Gastrointestinal Endoscopic Devices Market Report Scope & Overview:

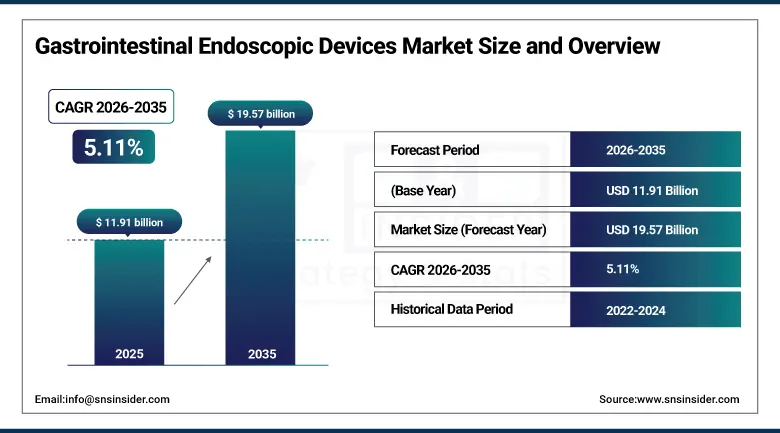

The Gastrointestinal Endoscopic Devices Market was valued at USD 11.91 Billion in 2025 and is expected to reach USD 19.57 Billion by 2035, growing at a CAGR of 5.11% from 2026–2035.

The global gastrointestinal endoscopic devices market is growing at a sustained and commercially broad-based pace. Gastrointestinal endoscopic devices encompass the full spectrum of instruments used to visually examine, diagnose, and treat the GI tract including flexible endoscopes, capsule endoscopes, biopsy forceps, polypectomy snares, haemostasis devices, ERCP accessories, and stenting systems. The market is driven by the rising incidence and prevalence of gastrointestinal diseases including colorectal cancer, gastroesophageal reflux disease, inflammatory bowel disease, and peptic ulcer disease that collectively create structured demand for diagnostic and therapeutic endoscopic intervention.

In 2024, Olympus Corporation launched the EVIS X1 endoscopy system for the U.S. market, featuring TXI (Texture and Colour Enhancement Imaging) technology that improves detection of flat and depressed polyps that white light endoscopy misses, integrating AI-assisted lesion detection that alerts endoscopists to suspicious areas requiring closer examination. The system’s AI detection capability addresses one of the most commercially significant quality improvement opportunities in colonoscopy, whose polyp miss rate reduction creates patient safety benefit and medicolegal risk reduction motivation for hospital procurement.

Market Size and Forecast

-

Market Size in 2026E: USD 12.52 Billion

-

Market Size by 2035: USD 19.57 Billion

-

CAGR: 5.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Gastrointestinal Endoscopic Devices Market - Request Free Sample Report

Gastrointestinal Endoscopic Devices Market Trends

-

AI-powered polyp detection and characterization technologies are driving demand for advanced gastrointestinal endoscopy systems that improve colorectal cancer screening accuracy

-

Adoption of disposable flexible endoscopes is increasing as healthcare providers prioritize infection prevention and reduce risks associated with device reprocessing

-

Capsule endoscopy is gaining popularity due to its minimally invasive nature and improved patient acceptance for gastrointestinal diagnostics

-

Growing use of endoscopic mucosal resection (EMR) and endoscopic submucosal dissection (ESD) is expanding therapeutic endoscopy applications for early gastrointestinal cancers and complex polyps

-

Robotic-assisted endoscopy systems are emerging as next-generation solutions that enhance navigation, precision, and procedural efficiency in gastrointestinal examinations and treatments

