Microsurgery Market Overview & Scope

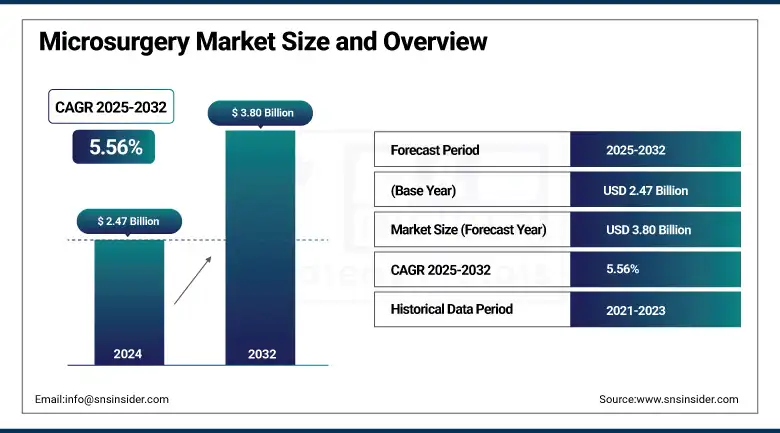

The Microsurgery Market size was valued at USD 2.47 billion in 2024 and is expected to reach USD 3.80 billion by 2032, growing at a CAGR of 5.56% over the forecast period of 2025-2032.

The microsurgery market is transforming globally, and this transformation is supported by advancements in technology, growing demand for minimally invasive procedures, and a steep rise in complex surgical cases, especially in the reconstructive, neurological, and oncological fields. With more than 1/3 of the global population affected by neurological disorders (WHO, 2024) and over 1.9 million new cancer cases annually reported in the U.S. (CDC, 2024), the demand for precision surgical interventions has increased. Robot-assisted microsurgery and artificially intelligent systems enable precise operations for delicate tasks like fixing lymphatic problems, repairing peripheral nerves, or reconstructing after cancer. The U.S. microsurgery market is particularly vibrant, where even institutions like Cedars-Sinai and the Yale New Haven Hospital have adopted commercially approved robotic systems (Symani and others). R&D spending continues to be a driver of supply-side growth with strategic funding, like MMI’s USD 110M raise to scale microsurgical robotic systems.

To Get more information On Microsurgery Market - Request Free Sample Report

For instance, Investor confidence and innovation remain strong in the global microsurgery market growth, as in early 2025, Horizon Surgical obtained USD 30 million in funding to bring its AI-powered microsurgery robotics platform to market.

Regulatory approvals, such as the FDA’s de novo clearance for Symani and AI-helmed scientific review pilots, are also driving the market for microsurgery. Increasing mastectomy rates, increasing levels of demand, the number of lymphedema patients (~10 million Americans), and the number of surgeries in high-risk specialties (Johns Hopkins Medicine). In addition, the 2024 HRSA Health Workforce Report indicates that the growth of the surgical specialization workforce provides long-term market scalability. The aforesaid trends, coupled with a robust R&D landscape, are favoring the microsurgery market in top microsurgery companies.

For instance, Kuwait introduced the region's first national skin bank and microsurgery lab in March 2025, reiterating global interest in increasing surgical infrastructure and recovery for trauma and burn patients.

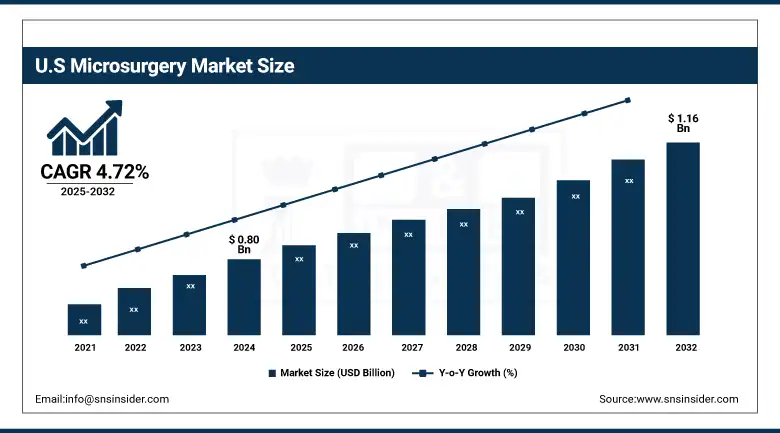

The U.S. microsurgery market size was valued at USD 0.80 billion in 2024 and is expected to reach USD 1.16 billion by 2032, growing at a CAGR of 4.72% over the forecast period of 2025-2032.

