Multi Crystalline Silicon Market Report Scope & Overview:

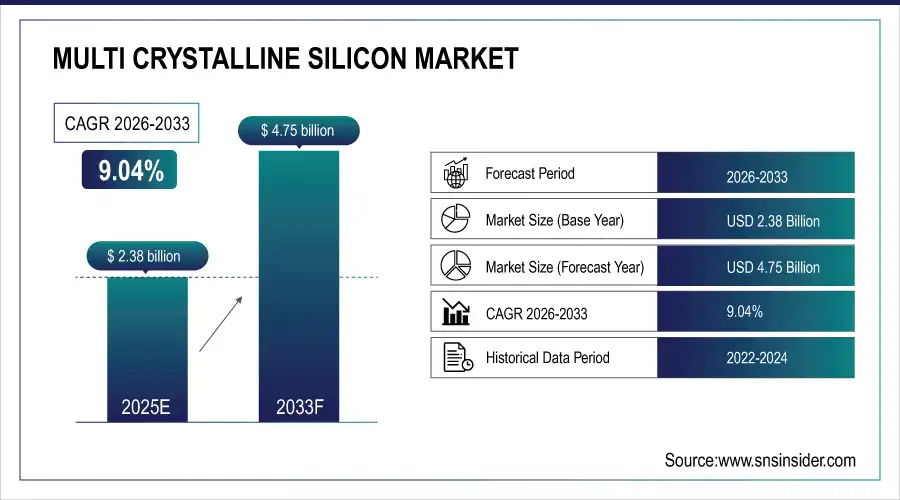

The Multi Crystalline Silicon Market size was valued at USD 2.38 Billion in 2025E and is projected to reach USD 4.75 Billion by 2033, growing at a CAGR of 9.04% during 2026–2033.

The Multi Crystalline Silicon Market is witnessing strong demand growth, driven by accelerating adoption of renewable energy solutions and increasing deployment of photovoltaic systems worldwide. Because silicon remains a cost‑effective and high‑efficiency semiconductor material, its multi crystalline variant is widely used in solar panel manufacturing and electronics. This cause, expanding energy transition initiatives and consumer preference for clean power, effects greater investments and enhanced capacity expansions by industry players, improving production scalability and cost optimization across regions.

Multi Crystalline Silicon Market Size and Forecast:

-

Market Size in 2025E: USD 2.38 Billion

-

Market Size by 2033: USD 4.75 Billion

-

CAGR: 9.04% from 2025 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information On Multi Crystalline Silicon Market - Request Free Sample Report

Key Multi Crystalline Silicon Market Trends

-

Increasing renewable energy mandates and government incentives are accelerating multi crystalline silicon adoption in solar PV systems.

-

Advances in cell manufacturing technologies are reducing production costs and improving module efficiency.

-

Demand from electronics and semiconductor applications is expanding due to reliability and performance advantages.

-

Integration with utility‑scale solar farms is boosting demand for high‑volume silicon wafers.

-

Strategic capacity additions by major manufacturers enhance supply chain robustness.

-

Growing investments in clean tech infrastructure are supporting long‑term adoption.

U.S. Multi Crystalline Silicon Market Insights:

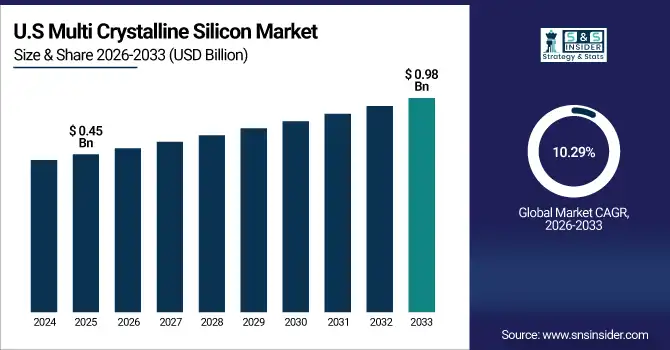

The U.S. Multi Crystalline Silicon Market size was USD 0.45 billion in 2025E and is expected to reach USD 0.98 billion by 2033, growing at a CAGR of 10.29% over the forecast period of 2026–2033. Because aggressive renewable energy targets and solar project deployments are increasing nationwide, this cause, favorable policies and utility investments, effects sustained demand for multi crystalline silicon. Rising electronics manufacturing further amplifies adoption, enhancing domestic supply chain investments and technology improvements.

