mRNA Therapeutics Contract Development & Manufacturing Market Report Scope & Overview:

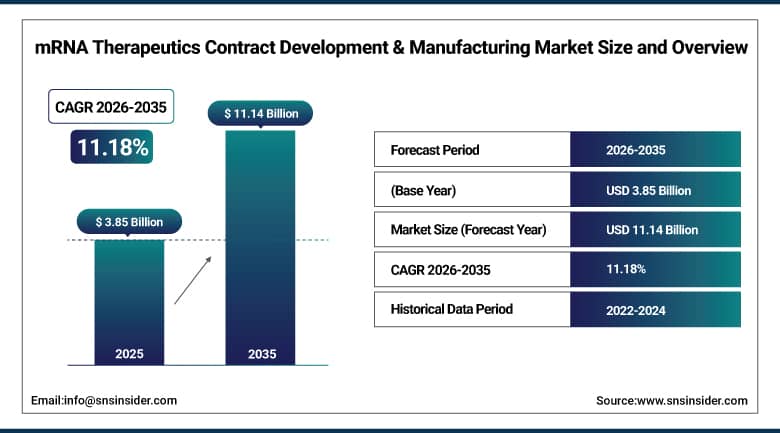

The mRNA Therapeutics Contract Development & Manufacturing Market was valued at USD 3.85 Billion in 2025 and is expected to reach USD 11.14 Billion by 2035, growing at a CAGR of 11.18% from 2026–2035.

The global mRNA therapeutics contract development and manufacturing market is experiencing robust growth driven by the commercial validation of mRNA technology from COVID-19 vaccine programme’s, expanding mRNA therapeutic pipeline across cancer immunotherapy, rare genetic disease, and protein replacement therapy applications, and the pharmaceutical industry's growing outsourcing of specialized mRNA production to CDMOs. mRNA CDMO services encompass plasmid DNA production, in vitro transcription, lipid nanoparticle formulation, aseptic fill/finish, analytical testing, and regulatory submission support whose combined technical complexity creates commercial motivation for pharmaceutical and biotech companies to partner with specialist CDMOs rather than build proprietary mRNA manufacturing infrastructure.

In January 2025, Meiji Seika Pharma received approval to add domestic manufacturing sites in Japan for KOSTAIVE, its self-amplifying mRNA COVID-19 vaccine, amending its manufacturing and marketing approval to enhance local production capacity. This milestone demonstrates the commercial maturation of self-amplifying mRNA technology beyond conventional modRNA platforms, creating a new CDMO service category whose saRNA production requirements differ from conventional mRNA manufacturing and create differentiated commercial opportunity for CDMOs capable of supporting the next generation of mRNA vaccine and therapeutic modalities.

Market Size and Forecast:

-

Market Size in 2026E: USD 4.28 Billion

-

Market Size by 2035: USD 11.14 Billion

-

CAGR: 11.18% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On mRNA Therapeutics Contract Development & Manufacturing Market - Request Free Sample Report

mRNA Therapeutics Contract Development & Manufacturing Market Trends:

-

Development of self-amplifying mRNA technologies is creating new manufacturing opportunities as lower-dose formulations require specialized production and formulation expertise

-

Growth of personalized cancer vaccines is driving demand for flexible CDMO capabilities that support rapid, patient-specific mRNA manufacturing and GMP production

-

Integration of AI, automation, and advanced analytics is improving mRNA process development, formulation optimization, quality control, and manufacturing efficiency

-

Expansion of GMP-grade plasmid DNA production is becoming a critical capability as high-quality template materials are essential for mRNA manufacturing and regulatory compliance

-

Increasing application of mRNA technologies in oncology, rare diseases, cardiovascular disorders, and other therapeutic areas is broadening demand for specialized CDMO development and manufacturing services beyond vaccines