U.S. Gastrointestinal Endoscopic Devices Market Outlook

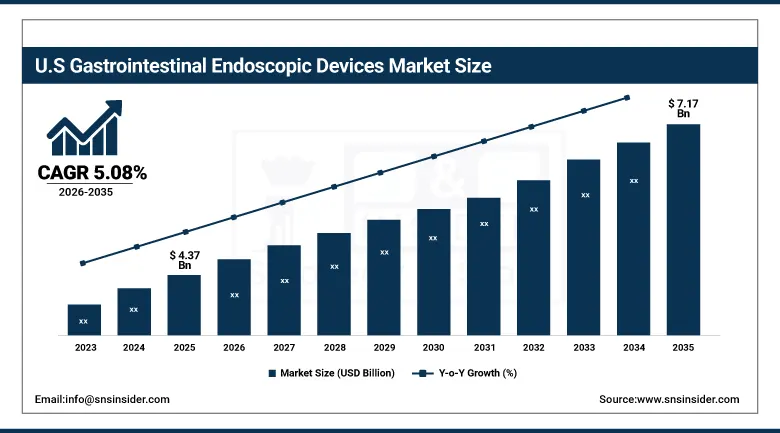

The U.S. Gastrointestinal Endoscopic Devices Market was valued at approximately USD 4.37 Billion in 2025 and is expected to reach approximately USD 7.17 Billion by 2035, growing at a CAGR of approximately 5.08%.

The U.S. is the world’s most commercially sophisticated GI endoscopic devices market within North America’s dominant revenue position. Olympus, Fujifilm Medical Systems, Pentax Medical, Boston Scientific, and Cook Medical’s U.S. operations collectively define the commercial GI endoscopy landscape. ACS and ASGE’s colorectal cancer screening guidelines, CMS’s Medicare coverage for colonoscopy, and the U.S. Preventive Services Task Force’s colorectal cancer screening recommendations collectively create structured institutional endoscopy volume that sustains above-average GI endoscopic device procurement. The ASC sector’s growing share of outpatient GI endoscopy creates new procurement channels that compound with hospital-based endoscopy volume.

Boston Scientific launched its AXIOS Stent and Electrocautery Enhanced Delivery System expansion in 2024 with new lumen-apposing stent size options for endoscopic ultrasound-guided drainage of pancreatic and peripancreatic fluid collections, enabling endoscopists to manage a broader range of fluid collection dimensions without open surgical drainage. The expansion reflects the commercial direction of interventional GI endoscopy toward replacing surgical procedures with endoscopic alternatives whose reduced patient morbidity and healthcare system cost create adoption motivation from both clinical and economic perspectives.

Gastrointestinal Endoscopic Devices Market Segment Analysis

-

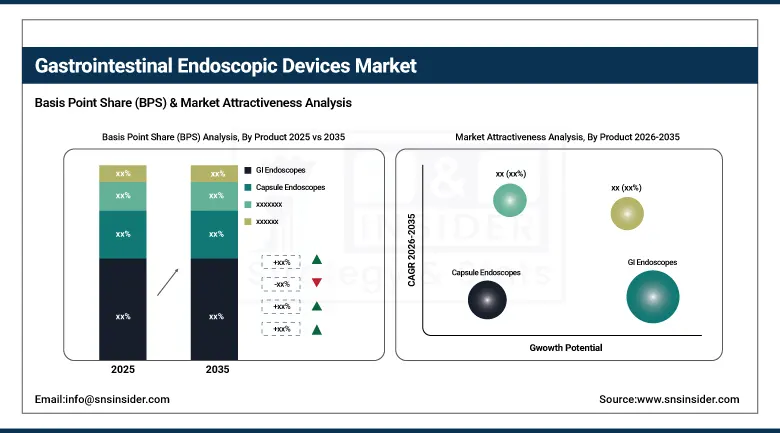

By Product, the GI Endoscopes segment dominated the Gastrointestinal Endoscopic Devices Market with approximately 48% share in 2025, while the Capsule Endoscopy segment is the fastest growing.

-

By Application, the Diagnostic GI Endoscopy segment dominated the Gastrointestinal Endoscopic Devices Market with approximately 62% share in 2025, while the Therapeutic/Interventional GI Endoscopy segment is the fastest growing.

-

By End User, the Hospitals & Clinics segment dominated the Gastrointestinal Endoscopic Devices Market with approximately 58% share in, while the Ambulatory Surgical Centres segment is the fastest growing.

By Product, GI endoscopes dominate, capsule endoscopy grows fastest

GI endoscopes retained the dominant product position with approximately 48% of the gastrointestinal endoscopic devices market in 2025. Endoscope capital procurement’s role as the primary investment in every GI endoscopy programme creates commercial relationships whose replacement cycle, processor upgrade, and scope fleet expansion create consistent procurement across the global endoscopy centre infrastructure. Olympus, Fujifilm, and Pentax Medical’s endoscope systems create long-duration institutional relationships whose reagent-like consumable demand for biopsy forceps, snares, and single-use accessories sustains commercial revenue beyond the capital procurement event. AI detection-enabled endoscope system upgrades, including Olympus’s EVIS X1 and Fujifilm’s ELUXEO series, create above-standard replacement procurement motivation that sustains GI endoscope segment revenue growth.

