Digital Dentistry Market Report Scope & Overview:

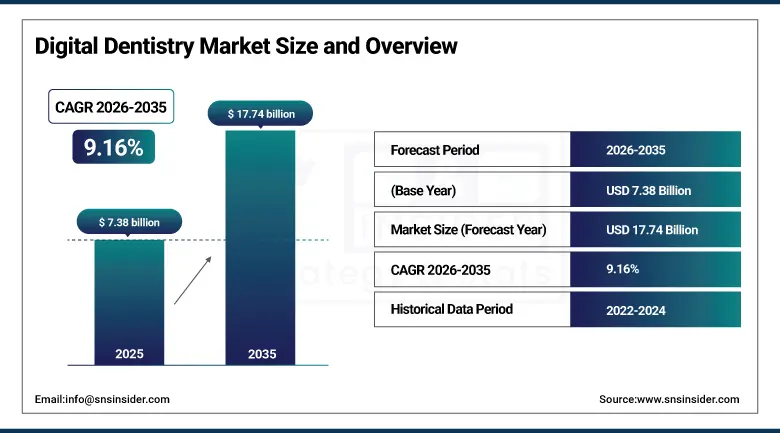

The Digital Dentistry Market was valued at USD 7.38 Billion in 2025 and is expected to reach USD 17.74 Billion by 2035, growing at a CAGR of 9.16% from 2026 to 2035.

Digital dentistry refers to the entire gamut of computer-assisted technologies used in the fields of dental diagnosis, treatment planning, production of prostheses, surgical planning, and dental office administration. It reflects a shift in the industry from an analogue workflow based on physical impressions, manual pouring of plaster models, and analog milling systems to a digitally enabled workflow based on intraoral scanners, CBCT, cloud treatment planning software, and automated machining and printing technologies. This shift is currently not happening consistently throughout all markets, but it is inevitable since it is driven by economic and clinical evidence proving the superiority of digital systems to analogue ones in terms of efficacy and efficiency at typical modern dental practice volumes. The case for digital dentistry is well-proven within orthodontics, implant dentistry, and restoration. Intraoral scanning removes the pain and lack of dimensional accuracy inherent to conventional polyvinylsiloxane impressions while offering a digital model whose accuracy allows for the creation of highly accurate prosthetic devices with minimal remakes. CBCT scans provide 3D bone density and volume information essential for planning dental implants.

Dentsply Sirona launched the Primemill premium in-office CAD/CAM milling system expansion in 2025, integrating its Cerec Primescan intraoral scanning, CEREC Software treatment planning, and Primemill fabrication into a seamlessly connected same-day dentistry platform capable of producing zirconia, lithium disilicate, and polymer-based restorations within a single patient visit.

Market Size and Forecast

-

Market Size in 2026E: USD 8.06 Billion

-

Market Size by 2035: USD 17.74 Billion

-

CAGR: 9.16% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Digital Dentistry Market - Request Free Sample Report

Digital Dentistry Market Trends

-

AI-powered dental imaging tools are improving accuracy in caries detection, periodontal analysis, and root canal diagnostics in digital dentistry workflows.

-

Integrated digital dentistry platforms combining scanning, imaging, CAD/CAM, and practice management are replacing fragmented workflows and improving operational efficiency.

-

Tele-dentistry and remote consultation platforms are expanding access to orthodontic monitoring and specialist dental care through digital channels.

-

Adoption of cloud-based dental practice management software is increasing for centralized data management and multi-location practice coordination.

-

Digital patient engagement tools such as virtual smile design and AR-based treatment visualization are improving patient experience and treatment acceptance rates.