Multi Crystalline Silicon Market Driver:

-

Growing Utility‑Scale Solar Deployment Accelerates Demand for Multi Crystalline Silicon

As global energy transitions favor renewables, expansion of utility‑scale solar projects has significantly increased demand for multi crystalline silicon. Because large solar farms require cost‑effective and scalable PV materials, this cause, rising project pipelines, effects higher silicon wafer production and investment in advanced manufacturing. Enhanced adoption in emerging markets and supportive policies create economies of scale, reducing per‑unit costs and fostering competitive advantages for producers. Greater integration with storage and grid infrastructure further cements multi crystalline silicon’s role.

In May 2025, a major utility announced a 500 MW solar farm expansion using multi crystalline silicon modules, highlighting cost savings over alternative materials and faster installation timelines. This deployment resulted in improved project economics and set benchmarks for future renewable energy builds.

Multi Crystalline Silicon Market Restraint:

-

Volatility in Polysilicon Feedstock Costs Limits Market Expansion

Because raw polysilicon feedstock prices fluctuate due to supply constraints and energy cost variability, this cause, rising input costs, effects pressure on multi crystalline silicon margins and pricing strategies. Higher feedstock expenses can delay production expansions, reduce profitability, and limit smaller manufacturers from scaling. Additionally, price unpredictability complicates long‑term contracts and investment planning, slowing adoption rates in cost‑sensitive regions and competing technologies.

In 2024, several producers postponed capacity additions after polysilicon feedstock prices surged unexpectedly, raising final silicon wafer costs and prompting buyers to defer purchases until price stability returned, illustrating how commodity swings impact production decisions.

Multi Crystalline Silicon Market Opportunity:

-

Integration of Advanced Crystal Growth Technologies Enhances Market Potential

Because continuous R&D is improving crystal growth processes and reducing defect rates, this cause, technological advancements, effects higher yield and performance of multi crystalline silicon wafers. These improvements support cost competitiveness with mono‑crystalline alternatives, expanding adoption across high‑efficiency modules and electronics. Enhanced automation reduces waste and improves throughput, offering producers differentiation. Increasing demand for high‑reliability semiconductor components presents additional growth avenues, especially in specialized applications beyond traditional solar.

In September 2025, a silicon manufacturer launched an advanced crystal furnace that increased wafer yield by 8%, enabling customers to produce higher‑efficiency solar modules while lowering overall production costs, demonstrating practical benefits of technology integration.

Multi Crystalline Silicon Market Segmentation Analysis:

By Grade, Solar-Grade Multi Crystalline Silicon Segment Dominates with 69% Share in 2025, Electronic-Grade to Record Fastest Growth with 11.06% CAGR

The Solar-Grade Multi Crystalline Silicon segment held a dominant market share of approximately 69% in 2025. Because solar grade silicon is optimized for photovoltaic performance and cost efficiency, this cause, broad adoption in utility-scale and residential solar projects, effects widespread deployment in global renewable energy systems. Continuous advancements in production processes improve cell conversion efficiency and module reliability, enabling manufacturers to scale operations while supporting global clean energy transition goals.

The Electronic-Grade Multi Crystalline Silicon segment is expected to experience the fastest growth over 2026–2033, with a CAGR of 11.06%. Because high-purity materials are critical for semiconductors and electronic devices, this cause, increasing demand for connected devices and high-reliability applications, effects rapid adoption of electronic-grade silicon. Improvements in purity control and defect reduction enhance performance for precision electronics, expanding its market relevance beyond traditional solar applications.

