Orthodontic Supplies Market Size & Trends:

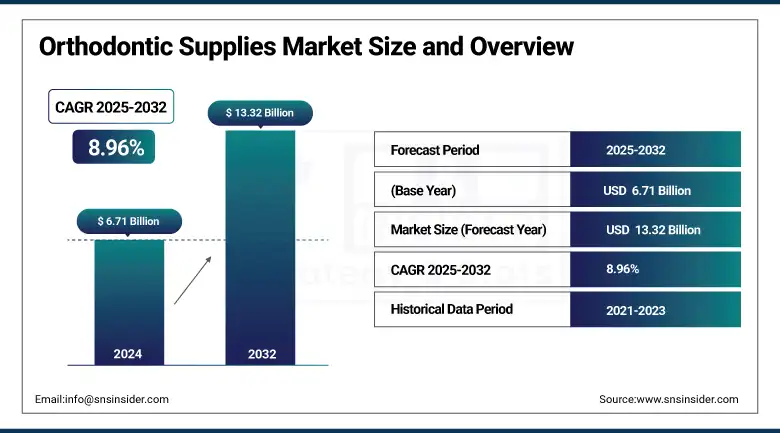

The Orthodontic Supplies Market size was USD 6.71 billion in 2024 and is expected to reach USD 13.32 billion by 2032, growing at a CAGR of 8.96% over 2025-2032.

The global orthodontic supplies market is experiencing demand growth with an increasing prevalence of malocclusion, a surge in the number of dental cosmetic procedures, and growing awareness of oral health globally. The market for fixed braces, removable aligners, and supporting materials is growing, fueled by the boom in teen and adult orthodontics, particularly in the US, China, and parts of Eastern Europe. Rising middle-class integration and per capita dental expenditure will contribute to a robust global orthodontic supplies market expansion in developing countries.

To Get more information On Orthodontic Supplies Market - Request Free Sample Report

Orthodontic Supplies Market Size and Forecast:

-

Market Size in 2024: USD 6.71 billion

-

Market Size by 2032: USD 13.32 billion

-

CAGR: 8.96% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

In May 2024, Align Technology revealed a broader AI-driven platform for virtual orthodontic treatment, improving treatment planning and aligner personalization.

The orthodontic supplies market trends are being transformed by technological innovations such as AI-based treatment planning and 3D-printed aligners, which have made the development of orthodontic solutions quicker and more accurate. Furthermore, rising R&D investment by leading orthodontic supplies manufacturers, including 3M, Align Technology, Dentistry Sirona, also promotes product innovation. The launch of products is being expedited by regulatory nods, such as that of FDA clearance in case of next-gen clear aligners and a CE-marked for self-ligating brackets. Rising investments in dental clinics and digital orthodontics infrastructure, particularly in Asia-Pacific and Latin America, are further fueling supply chain growth and strengthening the presence of products, pushing the orthodontic supplies market trends competition.

For instance, Dentsply Sirona put up USD 80 million for a new R&D center specializing in digital orthodontics and materials science with the intention of establishing long-term orthodontic supplies market analysis through breakthrough innovations.

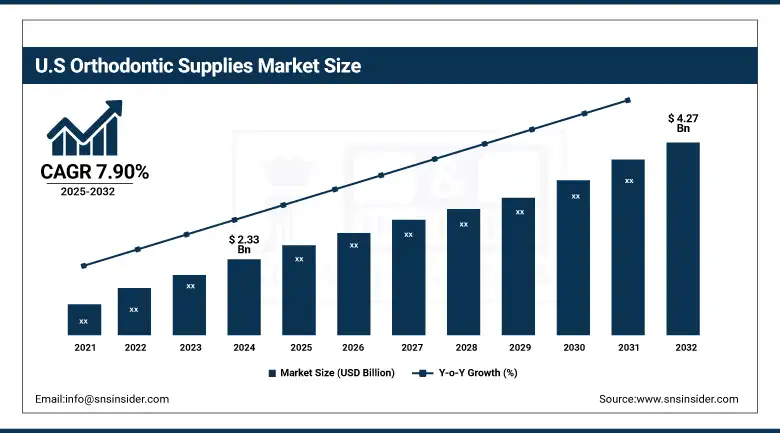

The U.S. orthodontic supplies market size was USD 2.33 billion in 2024 and is expected to reach USD 4.27 billion by 2032, growing at a CAGR of 7.90% over 2025-2032. The US dominated the region with wider acceptance of digital orthodontics, and the presence of an established DSO network support. The U.S. orthodontics market addresses approximately 4 million Americans each year, with robust increases in adult aligner users. Positive insurance policies as well as legislative assistance (e.g., FDA approvals for clear aligners and bonding agents) also contribute to market penetration. Close behind is Canada, which has seen rising levels of government support for oral health initiatives. Mexico sees moderate growth while private clinics expand scale and pricing power. The U.S. is also a centre of some of the leading orthodontic supplies companies and innovation, catapulting the regional market share.

Orthodontic Supplies Market Trends:

-

Rising demand for aesthetic dentistry, including clear aligners and ceramic braces, is significantly driving the growth of the orthodontic supplies market globally.

-

Increasing prevalence of malocclusion and dental irregularities among both children and adults is boosting the need for orthodontic treatments and related products.

-

Technological advancements such as 3D printing, digital scanning, and CAD/CAM systems are improving the precision and customization of orthodontic devices.

-

Growing awareness about oral health and the importance of early orthodontic intervention is encouraging more patients to seek treatment.

-

Expansion of dental clinics and orthodontic practices, particularly in emerging markets, is enhancing accessibility to orthodontic care and supplies.

-

Rising adoption of minimally invasive and comfortable treatment options, including self-ligating braces and invisible aligners, is shaping market demand.

-

Strategic collaborations, product innovations, and increasing investments by key market players are accelerating the development of advanced orthodontic solutions.

Table: Regulatory Milestones & Approvals (2023–2025)

|

Region |

Authority |

Product |

Company |

Approval Date |

Significance |

|

China |

NMPA |

Palatal Expander |

Align Technology |

May-25 |

First 3D-printed appliance approved |

|

EU |

EMA/CE |

Ceramic Brackets |

JJOrtho |

Dec-24 |

Entry into the European market |

|

Brazil |

ANVISA |

Clear Aligners |

Aditek Orthodontics |

Jun-23 |

National commercial access |

|

India |

CDSCO |

Orthodontic Bonding Agents |

Modern Ortho |

Jan-25 |

Regulatory pathway streamlined |

Orthodontic Supplies Market Dynamics

Drivers:

-

Technological Advancements and Growing Aesthetic Dental Awareness Are Propelling the Orthodontic Supplies Market

The global orthodontic supplies market is experiencing growth due to rising technological advancements, the demand for aesthetic dentistry among the growing populace, and increased dental knowledge among different age groups. Increasing preference for personalized treatments, including 3D printed aligners and AI-based treatment planning solutions, is shaping the future of the market.

For instance, SmileDirectClub and uLab Systems are creating new treatment delivery models for same-day aligner fabrication and individualized modification. Investment in dental infrastructure, including private chains and dental service organizations (DSOs), is opening up access to extensive orthodontic care.

R&D spending is also increasing in 2023, an investment of a sizeable part of the USD 2.5 billion annual budget of Ormco (a division of Envista) in R&D has been assigned for SLBs and bonding systems. Meanwhile, positive regulatory support, including the FDA’s Simplified 510(k) process for digital orthodontic devices and CE Mark certification for self-ligating systems, speeds the introduction of products. Increasing inclination of adults and teens towards confidential treatment solutions, along with expanding insurance coverage, will further enhance the orthodontic supplies market share over the forecast years to come.

Restraints:

-

High Treatment Costs and A Lack of Access to Specialized Care Are Limiting Broader Market Penetration

The global orthodontic supplies market, although new and growing, is limited by some significant barriers. Orthodontic treatment is expensive, with traditional braces, which range between USD 3,000 and USD 7,000, and clear aligners, which can cost up to USD 8,000, pricing many cash and underinsured consumers out of the market. Furthermore, most countries have minimal reimbursement for orthodontics, which limits use. Limited supply by a low supply of orthodontists in low-income and rural areas makes it difficult to achieve it, despite an increasing demand.

More than 50% of the global population does not have access to essential oral health care, as estimated by the World Health Organization, an important aspect influencing the orthodontic supplies market research. The complicated regulatory procedures for device approvals, such as in Japan and Brazil, are bottlenecks to the arrival of new products. Moreover, smaller orthodontic supplies companies are often challenged by constraints on capital, and they are not able to dedicate funding to R&D and comply with changing regulations. These impediments delay the availability of economical and 21st-century options, which consequently reduces the number of consumers and curtails the prevalence of new orthodontic supplies market trends.

Orthodontic Supplies Market Segmentation Analysis

By Product

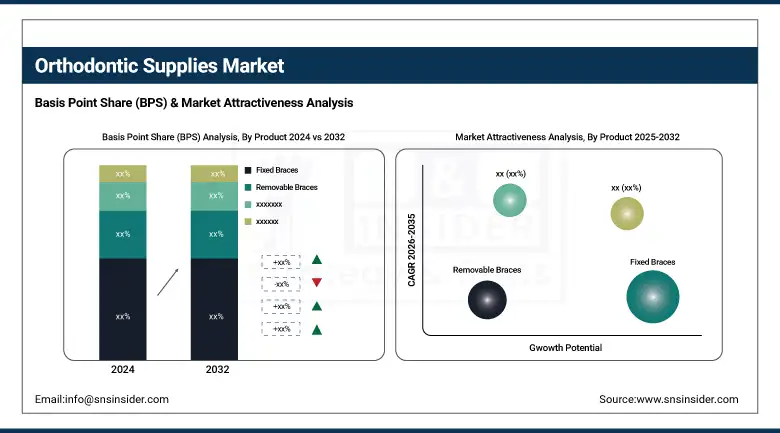

Fixed braces held a leading share in the orthodontic supplies market by product in 2024, with over 45% share of the market share as it is used as a standard option for the treatment of complex malocclusion due to their clinical effectiveness and cost-effective pricing as compared to other emerging alternatives. Nevertheless, removable braces (notably clear aligners) are the most rapidly growing product category because of rising patient demand for the aesthetic and convenient nature of these systems. Their portability, trend of use among working professionals and teenage population, and unnoticeable appearance have driven demand through clinical and home-based treatment.

Table: Product Innovation Pipeline by Key Companies (2023–2025)

|

Company |

Product/Technology |

Type |

Launch Stage |

Key Feature |

Target Segment |

|

Align Technology |

Invisalign Palatal Expander |

Removable Appliance |

Commercialized (2025) |

3D Printed, NMPA Approved |

Pediatric |

|

Envista (Ormco) |

Damon Ultima SL Brackets |

Fixed Braces |

Launched (2024) |

Torque control, low friction |

Teen/Adult |

|

JJOrtho |

Ceramic Bracket Series |

Fixed Braces |

Prototype |

Aesthetic, Heat-resistant |

Adults |

|

Ultradent |

Adhesive System X |

Adhesives |

Beta Testing |

Light-curing, Enhanced bond strength |

All ages |

|

Sino Ortho |

AlignPro Clear Aligners |

Removable Braces |

Regional Rollout (China) |

Budget aligners |

Cost-sensiti |

By Patient

In terms of patient type, children & teenagers accounted for the highest share, constituting about 60% market share in 2024, as the diagnosis for dental misalignment is high in the early years, and parents are investing more in orthodontic technology. Adults are the fastest-growing segment, as more people decide they would like their teeth to be more attractive or more functional later on in life, often with the help of invisible options, such as aligners.

By Distribution Channel

Wholesalers and distributors were the market leaders in available orthodontic supplies in 2024, holding 56.2% share of the market. This is thanks to their pre-existing relationship with dental facilities, efficient logistics, and experience in bulk purchase management. They help in creating an efficient distribution channel to bridge the gap between the demand and the supply of essential products, especially fixed braces and their related products, in the urban and semi-urban markets. At the same time, e-commerce became the fastest-growing segment as consumers turned to e-retail like never before. Any additional movement towards direct-to-consumer orthodontic models, coupled with increasing desire for convenience, particularly in the aligners and orthodontic accessory segment, is boosting online platform sales, especially in North America, Europe, and parts of Asia.

By End User

DSOs (Dental Service Organizations) and private clinics dominated the orthodontic supplies market in 2024, contributing to over 48% of the market share. Their superiority is due to high patient volumes, continuous investment in digital scanning and AI software tools for treatment, and quicker adoption of new orthodontic supplies and procedures. These environments also provide a more individualized patient experience, resulting in high levels of treatment adherence. Meanwhile, dental hospitals are observing the most rapid growth on the back of the increased investment in public dental infrastructure by governments and educational institutes. Improved orthodontic departments and subsidized care at public hospitals are working to increase access to orthodontic services, especially in developing nations.

Orthodontic Supplies Market Regional Insights

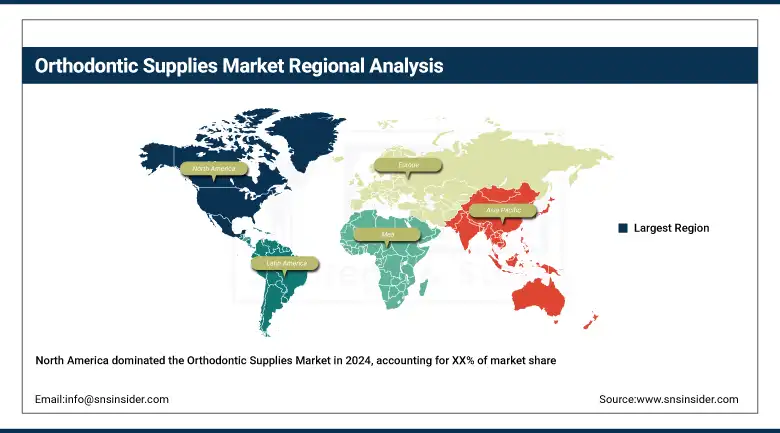

In 2024, North America was leading the orthodontic supplies market, owing to high orthodontic treatment prevalence, developed dental infrastructure, and high disposable income.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second fastest-growing region in the orthodontic supplies market, driven by Germany, the UK, and France. The market is favored by the high prevalence of cosmetic dentistry, the launch of government-sponsored oral healthcare programs, and the presence of leading dental product manufacturers.

Germany leads the region on account of a high concentration of orthodontic practitioners, supporting reimbursement policies, and early adoption of 3D dental technology. Poland and Turkey are expanding at a rapid pace, attributed to dental tourism and high-quality orthodontic offerings at competitive prices. Italy and Spain are on a fast pace for the growth of riding demand for adult orthodontics and public-private partnerships. High demand for aligners and self-ligating braces is being witnessed in the urban centers among working professionals.

Asia Pacific is the fastest-growing region in the orthodontic supplies market, which can be attributed to the expanding middle-class population, rising awareness about oral health, and increasing urbanization in the region.

China dominates the market in terms of percentage, as it is the most populous nation, and its dental aesthetics consciousness is on the rise and as the spread of numerous local players providing affordable services. The government’s drive towards online healthcare services integration and insurance reforms further underpins demand. India comes next, driven by robust expansion in dental clinic chains, low-cost private orthodontic treatments, and a booming call from younger people. Further, high health standards and the early acceptance of clear aligners and other orthodontic approaches have made Japan and South Korea the other major orthodontic supplies market growth centers. In addition, the growth in medical tourism in countries such as Singapore and Australia also contributes to regional growth momentum.

Table: Digital Adoption in Orthodontic Practices by Country (2024 Survey)

|

Country |

% of Clinics Using Digital Impressions |

AI-Based Treatment Planning Use |

Popular Digital Tool |

|

US |

78% |

65% |

iTero, Invisalign ClinCheck |

|

Germany |

70% |

52% |

3Shape TRIOS |

|

India |

48% |

41% |

Carestream Dental CS 3600 |

|

Brazil |

55% |

46% |

Easy Smile Digital |

|

Japan |

62% |

49% |

Ray Medical Imagin |

Key Players in the Orthodontic Supplies Market:

Notable orthodontic supplies companies in the market include Solventum Corporation, TP Orthodontics, Inc., Great Lakes Dental Technologies, DB Orthodontics Limited, Aditek Orthodontics, JJ ortho, Modern Orthodontics, Sino Ortho Limited, Astar Orthodontics Inc., and Ortho Caps GmbH.

Recent Developments in the Orthodontic Supplies Market:

-

In May 2025, Align Technology’s Invisalign Palatal Expander System, its first direct 3D‑printed orthodontic appliance, received NMPA approval in China, enabling both skeletal and dental arch expansion for growing patients. This groundbreaking digital orthodontic solution strengthens Align’s presence in the Asian market.

-

In April 2025, Align unveiled an advanced Invisalign system for Class II correction in 10–16-year-olds featuring integrated occlusal blocks that support lower‑jaw advancement. This innovation combines skeletal correction and teeth alignment in a single appliance, streamlining treatment for younger patients.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 6.71 billion |

| Market Size by 2032 | USD 13.32 billion |

| CAGR | CAGR of 8.96% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Removable Braces, Fixed Braces (Brackets, Archwires, Anchorage Appliances, and Ligatures), Adhesives, and Accessories) • By Patient (Adults, Children, and Teenagers) • By Distribution Channel (E-commerce Platforms, Wholesalers, and Distributors) • By End User (Dental Hospitals, DSOS & Private Clinics, and Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Solventum Corporation, TP Orthodontics, Inc., Great Lakes Dental Technologies, DB Orthodontics Limited, Aditek Orthodontics, JJ ortho, Modern Orthodontics, Sino Ortho Limited, Astar Orthodontics Inc., and Ortho Caps GmbH. |

Frequently Asked Questions

Ans: North America dominated the Orthodontic Supplies market.

Ans: The orthodontic supplies market, although new and growing, is limited by some significant barriers. Orthodontic treatment is expensive, with traditional braces, which range between USD 3,000 and USD 7,000, and clear aligners, which can cost up to USD 8,000, pricing many cash and underinsured consumers out of the market.

Ans: The orthodontic supplies market is experiencing growth due to rising technological advancements, the demand for aesthetic dentistry among the growing populace, and increased dental knowledge among different age groups.

Ans: The market is expected to reach USD 13.32 billion by 2032, increasing from USD 6.71 billion in 2024.

Ans: The Orthodontic Supplies market is anticipated to grow at a CAGR of 8.96% from 2025 to 2032.

Get in Touch