Tire Recycling Market Report Scope & Overview:

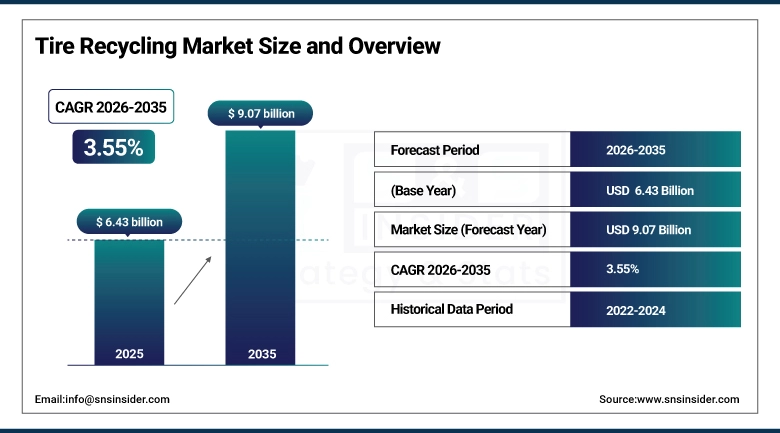

The Tire Recycling Market was valued at USD 6.43 billion in 2025 and is expected to reach USD 9.07 billion by 2035, growing at a CAGR of 3.55% from 2026-2035.

The global automotive fleet generates Over 1 billion end of life tires are generated from the global automotive fleet each year, making it one of the most durable industrial waste streams. Tires are resistant to degradation, making them durable in automobiles but a headache in landfills, where they do not break down, grow mosquitoes and can ignite into toxic infernos. Globally, regulations have grown tougher also raising recycling demand. Rubber granules, carbon black, steel and pyrolysis oil - the raw materials recycled from tires with real commercial value in construction, manufacturing and energy - can make tire recycling commercially viable alongside straightforward market-driven regulatory support.

According to the U.S. Environmental Protection Agency's Scrap Tire Markets report, about 290 million scrap tires are generated annually in the U.S., with 96% entering markets as recycled products — among the highest scrap tire recycling rates for any waste category. Europe attained a 96.1% end-of-life tire recovery rate for 2022, according to data from the European Tyre and Rubber Manufacturers' Association (ETRMA), with energy recovery (TDF) and material recovery (rubber granulates, carbon black, steel) split roughly evenly.

Tire Recycling Market Size and Forecast

-

Market Size in 2025: USD 6.43 Billion

-

Market Size by 2035: USD 9.07 Billion

-

CAGR: 3.55% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Tire Recycling Market - Request Free Sample Report

Tire Recycling Market Trends

-

Tire Pyrolysis Technology Development - employing pyrolysis involving temperature, pressure, and catalysts to break down the rubber from the tires to oil, carbon black, gas, and steel products to such an extent that the rCB obtained can replace the virgin CB in tire manufacturing.

-

Development work on devulcanization technology is making progress to enable the breaking up of the cross-linked structure of tire rubber through devulcanization technology to produce rCB with elastic properties close to those of the virgin CB – the most valuable product of the tire recycling process.

-

Extended Producer Responsibility legislation is gaining momentum to compel tire producers in countries beyond Europe and North America to establish systems for collecting and processing their waste tires after the useful life of the tires ends.

-

Tire-derived crumb rubber for use in road paving asphalt has been shown to increase road durability, reduce noise levels, and prevent rut formation compared to regular asphalt and has been adopted by several states and municipalities.

-

Reclaimed Carbon Black has attracted the attention of tire manufacturers with a commitment to the Circular Economy, including Michelin, Bridgestone, and Continental, who have set targets for using recycled products in tire manufacturing.

-

Ocean-bound tire waste recovery programs are addressing the estimated 4 million tires lost in waterways and ocean environments annually, recovering material for recycling while addressing an environmental impact that conventional scrap tire programs do not reach.

-

Electric vehicle tire recycling is creating new composition challenges as EV tires - which are heavier and wear faster than conventional vehicle tires due to EV weight and instant torque characteristics - generate above-average tire particulate matter and above-average scrap tire volume per vehicle.

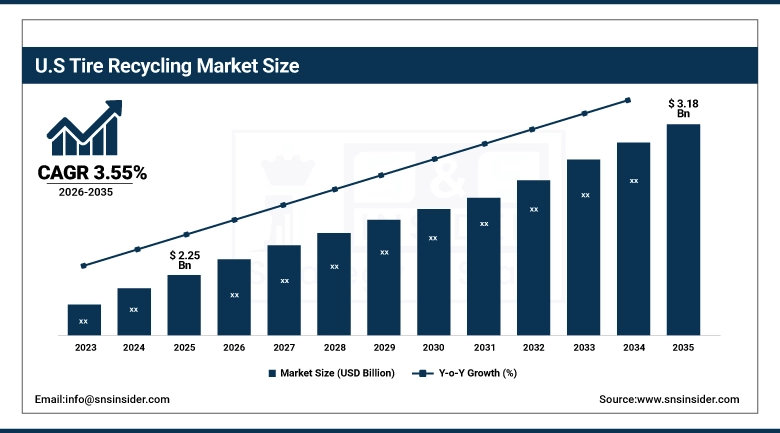

U.S. Tire Recycling Market was valued at USD 2.25 billion in 2025 and is expected to reach USD 3.18 billion by 2035, growing at a CAGR of 3.55% from 2026-2035.

The global Tire Recycling Market is being led by North America, with the U.S. at an advanced stage due to all 50 states having legislation prohibiting the use of whole tires in landfills and many restrictions on shredded tires. Being the biggest automobile market generates the most tons of scrap tires. Collection, processing, and distribution If you go back to the best tire recycling operators Liberty Tire Recycling; EnviroStar Inc. Particularly the U.S. tire-derived fuel (TDF) sector has reached a unique level, with cement kilns and pulp mills burning shredded tires as a high-BTU, cost-competitive and lower-imission replacement for coal

According to data cited in the U.S. Tire Manufacturers Association's 2023 Scrap Tire Report, TDF represented 130 million equivalent tires of scrap tire use - 43% of all scrap tire market volume - with cement kilns (54%) and pulp and paper mills (30%) being the two leading consumers of TDF. The growth in the rubber-recycling industry comes from two factors: a shortage of ingredients for new tires and applications.

Tire Recycling Market Segment Analysis

-

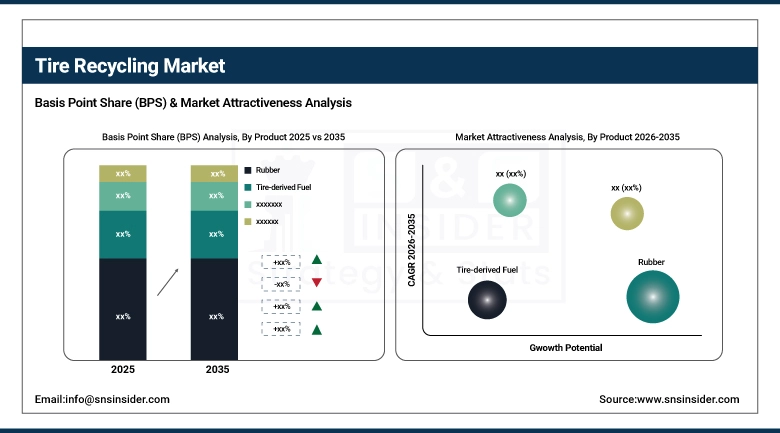

By Product, Rubber dominated with the largest share in 2025; Recovered Carbon Black and Tire-derived Fuel segments are growing steadily

-

By Application, Automotive dominated with the largest share in 2025; Building & Construction

By Product: Rubber Dominates, Recovered Carbon Black Growing Steadily

Rubber, with a revenue share of most in the global tire recycling market (in 2025), especially crumb rubber, granulates and ground rubber powder produced during mechanical processes for recycling tires have been dominating this type of a market as it finds extensive application in products such as playground surfaces, sports fields, rubberized asphalt and flooring systems along with automotive cases or construction products. The segment benefits from an existing recycling infrastructure, consistent and standardized product grades, and increasing demand for sustainable materials in various infrastructure and industrial applications. Tire-Derived Fuel (TDF) also had a considerable share, with shredded tire chips being ever more used for their high-calorific-value as supplementary fuel in cement kilns, pulp & paper mills and industrial boilers which provide both cost savings and waste reduction. Tire-Derived Aggregate (TDA) is continually becoming more popular in the civil engineering applications and drainage because TDA has a light structure and effectively absorbs shock.

Recovered Carbon Black (rCB) is emerging as one of the fastest-growing product segments supported by rising circular economy commitments from tire manufacturers and advancements in pyrolysis technologies. Major tire and rubber producers are increasingly incorporating recycled carbon black into tire compounds and industrial rubber products to reduce dependence on virgin carbon black and lower carbon emissions. Growing investments in sustainable tire recycling infrastructure across Europe and North America, combined with increasing regulatory pressure for waste reduction and material recovery, are accelerating commercial adoption of rCB globally.

By Application: Automotive Dominates, Building & Construction Growing Steadily

Automotive remained the dominant application segment in the tire recycling market in 2025 Owing to recycling tire material for the manufacturing of tires, automotive rubber components, retreading operations, and tire derived fuel applications the largest application segment in the tire recycling market remained automotive in 2025. In the effort to meet fuel economy standards and sustainability goals set by automotive manufacturers, vehicle mats, insulation products, seals/gaskets and underbody coatings are using larger amounts of recycled rubber or recovered materials. Another significant use of tire-derived fuel is to help supply energy for industrial uses associated with automotive and manufacturing supply chains. Increasing global vehicle production and replacement tire demand have fueled robust recycled tire-derived material consumption throughout the automotive space.

Building & Construction is emerging as a steadily growing application area driven by increasing use of crumb rubber and tire-derived aggregate in rubberized asphalt, playground surfaces, flooring systems, drainage layers, insulation materials, and lightweight fill applications. Governments and infrastructure developers are increasingly promoting sustainable construction materials to reduce environmental impact and improve waste management efficiency. Recycled tire materials provide durability, shock absorption, noise reduction, and weather resistance advantages, making them attractive for commercial infrastructure and urban development projects. Growing investments in green building initiatives and circular economy practices are further supporting expansion of recycled tire applications within the construction sector.

Tire Recycling Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

50% |

|

Middle East & Africa |

South Africa |

40% |

|

Latin America |

Brazil |

55% |

North America Tire Recycling Market Insights

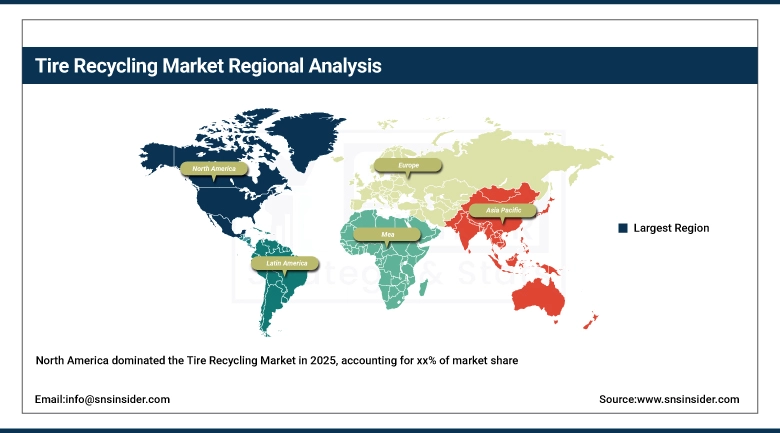

The global Tire Recycling Market was held at a high level 2025, where in North America took the largest revenue share in 2025 owing to the matured regulatory landscape in the U.S., well-established TDF markets cement and pulp industries, and comprehensive crumb rubber end market exists particularly within athletic surfaces and rubberized asphaltover. The Scrap Tire Management Council of the U.S. tracks data that shows some of the world-wide highest scrap tire utilization rates, more than 95 percent of generated scrap tires ultimately reaching beneficial use instead of stockpiling or illegal dump sites signifying decades-long evolution and market infrastructure investments on behalf of state regulators. Tire stewardship tickets in provinces across Canada are able to continuously provide areas for tires to be collected and recycled - creating a consistent flow of processing volume for Canadian recyclers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Tire Recycling Market Insights

Tire Recycling market in Europe owing to established EPR schemes across all EU member states supports the perception of responsible tire producers where tire producer responsibility scheme funded by manufacturer levies enabled systematic collection and processing infrastructure. The traditional tire recycling markets within Europe are Germany, France, the UK, Spain and Italy with well established processing capacity including end-markets for crumb rubber; TDF; and steel wire recovery. Article continues below The European Union's planned End-of-Life Vehicle Regulation -- the first of its kind in the world and one that might set targets for recycled material content in new vehicles -- will create more commercial pull from vehicle supply chains for recovered carbon black and reclaimed rubber from tire recycling. Scandinavian Enviro Systems' commercial-scale pyrolysis operations in Sweden are Europe's first industrial scale rCB production, showcasing the industrial model Europe is beginning to scale behind its circular economy agenda..

Asia Pacific Tire Recycling Market Insights

The Asia Pacific has the highest volume of tire recycling volume in the global and is one of the key regions for other value-added tire recycling technology markets as a result of having the largest scrap tire production, a huge vehicle fleet size in China and increasing amounts of scrap tires generated owing to India's rapidly developing automotive market. The implementation of China's National Solid Waste Management policies has impelled an increasing restriction on the landfill disposal of accumulated scrap tires, thus generating a regulatory pressure to invest in recycling capacity. Japan and South Korea have established tire recycling industries with high recovery rates sustained by efficient EPR systems and developed end markets.

Middle East & Africa and Latin America Tire Recycling Market Insights

The tire recycling market of the Middle East is also maturing, driven by stricter regulations in the Gulf states regarding scrap tire disposal as well as greater demand for sustainable materials from an active construction industry. Tire waste has become a priority category for circular economy treatment in the UAE's zero-waste-to-landfill ambitions - a key part of the country's Net Zero 2050 strategy - with rubberized asphalt pilot programs in Abu Dhabi and Dubai showcasing the construction application that developments such as this create a natural demand for in the region's ever-expanding road network. Brazil dominates the tire recycling market in Latin America, where rules were established for producer responsibility under the National Solid Waste Policy (PNRS), and collection and processing infrastructure has been built up that processes around 90% of Brazil's annual scrap tire generation - among the highest recovery rates in the developing world..

Tire Recycling Market Growth Drivers:

-

Circular economy mandates and sustainable construction demand driving global tire recycling market growth

Regulatory frameworks across the world are gradually closing disposal options for tire waste and increasing reuse of tires. End-market commercial pull from applications in which recycled tire materials create true performance benefits over alternatives contributes to the growth of the market space. Whenever the commodity market for scrap tires falls short of supply/demand equilibrium, regulatory pressure pushes back: landfill bans, EPR fee structures, and producer take-back obligations make sure that whatever the market does this quarter, next quarter putting your used tires in a dumpster cannot be viable. Market growth drivers: the commercial pull of the construction sector is expanding geographic reach and specification depth for applications that are creating demand for recycled tire products as the performance advantages of rubberized asphalt are documented in long-term roadway monitoring data, acceptance of rubber playground surfacing in safety certification, and expanded applications credited with recycled content under new sustainable building material certification programs.

Tire Recycling Market Restraints:

-

Quality consistency challenges and feedstock contamination limiting tire recycling market value creation and product acceptance

The foundational challenge in tire recycling is that the composition of scrap tire feedstock --different formulations from different manufacturers, passenger versus truck versus specialty tires, worn throughs and non-worn tires, variable levels of rim contamination (steel or otherwise) and other types of non-tire rubber material present with contaminated tires-- creates variability of input to output that remains difficult to standardize at a commercially viable scale. Tire-derived fiber (TDF) buyers often require max limits of chlorine content that are sometimes inadvertently exceeded when feedstock streams contain contaminated tire sources; Crumb rubber buyers for athletic surface applications specify very tight particle size distributions and contamination limits that recyclers need to satisfy with consistency across variable feedstock rCB profiles; On the other hand, rCB buyers for tire manufacturing applications seek consistent surface chemistry and impurity profiles that contemporary commercial pyrolysis operations struggle to achieve reproducibly from run to run.

Tire Recycling Market Opportunities:

-

Advanced pyrolysis technology and EV tire volume growth creating significant new tire recycling market opportunities globally

Advanced pyrolysis technology is the most commercially valuable of tire recycling technolgies with process control, catalyst chemistry, and post-processing of recycled carbon black improving continuously over the years to narrow the quality gap between rCB and virgin CB that has restricted rCB to low-value applications. Commercial pyrolysis facilities producing rCB at qualities sufficient to partially substitute in tire compounds (a market opening benchmark that provides more demand than any non-tire application given automotive tire manufacturers' consumption or orders of magnitude larger the carbon black associated with end-of-life vehicles) are operating or under development by companies including: Pyrolyx (now Circtec), Scandinavian Enviro Systems, Enrestec and Delta-Energy Group. That the volume growth of EV tires (and the scrap tire black mat/feedstock generated in service) is uniquely differentiated: lifecycle data shows that, on a per vehicle basis due to comparison between ICE and electric propulsion powertrain, EV tires wear faster than conventional tires (due to vehicle weight and torque characteristics), creating proportionally more scrap tire volume pervehicle than the ICE vehicles replaced, resulting in a recycling feedstock growth rate outpacing overall vehicle electrification metrics.

Recent Developments:

-

2026: Michelin announced commercial deployment of its Sustainera rCB tire compound in its X Multi D truck tire product line, incorporating 10% recovered carbon black from Pyrolyx/Circtec's pyrolysis operations - marking the first commercial-scale tire manufacturer deployment of rCB in a truck tire product, establishing a reference case for rCB quality acceptance in automotive manufacturing that other tire producers are expected to reference in their own circular material procurement evaluations.

-

2025: Liberty Tire Recycling acquired Enviro-Star's U.S. processing operations, creating the largest integrated scrap tire processing network in North America with 100+ collection facilities and 26 processing plants capable of processing 190 million scrap tire equivalents annually - a consolidation that improves collection logistics, feedstock consistency, and end-market supply reliability for crumb rubber and TDF buyers across the U.S.

-

2025: Continental AG and Scandinavian Enviro Systems announced a commercial supply agreement for recovered carbon black for Continental's tire manufacturing operations, with initial volumes of 1,500 metric tons of rCB annually - establishing the first direct supply relationship between a top-5 global tire manufacturer and a commercial pyrolysis rCB producer, signaling that the automotive supply chain is beginning to formalize procurement pathways for pyrolysis-derived circular materials.

Tire Recycling Market Key Players

-

Liberty Tire Recycling LLC

-

Genan Holding A/S

-

Scandinavian Enviro Systems AB

-

Pyrolyx AG (Circtec)

-

ECO Green Equipment LLC

-

Delta-Energy Group

-

Lehigh Technologies Inc. (Michelin)

-

Lakin Tire West Inc.

-

Tire Disposal & Recycling Inc.

-

Western Tire Recyclers

-

Enrestec Inc.

-

Tyre Recycling Solutions SA

-

Enviro-Star Inc.

-

Reclaim Industries Ltd.

-

REDOMA Recycling AB

-

Eldan Recycling A/S

-

TyreTeq AS

-

Black Bear Carbon BV

-

Bolder Industries Inc.

-

Rubber Conversion Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.43 Billion |

| Market Size by 2035 | USD 9.07 Billion |

| CAGR | CAGR of 3.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Rubber, Tire-derived Fuel, Tire-derived Aggregate, Carbon Black, Steel Wires, Others) • By Application (Rubber, Tire-derived Fuel, Tire-derived Aggregate, Carbon Black, Steel Wires, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Liberty Tire Recycling LLC; Genan Holding A/S; Scandinavian Enviro Systems AB; Pyrolyx AG; ECO Green Equipment LLC; Delta-Energy Group; Lehigh Technologies Inc.; Lakin Tire West Inc.; Tire Disposal & Recycling Inc.; Western Tire Recyclers; Enrestec Inc.; Tyre Recycling Solutions SA; Enviro-Star Inc.; Reclaim Industries Ltd.; REDOMA Recycling AB; Eldan Recycling A/S; TyreTeq AS; Black Bear Carbon BV; Bolder Industries Inc.; Rubber Conversion Inc. |

Frequently Asked Questions

North America dominated the Tire Recycling Market in 2025.

Building & Construction dominated the Tire Recycling Market application in 2025.

Rubber (crumb rubber/granulate) dominated with approximately 38% share; Recovered Carbon Black growing fastest.

The Tire Recycling Market was valued at USD 6.43 billion in 2025.

The Tire Recycling Market is expected to grow at a CAGR of 3.55% from 2026 to 2035.

Get in Touch