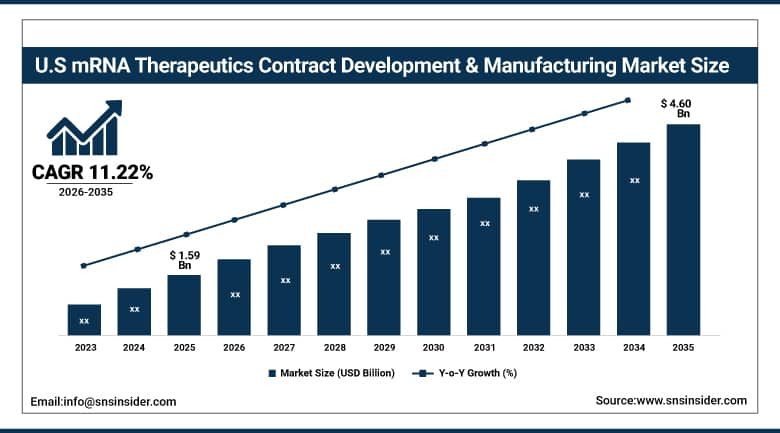

U.S. mRNA Therapeutics Contract Development & Manufacturing Market Outlook:

The U.S. mRNA Therapeutics Contract Development & Manufacturing Market was valued at approximately USD 1.59 Billion in 2025 and is expected to reach approximately USD 4.60 Billion by 2035, growing at a CAGR of approximately 11.22%.

The U.S. is the most commercially significant mRNA CDMO market within North America's dominant 45% global revenue position. Lonza's U.S. CDMO operations, Catalent's mRNA manufacturing capability, Thermo Fisher Scientific's Patheon division, TriLink BioTechnologies, and Aldevron (Danaher) collectively define the domestic mRNA CDMO commercial landscape. The FDA's supportive regulatory environment for mRNA-based therapies, the U.S. biopharmaceutical industry's extraordinary mRNA clinical pipeline, and BARDA's continued investment in mRNA vaccine manufacturing preparedness create the world's most commercially advanced mRNA CDMO demand environment. Multiple personalized cancer vaccine Phase II/III programmes and the expanding mRNA therapeutics IND pipeline create structured CDMO procurement whose commercial scale grows with each clinical programme advance.

In February 2023, Moderna forged an agreement with Life Edit Therapeutics to address genetic diseases using mRNA-based gene editing, combining Moderna's mRNA platform with Life Edit's specialized gene editing capabilities including the precise technique of base editing. The collaboration demonstrates the expansion of mRNA technology applications from vaccine-only to genetic disease treatment, creating new CDMO service requirements for precision mRNA manufacturing that supports gene-editing therapeutic programme’s whose technical complexity exceeds conventional mRNA vaccine manufacturing specifications.

mRNA Therapeutics Contract Development & Manufacturing Market Segment Analysis:

-

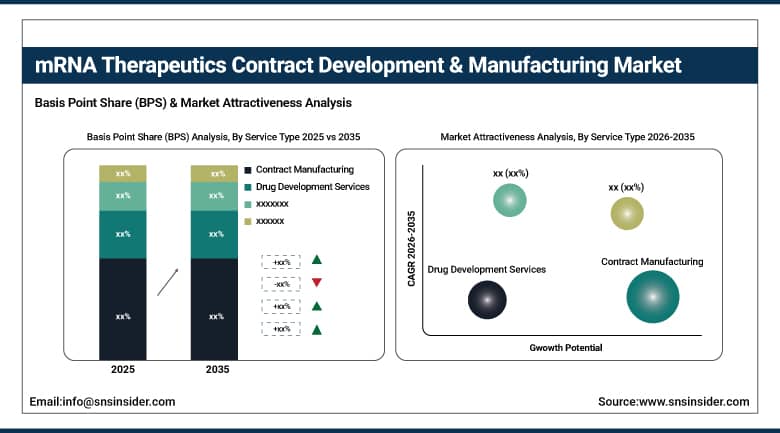

By Service Type, the Contract Manufacturing segment dominated the mRNA Therapeutics CDM Market with approximately 48% share in 2025, while the Drug Development Services segment is the fastest growing.

-

By Application, the Viral Vaccines segment dominated the mRNA Therapeutics CDM Market with approximately 52% share in 2025, while the Cancer Immunotherapy segment is the fastest growing.

-

By Indication, the Infectious Diseases segment dominated the mRNA Therapeutics CDM Market with approximately 58% share in 2025, while the Metabolic & Genetic Diseases segment is the fastest growing.