Capsule endoscopy is the fastest-growing product because the swallowable pill camera’s patient acceptability advantage creates diagnostic access in populations whose conventional endoscopy acceptance is limited. Each clinical programme that establishes capsule endoscopy for small bowel Crohn’s disease evaluation, obscure GI bleeding investigation, and surveillance creates PillCam procurement whose consumable per-procedure commercial value creates recurring revenue. Colon capsule endoscopy’s growing clinical evidence base for colorectal cancer screening in patients who decline conventional colonoscopy creates a new procurement category whose commercial momentum compound with regulatory approval expansion globally.

By Application, diagnostic dominates, therapeutic grows fastest

Diagnostic GI endoscopy retained the dominant application position with approximately 62% of the gastrointestinal endoscopic devices market in 2025. Colorectal cancer screening colonoscopy’s population-scale volume, upper GI diagnostic gastroscopy’s widespread indication for dyspepsia and reflux evaluation, and IBD surveillance endoscopy’s longitudinal monitoring requirement collectively create the most commercially consistent and highest-volume GI endoscopy application category. Each national colorectal cancer screening programme that specifies colonoscopy as the primary screening modality creates institutional-scale diagnostic endoscope procurement whose per-procedure accessory consumption compounds with programme throughput.

Therapeutic and interventional endoscopy is the fastest-growing application because the extraordinary expansion of endoscopic treatment options from conventional polypectomy through ESD, ERCP, EUS-guided intervention, and per-oral endoscopic myotomy is progressively replacing surgical alternatives with less invasive endoscopic approaches that create premium device procurement. Each new endoscopic technique that achieves clinical guideline endorsement creates structured therapeutic device procurement from GI training programmes whose adoption compounds with the endoscopic skill set’s progressive dissemination across international endoscopy practice.

By End User, hospitals dominate, ASCs grow fastest

Hospitals and clinics retained the dominant end-user position with approximately 58% of the GI endoscopic devices market in 2025. Hospital endoscopy units’ comprehensive capability encompassing emergency GI haemorrhage management, complex therapeutic ERCP and EUS procedures, cancer staging, and intensive care setting GI assessment creates procurement breadth whose combined value sustains hospital’s aggregate market leadership. Each hospital’s multi-room endoscopy suite creates multi-endoscope system installation whose video processor, stack equipment, and scope fleet represent capital procurement relationships whose replacement and expansion sustains consistent commercial engagement.

Ambulatory surgical centres are the fastest-growing end user because the outpatient colonoscopy and upper GI endoscopy migration from hospital setting toward ASC creates above-average procurement growth from operators who are expanding GI endoscopy capacity. ASC’s lower per-procedure operating cost relative to hospital outpatient department creates payer incentive for procedure volume migration whose commercial consequence creates ASC endoscopy programme investment. Each new ASC that establishes GI endoscopy capability creates capital endoscope procurement whose consumable demand sustains multi-year commercial relationships.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Gastrointestinal Endoscopic Devices Market Insights

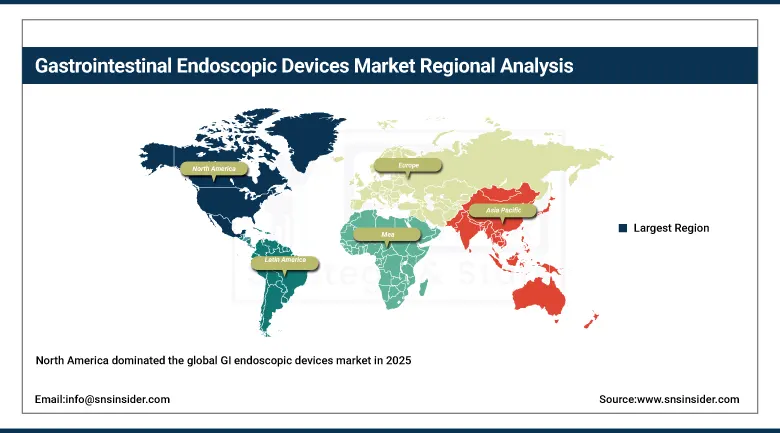

North America dominated the global GI endoscopic devices market in 2025. The United States accounts for approximately 87.4% of North American revenues through Olympus, Fujifilm, Boston Scientific, and Cook Medical’s commercial operations, the most comprehensive colorectal cancer screening infrastructure of any national system, and above-average per-procedure device accessory consumption that reflects the U.S. endoscopy practice’s premium quality standard.