Microsurgery Market Dynamics

Drivers:

-

Rising Demand for Precision Procedures and Technological Innovation Fuels Market Growth

The incessant demand for ultra-precision in surgical procedures due to the burgeoned disease burden, coupled with lucrative technological investments, is expected to favor growth in the microsurgery market. Microsurgery is now becoming a critical tool in the treatment of vascular disorders, congenital malformations, and reconstructive procedures, particularly in solid organ transplantation and trauma rehabilitation. For instance, the increasing incidence of diabetic foot ulcers with a need for revascularization, affecting around 15% of diabetic patients globally (PubMed, 2024), has led to the increased clinical use microsurgical approach. From the supply side, companies like MedithinQ are making significant investments in 3D visualization technology, such as their recent Scopeye technology, to increase intraoperative precision.

R&D expenditure has also skyrocketed, and Horizon Surgical has already rolled out a microsurgical AI robotic prototype, proving this innovation is still underway. Also, AI solutions are helping surgeons achieve better aesthetic results and reduce operative time for faster recoveries. Regulatory frameworks are emerging to accommodate these innovations, e.g., the FDA’s 2024 pilot program for AI-augmented reviews is accelerating device approvals. All these variables and training programs, like those in microsurgery, were influencing the precision and availability of the technique. With more microsurgery players than ever increasingly vying for a piece of this pie, it is only natural that improved device efficacy, surgeon comfort, and patient results will continue to foster the development of the global microsurgery market in various therapeutic areas.

Restraints:

-

High Cost, Skill Barriers, and Infrastructure Gaps Hinder Market Expansion

Although the microsurgery market is progressing fast, there are significant barriers to its growth, such as the high cost of the procedures, longer learning time for health professionals, and lack of infrastructure in emerging economies. Microsurgery typically uses expensive robotic systems, precise tools, and high-resolution imaging devices, which increases the costs of design, installation, and repair substantially. For instance, robot-assisted systems for microsurgery, such as Symani or Da Vinci, may carry a price tag of over USD 2 million per system, which hinders their penetration into smaller hospitals and low-resource environments. Moreover, microsurgery practice is highly skill-demanding and limited to a few highly specialized providers.

The Bureau of Health Workforce (2024) emphasizes the lack of a specialty surgical workforce, particularly in rural and underserved areas, leading to supply-side barriers. In addition, the lack of microsurgical facilities (high magnification operating microscopes, microsurgical instruments, etc.) in many areas of the world limits widespread application. Regulatory approval processes, despite being improved, require long gestation periods and complicate the compliance requirements of new AI-robotic integrations, which delays commercialization. These combined factors still serve to inhibit the growth of microsurgery market shares, notably in a cost-sensitive or resource-limited market. Addressing these challenges will require subsidized healthcare policies, focused training programs, and modular technology solutions to scale and democratize microsurgery globally.

Microsurgery Market Segmentation Analysis

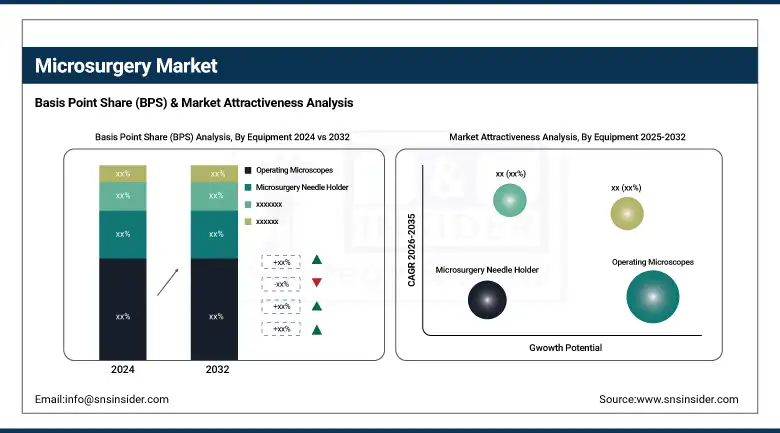

By Equipment

In 2024, operating microscopes were the key segment in the global microsurgery market, having accounted for over 38.8% share of the overall revenue. This supremacy is largely a result of the critical requirement for high-magnification visualization in improving surgical accuracy in complicated procedures, including neurovascular anastomosis, free flap reconstruction, and ophthalmic operations. With the development of advanced digital and robot-compatible microscopes, respectively, a real-time, high-resolution, and 3-dimensional view could be obtained for complex anatomy. As a result, surgeons favor these systems more and more for their better postoperative results and lower intraoperative mismaneuvers.