-

By End User, the Biotechnology Companies segment dominated the mRNA Therapeutics CDM Market with approximately 42% share in 2025, while the Pharmaceutical Companies segment is the fastest growing.

By Service Type, contract manufacturing dominates, drug development grows fastest

Contract manufacturing services retained the dominant position with approximately 48% of the mRNA therapeutics CDM market in 2025. The mRNA CDMO's primary commercial value proposition is its ability to manufacture GMP-grade mRNA drug substance and drug product for clients whose own manufacturing infrastructure cannot efficiently or economically produce clinical and commercial mRNA supply. The technical complexity of mRNA GMP manufacturing encompasses plasmid DNA template quality management, in vitro transcription reaction optimization, RNA purification from reaction by-products, lipid nanoparticle encapsulation at defined size distribution and encapsulation efficiency, and aseptic fill/finish under stringent cold-chain conditions whose combined requirement creates specialized CDMO capability that generalist pharmaceutical CMOs cannot provide equivalently.

Drug development services are the fastest-growing segment because the extraordinary mRNA therapeutic pipeline expansion is creating above-average demand for early-stage development services whose IVT process development, LNP formulation screening, preclinical manufacturing, and analytical method development create the commercial engagement that precedes and defines subsequent manufacturing programme scope. Each new mRNA therapeutic programme that enters IND-enabling studies creates drug development service procurement whose timeline from sequence optimization through GLP manufacturing and clinical batch production creates multi-year CDMO engagement whose total programme value substantially exceeds individual batch manufacturing fees.

By Application, viral vaccines dominate, cancer immunotherapy grows fastest

Viral vaccines retained the dominant application position with approximately 52% of the mRNA therapeutics CDM market in 2025. The commercial validation of mRNA COVID-19 vaccines established viral vaccine as the mRNA application category with the most commercially mature CDMO manufacturing infrastructure, the most regulatory submission experience, and the most established quality standard framework. The COVID-19 vaccine commercial manufacturing programmes created the global mRNA CDMO capacity buildout whose repurposing for RSV vaccine, influenza mRNA vaccine development, and pandemic preparedness manufacturing creates consistent CDMO procurement demand. Moderna and BioNTech's mRNA vaccine platform extension into RSV, CMV, EBV, and HIV vaccine development creates sustained CDMO manufacturing demand beyond the COVID-19 programme cycle.

Cancer immunotherapy is the fastest-growing application because personalized neoantigen mRNA vaccine programme’s, including BioNTech and Moderna's mRNA neoantigen vaccine Phase III collaborations with Merck, create the most commercially transformative new mRNA therapeutic application category. Each personalized cancer vaccine programme whose patient-specific neoantigen sequence requires individual GMP mRNA manufacturing within defined clinical timelines creates a CDMO service model fundamentally different from standard vaccine manufacturing, requiring flexible small-volume rapid-turnaround capabilities whose specialized commercial model creates differentiated above-commodity CDMO pricing.

By Indication, infectious diseases dominate, metabolic & genetic grows fastest

Infectious diseases retained the dominant indication with approximately 58% of the mRNA therapeutics CDM market in 2025. The COVID-19 vaccine emergency use authorization and full approval created the most commercially significant single-indication CDMO manufacturing programme in pharmaceutical history whose capacity investment repurposed across RSV, influenza, and emerging pathogen vaccine development sustains infectious disease as the dominant indication. The global health security landscape's recognition of mRNA vaccine platforms’ rapid response capability for emerging infectious disease threats creates government procurement commitment for mRNA manufacturing capacity whose commercial certainty sustains CDMO infrastructure investment.

Metabolic and genetic diseases are the fastest-growing indication because the extraordinary unmet medical need in rare metabolic and genetic conditions whose existing enzyme replacement and gene therapy treatments have created proof-of-concept for mRNA-based protein supplementation and gene editing approaches. Moderna’s propionic acidemia, methylmalonic acidemia, and glycogen storage disease mRNA therapeutic programme’s, combined with multiple rare disease biotech companies’ mRNA platform investments, create a growing CDMO demand segment whose per-programme commercial value substantially exceeds infectious disease vaccine manufacturing economics.