Canada contributes approximately 12.6% of North American revenues through its provincial colorectal cancer screening programmes, hospital endoscopy unit investment, and the growing ASC sector’s outpatient colonoscopy expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Gastrointestinal Endoscopic Devices Market Insights

Europe is a technically sophisticated GI endoscopic devices market where national bowel cancer screening programmes, ESGE’s clinical guidelines, and Olympus and Fujifilm’s European commercial operations create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced GI endoscopy training infrastructure, mandatory colonoscopy screening programme, and the hospital sector’s premium endoscope specification.

The United Kingdom, France, and Italy are significant secondary markets where NHS and equivalent national healthcare system bowel screening programme investment, the academic gastroenterology community’s technology adoption, and the private endoscopy sector’s premium device specification create consistent procurement.

Asia Pacific Gastrointestinal Endoscopic Devices Market Insights

Asia Pacific is the fastest-growing regional GI endoscopic devices market, driven by China’s colorectal and gastric cancer screening programme expansion, Japan’s high per-capita GI endoscopy rate, South Korea’s national cancer screening infrastructure, and India’s rapidly expanding private hospital endoscopy capacity. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary hospital network expansion, government’s GI cancer screening investment, and the domestic endoscopy equipment manufacturer development.

Japan’s world-leading per-capita endoscopy rate, whose gastric cancer screening culture creates above-average endoscope procurement per population, and South Korea’s national cancer screening programme create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Gastrointestinal Endoscopic Devices Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital endoscopy network, Vision 2030’s healthcare investment, and the Ministry of Health’s GI cancer screening programme development. Brazil leads Latin American revenues at approximately 44.2% through its hospital endoscopy infrastructure, the private gastroenterology sector’s technology adoption, and the growing colorectal cancer awareness creating screening programme investment.

UAE’s advanced private hospital endoscopy and South Africa’s academic medical centre create significant MEA secondary markets whose GI endoscopic device procurement reflects growing GI disease burden awareness.

Market Dynamics

Growth Drivers: Rising GI disease incidence and AI-powered endoscopy creating diagnostic quality upgrade procurement

Rising incidence of gastrointestinal diseases is the GI endoscopic devices market’s most commercially certain structural growth driver. Colorectal cancer’s position as the second most common cancer death cause globally, gastric cancer’s high incidence in Asia Pacific, and the growing global burden of IBD, GERD, and Barrett’s oesophagus collectively create expanding endoscopic diagnostic and therapeutic procedure volume whose device procurement grows proportionally. Each national colorectal cancer screening programme that specifies colonoscopy as the primary screening modality creates institutional endoscope procurement whose per-procedure accessory consumption sustains long-term commercial relationships.

AI-powered endoscopy system adoption is creating diagnostic quality upgrade procurement that motivates endoscope system replacement beyond normal lifecycle timing. Olympus’s EVIS X1’s AI lesion detection, Fujifilm’s ELUXEO series’ CADe AI integration, and Medtronic’s GI Genius’s FDA-cleared computer-aided detection collectively demonstrate the commercial AI endoscopy ecosystem whose adoption in quality-focused GI practices creates structured upgrade procurement.

Restraints: High cost of advanced systems and limited reimbursement in emerging markets

Advanced endoscopic system cost, including high-definition endoscope processors at USD 30,000-80,000 and therapeutic scope systems at higher price points, creates capital procurement barriers for smaller hospitals and endoscopy centres whose budgets cannot accommodate premium technology specification. Each healthcare system that restricts advanced endoscope system procurement to major centres creates market access limitation in secondary and tertiary care settings.

Reimbursement limitations for certain advanced endoscopic procedures in emerging and developing market healthcare systems create adoption barriers that prevent clinical guideline-endorsed techniques from achieving commercial adoption rates proportional to clinical need. Each healthcare system that does not reimburse ESD, capsule endoscopy, or EUS-guided intervention creates a clinical adoption gap whose commercial impact limits device procurement below the epidemiologically indicated volume.

