Modular Chillers Market Report Scope & Overview:

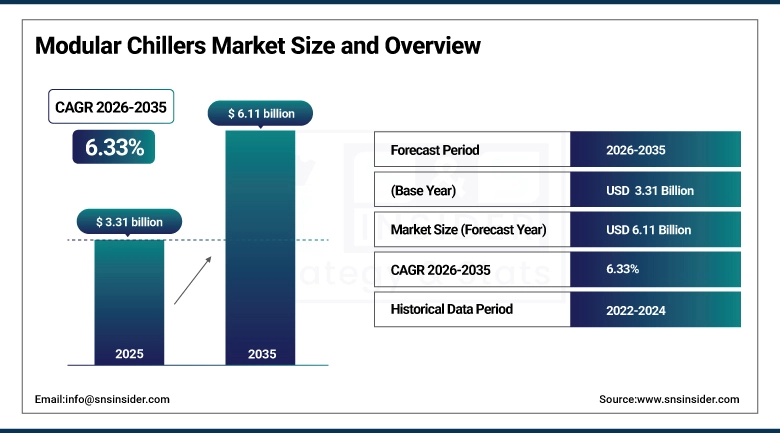

The Modular Chillers Market was valued at USD 3.31 billion in 2025 and is expected to reach USD 6.11 billion by 2035, growing at a CAGR of 6.33% over the forecast period of 2026-2035.

Modular chillers are scalable cooling solutions that consist of multiple smaller chiller units working in tandem to provide the output equivalent to a single large chiller, but with accompanying highly beneficial attributes such as redundancy, simpler maintenance, and flexible capacity management. In the event that one module requires maintenance, all of the other modules stay powered as well, which is essential in data centers, hospitals, and pharmaceutical facilities where downtime is not an option. On account of their mutability, they can likewise be moved more effectively, set up in superior ways and incorporated into different systems. The modular chillers with inverter-driven compressors exhibit considerably improved part-load efficiency over traditional fixed-speed chillers, fueling adoption.

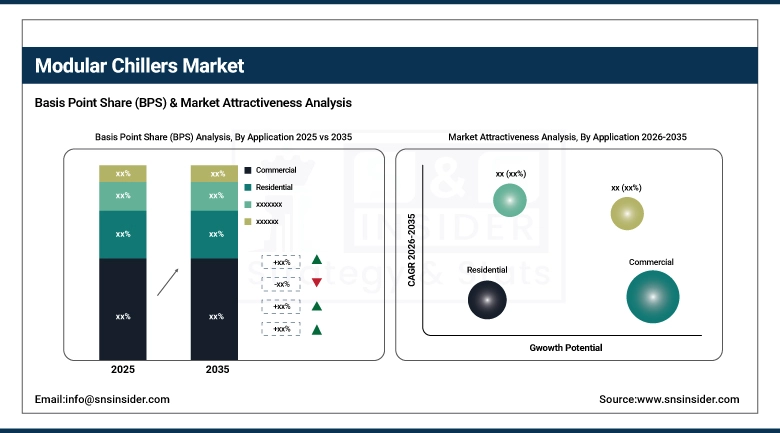

In terms of application, the modular chillers market is segmented into commercial and industrial applications, with commercial holding most significant share (47.80%) in 2023–due to the need for cooling in data centers, healthcare facilities and large office complexes, among others. Data centers matter especially because their cooling needs are steady, mission-critical and rising sharply alongside the expansion of cloud computing and AI workloads.

LG Electronics' IoT-monitoring-enabled advanced residential modular chiller and Mitsubishi Electric's quiet, energy-efficient residential modules released in 2024 signal that major manufacturers are investing seriously in the residential application segment, which is expected to grow at the highest CAGR of 7.44% through 2035.

Market Size and Forecast:

-

Market Size in 2025: USD 3.31 Billion

-

Market Size by 2035: USD 6.11 Billion

-

CAGR: 6.33% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Modular Chillers Market - Request Free Sample Report

Modular Chillers Market Trends:

-

IoT-enabled smart monitoring of modular chiller performance allowing predictive maintenance and remote operation optimization.