By End User, biotech companies dominate, pharmaceutical companies grow fastest

Biotechnology companies retained the dominant end-user position with approximately 42% of the mRNA therapeutics CDM market in 2025. Biotech companies with mRNA-native technology platforms including Moderna, BioNTech, CureVac, and Arctus Biotherapeutics, combined with early-stage mRNA therapeutics companies whose programmes are advancing through clinical development, create the most commercially concentrated mRNA CDMO customer segment. The biotech company's typical outsourcing model, where internal manufacturing infrastructure is maintained at development scale while commercial manufacturing is delegated to CDMO partners, creates enduring long-duration CDMO relationships whose programme value grows with each clinical stage advance.

Pharmaceutical companies are the fastest-growing end user because established pharmaceutical companies’ progressive adoption of mRNA modality for vaccine, therapeutics, and combination product development creates growing CDMO partnership demand from organizations whose internal biologics manufacturing infrastructure requires supplementation with specialized mRNA capability. AstraZeneca's mRNA platform investment, Sanofi’s mRNA vaccine collaboration, and multiple large pharma companies’ mRNA pipeline acquisitions collectively create structured CDMO demand from pharmaceutical sector customers whose procurement scale substantially exceeds early-stage biotech equivalents.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America mRNA Therapeutics CDM Market Insights

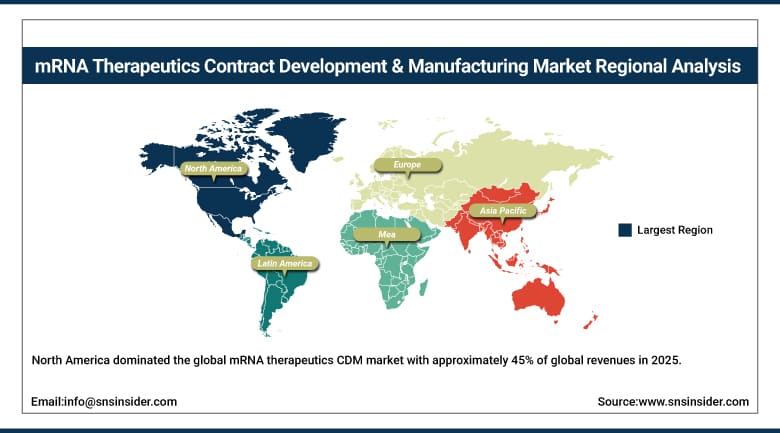

North America dominated the global mRNA therapeutics CDM market with approximately 45% of global revenues in 2025, driven by strong presence of biotech companies, research institutions, and a supportive regulatory environment. The United States accounts for approximately 87.4% of North American revenues through Lonza, Catalent, Thermo Fisher Scientific's Patheon, TriLink BioTechnologies, and Aldevron's combined commercial presence whose mRNA CDMO portfolio defines the global service standard.

Canada contributes approximately 12.6% of North American revenues through its active mRNA research community, Precision BioSciences and other biotech companies’ CDMO partnerships, and the National Research Council's mRNA manufacturing capability investment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe mRNA Therapeutics CDM Market Insights

Europe is a technically sophisticated mRNA therapeutics CDM market where BioNTech's German headquarters, Lonza's Swiss CDMO operations, Wacker Biotech's German mRNA manufacturing, and the EMA's regulatory framework create a comprehensive mRNA CDMO ecosystem. Germany accounts for approximately 22.3% of European revenues through BioNTech's domestic manufacturing, Wacker Biotech’s mRNA production capability, and the pharmaceutical industry’s mRNA partnership investment.

The United Kingdom, Belgium, and the Netherlands are significant secondary European markets where AstraZeneca’s Cambridge mRNA programme, UCB’s mRNA investment, and CDMOs including Recipharm and AGC Biologics’ European operations create consistent mRNA CDMO procurement.

Asia Pacific mRNA Therapeutics CDM Market Insights

Asia Pacific is the fastest-growing regional mRNA therapeutics CDM market, driven by China's growing mRNA vaccine programme, Japan's self-amplifying mRNA commercial approval, South Korea's Samsung Biologics mRNA capability, and India's emerging mRNA CDMO infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic mRNA vaccine development programme, WUXI Biologics’ mRNA manufacturing capability, and the government's biopharmaceutical manufacturing investment.