Opportunities: Disposable endoscope market and AI colonoscopy detection systems

Disposable flexible endoscope market expansion represents the most commercially transformative near-term product development direction whose infection control motivation creates structured procurement from hospital infection control programmes. Each regulatory action against reprocessed endoscope-associated infection creates clinical motivation for single-use endoscope adoption whose commercial momentum compounds with FDA’s and CE’s progressive regulatory engagement with single-use endoscope submissions.

AI colonoscopy detection system adoption represents a growing commercial opportunity whose regulatory clearance pathway is established and whose clinical evidence base is progressively demonstrating adenoma detection rate improvement. Each healthcare system that adopts AI detection as standard colonoscopy quality infrastructure creates procurement that sustains above-average revenue growth in the GI endoscopy AI accessory market.

Recent Developments:

-

2024: Olympus Corporation launched the EVIS X1 endoscopy system in the U.S. market in 2024, featuring TXI technology for improved flat and depressed polyp detection and integrated AI-assisted lesion detection that alerts endoscopists to suspicious areas during colonoscopy.

-

2024: Boston Scientific expanded its AXIOS Stent and Electrocautery Enhanced Delivery System in 2024 with new lumen-apposing stent size options for endoscopic ultrasound-guided drainage of pancreatic and peripancreatic fluid collections.

-

2024: Medtronic expanded commercial availability of its GI Genius intelligent endoscopy module in 2024 across European and international markets, providing FDA-cleared AI-powered polyp detection assistance as an add-on to existing colonoscopy systems without requiring endoscope system replacement.

Gastrointestinal Endoscopic Devices Market Key Players

-

Olympus Corporation

-

Fujifilm Holdings Corporation

-

Pentax Medical (HOYA Corporation)

-

Boston Scientific Corporation

-

Cook Medical LLC

-

Medtronic plc

-

Given Imaging Ltd. (Medtronic)

-

Stryker Corporation

-

Karl Storz GmbH & Co. KG

-

Conmed Corporation

-

Endo-Therapeutics Inc.

-

US Endoscopy Group

-

Bracco Imaging SpA

-

Hobbs Medical Inc.

-

Interscope Inc.

-

Capsugel (Lonza Group)

-

IntroMedic Co., Ltd.

-

Nuo Therapeutics Inc.

-

Ovesco Endoscopy AG

-

Micro-Tech Endoscopy

Gastrointestinal Endoscopic Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.91 Billion |

| Market Size by 2035 | USD 19.57 Billion |

| CAGR | CAGR of 5.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (GI Endoscopes/Gastroscopes/Colonoscopes/Enteroscopes, Capsule Endoscopes, Biopsy Devices, Hemostasis Devices, ERCP Devices, Stenting & Dilation Devices, Others) • by Application (Diagnostic GI Endoscopy, Therapeutic/Interventional GI Endoscopy) • by End User (Hospitals & Clinics, Ambulatory Surgical Centres/ASCs, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Olympus Corporation, Fujifilm Holdings Corporation, Pentax Medical (HOYA Corporation), Boston Scientific Corporation, Cook Medical LLC, Medtronic plc, Given Imaging Ltd, Stryker Corporation, Karl Storz GmbH & Co. KG, Conmed Corporation, Endo-Therapeutics Inc., US Endoscopy Group, Bracco Imaging SpA, Hobbs Medical Inc., Interscope Inc., Capsugel (Lonza Group), IntroMedic Co., Ltd., Nuo Therapeutics Inc., Ovesco Endoscopy AG, Micro-Tech Endoscopy |

Frequently Asked Questions

The Gastrointestinal Endoscopic Devices Market is expected to grow at a CAGR of 5.11% from 2026 to 2035.

The Gastrointestinal Endoscopic Devices Market was valued at USD 11.91 Billion in 2025.

Rising incidence of gastrointestinal diseases including colorectal cancer, GERD and AI-powered endoscopy system adoption creating diagnostic quality upgrade procurement beyond normal lifecycle replacement timing.

GI Endoscopes dominated the Gastrointestinal Endoscopic Devices Market with approximately 48% share in 2025, while Capsule Endoscopy is the fastest growing segment.

North America dominated the Gastrointestinal Endoscopic Devices Market in 2025, with the United States accounting for approximately 87.4% of North American revenues. Asia Pacific is the fastest-growing region.

Get in Touch