The U.S. Digital Dentistry Market Outlook

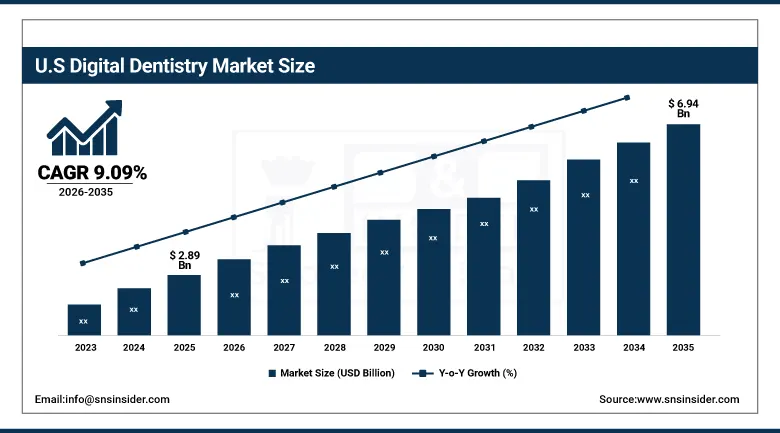

The U.S. Digital Dentistry Market was valued at approximately USD 2.89 Billion in 2025 and is expected to reach approximately USD 6.94 Billion by 2035, growing at a CAGR of approximately 9.09%.

The US leads the digital dentistry market globally, being underpinned by the country’s per capita spending on dental care among all leading economies, the most commercially evolved environment for dental technologies, and the current state of affairs in dental practices where the private and corporate investments aimed at technology differentiation ensure steady demand for innovative digital dental solutions. The process of consolidation in the form of dental service organizations backed by private equity has become an important structural driver of the adoption of digital technologies, with DSO management teams working on the implementation of digital workflows across their practice networks. Finally, there is the certainty provided to dental technology vendors by FDA-approved procedures, such as those under the 510(k) clearance route.

Patterson Companies expanded its Patterson Dental digital technology distribution programme in 2025, establishing enhanced clinical support and in-practice training services for its expanded intraoral scanner and CAD/CAM equipment portfolio from technology partners including Dentsply Sirona, 3Shape, and Planmeca.

Digital Dentistry Market Segment Analysis

-

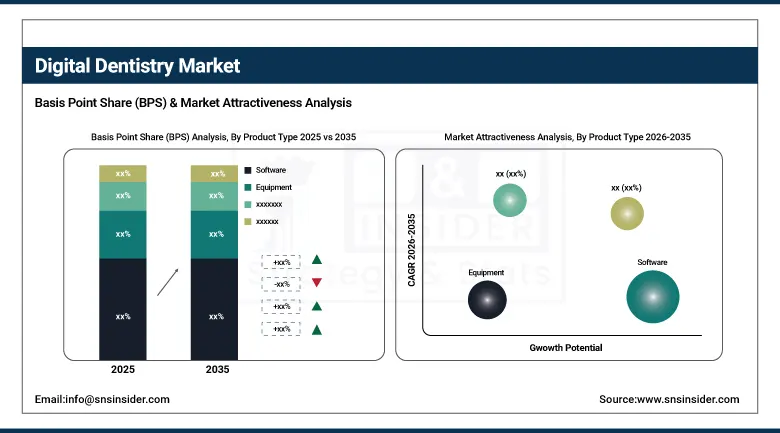

By Product Type, the software segment dominated the digital dentistry market with 55.20% share in 2025, while the equipment segment is the fastest growing product type during 2026 to 2035.

-

By Technology, the CAD/CAM systems segment dominated the digital dentistry market with 34.82% share in 2025, while the 3d printing segment is the fastest growing technology during 2026 to 2035.

-

By Application, the restorative dentistry segment dominated the digital dentistry market with 38.47% share in 2025, while the implantology segment is the fastest growing application during 2026 to 2035.

-

By End User, the dental clinics & hospitals segment dominated the digital dentistry market with 66.80% share in 2025, while the dental laboratories segment is the fastest growing end user during 2026 to 2035.

By Product Type, software dominates, equipment grows fastest

Software generated 55.20% of digital dentistry market revenue in 2025, encompassing treatment planning applications, CAD software for prosthetic design, practice management platforms, patient communication tools, and AI-powered diagnostic imaging software whose combined recurring subscription and license revenue exceeds equipment sales in the established digital dentistry markets of North America and Europe.