Japan represents a commercially significant market where the domestic approval of KOSTAIVE self-amplifying mRNA vaccine in January 2025 demonstrates the region's progressive regulatory acceptance of next-generation mRNA modalities, creating commercial precedent that sustains Japan's mRNA CDMO market development.

MEA & Latin America mRNA Therapeutics CDM Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s biopharmaceutical manufacturing investment, healthcare localization initiative, CDMO sector development policies, and the growing domestic mRNA vaccine programme creating structured CDMO procurement. The UAE’s specialty pharmaceutical manufacturing investment and Egypt’s expanding vaccine production capacity add complementary Gulf and North African regional demand. Brazil leads Latin American revenues at approximately 44.2% through Fiocruz’s mRNA vaccine manufacturing partnership with BioNTech, government biopharmaceutical capability investment, and the growing biotech sector. Argentina’s life sciences research and Mexico’s pharmaceutical sector collectively sustain Latin American CDM market development through 2035.

Market Dynamics:

Growth Drivers: mRNA therapeutic pipeline expansion and personalized medicine creating above-average CDMO service demand

The mRNA therapeutic pipeline's expansion from vaccine-only toward oncology, rare disease, cardiovascular, and protein replacement therapy applications is the mRNA CDMO market's most commercially transformative structural growth driver. Each new mRNA therapeutic programme that advances from discovery through IND-enabling studies, Phase I, Phase II, and Phase III creates a progression of CDMO service procurement whose aggregate commercial value increases with each clinical stage advancement. The BioNTech-Merck mRNA personalized cancer vaccine Phase III, Moderna's mRNA-1283 next-generation COVID vaccine, and multiple rare disease mRNA therapeutic programmes collectively create the mRNA CDMO pipeline whose commercial materialization sustains market growth through the forecast period.

Personalized medicine's adoption of mRNA technology for patient-specific therapeutic applications creates the most commercially premium CDMO service category whose individual patient manufacturing requirement creates per-batch commercial relationships with above-standard-vaccine pricing. Each personalized neoantigen vaccine programme that identifies patient-specific tumor mutations, synthesizes corresponding mRNA sequences, and manufactures GMP individual patient doses within 6-8 weeks creates CDMO service demand whose unique technical and timeline requirements create differentiated commercial relationships.

Restraints: Cold-chain infrastructure requirement and LNP manufacturing scale-up complexity

mRNA therapeutic products’ requirement for continuous cold-chain storage and distribution at -20°C or -70°C creates infrastructure investment requirements for both CDMO manufacturing operations and downstream distribution logistics that add cost and operational complexity relative to conventional small molecule pharmaceutical manufacturing. Each new mRNA therapeutic programme that requires cold-chain distribution infrastructure creates supply chain investment whose cost is amortized across manufacturing programme economics.

LNP manufacturing scale-up complexity creates technical barriers that limit the pace at which CDMOs can expand mRNA therapeutic manufacturing capacity. The microfluidic mixing processes that produce LNPs at laboratory scale do not readily translate to large-scale manufacturing without process development investment whose timeline creates capacity bottlenecks when multiple clinical programmes simultaneously require commercial-scale LNP manufacturing.

Opportunities: Self-amplifying mRNA manufacturing and mRNA-based gene editing therapeutic CDMO services

Self-amplifying mRNA technology's smaller dose requirement creates a manufacturing economics advantage who’s lower per-dose antigen mass requirement reduces both API cost and manufacturing batch size relative to conventional mRNA vaccines. Each self-amplifying mRNA programme that advances to clinical and commercial manufacturing creates a CDMO service requirement whose differentiated technical capability creates commercial opportunities for CDMOs investing in saRNA-specific manufacturing process development.

mRNA-based gene editing therapeutic CDMO services represent the most commercially premium emerging opportunity whose technical complexity, combining mRNA delivery with gene editing payload, creates above-conventional-mRNA manufacturing specifications requiring specialized CDMO capability investment whose early commercial relationships create sustainable competitive advantage.

Recent Developments:

-

2025: Meiji Seika Pharma received approval in January 2025 to add domestic manufacturing sites in Japan for KOSTAIVE, its self-amplifying mRNA COVID-19 vaccine, enhancing local production capacity for next-generation mRNA vaccine modalities.

