample Report

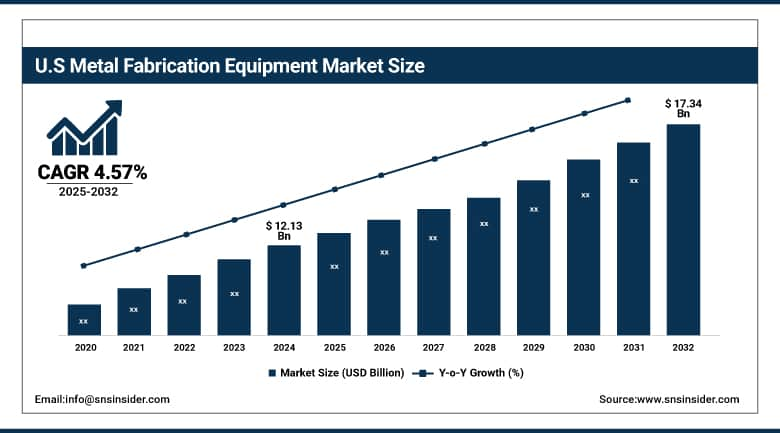

The U.S. Metal Fabrication Equipment Market, valued at USD 12.13 billion in 2024, is projected to grow at 4.57% CAGR, reaching USD 17.34 billion by 2032. The growth is propelled by the increasing industrial automation and advanced manufacturing practices, and the growing demand for the equipment from high-demand industries such as the automobile, aerospace, and construction. In addition, the government directed its efforts at the reshoring of the manufacturing process and investment in infrastructure, further strengthening the demand for domestic equipment.

Metal Fabrication Equipment Market Dynamics:

Drivers

-

Industrialization and Automation Drive Surge in Global Metal Fabrication Equipment Demand

The current trend of rapid industrialization worldwide stimulates the growth of the metal fabrication equipment market significantly because the increasing manufacturing activities require efficient and precise metal components. Automation contributes to this need through boosting productivity, reducing human-made mistakes, and lowering operational costs. The combination of such advanced technologies as Industry 4.0 and the Internet of Things make this trend even faster. Various governments make significant investments into these technologies to modernize the manufacturing infrastructure, which results in smart factories with production processes optimized on the basis of real-time data in combination with interconnected machinery. Another goal of the described technological trend is the improvement of fabrication speed and quality, supported by mass customization and flexible manufacturing. Altogether, the synergy of industrialization and automation represents a serious driving force, making the metal fabrication equipment market evolve because of the growing demand from different industries for sophisticated and reliable metal products.

Restraint

-

Prohibitive Automation Costs (USD 50 K-100 K) Lock SMEs Out of Metal Fabrication's Industry 4.0 Revolution

The metal fabrication industry’s shift toward automation faces a major barrier: high upfront costs. Advanced equipment, such as various sizes of CNC machines, robotic welders, and laser cutters, can cost anywhere from USD 50,000 to USD 100,000. Thus, whereas large manufacturers and corporations can afford to invest in such technology, the same process can be too financially demanding for the vast majority of small and medium-sized enterprises. Conversely, the affordability of such technology could significantly improve the industry performance and drive growth due to the increased efficiency and cutting-edge precision of Industry 4.0 equipment. Some firms have resorted to utilizing leasing models, and some try to mitigate the costs by receiving government subsidies. However, those are still not widely available enough to stop the gap between large and small fabricators from continuously growing, and the process of the market growth from stalling.

Metal Fabrication Equipment Market Segmentation Analysis:

By Material Type

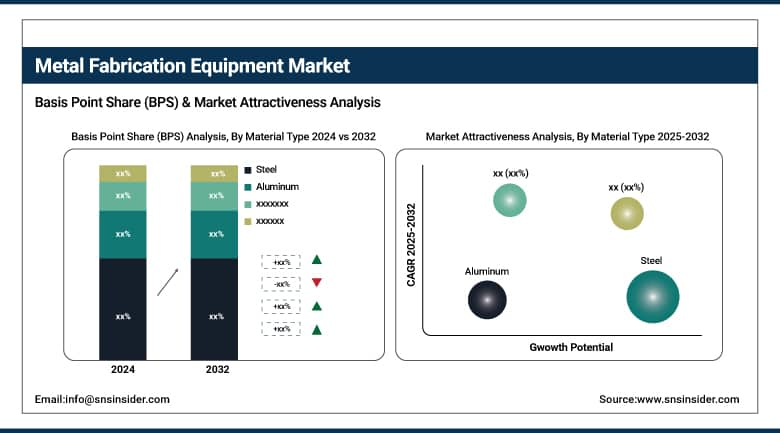

Steel remains the leading material in metal fabrication, holding a dominant 42% market share in 2024, due to its unmatched strength, durability, and cost-efficiency. The utilized category includes coiled and flat sheet, hot-rolled and cold-rolled strip, plate, sections, and organic-coated, among others. Steel is extensively employed in construction for making structural frameworks and heavy equipment for robust components, with chassis and body panels being fabricated for the automotive industry. Steel’s weldability, formability, versatility, and recyclability enhance demand across various processors. Steel is usually the material of choice for high-load applications where resilience is imperative, although its share is subject to strong resistance from alternative products, such as other metals or composites. The material’s price point and availability reliably keep it in the lead in industries like infrastructure, shipbuilding, and industrial equipment manufacturing.

Aluminum is experiencing rapid growth in metal fabrication, driven by its lightweight nature, corrosion resistance, and sustainability benefits. The sector’s growth was driven by the superior weight, corrosion resistance, and sustainability of the material. The auto industry, including electric vehicles, relies on aluminum to ensure the weight of the vehicles remains lowered, meaning that less energy is consumed and the battery range can be extended. The aircraft industry also relies on aluminum alloys to construct aircraft structures to improve fuel efficiency and the payload capacity of their planes. As the most recycled substance on the planet, aluminum is fully recyclable, which helps the aluminum market implement tailored carbon emission reduction targets and benefit many sectors, like the renewable, packaging, and consumer electronics, in critical waste reduction efforts.

By Equipment Type

The cutting equipment segment dominated the market and accounted for 38% of the metal fabrication equipment market share. This is owing to the cutting process’s irreplaceable role in the majority of key industries, such as automotive, construction, or industrial manufacturing. Innovative metal cutting technologies, including laser, plasma, or waterjet systems, offer high speed and accuracy of slicing metal sheets, tubes, or plates, ensuring high productivity with minimized waste. In addition, the industry witnesses an increasing demand for automated cutting solutions, fueled by the integration with Industry 4.0. Rising infrastructure development and trends such as an increased number of automotive manufacturing processes add to the demand for cutting, and the equipment type’s dominance. Finally, the segment’s superiority is well-justified, as emerging, cutting-edge technologies are accompanied by their improved versions for more accurate, efficiency-boosting operation.

The machining equipment segment is the fastest-growing in the metal fabrication market, driven by increasing automation and precision manufacturing demands. The unsustainable demand for higher automation and precision in the manufacturing process is possible due to emerging CNC systems, including multi-axis milling and turning center. They are increasingly used in the production of high-tolerance elements of such industries as aerospace, medical devices, or automotive vehicles. Improved productivity and reduced operational expenses can also be attributed to the inclusion of IoT, AI, or smart manufacturing in the machining process. Therefore, the demand for more intelligent, automated solutions in light of the Industry 4.0 adoption fuels the segment’s swift growth in the metal fabrication equipment market.

By End User

The automotive segment is the largest consumer of metal fabrication equipment, holding a 32% market share in 2024, Considering the quantity of metal used in vehicle production, such a situation should not be surprising. Cabs, body panels, chassis, detail components, exhaust systems, and heavy engine parts rely heavily on fabricated steel and aluminum. The growing electric vehicles market boosts the demand for precision cutting and welding equipment. Lightweight trends and tightening fuel efficiency requirements encourage automakers to experiment with fabrics, alloys, and structural designs. With the increased production of vehicles in the world, mostly in emerging markets, the automotive end-user is and will continue to be the most important in the future demand for metal fabrication equipment.

The aerospace & defense segment is the fastest-growing segment in metal fabrication, fueled by rising demand for lightweight, high-strength materials like titanium, aluminum alloys, and composites. The demand for lightweight high-strength materials, such as aluminum alloys, titanium, and composites in the aviation sector stimulates the sector’s growth. It is also crucial for the development of space technology, such as the growing number of satellites and rocket boosters. With the return to the main roads and the rising of defense expenditures expanding all around the world, the area may stand out in the upcoming years. The sector needs a higher level of precision due to an array of complex metallic products. For instance, such complex shapes as turbines, blades, and casing require a 5-axis machining, whereas the boundaries, ribs, and enclosures are crafted with the help of laser-cutting.

Metal Fabrication Equipment Market Regional Outlook:

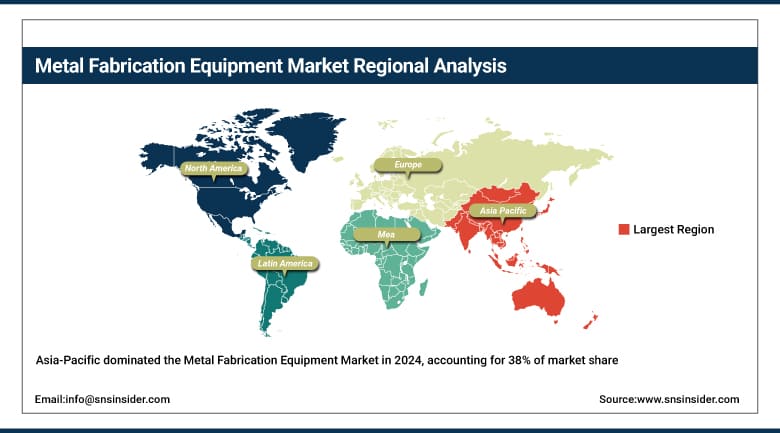

Asia-Pacific dominated the metal fabrication equipment market with a 38% share in 2024, led by China, India, and Japan. Expanding automotive and construction sectors, rapid industrialization, and low labor costs have been drivers. China, as the leading manufacturing country, massively invests in automation, as it is also the key consumer. Policies like Make in India further drive the market. The cost and export-oriented nature of the industries have cemented Asia’s predominant position, and it outpaces both the production and consumption ends of the market.

China dominated the Asia-Pacific metal fabrication equipment market, accounting for the largest share due to its vast manufacturing, strong industrial, and export bases. The country is also the leading global hub for automotive, machinery, and construction. The ‘Made in China 2025’ initiatives have further established the country’s dominance.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America is the fastest-growing region in the metal fabrication equipment market in 2024, due to the ongoing industrialization, technological advancements, a growing demand for metals from the automobile and aerospace industries. This growth is led by the U.S., where existing and new companies heavily invest in automation and smart manufacturing. In addition, the government’s support for domestic manufacturing and adoption of novel machinery accelerates the expansion. The focus of the region on the precision of engineering and sustainability of processes also makes it a fast-growing market and a central region for innovations.

Europe holds a significant share of the metal fabrication equipment market, and the growth of the market is facilitated by a strong industrial base and supported by the high demand for the equipment from the automobile, machinery, and construction industries. In particular, this growth is sustained in Germany, Italy, and France, which are leading adopters of automation and Industry 4.0. Furthermore, Europe has strict environmental regulations, which lower the margins of companies and make energy-efficient and eco-friendly equipment beneficial, supporting the growth of the market. Europe, while presenting steady growth, is a critical region due to its advanced engineering focus and the push to implement high-quality solutions.

Key Players:

-

Amada Corporation

-

Bystronic Laser AG

-

Yamazaki Mazak Corporation

-

DMG Mori

-

Okuma Corporation

-

Hypetherm Associates Inc.

-

Prima Industrie

-

BLM Group

Recent Development

-

In October 2024, AMADA Italia S.r.l., a subsidiary of Amada Corporation, opened a new welding technical center in Piacenza City, Italy, aimed at boosting sales of metal fabrication equipment for automotive and related sectors.

-

In January 2025, Amada's Long-term Vision and Medium-term Business Plan 2025 emphasize developing new products to resolve social issues, reducing environmental impact, improving productivity, requiring fewer skills, and expanding automation products for whole-factory control. They also aim to expand business domains to highly reflective materials (copper, aluminum), non-metallic materials, and micro-processing.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 68.30 Billion |

| Market Size by 2032 | USD 94.53 Billion |

| CAGR | CAGR of 4.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment Type (Cutting Equipment (Laser Cutting Machine, Plasma Cutting Machine, Waterjet Cutting Machine, Flame Cutting Machine, Others [Bandsaws, etc.]), Machining Equipment (CNC Machine, Lathe Machine, Drilling Machine), Welding Equipment (Arc Welding Machine, Resistance Welding Machine, Laser Welding Machine, Robotic Welding Equipment), Bending & Forming Equipment (Press Brakes, Rolling Machine, Stamping Machine, Others [Stretch Forming Equipment, etc.]), Others (Shearing Equipment, etc.) • By Material Type (Steel, Aluminum, Copper, Others (Alloys, etc.) • By End User (Automotive, Aerospace & Defense, Construction, Electronics, Energy, Shipbuilding, Others (Consumer Goods, etc.) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Trumpf Group (Germany), Amada Corporation (Japan), Bystronic Laser AG (Switzerland), Yamazaki Mazak Corporation (Japan), Sandvik AB (Sweden), DMG Mori (China), Okuma Corporation (Japan), Hypetherm Associates Inc (U.S.), Prima Industrie (Italy), BLM Group (Italy) |

Get in Touch