By Production, Wafer Silicon Segment Dominates with 42% Share in 2025, Cell Silicon to Record Fastest Growth with 10.62% CAGR

The Wafer Silicon segment held the largest market share of around 42% in 2025. Because wafer silicon serves as the foundational input for PV cell assembly and electronic fabrication, this cause, integration into module and device production, effects strong revenue contribution. Advancements in slicing, surface quality, and wafer consistency further improve output efficiency, enabling manufacturers to meet diverse application requirements and scale PV and electronics supply chains.

The Cell Silicon segment is expected to experience the fastest growth over 2025–2033, with a CAGR of 10.62%. Because finished cell components are critical for module assembly and solar installations, this cause, growing downstream solar deployment, effects increased demand for high-efficiency cell silicon. Technological improvements in cell design, integration, and performance optimization further boost adoption across global PV manufacturing.

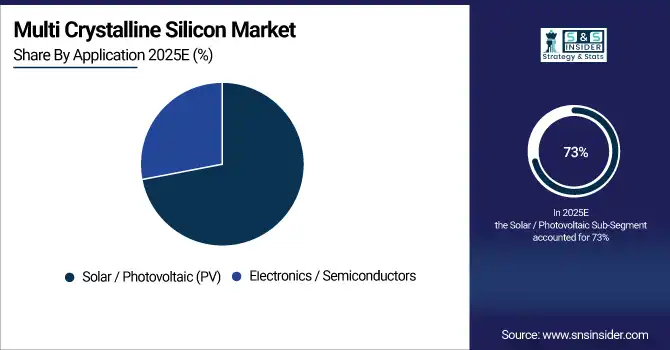

By Application, Solar / Photovoltaic (PV) Segment Dominates with 73% Share in 2025, Electronics / Semiconductors to Record Fastest Growth with 12.17% CAGR

The Solar / Photovoltaic (PV) segment held a dominant market share of approximately 73% in 2025. Because PV systems remain the largest end-use application for multi crystalline silicon, this cause, global renewable energy targets and cost-effective panel production, effects widespread adoption in residential, commercial, and utility-scale installations. Improvements in manufacturing and government incentives further support PV penetration, sustaining multi crystalline silicon demand.

The Electronics / Semiconductors segment is expected to experience the fastest growth over 2026–2033, with a CAGR of 12.17%. Because electronic devices and components require high-quality, reliable silicon, this cause, increasing IoT, 5G, and semiconductor production, effects strong market growth. Enhanced purity, processing improvements, and high reliability of multi crystalline silicon expand its adoption in advanced electronics applications.

By End User, Commercial & Industrial Segment Leads with 62% Share in 2025, Residential Segment to Record Fastest Growth with 10.51% CAGR

The Commercial & Industrial segment held a dominant market share of around 62% in 2025. Because large-scale solar investments from utilities and enterprises drive high-volume purchases, this cause, economies of scale and cost effectiveness, effects substantial revenue contribution from commercial & industrial installations. Long-term power purchase agreements and large project pipelines further strengthen sustained multi crystalline silicon demand.

The Residential segment is expected to experience the fastest growth over 2026–2033, with a CAGR of 10.51%. Because homeowners are increasingly adopting solar solutions to reduce energy costs and enhance energy independence, this cause, growing residential electrification trends, effects rapid adoption of multi crystalline silicon modules. Affordable and efficient solar solutions support broader market penetration in the residential sector.

Multi Crystalline Silicon Market Regional Insights

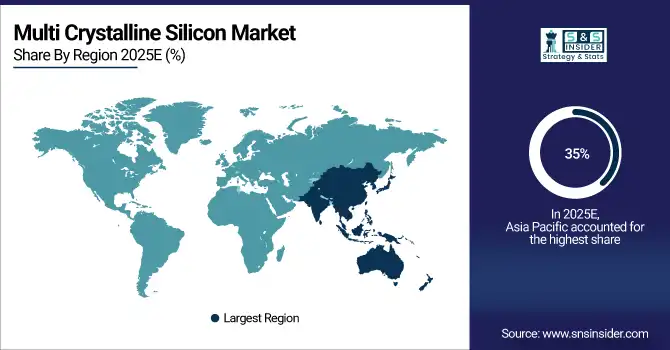

Asia Pacific Dominates Multi Crystalline Silicon Market in 2025

In 2025, Asia Pacific commands an estimated 35% share of the Multi Crystalline Silicon Market, driven by its strong PV manufacturing capacity and aggressive solar deployment policies. The region benefits from large-scale production hubs in China and India, supporting both domestic and export markets. Government incentives and renewable energy mandates accelerate module production and integration, making Asia Pacific the focal point for multi crystalline silicon adoption and technology investment.