Equipment is growing fastest as dental practice adoption of digital physical infrastructure, including intraoral scanners, CBCT imaging systems, CAD/CAM milling units, and 3D printers, continues expanding into previously underserved market segments including smaller independent dental practices in emerging markets and corporate dental group acquisitions whose new equipment investment follows practice acquisition.

By Application, restorative dentistry dominates, implantology grows fastest

Restorative dentistry retained the dominant application position with 38.47% of digital dentistry revenue in 2025, reflecting the central role of prosthetic restoration fabrication in the dental workflow and the well-established commercial success of digital restorative workflows from intraoral scan to CAD/CAM crown production. The volume of restorative dental procedures globally, encompassing direct and indirect restorations across tooth-colored composites, ceramic inlays and onlays, full crowns, and multi-unit bridges, provides the largest application market for CAD/CAM fabrication technology and digital imaging systems whose adoption is most commercially mature.

Implantology is growing fastest as guided implant surgery using CBCT-derived surgical guides, digital implant planning software, and immediate loading protocols whose success depends on precise planning enable implant procedure outcomes that attract growing patient demand and clinical adoption. Each implant case requires CBCT imaging, digital planning, and often guided surgery infrastructure that creates multi-product digital dentistry procurement per procedure.

By Technology, CAD/CAM systems dominate, 3D printing grows fastest

CAD/CAM systems accounted for 34.82% of digital dentistry technology revenue in 2025, driven by the widespread adoption of in-office and laboratory milling systems for same-day crown and prosthetic production whose clinical and economic advantages over conventional laboratory workflows are thoroughly documented across dental professional literature. The CAD/CAM category spans chairside systems including Dentsply Sirona's Cerec and KaVo's Arctica to large laboratory milling centers whose multi-axis precision milling produces implant bars, full-arch frameworks, and complex prosthetic structures from blocks of zirconia, titanium, and polymer materials.

Three-dimensional printing is growing fastest as dental photopolymer print technology has matured sufficiently to produce clinically accepted surgical guides, orthodontic aligner models, temporary restorations, and increasingly permanent restorations at print costs per unit substantially below equivalent milling-based production, generating strong economic incentive for in-laboratory and in-practice 3D printing adoption.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Digital Dentistry Market Insights

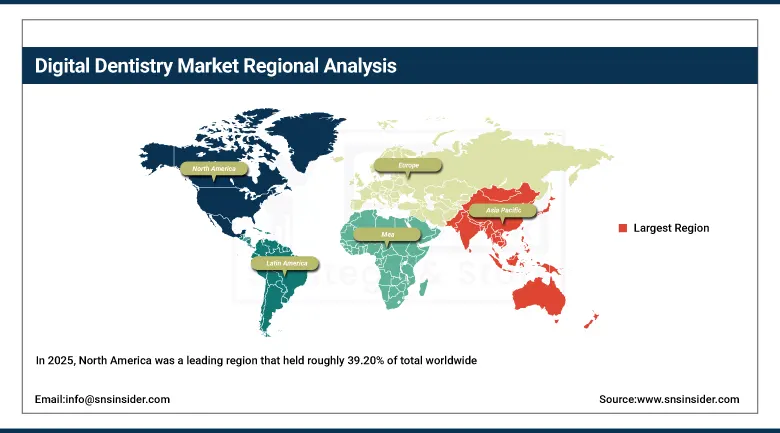

In 2025, North America was a leading region that held roughly 39.20% of total worldwide spending on digital dentistry. North American dominance is mainly attributed to the United States, which makes up around 84.73% of the regional spend because of its status as the region with the largest spending on dental care, the highest adoption rate of dental technology of all major economies, and the spending capacity of dental service organizations who adopt digital workflows. Canada supplements the United States with its robust private dental care system and its rising number of corporate dental organizations.

