Genetic Testing Market Report Scope & Overview:

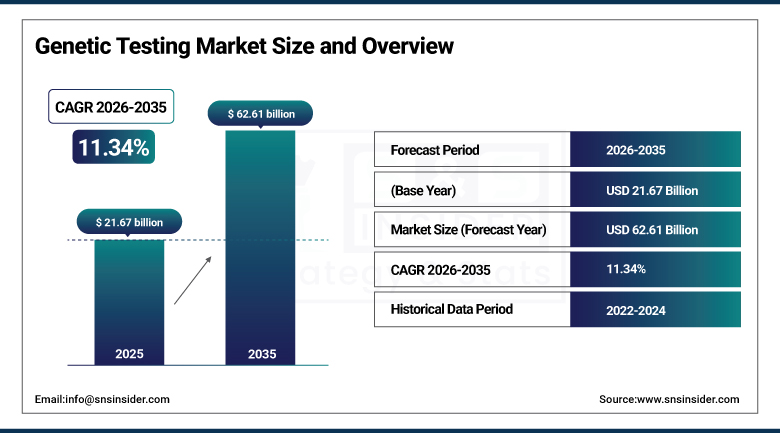

The Genetic Testing Market was valued at USD 21.67 billion in 2025 and is expected to reach USD 62.61 billion by 2035, growing at a CAGR of 11.34% from 2026-2035.

The Genetic testing Market has reached a tipping point that redefines what it means to know more about your health. A whole genome sequence used to cost thousands of dollars and take weeks five years ago. This is the story of how a capability that was once limited to only a handful of top tier research hospitals is now being made available to, on the consumer side, individual consumers and, from a community clinic and oncology practice perspective, community oncology practices in every major city. And this wide increase in accessibility is wrestling its way into every part of the market at once: more carrier screening before families are started, more genomic tumour profiling for cancer patients before treatment decisions, more ancestry and health risk tests ordered directly online. All of those use cases indicate an individual commercial opportunity, and they are growing parallel to one another in a market that has not yet had a peak.

Around 10 million people die of cancer in 2023 according to the WHO, with genetic mutations having a large role in the onset and progression of disease. Genetic disorders are diseases caused by abnormalities in an individual's genome, which impacts millions across the world. With over 6,000 known genetic disorders, early and accurate genetic screening and diagnosis hold immense medical and commercial value.

Genetic Testing Market Size and Forecast

-

Market Size in 2025: USD 21.67 Billion

-

Market Size by 2035: USD 62.61 Billion

-

CAGR: 11.34% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Genetic Testing Market - Request Free Sample Report

Genetic Testing Market Trends

-

Whole genome and whole exome sequencing adoption in clinical settings is expanding beyond rare disease diagnosis into oncology, pharmacogenomics, and preventive health applications as costs decline toward consumer-accessible levels.

-

Liquid biopsy genetic testing detecting circulating tumour DNA from blood samples is advancing toward routine clinical use for cancer detection, treatment monitoring, and minimal residual disease assessment.

-

Polygenic risk score (PRS) adoption is growing as a clinical tool for quantifying individual disease susceptibility across complex conditions including cardiovascular disease, diabetes, and common cancers.

-

AI-powered genomic interpretation platforms are reducing the time and specialist expertise required to translate raw genetic data into actionable clinical recommendations, democratizing genetic insights.

-

Pharmacogenomic testing matching drug prescriptions to individual genetic metabolism profiles is gaining traction in psychiatry, cardiology, and oncology as payer coverage expands for validated gene-drug interactions.

-

CRISPR-based diagnostic applications are entering clinical evaluation for rapid pathogen identification and somatic mutation detection, building on the molecular biology infrastructure created by genetic testing adoption.

-

Direct-to-consumer genetic testing platforms are expanding their health risk and wellness offering beyond ancestry toward clinically validated disease predisposition panels, blurring the consumer-clinical boundary.

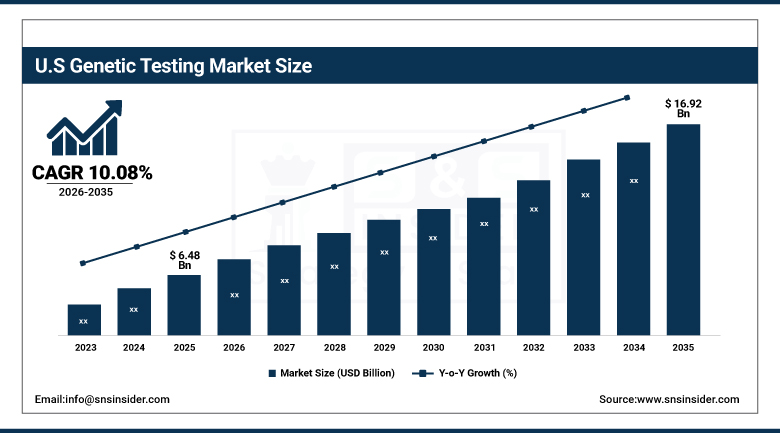

The U.S. Genetic Testing Market was valued at USD 6.48 billion in 2025 and is expected to reach USD 16.92 billion by 2035, growing at a CAGR of 10.08% from 2026–2035.

The United States constitutes the biggest global market for genetic testing and arguably fuses the most active FDA device clearance pathway (e.g., genetic diagnostics), the highest density of oncology centers that deploy genomic tumour profiling, the highest commercially developed direct-to-consumer genetic testing sector in the world, and the National Institutes of Health and other funders actively investing in genomic medicine research architecture. The U.S. is host to competition as several companies including Illumina, Myriad Genetics, Invitae, Natera, Foundation Medicine, and Guardant Health are based here and offer competing clinical as well as consumer genetic testing applications. The evolving regulatory environment in which the FDA governs genetic testing, as well as the agency's rapidly changing stance regarding laboratory-developed tests, companion diagnostics, and direct-to-consumer tests, is directly reflective of each of these companies' product pipelines with enormous implications for ongoing commercial development.

The national genomic database enrolling more than 1 million participants, funded by the NIH's All of Us Research Program is the research infrastructure that undergirds next-generation genetic test development. Nexus for Genomic Testing: The Centre for Medicare & Medicaid Services (CMS) supports NGS-based testing for Medicare beneficiaries with advanced cancer, establishing reimbursement certainty and fuelling the rapid spread of oncogenomics across U.S. oncology practices.

Genetic Testing Market Segment Analysis

-

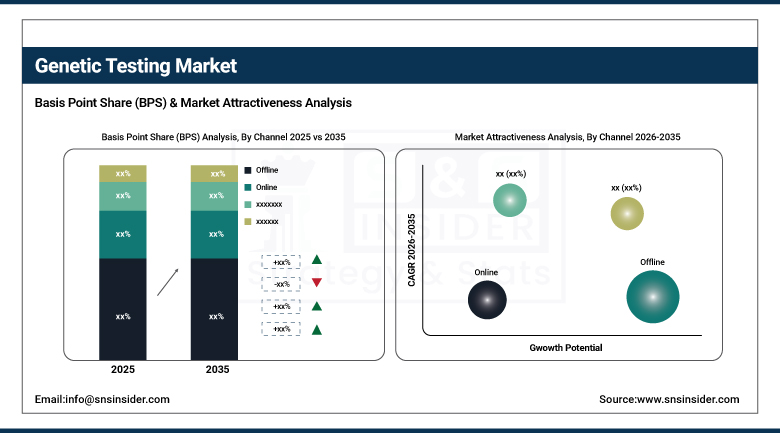

By Channel, Offline segment dominated with 60.32% share in 2025; Online fastest growing (CAGR 12.07%).

-

By Technology, Next Generation Sequencing (NGS) dominated with 49.15% share in 2025; Array Technology and PCR-based growing.

-

By Product, Consumables segment dominated the market; Equipment and Software & Services growing steadily.

-

By Application, Health & Wellness – Predisposition/Risk segment dominated with 51.23% share in 2025; Genetic Disease Carrier Status fastest growing.

-

By End Use, Hospitals & Clinics dominated the Genetic Testing Market in 2025; Diagnostic Laboratories growing steadily.

By Channel, Offline segment dominates the Genetic Testing Market, Online segment expected to grow fastest

In 2025, the Offline channel segment contributed approximately 60.32% to the revenue of the Genetic Testing Market for the same year, due to the strong presence of hospitals and diagnostic laboratories as well as specialized genetic testing centres for clinical use that involves on-site specimen collection, physician supervision and/or regulatory-compliant laboratory processing. This reliance on data is exacerbated by the finite number of category application, with a significant portion of genetic tests for prenatal screening, hereditary disease detection, and oncology diagnosis highest revenue application categories — as they predominantly flow through offline clinical channels, which more or less require a physician to ensure that the right test is selected, that adequate sample quality is assured, and that results are interpreted properly. Both healthcare professionals and payers preferentially guide complex and high-risk genetic testing through established clinical infrastructure, and the reliability, credibility and medico-legal position of offline diagnostic services sustain their market position.

Among them, Online channels are expected to witness the fastest growth at approximately 12.07% CAGR during the forecast period, owing to the increasing availability and convenience of direct-to-consumer genetic testing. Home testing kits, which allow for the collection of a saliva sample and provide a secure digital platform for the delivery of online results of the analysis, provide genetic testing to a segment of the population that would perhaps never set foot in a clinical facility to learn information about their discretionary health status. Telehealth and online genetic counselling is also being introduced on a bigger scale, making the prospects of online channels even more enticing: once again, consumers can more easily interpret their results with a professional without stepping into a clinical visit.

By Technology, NGS segment dominates the Genetic Testing Market, Array Technology and PCR-based growing steadily

More than half of the technology share in the Genetic Testing Market in 2025 was held by Next-Generation Sequencing amounting to an approximate value of 49.15%. The unique ability to perform high-throughput, accurate and cost-effective genetic analysis across a diverse set of applications cancer diagnosis, hereditary disease testing, pharmacogenomics, non-invasive prenatal testing NGS is the technology of choice for clinical and research applications alike. Specifics: Whole-genome and targeted panel sequencing is faster, cheaper, and more accessible than any previous generation from Illumina's NovaSeq X series and Thermo Fisher's Ion Torrent platform. Each of these applications has helped shape the segment to dominate the market, with NGS being the preferred choice for non-invasive prenatal testing, expanded carrier screening, and comprehensive genomic profiling for cancer treatment selection.

Prominent players include Array Technology and PCR-based testing, providing strong market positions as established, validated platforms of broad clinical relevance in specified applications. While array-based tests fulfil the scalability value proposition for high volume applications such as SNP genotyping for direct-to-consumer health and ancestry platforms, PCR-based testing remains the gold standard for rapid molecular diagnostics for infectious disease, and pharmacogenomic single-gene testing, where turn-around time and low cost are value drivers out-weighing the need for complete sequencing coverage. Because FISH preserves clinical applicability for cytogenetic applications, particularly for haematological malignancy diagnosis where alteration of chromosomes into spectrally-distinct whole-chromosome paint-like FISH probes provides information that sequence-based methods cannot directly capture.

By Application, Health & Wellness segment dominates the Genetic Testing Market, Genetic Disease Carrier Status expected to grow fastest

The Health and Wellness predisposition/risk/tendency segment dominated the market and accounted for 51.23% of the overall market in 2025, showing the tremendous consumer demand for personalized health intelligence that has been transformed into a very large and rapidly expanding commercial market by genetic testing companies. Tests evaluating personal risks for cardiovascular diseases, diabetes, neurodegenerative disorders and cancer predisposition give consumers the genetic risk information they can use to make informed lifestyle and healthcare decisions. The immense subscriber bases of companies such as 23andMe, AncestryDNA, and MyHeritage have been built around this value proposition and improved polygenic risk scores have enhanced the predictive accuracy to levels of growing clinical interest.

Based on application, the Genetic Disease Carrier Status segment is expected to grow up to highest application CAGR during the forecast period due to the growing adoption of expanded carrier screening comprehensive panels testing dozens to hundreds of recessive genetic conditions in preconception and prenatal care. The demand for carrier status testing is shifting from specialist referral to integration into routine primary care, as genetic counsellors and reproductive medicine specialists consider carrier screening to be a standard of care, along with the continued decline in laboratory costs associated with comprehensive panels. The growth of the segment is evidence-based; knowing carrier status for diseases such as spinal muscular atrophy, cystic fibrosis and fragile X prior to conception enables couples to make appropriate reproductive choices.

Genetic Testing Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

Israel |

35% |

|

Latin America |

Brazil |

48% |

North America Genetic Testing Market Insights

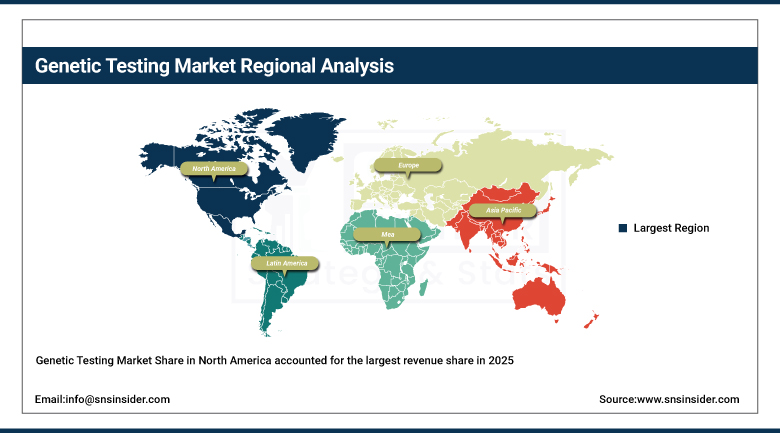

Genetic Testing Market Share in North America accounted for the largest revenue share in 2025 owing to the U.S. concentration of the largest number of qualified genetic testing companies worldwide, the most mature oncogenomics market globally, and the number one per-capita direct-to-consumer genetic testing adoption rate in the world. Through initiatives such as All of Us precision medicine and NHGRI genomic medicine programs, federal research investment via the NIH further develops the science that commercial genetic testing companies then take to the clinic. The rapidly increasing clinical implementation of liquid biopsy tests for both cancer detection and the monitoring of treatment responses, coupled with the increasing coverage by Medicare and private insurance, represents one of the liveliest developmental hotbeds in the U.S. genetic testing market.

The U.S. National institutes of Health National Human Genome Research Institute (NHGRI) has funded over 4.8 billion USD of genomic research and clinical applications since the completion of Human Genome Project. Multiple genetic testing products have received FDA Breakthrough Device designation, expediting their regulatory review and commercial availability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Genetic Testing Market Insights

Asia Pacific is the largest and fastest growing genetic testing market, underpinned by the world's largest national genomic medicine programs in China, Japan and South Korea, rapidly developing genetic counselling infrastructure in India and a burgeoning consumer demand for health genetic testing in the broad expanse of the region's burgeoning early-to-middle income consumer class. The scale of the Chinese government investment in genomic infrastructure is represented by places such as the National Genomics Data Centre in China and the China Kadoorie Biobank one of the world's largest prospective genetic epidemiology studies. Routine tumour genomic profiling for appropriate therapy selection has become a standard of care in Japan through the efforts of the National Cancer Centre of Japan; this success is having a ripple effect, making clinical genetic testing more commonplace in oncology practices across the country. Genetic testing infrastructure is now being established due to formal government genetic screening programs in India for hereditary blood disorders, in what is arguably a market with massive unmet need.

In the case of China, next-generation sequencing-based prenatal diagnosis was incorporated into national maternal health guidelines by the National Health Commission, and usage among licensed prenatal diagnosis centers nationwide was made mandatory. Japan's Ministry of Health, Labour and Welfare (MHLW) provides reimbursement for comprehensive genomic profiling panels for cancer patients, creating an extensive onco-genomics testing market with national health insurance coverage.

Europe Genetic Testing Market Insights

Europe is by far the most important market for Genetic Testing Market globally; UK, Germany, France and other Nordic countries lead. Together with its successor Genomics England program, the UK's 100,000 Genomes Project has built one of the most integrated national genomic medicine systems in the world, where whole genome sequencing is integrated into NHS clinical pathways for rare disease, cancer and infectious disease applications. To comply, both established clinical genetics laboratories and new direct-to-consumer testing models must navigate a complex compliance framework driven by GDPR data governance requirements that shape the storage, processing, and sharing of genetic data.

Genomics England's NHS Genomic Medicine Service has provided whole genome sequencing to more than 130,000 NHS patients who have rare disease and cancer. The EU's Genomics Initiative ‘1+ Million Genomes' plans to sequence one million genomes to be made available for research across all EU member states by 2026.

Middle East & Africa and Latin America Genetic Testing Market Insights

Both regions are relatively early in the evolution of the genetic testing market but demonstrating significant progress in certain aspects. Israel is unique in having a strong genetic research and testing environment, thanks to such factors as Maccabi Healthcare Services' one of the largest genome patient databases in the world, tech-enabled paradigm shifts in Israeli companies striving at innovation in computational genomics and AI-based genetic interpretation. Gulf states are investing in genomic medicine infrastructure through initiatives such as Saudi Arabia's Saudi Genome Program and the UAE Genome Program. With a pharmaceutical and academic research community that is among the largest in Latin America, Brazil has a vibrant environment for the development of genetic tests, and its genetic diversity makes it a source of potential interest for research and of commercial opportunity for ancestry and health risk genetic testing for other countries as well as for itself.

Genetic Testing Market Growth Drivers:

Rising cancer prevalence and technological advances in NGS dramatically expanding clinical and consumer genetic testing adoption

The growth engine of the market out of these operates simultaneously through two channels, one reinforcing the other. Clinically, the evidence base for genetic testing in oncology, rare disease diagnosis, prenatal care, and pharmacogenomics continues to expand, pulling physician adoption and payer coverage along with it. Regarding consumers, the growing population of direct-to-consumer genetic testing users often have now had the experience of personally experiencing the value of genetic information, increasing predisposition to engaging in clinical genetic testing recommendations made by their physician. The two channels feed back positively on one another: consumer testing helps educate genetic health, which fuels demand for clinical tests, and clinical testing provides evidence that genetic susceptibility conditions can be diagnosed and treated in clinically meaningful ways that can sustain consumer testing.

According to WHO's Global Cancer Observatory, due to ageing of the population, the number of cancer cases are estimated to increase by 77% globally between 2022 and 2050, leaving room for a large and growing genetic cancer screening and tumour profiling market. Genetic counselling and BRCA testing in women with family history risk factors are clinically used and reimbursed, due to recommendations from the U.S. Preventive Services Task Force (USPSTF), affecting millions of Americans.

Genetic Testing Market Restraints:

High testing costs and limited insurance coverage creating access barriers restricting genetic testing adoption globally

While cost reductions seen at the level of sequencing technologies can be impressive, genetic testing continues to be expensive for many of those applications that show the clearest clinical value. Whole genome sequencing, pan-cancer comprehensive gene panel tests, and advanced liquid biopsy assays (typically for minimal residual disease) are all examples of tests with variable out-of-pocket expenses for patients, with uneven insurance coverage for these tests lagging behind their individual price points. Search Reimbursement landscapes differ significantly by markets the U.S., UK and a number of European countries have formal clinical genetic testing coverage systems, albeit with different degrees of breadth, while waiting for many developing countries with clinical genetic testing reimbursement systems that provide inexpensive access to their populations. Concerns regarding privacy, especially regarding access to genetic information by employers and insurers, have made some consumer segments more hesitant and have restricted market penetration in otherwise supportive demographics.

Genetic Testing Market Opportunities:

Growing pharmacogenomics adoption and personalized medicine integration creating transformative genetic testing market growth opportunities

Pharmacogenomics could have one of the most easily-recognizable near-term expansion prospects in the genetic testing marketplace because it provides specificity, documentation and relevance to treatment outcomes. But if a genetic test can accurately predict that a patient will not metabolize a best-selling antidepressant with an expected low response rate, preventing potentially weeks of ineffective treatment and possibly dangerous adverse events, then the clinical and economic rationale for routine pre-prescription genetic testing is unassailable. U.S. and European major health systems have begun to use pre-trained programs for testing relevant genes by sequencing once and being able to store results for lifetime clinical use, leading to durable recurring test utilization from a single encounter. With growing insurance coverage for validated gene-drug pairs and electronic health record integration of pharmacogenomic results, this market size is expected to increase significantly as a portion of the overall market size.

Recent Developments:

-

2025: Myriad Genetics launched Precise MRD for minimal residual disease detection in hematological malignancies, enabling oncologists to monitor treatment response and detect disease recurrence at circulating tumor DNA levels below conventional imaging detection thresholds, with initial commercial rollout across major U.S. academic cancer centers.

-

2025: Illumina launched the NovaSeq X Plus high-throughput sequencing system with AI-assisted variant calling that reduces whole genome sequencing cost below USD 200 per genome at high throughput, marking a commercial milestone that further expands the economic viability of population-scale genomic medicine programs.

-

2026: Natera received FDA clearance for its Signatera ctDNA minimal residual disease test expansion into adjuvant treatment monitoring for stage II-III colorectal cancer patients, establishing a reimbursed clinical indication that creates a large recurring testing market among the approximately 150,000 Americans diagnosed with this stage annually.

Genetic Testing Market Key Players

Some of the Genetic Testing Market Companies

-

Illumina, Inc.

-

Myriad Genetics, Inc.

-

Thermo Fisher Scientific Inc.

-

Natera, Inc.

-

Guardant Health, Inc.

-

Foundation Medicine, Inc. (Roche)

-

Invitae Corporation

-

23andMe Holding Co.

-

Abbott Laboratories

-

Bio-Rad Laboratories, Inc.

-

F. Hoffmann-La Roche Ltd.

-

Quest Diagnostics Incorporated

-

LabCorp (Laboratory Corporation of America)

-

Counsyl (Myriad Genetics)

-

GeneDx, Inc.

-

Color Genomics Inc.

-

Ancestry.com DNA, LLC

-

Genomic Health, Inc. (Exact Sciences)

-

Centogene AG

-

Blueprint Genetics Oy

Genetic Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.67 Billion |

| Market Size by 2035 | USD 62.61 Billion |

| CAGR | CAGR of 11.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Next Generation Sequencing, Array Technology, PCR-based Testing, FISH, Others) • By Application (Ancestry & Ethnicity, Traits Screening, Genetic Disease Carrier Status, New Baby Screening, Health and Wellness - Predisposition/ Risk / Tendency) • By Product (Consumables, Equipment, Software & Services) • By Channel (Online, Offline) • By End Use (Hospitals & Clinics, Diagnostic Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Illumina, Inc., Myriad Genetics, Inc., Thermo Fisher Scientific Inc., Natera, Inc., Guardant Health, Inc., Foundation Medicine, Inc. (Roche), Invitae Corporation, 23andMe Holding Co., Abbott Laboratories, Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd., Quest Diagnostics Incorporated, LabCorp (Laboratory Corporation of America), Counsyl (Myriad Genetics), GeneDx, Inc., Color Genomics Inc., Ancestry.com DNA, LLC, Genomic Health, Inc. (Exact Sciences), Centogene AG, Blueprint Genetics Oy |

Frequently Asked Questions

North America dominated the Genetic Testing Market in 2025.

The Health & Wellness – Predisposition/Risk segment dominated with approximately 51.23% share in 2025.

The Next Generation Sequencing (NGS) segment dominated with approximately 49.15% share in 2025.

The Genetic Testing Market was valued at USD 21.67 billion in 2025.

The Genetic Testing Market is expected to grow at a CAGR of 11.34% from 2026 to 2035.

Get in Touch