China is the dominating country in Asia Pacific, with massive solar panel manufacturing capacity and extensive domestic renewable energy deployment. Because China maintains highly integrated supply chains, this cause, cost efficiency and large-scale production, effects significant exports and regional influence. Rapid electrification, utility-scale solar projects, and growing electronics manufacturing further boost multi crystalline silicon demand, establishing China as the central driver of market growth in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is the Fastest-Growing Region in Multi Crystalline Silicon Market in 2025

North America is projected to grow at an estimated CAGR of 10.9% in 2025, fueled by increasing renewable mandates, residential solar adoption, and expanding utility-scale PV installations. Investments in clean energy infrastructure, combined with favorable policy frameworks, accelerate the deployment of multi crystalline silicon modules across the region.

The United States dominates North America’s Multi Crystalline Silicon Market due to its mature solar energy ecosystem, growing electronics manufacturing demand, and supportive federal and state incentives. Because domestic policies encourage renewable energy investments, this cause, stable project pipelines and local manufacturing growth, effects rapid adoption of multi crystalline silicon. Strong R&D focus and production capacity enhancements further solidify the U.S. as the primary contributor to regional market expansion.

Europe Multi Crystalline Silicon Market Insights, 2025

Europe held a significant portion of the Multi Crystalline Silicon Market in 2025, driven by renewable energy targets, sustainability policies, and PV deployment incentives. Because stringent emissions standards and supportive regulations exist, this cause, increased solar installations, effects higher demand for multi crystalline silicon.

Germany leads Europe’s Multi Crystalline Silicon Market due to robust solar adoption, federal renewable energy programs, and advanced manufacturing ecosystems that prioritize clean energy transitions. The country’s emphasis on digitalized energy infrastructure, industrial innovation, and regional cooperation strengthens its market leadership. Germany’s integrated production and policy support further drive technology adoption and reinforce its dominance within Europe.

Middle East & Africa and Latin America Multi Crystalline Silicon Market Insights, 2025

In 2025, Middle East & Africa and Latin America showed steady growth in the Multi Crystalline Silicon Market, driven by rising solar investments, expanding electrification needs, and high renewable energy potential. Because both regions prioritize energy security and sustainable development, this cause, strategic renewable initiatives, effects increased adoption of cost-effective silicon materials.

In Latin America, Brazil dominates due to extensive utility-scale PV projects and a focus on export-oriented solar energy production. In the Middle East, the UAE leads adoption through ambitious clean energy strategies and desert solar initiatives. Both regions demonstrate growing market relevance, with investments and government programs supporting multi crystalline silicon deployment and future growth opportunities.

Multi Crystalline Silicon Market Key Players:

-

Wacker Chemie AG

-

GCL-Poly Energy Holdings Limited

-

OCI Company Ltd.

-

REC Silicon ASA

-

Daqo New Energy Corp.

-

JinkoSolar Holding Co., Ltd.

-

Trina Solar Limited

-

Canadian Solar Inc.

-

LONGi Green Energy Technology Co., Ltd.

-

JA Solar Technology Co., Ltd.

-

Hanwha Q CELLS Co., Ltd.

-

ReneSola Ltd.

-

SunPower Corporation

-

First Solar, Inc.

-

Motech Industries Inc.

-

Yingli Green Energy Holding Company Limited

-

TBEA Co., Ltd.

-

Tongwei Co., Ltd.

-

Shunfeng International Clean Energy Limited

-

China Sunergy Co., Ltd.