U.S. dental care expenditure exceeds USD 174 billion annually, making it one of the world’s largest dental healthcare markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Digital Dentistry Market Insights

Europe accounted for about 28.47% of worldwide Digital Dentistry sales in 2025. Among the leading countries are Germany, France, United Kingdom, Switzerland, and Italy due to their highly advanced dental equipment manufacturing industries as well as dental practices' high degree of integration with digital technologies. Germany alone contributed around 28.47% of Europe's revenue because of its superior dental equipment manufacturing industry which is represented by such companies as Dentsply Sirona, KaVo Kerr Group, and Bego with substantial manufacturing facilities in Germany. Europe features one of the highest levels of digital workflow integration in dental labs across the globe, stimulated by competition to achieve greater precision and reduce production time.

The United Kingdom has over 44,000 registered dentists, while France has more than 47,000 dental practitioners adopting digital imaging and orthodontic technologies.

Asia Pacific Digital Dentistry Market Insights

The Asia Pacific region will experience the highest growth rate among all regional digital dentistry markets, at a CAGR of about 12.84% up to 2035, thanks to the increasing investments in dental facilities infrastructure, increasing demand for aesthetic and restorative dental treatments from middle-class urban populations, and oral health programs introduced by governments which are improving dental care availability among the rural population of the region. China represents about 38.47% of Asia Pacific revenues because of its booming private dentistry sector, dental laboratories embracing digitization technology, and increasing government investments in dental health initiatives. India, Japan, South Korea, and Australia make valuable contributions as well; particularly notable are the advanced aesthetic dentistry culture of South Korea and the dental tourism services offered in India.

Japan has over 100,000 practicing dentists and is a major adopter of advanced dental imaging, robotics, and digital prosthodontic technologies.

MEA & Latin America Digital Dentistry Market Insights

The Middle East and Latin America regions are emerging markets for Digital Dentistry, with increasing investments in private dental care facilities, increased customer awareness of aesthetic dentistry, and exposure to foreign training programs creating growing adoption of digital dental technologies. In the MEA region, the UAE has the largest share of revenue at approximately 22.84% of the total because of its diverse and well-developed private dental industry that caters to an international clientele with technological standards equal to or higher than the expectations in the North American and European markets. In the Latin American region, the largest revenue share belongs to Brazil with approximately 43.84%, thanks to its large number of dentists globally and the presence of the fast-growing cosmetic dentistry sector.

The UAE has around 5,000–6,000 licensed dentists, with a high concentration in Dubai and Abu Dhabi private clinics.

Market Dynamics

Growth Drivers: Rising demand for same-day dentistry solutions and increasing technology standardization across dental service organizations are driving digital dentistry market growth.

Economically, there has been much progress made with regards to investing in digital dentistry due to the reduced cost of technology. The use of a chair side CAD/CAM machine to deliver same day crowns through eliminating time in the laboratory, eliminating patient inconvenience with provisional crowns, and cutting the time it takes to get paid down from four to six weeks to one visit allows the system payback within one to two years. The need for capital efficiency in dental service organizations makes this investment decision very strong since it is possible to measure improvement in return on investment across several purchased offices.

Restraints: High digital equipment costs and limited digital workflow expertise among dental professionals are restraining digital dentistry market growth, especially in smaller clinics and emerging markets.

An overall digital dentistry chairside process using intraoral scanner, CBCT machine, CAD/CAM miller, and the associated software would have an overall capital cost ranging from USD 150,000 up to USD 400,000, a level of expenditure that serves as a high economic barrier, especially for small independent dental offices which are unable to comfortably finance either the debt service or opportunity cost of such an investment. Clinical skills development for a digital dentistry process involves training costs, since dentists who have only received analogue dental training need to acquire technical skills in terms of digital scanning techniques and digital treatment planning among others. Additionally, emerging economies have inferior digital dental equipment maintenance infrastructures compared to North America and Europe, and hence practices considering investing in such equipment face risks of equipment breakdowns and failure in the event of maintenance requirements.