-

2024: Lonza expanded its mRNA CDMO capabilities in 2024 with new GMP manufacturing suites at its Visp, Switzerland facility dedicated to lipid nanoparticle formulation and fill/finish for clinical-stage mRNA therapeutic programmes, targeting the growing personalized medicine and rare disease mRNA pipeline.

-

2024: Catalent invested in expanded mRNA manufacturing infrastructure in 2024 at its Bloomington, Indiana facility, adding in vitro transcription and RNA purification capacity to serve the growing pharmaceutical company outsourcing demand for mRNA therapeutic clinical supply.

-

2023: Moderna forged an agreement with Life Edit Therapeutics in February 2023 to address genetic diseases using mRNA-based gene editing, combining Moderna's mRNA platform with Life Edit's base editing capabilities, creating new CDMO service requirements for precision mRNA therapeutic manufacturing.

-

2023: Thermo Fisher Scientific expanded its Patheon mRNA CDMO services in 2023 with new analytical testing capability for mRNA sequence integrity, LNP characterization, and stability testing, serving the growing pharmaceutical and biotech client base requiring comprehensive mRNA drug product quality services.

mRNA Therapeutics Contract Development & Manufacturing Market Key Players:

-

Lonza Group AG

-

Catalent Inc. (Novo Holdings)

-

Thermo Fisher Scientific Inc. (Patheon)

-

Aldevron LLC (Danaher Corporation)

-

TriLink BioTechnologies

-

Wacker Biotech GmbH

-

AGC Biologics

-

Recipharm AB

-

Samsung Biologics Co. Ltd.

-

WuXi Biologics Co. Ltd.

-

BIOMAY AG

-

Kaneka Eurogentec S.A.

-

eTheRNA immunotherapies nv

-

Biocina d.o.o.

-

Arcturus Therapeutics Holdings

-

CureVac SE

-

Precision BioSciences Inc.

-

ProQR Therapeutics

-

Orna Therapeutics

-

Moderna Inc.

mRNA Therapeutics Contract Development & Manufacturing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.85 Billion |

| Market Size by 2035 | USD 11.14 Billion |

| CAGR | CAGR of 11.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Service Type (Contract Manufacturing, Drug Development Services, Analytical & Testing Services, Regulatory & Compliance Services, Others) • by Application (Viral Vaccines, Protein Replacement Therapies, Cancer Immunotherapy, Rare Genetic Disease Therapies, Others) • by Indication (Infectious Diseases, Metabolic & Genetic Diseases, Oncology, Cardiovascular Diseases, Others) • by End User (Biotechnology Companies, Pharmaceutical Companies, Academic & Research Institutions, Government & Non-Profit Organizations) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Lonza Group AG, Catalent Inc. (Novo Holdings), Thermo Fisher Scientific Inc. (Patheon), Aldevron LLC (Danaher Corporation), TriLink BioTechnologies, Wacker Biotech GmbH, AGC Biologics, Recipharm AB, Samsung Biologics Co. Ltd., WuXi Biologics Co. Ltd., BIOMAY AG, Kaneka Eurogentec S.A., eTheRNA immunotherapies nv, Biocina d.o.o., Arcturus Therapeutics Holdings, CureVac SE, Precision BioSciences Inc., ProQR Therapeutics, Orna Therapeutics, Moderna Inc. |

Frequently Asked Questions

The mRNA Therapeutics Contract Development & Manufacturing Market is expected to grow at a CAGR of 11.18% from 2026 to 2035.

The mRNA Therapeutics Contract Development & Manufacturing Market was valued at USD 3.85 Billion in 2025.

The expanding mRNA therapeutic pipeline beyond infectious disease vaccines into oncology, rare genetic disease, and protein replacement therapy creating above-average CDMO service procurement, and personalized medicine's adoption of patient-specific mRNA neoantigen cancer vaccines creating premium manufacturing service relationships.

Viral Vaccines dominated the market with approximately 52% share in 2025, while Cancer Immunotherapy is the fastest growing segment.

North America dominated the mRNA Therapeutics Contract Development & Manufacturing Market with approximately 45% of global revenues in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch