Next Generation Computing Market Report Scope & Overview:

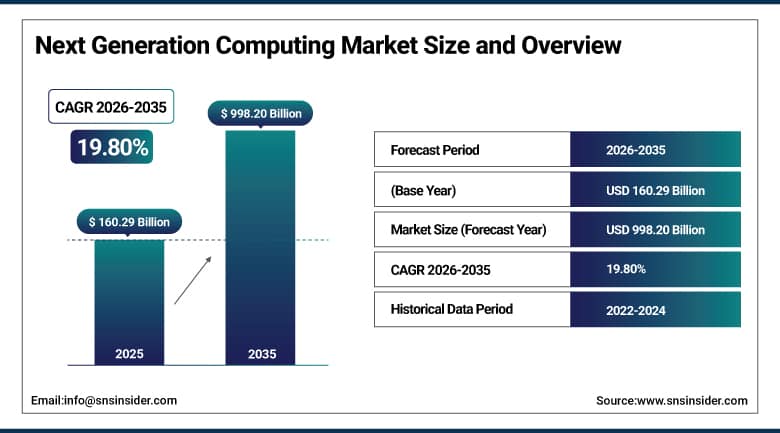

The Next Generation Computing Market was valued at USD 160.29 Billion in 2025 and is expected to reach USD 998.20 Billion by 2035, growing at a CAGR of 19.80% from 2026 to 2035.

The Next Generation Computing Market is experiencing strong growth due to the increased use of artificial intelligence, machine learning, quantum computing, and high-performance computing by different sectors. The growing demand for cloud computing, edge computing, and computing-related applications is leading to greater investment in advanced computing solutions. Increased instances of digital transformation, proliferation of 5G networks, and increased usage of AI-powered analytics are creating greater demand in the market. Moreover, government spending on quantum computing, rising cybersecurity concerns, and the need for fast computing, scalable computing, and energy-efficient computing architecture are helping boost the adoption of next generation computing technology.

UNESCO-designated International Year of Quantum Science and Technology (2025) underscores the rapid advancement of quantum computing research, with global investments in quantum technologies exceeding USD 55.7 billion. Additionally, in 2026, the National Institute of Standards and Technology (NIST) launched the USD 20 million Quantum Manufacturing Engineering Center (QMEC) to accelerate quantum hardware manufacturing and strengthen industry standards, supporting next-generation computing innovation.

Market Size and Forecast

-

Market Size in 2026E: USD 192.03 Billion

-

Market Size by 2035: USD 998.20 Billion

-

CAGR: 19.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Next Generation Computing Market - Request Free Sample Report

Next Generation Computing Market Trends

-

Rising adoption of AI, quantum computing, and high-performance computing technologies driving the evolution of next-generation computing platforms

-

Growing demand for edge computing and distributed processing enabling low-latency data analysis and real-time decision-making across industries

-

Increasing integration of heterogeneous computing architectures combining CPUs, GPUs, NPUs, and specialized accelerators to enhance computational efficiency

-

Expanding investments in cloud-native infrastructure and advanced data centers supporting scalable, secure, and energy-efficient computing environments

-

Continuous advancements in semiconductor technologies, neuromorphic computing, and photonic computing improving processing performance, power efficiency, and scalability

The U.S. Next Generation Computing Market Outlook

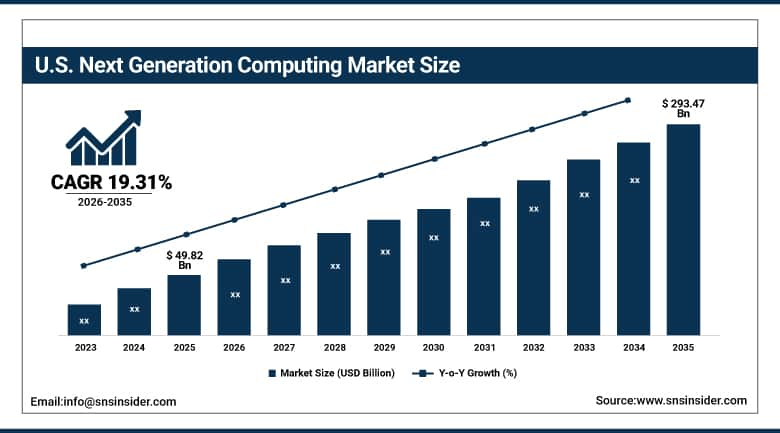

The U.S. Next Generation Computing Market was valued at approximately USD 49.82 Billion in 2025 and is expected to reach approximately USD 293.47 Billion by 2035, growing at a CAGR of approximately 19.31%.

The United States is the world's leading next generation computing market through the concentration of both the most advanced quantum computing technology developers including IBM, Google, IonQ, Rigetti, Quantinuum, and Microsoft and the largest commercial AI and HPC computing infrastructure deployment whose GPU cluster investments by hyperscalers exceed all other national markets. The National Quantum Initiative Act and its successor programmes have provided sustained federal funding whose allocation to university research, national laboratory programmes, and startup ecosystem development has created the deepest quantum computing talent pool and most commercially developed quantum application development ecosystem globally.

Next Generation Computing Market Segment Analysis

-

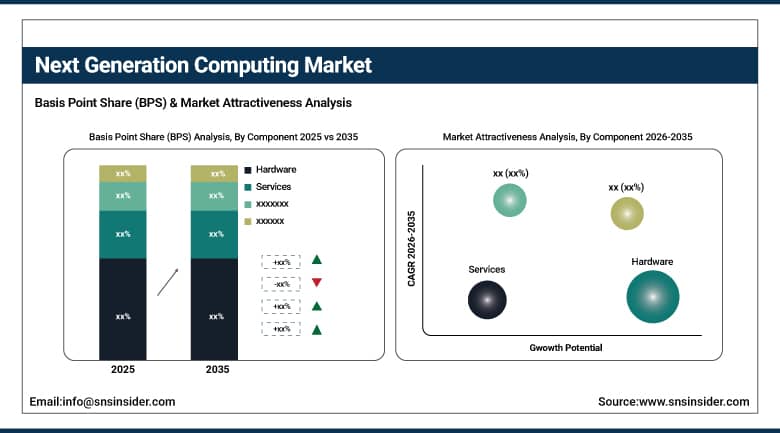

By Component, Hardware segment dominated the Next Generation Computing Market in 2025 with 56% share; Services segment is the fastest growing segment.

-

By Deployment, Cloud segment dominated the Next Generation Computing Market in 2025 with 61% share; Cloud segment is also the fastest growing segment.

-

By Type, Cloud Computing segment dominated the market in 2025 with 37% share; Quantum Computing segment is the fastest growing segment.

-

By Industry, IT & Telecom segment dominated the market in 2025 with 28% share; Healthcare & Life Sciences segment is the fastest growing segment.

By Component, Hardware segment dominates the Next Generation Computing Market, Services segment expected to grow fastest

The Hardware segment dominated the Next Generation Computing Market owing to increasing demand for advanced processors, GPUs, AI accelerators, quantum processors, memory systems, and high-performance networking equipment. All these components help in building up the backbone of the next generation computing infrastructure, which enables fast processing of data, simulation of complex systems, and artificial intelligence. Ongoing investment in semiconductor research, data centers, and edge computing infrastructure has helped in boosting adoption in the hardware segment. Ongoing need for high performance computing helps in boosting the dominant market share of the segment globally.

The Services segment is the fastest growing in the Next Generation Computing Market owing to increasing demands for consulting, integration, deployment, and managed services for advanced computing environments. Enterprises need specific skills for implementing artificial intelligence, quantum computing, cloud native, and high-performance computing. Increased digital transformations, hybrid infrastructure, and complexities of technologies are fueling service demands. Continuous efforts in modernizing enterprises are boosting the growth of the services segment across the world.

By Deployment, Cloud segment dominates the Next Generation Computing Market, Cloud segment expected to grow fastest

The Cloud segment dominated the Next Generation Computing Market and is also the fastest growing deployment model because of its scalability and flexibility as well as ability to offer on-demand access to powerful computing capabilities. Businesses are using cloud technologies to facilitate the use of artificial intelligence, machine learning, big data analytics, edge computing, and high performance computing without having to make any major infrastructure investments. Cloud computing allows for faster application development, global reach, efficient resource usage, and cost savings. Continuous enterprise digitization, rise of hyperscale data centers, hybrid/multi-cloud strategies, and innovations in cloud computing will keep reinforcing its market dominance.

By Type, Cloud Computing segment dominates the Next Generation Computing Market, Quantum Computing segment expected to grow fastest

The Cloud Computing segment dominated the Next Generation Computing Market because of the extensive adoption of scalable computing platforms that facilitate artificial intelligence, analytics, applications development, and digital transformation. With cloud computing, one is able to gain access to advanced computing technologies at relatively low operational costs and with a lot of flexibility. The expansion of cloud computing infrastructure, adoption of software as a service, and adoption of distributed computing systems are some of the factors that make the segment leader. Investments in cloud services continue to sustain its market leadership position.

The Quantum Computing segment is the fastest growing in the Next Generation Computing Market owing to the high speed of technological innovation and investments from governments, research centers, and tech companies. The unique capability of quantum computers to solve very complicated optimization, cryptography, drug discovery, and scientific research problems is the main reason behind such growth. Ongoing improvements in hardware and algorithms together with error correction innovations are driving commercialization of these solutions.

By Industry, IT & Telecom segment dominates the Next Generation Computing Market, Healthcare & Life Sciences segment expected to grow fastest

The IT & Telecom segment dominated the Next Generation Computing Market because of their heavy usage of computing technology to provide cloud services, network optimization, security, artificial intelligence, and big data processing. The fast proliferation of digital services, 5G infrastructure, and hyperscale data centers has led to a rise in demand for high-performance computing systems. Investments in automation, edge computing, and intelligent network management continue to boost usage of the technology, which further enhances the segment’s dominance in the global technology ecosystem.

The Healthcare & Life Sciences segment is the fastest growing in the Next Generation Computing Market because of the rising usage of artificial intelligence, genomics, precision medicines, and biomedical research. The next generation of computing technologies helps in analyzing complex biological information, provides accurate diagnoses and drug development process. Investments in digital health infrastructure and computational research have increased the demand, while the expanding usage of high-performance computing in personalized medicine and decision making drives market growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Next Generation Computing Market Insights

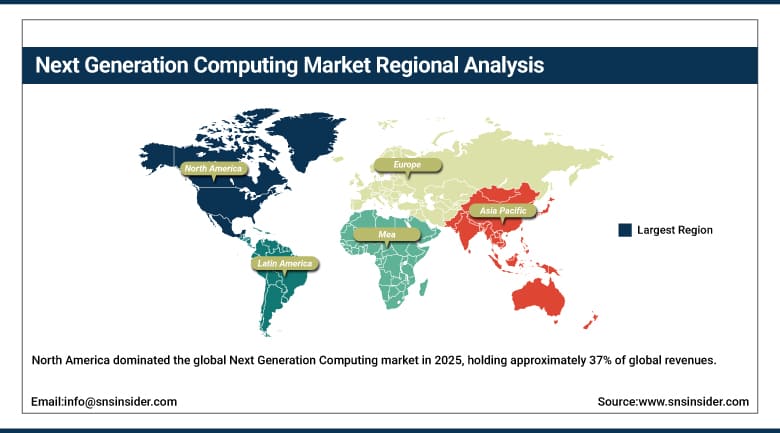

North America dominated the global Next Generation Computing market in 2025, holding approximately 37% of global revenues. The United States accounts for approximately 84.73% of regional revenue through the domestic headquarters of IBM, Google, Microsoft, Intel, NVIDIA, and Amazon whose combined next generation computing R&D investment and commercial deployment scale exceed any other national market's contribution, the most extensive federal government quantum computing and HPC programme investment globally, and the highest concentration of university quantum research excellence at MIT, Caltech, UC Berkeley, and Chicago whose scientific output creates the talent pipeline and intellectual property base for commercial quantum development.

Canada contributes meaningful supplementary North American demand through the University of Waterloo's Perimeter Institute quantum research programme and companies including Xanadu and D-Wave whose quantum computing platforms contribute to North American next generation computing revenue.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Next Generation Computing Market Insights

Europe held approximately 23.84% of global Next Generation Computing revenues in 2025. Germany accounts for approximately 27.84% of European revenues through its Fraunhofer Society's quantum computing and HPC research investment, BMW, Volkswagen, and BASF's enterprise quantum computing exploration programmes, and the domestic presence of Atos SE and Infineon Technologies whose next generation computing products and services serve European market demand.

The EU Quantum Flagship programme, whose EUR 1 billion investment in quantum technologies through 2028 funds quantum hardware development, algorithm research, and standardisation work, is creating European quantum computing capability that supplements U.S. and Chinese commercial quantum leadership. The UK's National Quantum Technology Programme and its investment in quantum photonics, sensing, and communications positions the UK as Europe's leading quantum startup ecosystem.

Asia Pacific Next Generation Computing Market Insights

Asia Pacific is the fastest-growing regional Next Generation Computing market, projected to expand at a CAGR of approximately 22.00% through 2035. China accounts for approximately 38.47% of Asia Pacific revenues through its national quantum computing investment programme targeting leadership in quantum science, its Alibaba Cloud Quantum Development Platform, and the government's Made in China 2025 semiconductor and advanced computing strategic initiatives whose funding sustains both quantum hardware development and HPC infrastructure deployment.

Japan's Society 5.0 framework and its quantum computing investment through the JST and MEXT research programmes contribute precision quantum hardware development. South Korea, India, Singapore, and Australia each contribute growing Asia Pacific next generation computing demand through their national quantum and HPC strategic investment programmes.

MEA & Latin America Next Generation Computing Market Insights

Middle East and Latin America are growing Next Generation Computing markets where government digital transformation investment and enterprise AI adoption are creating expanding HPC and early quantum computing demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its G42 AI and computing investment programme, its smart government infrastructure requiring HPC capabilities, and the UAE's national quantum computing roadmap whose institutional investment positions the country as the Middle East's leading next generation computing adopter.

Saudi Arabia's Smart Saudi digital transformation programme and NEOM's computing infrastructure investment contribute growing MEA HPC demand. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its academic and research HPC infrastructure, financial services sector AI computing investment, and growing quantum computing awareness in research institutions.

Market Dynamics

Growth Drivers: Frontier AI training demand and advancing quantum computing commercialization accelerate next-generation computing infrastructure investments globally.

Frontier AI training compute demand has created a step-function increase in HPC infrastructure procurement defined by hyperscaler capex commitments. Amazon, Microsoft, Google, and Meta each announced 2025 capital expenditure plans exceeding USD 60 billion directed primarily toward AI computing infrastructure, creating a positive feedback loop where AI value justifies further investment requiring more HPC infrastructure. Quantum computing's approaching commercial advantage threshold in simulation, optimisation, and sampling is driving enterprise preparation investment in quantum software development, hybrid algorithm development, and quantum cloud access that sustains early-stage revenue growth.

Restraints: Quantum error rates, decoherence limitations, and skilled talent shortages restrict enterprise quantum computing adoption.

Current-generation quantum processors, including IBM's 127 to 1,000 qubit processors and Google's Willow chip, achieve physical qubit error rates that require tens to hundreds of physical qubits per logical qubit for error correction, reducing the effective logical qubit count available for algorithm execution to levels that constrain practical quantum advantage to narrow problem domains.

The dilution refrigerator operating requirements of superconducting quantum processors, which must be cooled to millikelvin temperatures near absolute zero, impose infrastructure constraints that limit quantum computer deployment to specialised facilities and make direct enterprise-premises quantum deployment impractical, sustaining cloud-based quantum access as the primary commercial delivery model. The global shortage of quantum computing professionals with the combined physics, computer science, and domain knowledge required to develop practically useful quantum algorithms creates a talent supply bottleneck that limits the velocity of enterprise quantum application development even when cloud quantum computing access is commercially available.

Opportunities: Post-quantum cryptography and neuromorphic edge AI create high-value next-generation computing market expansion.

NIST's 2024 finalisation of post-quantum cryptographic algorithms CRYSTALS-Kyber and CRYSTALS-Dilithium has created a defined migration target for enterprise cryptographic infrastructure. Post-quantum migration encompasses every encrypted communication protocol, certificate authority, VPN tunnel, and secure storage system, creating a multi-year enterprise security infrastructure replacement cycle whose computing hardware, software, and services constitute a transformative next generation computing opportunity. Neuromorphic computing's energy efficiency in always-on edge pattern recognition creates commercial opportunities in IoT sensor intelligence, smart city monitoring, and consumer device ambient AI where battery and thermal constraints make GPU inference architecturally incompatible.

Recent Developments:

-

2025: IBM expanded its Quantum Network to over 400 client organisations globally with over 600,000 registered quantum computing learners on its platform, and Google's Willow quantum chip demonstrated error reduction scaling with qubit count, providing the first experimental evidence consistent with fault-tolerant quantum computation.

-

2025: Cisco unveiled a prototype quantum networking chip and established a quantum computing laboratory in Santa Monica targeting quantum-safe communications protocols, and SeeQC announced a modular quantum computing architecture combining classical and quantum chipsets for low-latency real-time processing targeting financial and cybersecurity applications.

-

2025: Microsoft announced progress on its topological qubit approach using Majorana-based hardware for inherently error-protected quantum operation, representing a fundamentally different path toward fault-tolerant quantum computing whose realisation could enable practical quantum advantage without the error correction overhead constraining current probabilistic qubit architectures.

Next Generation Computing Market Key Players are:

-

IBM Corporation

-

Microsoft Corporation

-

Google LLC

-

Intel Corporation

-

NVIDIA Corporation

-

Advanced Micro Devices, Inc. (AMD)

-

Amazon Web Services (AWS)

-

Oracle Corporation

-

Hewlett Packard Enterprise (HPE)

-

Dell Technologies Inc.

-

Fujitsu Limited

-

NEC Corporation

-

Atos SE

-

Rigetti Computing, Inc.

-

IonQ, Inc.

-

D-Wave Quantum Inc.

-

Quantinuum

-

PsiQuantum Corporation

-

Cerebras Systems Inc.

-

Graphcore Limited

Next Generation Computing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 160.29 Billion |

| Market Size by 2035 | USD 998.20 Billion |

| CAGR | CAGR of 19.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Deployment (On-premise, Cloud) • By Type (Quantum Computing, Edge Computing, High-Performance Computing (HPC), Cloud Computing, Others) • By Industry (Healthcare and Life Sciences, BFSI, IT & Telecom, Government, Energy & Utilities, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Microsoft Corporation, Google LLC, Intel Corporation, NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Amazon Web Services (AWS), Oracle Corporation, Hewlett Packard Enterprise (HPE), Dell Technologies Inc., Fujitsu Limited, NEC Corporation, Atos SE, Rigetti Computing, Inc., IonQ, Inc., D-Wave Quantum Inc., Quantinuum, PsiQuantum Corporation, Cerebras Systems Inc., Graphcore Limited |

Frequently Asked Questions

North America dominated the Next Generation Computing Market in 2025.

The Next Generation Computing Market is expected to grow at a CAGR of 19.80% from 2026 to 2035.

The Next Generation Computing Market was valued at USD 160.29 Billion in 2025.

The high-performance computing (HPC) segment dominated the Next Generation Computing Market.

Frontier AI, quantum computing, post-quantum cryptography, neuromorphic AI, and government investments are driving Next Generation Computing Market growth globally.

Get in Touch