Opportunities: AI-based diagnostic imaging and tele-dentistry platform expansion are creating major growth opportunities by extending digital dentistry into preventive and remote care services.

Commercial success lies in AI diagnostic imaging software that achieves more than 90% accuracy in detecting carious teeth and assessing the level of periodontal bone. At practice level, AI diagnostics that identify pathologies for a clinician to check prior to reading X-ray images helps enhance detection, minimize risks of missing diagnosis, and ensure return on investment by way of improved clinical outcomes. Tele-dentistry services are increasingly leveraging the commercial potential of digital dentistry by offering consultations and monitoring to areas that lack specialists because patients there are unwilling to use digital technology.

Recent Developments:

-

2025: Dentsply Sirona launched the Primemill premium in-office milling system integration with Primescan intraoral scanning and CEREC Software, achieving 62% reduction in AI-guided crown design time and enabling same-day zirconia and lithium disilicate restoration production at general dental practices without advanced CAD/CAM design training.

-

2025: 3Shape launched its Unite platform ecosystem management system enabling seamless data flow across its Trios intraoral scanner, Dental System laboratory software, and cloud collaboration tools, providing dental clinics and laboratories with unified order management, case tracking, and quality documentation across the complete digital clinical and laboratory workflow.

Digital Dentistry Market Key Players are:

-

Dentsply Sirona Inc.

-

Align Technology Inc.

-

3Shape A/S

-

Planmeca Oy

-

Straumann Holding AG

-

Nobel Biocare (Straumann Group)

-

Carestream Dental LLC

-

Ivoclar AG

-

KaVo Kerr Group (Envista Holdings)

-

Zimmer Biomet Holdings Inc.

-

Patterson Companies Inc.

-

Henry Schein Inc.

-

SprintRay Inc.

-

Roland DGA Corporation

-

Shofu Dental Corporation

-

GC Corporation

-

BEGO GmbH & Co. KG

-

Midmark Corporation

-

Medit Corp.

-

Vatech Co. Ltd

Digital Dentistry Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.38 Billion |

| Market Size by 2035 | USD 17.74 Billion |

| CAGR | CAGR of 9.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Equipment, Software) • By Technology (CAD/CAM Systems, Digital Imaging & Radiology, Intraoral Scanners, 3D Printing, Dental Practice Management Software, Others) • By Application (Restorative Dentistry, Orthodontics, Implantology, Endodontics, Prosthodontics, Others) • By End User (Dental Clinics & Hospitals, Dental Laboratories, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dentsply Sirona Inc., Align Technology Inc., 3Shape A/S, Planmeca Oy, Straumann Holding AG, Nobel Biocare (Straumann Group), Carestream Dental LLC, Ivoclar AG, KaVo Kerr Group (Envista Holdings), Zimmer Biomet Holdings Inc., Patterson Companies Inc., Henry Schein Inc., SprintRay Inc., Roland DGA Corporation, Shofu Dental Corporation, GC Corporation, BEGO GmbH & Co. KG, Midmark Corporation, Medit Corp., Vatech Co. Ltd. |

Frequently Asked Questions

North America dominated the Digital Dentistry Market in 2025, holding approximately 39.20% of global revenues, with the United States accounting for approximately 84.73% of North American revenues.

The restorative dentistry segment dominated the Digital Dentistry Market with 38.47% share in 2025.

The primary growth factors are the clinical and economic advantages of same-day digital crown production over conventional laboratory workflows, dental service organization network-wide digital technology standardization programmes creating large-volume equipment procurement, AI-powered diagnostic imaging improving clinical detection accuracy and practice efficiency, and the growing consumer demand for aesthetic dental treatments whose precision requirements favor digital diagnostic and fabrication workflows.

The Digital Dentistry Market was valued at USD 7.38 Billion in 2025.

The Digital Dentistry Market is expected to grow at a CAGR of 9.16% from 2026 to 2035.

Get in Touch