Competitive Landscape of Multi Crystalline Silicon Market

Wacker Chemie AG

Wacker Chemie AG is a Germany-based global leader in specialty chemicals and silicon production, offering high-quality multi crystalline silicon for photovoltaic (PV) and electronic applications. The company operates integrated polysilicon and wafer production facilities, enhancing supply chain efficiency, product consistency, and scalability. Its role in the Multi Crystalline Silicon Market is significant, delivering reliable silicon solutions that support high-performance PV modules and electronics manufacturing.

-

In 2025, Wacker Chemie AG expanded its silicon wafer production capacity, improving throughput and reducing manufacturing costs, enabling more competitive pricing and strengthened market position.

GCL Poly Energy Holdings Limited

GCL Poly, headquartered in China, is a leading solar materials supplier, specializing in polysilicon and multi crystalline silicon wafers. The company supports large-scale PV manufacturers with competitive pricing, high-volume capacity, and integrated supply chains. Its role in the market is central, providing scalable silicon solutions critical for global solar module production and deployment.

-

In 2025, GCL Poly announced the commissioning of new silicon processing lines, increasing wafer output to meet the growing demand in emerging solar markets, reinforcing its position as a key supplier across Asia and international regions.

OCI Company Ltd.

OCI Company Ltd., based in South Korea, produces high-purity silicon materials for multi crystalline applications in solar and industrial sectors. The company emphasizes quality, innovation, and reliability, supplying feedstock to top manufacturers worldwide. Its role in the Multi Crystalline Silicon Market is important, ensuring consistent material performance for PV and electronic applications.

-

In 2025, OCI Company Ltd. implemented improved purification techniques to enhance crystal quality and reduce defect levels, increasing yield efficiency for downstream module and semiconductor production.

REC Silicon ASA

REC Silicon ASA, headquartered in Norway, specializes in advanced silicon materials for PV and electronics markets, emphasizing sustainable production practices. Its portfolio includes multi crystalline silicon optimized for high energy yield, reliability, and consistent performance. The company plays a crucial role in the market by supplying materials that meet growing renewable energy and semiconductor performance demands.

-

In 2025, REC Silicon ASA launched optimized silicon blocks that improved module efficiency, attracting new PV manufacturers and expanding its market presence in both commercial and utility-scale solar installations.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | US$ 2.38 Billion |

| Market Size by 2033 | US$ 4.75 Billion |

| CAGR | CAGR of 9.04 % From 2026 to 2033 |

| Base Year | 2025E |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Solar-grade multi-crystalline silicon, Electronic-grade multi-crystalline silicon) • By Application (Solar / Photovoltaic (PV), Electronics / Semiconductors) • By Production (Block / Ingot Silicon, Wafer Silicon, Cell Silicon, Module Silicon) • By End-User (Residential [home solar installations], Commercial & Industrial [business solar, utility-scale projects]) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Wacker Chemie AG, GCL-Poly Energy Holdings Limited, OCI Company Ltd., REC Silicon ASA, Daqo New Energy Corp., JinkoSolar Holding Co., Ltd., Trina Solar Limited, Canadian Solar Inc., LONGi Green Energy Technology Co., Ltd., JA Solar Technology Co., Ltd., Hanwha Q CELLS Co., Ltd., ReneSola Ltd., SunPower Corporation, First Solar, Inc., Motech Industries Inc., Yingli Green Energy Holding Company Limited, TBEA Co., Ltd., Tongwei Co., Ltd., Shunfeng International Clean Energy Limited, China Sunergy Co., Ltd. |

Frequently Asked Questions

Asia-Pacific dominated the Multi Crystalline Silicon Market in 2025E.

The “Solar-grade multi-crystalline silicon” segment dominated during the projected period.

Rising global demand for solar energy and high-purity silicon in PV and electronic applications drives the Multi Crystalline Silicon Market.

The market was valued at USD 2.38 Billion in 2025E and is projected to reach USD 4.75 Billion by 2033.

The Multi Crystalline Silicon Market is expected to grow at a CAGR of 9.04% during 2026–2033.

Get in Touch