The micro sutures segment is expected to be the fastest-growing segment of the microsurgery market, due to rising demand for fine, accurate tissue approximation in various surgery applications. These ultrafine sutures are a must for microvascular anastomosis, nerve coaptation & ocular repairs which require low tissue reaction and high tensile strength. New suture materials, for instance, bioresorbable suture and antimicrobial-coated suture, have increased the potential applications of these materials.

By Procedure

Free tissue transfer was the largest procedure in the microsurgery market with a revenue share of 36.3% in 2024. This is accomplished by transferring skin, fat, muscle, or bone with its blood supply from one area of the body to another, thereby serving as the foundation in a majority of reconstructive procedures for patients who have faced trauma, had cancer removed, or were born with congenital defects. Its popularity in plastic, orthopedic, and maxillofacial surgery speaks in favor of this approach. With the improvement of the quality and the diversity of the surgical equipment and the advancement of microvascular anastomosis, free grafts have become increasingly reliable and successful.

The transplantation segment is expected to register the highest CAGR in the microsurgery market, due to the increasing incidence of organ failure, increasing success rates of transplants, and utilization of microsurgery in composite tissue allotransplantation (such as face and hand transplantation). Microscopic surgery is critical to the success of these intricate operations, which involve connecting tiny blood vessels and nerves. As liver, kidney, and vascularized composite (VCA) organ transplantation is becoming more prevalent around the world, microsurgical skills and instrumentation are increasingly necessary.

By Application

Plastic & reconstructive surgery held the largest market share in the global microsurgery market in 2024, applicable for a segment high of more than 28.2% of total market share in revenue. This trend is being dictated by the increased incidence of trauma, burns, tumour defects, and congenital defects, which demand both functional and aesthetic rehabilitation. It is the key operative technique in such applications of breast reconstruction following mastectomy, cleft palate repair, and facial reanimation. Growing interest in sophisticated cosmetic techniques and insurance coverage for reconstructive procedures in several countries promoted interest in microsurgical techniques.

The ophthalmic application is expected to be the fastest-growing segment in the microsurgery market, driven by the growing prevalence of vision-related disorders, including cataracts, glaucoma, and retinal diseases, worldwide. Growing numbers of elderly people, and the high usage of screens and lifestyle-related vision issues, are contributing to a growing demand for accurate eye surgeries. Microsurgical procedures are necessary in operations such as phacoemulsification, retinal detachment repair, and corneal transplant. The demand for minimally invasive procedures has driven the advent of micro-incision tools and robotics systems specifically designed for ophthalmology.

By End-use

The hospitals and clinics had the highest end-use share in the microsurgery market in 2024, contributing 39.4% to the total revenue. They have dominated in doing so due to access to cutting-edge equipment, top microsurgical talent, and the robotic surgical system that has enabled them to do high-risk, complicated moves. Tertiary care hospitals are the main settings for neurosurgical tumor resection, reconstructive transplant surgery, and microvascular anastomosis. The existence of multidisciplinary teams, protection by an anesthetist, and high care postoperatively additionally strengthens the position of the hospital when it comes to performing microsurgery.

The Ambulatory Surgical Centers (ASCs) segment is expected to be the fastest-growing end-users of the microsurgery market, due to the rising demand for cost-effective and outpatient surgical procedures. The move toward same-day surgeries, including ophthalmology, cosmetic, and reconstructive procedures, is driving the importance of ASCs. These places have shorter patient waits, lower chances of infection, and are less costly than conventional hospitals. Compact microsurgical systems and easy-to-use digital operating platforms enable complex operations to be performed outside hospital facilities.

Microsurgery Market Regional Insights

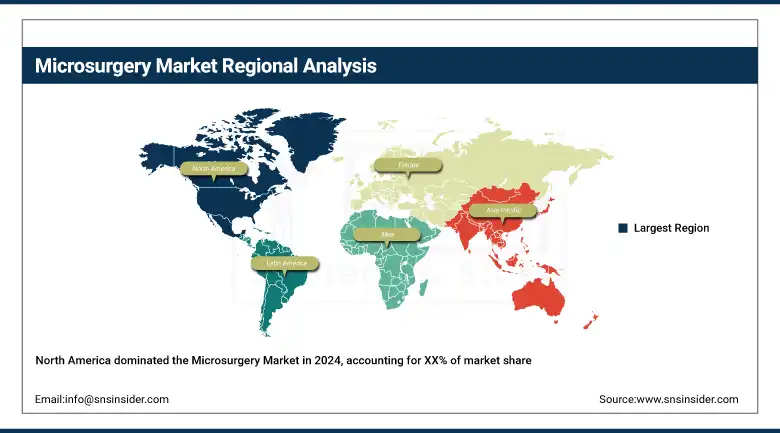

North America was the leading regional segment of the global microsurgery market in 2024, due to a highly developed healthcare system, early adoption of robotic and AI-enabled microsurgery, and a high number of surgical procedures. The U.S. generated the highest revenue as it is home to a large number of leading microsurgery companies, a well-established reimbursement structure, and considerable clinical R&D investments. The CDC estimates more than 600000 microsurgical procedures are performed each year in the U.S., particularly in plastic-reconstructive, neurosurgery, and ophthalmology. This dominance is also being underpinned by government spending on medical innovation and fast-rising rates of chronic diseases. Canada is also playing a large part, as public funds are used to support microsurgical training and minimally invasive methods. In Mexico, which is still developing in microsurgery, the demand for cosmetic and reconstructive microsurgery is increasing with medical tourism.

Get Customized Report as per Your Business Requirement - Enquiry Now

Region-wise, Europe is the second largest market of microsurgery, which is attributed to the presence of a universal healthcare system and well-developed surgical protocols, and higher adoption rates of precision technologies. The German market is held by all the leading players, with a strong preference for surgical device manufacturers, Leica Microsystems, and Carl Zeiss AG, and microsurgical research. Germany also carried out more than 100,000 microsurgical operations last year, notably in oncology, reconstructive, and neurological procedures. High investment in outpatient microsurgery services and robotic platforms is also witnessing high investments from France and the UK. The UK’s NHS has introduced minimally invasive surgical systems in public hospitals, prompting demand.

Asia Pacific is expected to be the fastest-growing region in the microsurgery market due to increasing healthcare spending, the rise in surgery volumes, and the rapid adoption of advanced technologies. China leads the region, driven by an explosion in reconstructive and ophthalmic surgeries, in addition to government-supported infrastructure growth. More than 800,000 reconstructive microsurgeries were conducted in 2024, when the demand soared, the National Health Commission of China says. Increased medical tourism, a burgeoning load of cancer-related surgeries, and widening of microsurgical training in the tertiary centers have India fast-tracking and gaining it. Japan and South Korea, on the other hand, have also embraced robotic microsurgery platforms, especially in neurology and plastic surgery, to keep up with an aging population and high-tech expenditures.

Key Players in the Microsurgery Market

Leading microsurgery companies operating in the global market include Haag-Streit Group, Olympus Corporation, Leica Microsystems, B. Braun Melsungen AG, Accurate Surgical & Scientific Instruments Corp., Surtex Instruments Ltd., Scanlan International, Carl Zeiss AG, KLS Martin Group, Topcon Corporation, and Integra LifeSciences.

Recent Developments in the Microsurgery Market

-

In April 2025, Yale New Haven Hospital became the first center in New England to implement a robotic microsurgery system, advancing its capabilities in nerve repair and lymphatic surgeries with improved precision and reduced recovery times.

-

In March 2025, Horizon Surgical announced a USD 30 million investment to accelerate the development of its AI-powered microsurgery robotics platform, aimed at enhancing precision in complex reconstructive procedures and improving surgical workflow efficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.47 billion |

| Market Size by 2032 | USD 3.80 billion |

| CAGR | CAGR of 5.56% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Equipment (Operating Microscopes, Micro Sutures, Micro Forceps, Microsurgery Needle Holder, Others) • By Procedure (Transplantation, Suture & Grafting, Free Tissue Transfer, Others) • By Application (Orthopedic, Neurology, Gynecological & Urological Microsurgery, Ophthalmic, Plastic & Reconstructive, Oncology, Others) • By End-Use (Hospitals & Clinics, Ambulatory Surgical Centers, Academics and Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Haag-Streit Group, Olympus Corporation, Leica Microsystems, B. Braun Melsungen AG, Accurate Surgical & Scientific Instruments Corp., Surtex Instruments Ltd., Scanlan International, Carl Zeiss AG, KLS Martin Group, Topcon Corporation, and Integra LifeSciences. |

Frequently Asked Questions

Ans: North America dominated the Microsurgery market.

Ans: There are significant barriers to its growth, such as the high cost of the procedures, longer learning time for health professionals, and lack of infrastructure in emerging economies.

Ans: Incessant demand for ultra-precision in surgical procedures due to the burgeoned disease burden, coupled with lucrative technological investments, is expected to favor growth in the microsurgery market.

Ans: The market is expected to reach USD 3.80 billion by 2032, increasing from USD 2.47 billion in 2024.

Ans: The Microsurgery market is anticipated to grow at a CAGR of 5.56% from 2025 to 2032.

Get in Touch