-

Transition to low-global-warming-potential refrigerants (R-32, R-290, R-454B) driven by phase-down regulations for HFC refrigerants.

-

Growing data center market creates significant demand for redundant, scalable modular chiller cooling solutions.

-

Inverter-driven compressor technology improving part-load efficiency, which is critical for commercial applications with variable cooling loads.

-

Residential modular chillers gaining traction as smart home adoption and energy efficiency awareness grow.

-

Climate change increasing cooling degree days in temperate regions, expanding the addressable market for chillers.

-

LEED and green building certifications driving adoption of high-efficiency modular chiller systems in new commercial construction.

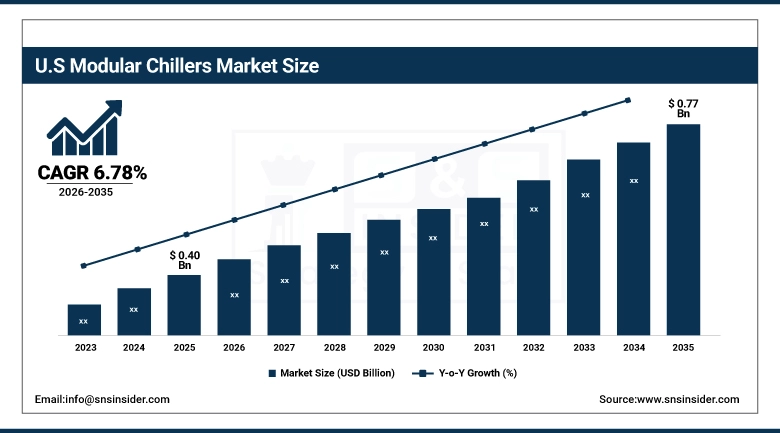

U.S. Modular Chillers Market was valued at USD 0.40 billion in 2025 and is expected to reach USD 0.77 billion by 2035, at a CAGR of 6.78% from 2026 to 2035.

The U.S. modular chillers market is boosted by larger commercial building stock, burgeoning data center industry, expansion of healthcare facilities and growing inclination towards high-efficiency cooling solutions carried out through LEED & ENERGY STAR-certified building standards. To progress our decarbonization goals, utility rebate programs and the Department of Energy's energy efficiency requirements in buildings further compel building owners to replace their inefficient legacy chiller systems with modern modular alternatives. Data Center Boom in the U.S. fueled by AI Infrastructure Investment with an Increased Demand for Scalable, Redundant Cooling Solutions.

SummaryU.S. Data Center Construction Market Booms on AI computing investment from Amazon, Google, Microsoft and Meta These data centers all need significant cooling infrastructure, and the redundancy and scalability of modular chillers lend themselves to this application as a high-value demand driver through the forecast period.

Modular Chillers Market Segment Analysis:

-

Based on Type, Water-Cooled chillers held the largest share in 2025; Air-Cooled is expected to grow at the highest CAGR of 6.45%.

-

Based on Application, Commercial led with 47.80% share; Residential is the fastest-growing application segment (CAGR 7.44%).

-

Based on Compressor Technology, Scroll compressors dominate due to compactness and quiet operation; Screw compressors are growing fastest for industrial applications.

-

Based on Capacity, 200–500 kW range is most common in commercial applications; Above 500 kW serves large industrial and data centre applications.

By Application: Commercial Dominating Residential Fastest Growing

The largest share of the market was held by commercial applications, involving office buildings, data centers, hospitals, hotels, shopping centers, and educational institutions. These facilities can benefit from cooling that is energy efficient, reliable and scales as the space usage changes. This segment is particularly influenced by the rapid development of data centers which require thousands of megawatts to be added in new cooling capacity due to large-scale capacity expansions propelled mainly by AI and cloud computing. Because unplanned cooling failures can shut down operations leading to huge losses of revenue, practically all commercial facilities enjoy the built-in redundancy that modular chillers provide.

The fastest growing are residential modular chiller systems, as advanced heat pump based modular systems to provide both heating and cooling need to be widely accepted by homeowners who desire full climate control. Central modular chiller systems for several apartments in high-density urban residential buildings provide greater efficiency and management benefits than room air conditioners at an individual level. Awareness of the smart home across various verticals and integration through remote monitoring as well as control via smartphone apps is making residential modular systems more appealing to technology-oriented consumers.

By Type: Water-Cooled Modular Chillers Dominating and Air-Cooled Modular Chillers Fastest Growing

Water cooled modular chillers release heat using the cooling tower or condenser water loop, which is much more energy efficient than air-cooled models. They are ideally suited for large commercial buildings, hospitals, and industrial plants that require maximum efficiency with the capability to handle cooling loads exceeding 500 kW. Water cooled systems have more complicated installation (a cooling tower and condenser water piping), but energy cost savings over the life of the equipment justify this investment with large scale systems.

Air-cooled modular chillers directly reject heat to the atmosphere through air-cooled condensers, eliminating the need for a cooling tower and condensed water system. They are also easier to install, making them the ideal choice for projects where installation simplicity and lower capital cost is a top priority, such as in small to medium commercial facilities (incl. They are useful in applications where water availability is limited and their flexibility makes them a true advantage. Growth within this segment has been driven by the introduction of new air-cooled modular chiller ranges with better efficiency ratings from major manufacturers such as LG, Mitsubishi and Johnson Controls.

By Compressor Technology: Scroll Compressor Dominating Screw Compressor Fastest Growing

Scroll compressors dominate the modular chiller market because of their compact size, quiet operation, reliability, and good energy efficiency at part-load conditions typical of commercial buildings. They are the standard compressor technology in most air-cooled modular chillers up to about 500 kW capacity. Their smooth, continuous compression action produces lower noise and vibration than reciprocating compressors, which is important for near-occupied spaces. Scroll compressors from Copeland, Danfoss, and Hitachi are widely used in leading modular chiller products.

screw compressors are employed, as the higher efficiency at high loads and the design to continue operating with occasional liquid refrigerant slugs make it a preferred choice. They particularly lend themselves to industrial process cooling, where continuous duty at a high load is often experienced. Modern screw chillers with variable-speed drive (VSD) compressors are up to three times as efficient under part-load conditions than older fixed-speed designs.

By Capacity: 200–500 kW dominating and Above 500 kW Fastest Growing

200-500 kW range remains at the heart of commercial modular chiller market as these equipment serves mid-sized office buildings, hotels, hospital and commercial refrigeration plants. It is the most competitive capacity range and includes products from nearly every major HVAC manufacturer. Based on step-changer compresses and fans — in almost all circumstances, these products are equipped with variable-speed drives, further enhancing their seasonal efficiency ratings

Above 500 kW is used for large hospital campuses, heavy industries like manufacturing plants, and commercial buildings. These systems typically include screw or centrifugal compressors with water cooled condensers for maximum efficiency. This capacity portion is primarily driven by the explosive growth of the data center industry; hyperscale facilities utilize various large chiller modules with thousands of kW total aggregate capacity supplied from a number of modules and include integrated redundancy.

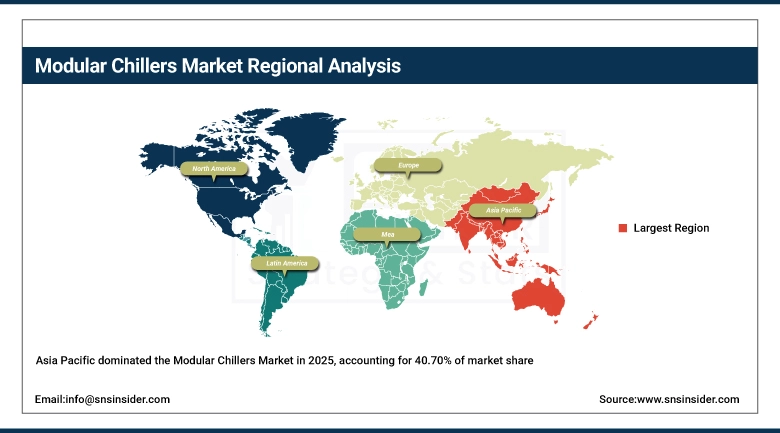

Modular Chillers Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

48% |

|

Middle East & Africa |

UAE |

40% |

|

Latin America |

Brazil |

51% |

Modular Chillers Asia Pacific Market Insights:

Asia Pacific led the overall modular chillers market, accounting for a revenue share of 40.70% propelled by rapid urbanization, industrial development and rising investment in energy-efficient HVAC infrastructure across China, India, Japan and Southeast Asia. China is a main demand driver due to its extensive commercial property development activity, ranging from data centers to office complexes. Rising energy prices are driving the growing use of modular chillers in India's fast-growing retail and hospitality sectors.

Get Customized Report as per Your Business Requirement - Enquiry Now

Modular Chillers North America Market Insights:

Modular Chillers market in North America is the second largest and growing with high pace on account of increasing demand for modular chillers from commercial and Data centre segments The boom in construction of U.S. data centers, enabled by investment to support AI computing infrastructure, is resulting in a particularly strong demand for scalable, redundant cooling solutions. Expansion of healthcare and energy efficiency mandates for government buildings are other drivers behind demand. Canadian revenue is from commercial building renovation programs and sustainable datacenter investments..

Modular Chillers Europe Market Insights:

Europe is one of the most important markets for energy-efficient modular chillers due to strict EU energy performance standards for new buildings or renovations as well as relatively high electricity prices which makes efficiency an economically critical factor and strong sustainability goals. The primary markets are Germany, France and the UK. The EU has pushed for drastic drops in energy consumption from buildings, leading to demand–as well as regulations like the Energy Efficiency and Ecodesign directives–for cooling systems that are more efficient, including high-efficiency modular chillers with inverter technology.

Modular Chillers Middle East & Africa Market Insights:

With extreme outdoor temperatures, the level of cooling demand is extremely high in the Middle East which makes it a stable and attractive market for modular chillers used in commercial buildings, data centers, and industrial facilities. Demand for large commercial cooling systems is growing as a result of major construction programs in Saudi Arabia, UAE and Qatar. NEOM in Saudi Arabia and other smart city developments across the region are built on advanced HVAC infrastructure as an essential element.

Modular Chillers Latin America Market Insights:

Latin America: Modular chiller market growing with commercial construction activity in Brazil, Mexico and Chile This was mainly due to growth in shopping center and hospitality. The hot climate of most major population centers in this region creates stable demand for cooling year-round. With Government programs to achieve better energy efficiency of commercial buildings, high- efficiency modular packages Chiller systems are now slowly picking up the market..

Modular Chillers Market Growth Drivers

-

Energy efficiency requirements and growing data center demand are the key growth drivers

Escalating electricity prices along with increasingly stringent building energy efficiency standards are driving building managers to upgrade their antiquated, inefficient, legacy chiller systems with new modular options that provide significantly higher efficiency ratings.. Concurrently, the still ongoing global data center construction boom propelled by AI, cloud computing and streaming services is generating unprecedented demand for dependable, scalable and redundant cooling infrastructure. Data centers are the best-use case for modular chillers since the redundancy of keeping a server cool when one of the cooling modules fails.

Modular chillers are both a demand drive and an industry challenge for climate change. Hotter summers in previously temperate areas of Northern Europe, the northern U.S., and Japan are catalyzing first-time cooling adoption in buildings that never had AC before, and thus expanding the TAM. At the same time, elevated ambient temperatures lead to lower chiller efficiency, and manufacturers are being challenged to develop chillers that offer high efficiency ratings over a wider range of operating temperatures.

Modular Chillers Market Restraints

-

High initial investment and refrigerant regulatory compliance create adoption barriers

A modular chiller system is much more expensive on an upfront capital cost than the purchase of individual room air conditioners or basic split systems. But for smaller commercial operators with limited capital budgets, the requirement for this initial investment represents a significant barrier to entry even where lifecycle economics would strongly favor modular systems. Furthermore, evolving regulations around refrigerant phase down per the Kigali Amendment are forcing equipment upgrades and leaving buyers unsure about the long-term regulatory compliance status of particular refrigerants.

Modular Chillers Market Opportunities

-

Smart building integration and next-generation refrigerants create premium market opportunities

The ability to integrate modular chillers into smart building management systems provides a compelling premium value proposition through the real-time load optimization, demand response participation and predictive maintenance scheduling that the combination allows—thereby creating an opportunity for higher margins. Manufacturers designing chiller systems that integrate with building automation systems of leading market vendors can target higher-end commercial segments. With the shift to next-generation low-GWP refrigerants like R-454B and R-290, manufacturers can establish technological leadership by being the first or most ready to bring development methodology on refrigerant-compatible product to market.

Modular Chillers Recent Developments

-

2025: Johnson Controls introduced the York YLAA air-cooled modular chiller series using R-454B low-GWP refrigerant with a magnetic bearing oil-free centrifugal compressor option, delivering 40% lower GWP than HFC alternatives while improving energy efficiency ratings for commercial applications.

-

2024: LG Electronics launched an advanced residential modular chiller with integrated IoT monitoring and smartphone control, featuring automatic demand response capabilities that reduce peak electricity consumption and qualify owners for utility rebate programs in several U.S. states.

-

2023: Mitsubishi Electric introduced the CITY MULTI R3 modular chiller system with an enhanced inverter-driven compressor capable of maintaining full capacity at outdoor temperatures up to 52°C, addressing the growing market in hot climate regions including the Middle East and South Asia.

Modular Chillers Key Players

-

Trane Technologies plc

-

Johnson Controls International plc

-

Daikin Industries Ltd.

-

Mitsubishi Electric Corporation

-

LG Electronics Inc.

-

Midea Group

-

Gree Electric Appliances Inc.

-

Haier Group Corporation

-

Frigel Firenze S.p.A.

-

Aermec S.p.A.

-

Smardt Chiller Group Inc.

-

Dunham-Bush Group

-

Climaveneta S.p.A. (Mitsubishi Electric Hydronics & IT Cooling)

-

McQuay Air-Conditioning Ltd. (Daikin legacy brand)

-

Blue Star Limited

-

Thermax Limited

-

Schneider Electric SE (HVAC integration solutions)

-

Nanjing TICA Climate Solutions Co., Ltd

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.31 Billion |

| Market Size by 2035 | USD 6.11 Billion |

| CAGR | CAGR of 6.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Water-Cooled, Air-Cooled) • By Application( Commercial, Residential, Industrial) • By Compressor Technology (Scroll, Screw, Centrifugal) • By Capacity (Below 200 kW, 200–500 kW, Above 500 kW) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Carrier Global Corporation, Trane Technologies plc, Johnson Controls International plc, Daikin Industries Ltd., Mitsubishi Electric Corporation, LG Electronics Inc., Midea Group, Gree Electric Appliances Inc., Haier Group Corporation, Multistack LLC, Frigel Firenze S.p.A., Aermec S.p.A., Smardt Chiller Group Inc., Dunham-Bush Group, Climaveneta S.p.A., McQuay Air-Conditioning Ltd., Blue Star Limited, Thermax Limited, Schneider Electric SE, Nanjing TICA Climate Solutions Co., Ltd. |

Frequently Asked Questions

Asia Pacific leads with 40.70% revenue share, driven by rapid urbanization and commercial construction in China, India, and Southeast Asia.

Air-Cooled modular chillers are growing at the highest CAGR of 6.45%, driven by simpler installation and growing adoption in small commercial and residential applications.

Commercial applications lead with 47.80% market share, with data centers being a key growth driver within this segment.

The Modular Chillers Market was valued at USD 3.31 billion in 2025.

The Modular Chillers Market is expected to grow at a CAGR of 6.33% from 2026 to 2035.

Get in Touch