Palladium Market Report Scope & Overview:

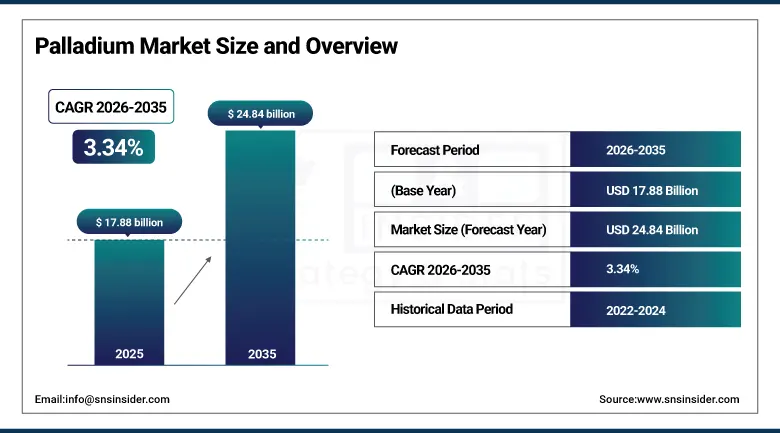

The Palladium Market was valued at USD 17.88 Billion in 2025 and is expected to reach USD 24.84 Billion by 2035, growing at a CAGR of 3.34% from 2026–2035.

The global palladium market occupies a strategically indispensable position in the global economy as one of the rarest platinum group metals whose unique catalytic, electrical, and chemical properties create irreplaceable applications across the automotive emission control, electronics manufacturing, chemical processing, and emerging hydrogen technology sectors. Palladium’s primary commercial application as the critical active catalyst material in three-way catalytic converters for gasoline and hybrid vehicle exhaust treatment systems accounts for approximately 80 to 85% of global fabrication demand. The palladium market’s supply architecture is defined by its extraordinary geographic concentration, with the Norilsk-Talnakh region of Russia and South Africa’s Bushveld Igneous Complex together accounting for approximately 75 to 80% of global mined palladium production, creating supply vulnerability to operational disruption, labour action, geopolitical restriction, and natural disaster events at these production centres that has historically generated acute price spikes whose commercial consequences ripple through the entire automotive and electronics industries that depend on palladium supply continuity.

Sibanye Stillwater’s March 2025 commissioning of an advanced automated palladium recycling unit at its Montana operation, increasing recovery efficiency by 15% through improved sorting, pre-processing, and hydrometallurgical extraction technologies, represents the strategic investment direction that leading PGM companies are pursuing to develop recycling as a commercially significant and supply-chain-resilient secondary palladium source that partially offsets the geopolitical and operational supply risks associated with primary mined production concentration.

Market Size and Forecast

-

Market Size in 2026E: USD 18.48 Billion

-

Market Size by 2035: USD 24.84 Billion

-

CAGR: 3.34% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Palladium Market - Request Free Sample Report

Palladium Market Trends

-

Growing investment in palladium recycling infrastructure and technology across the automotive, electronics, and jewellery sectors, driven by the combination of palladium’s high market value.

-

Accelerating research and commercial development of palladium’s hydrogen absorption and membrane separation properties for applications including hydrogen fuel cell components, hydrogen purification membranes for industrial and energy applications.

-

Rising adoption of palladium in electronics manufacturing applications including multi-layer ceramic capacitors whose palladium-silver electrode systems provide superior performance at elevated temperatures, electrical connectors.

-

Growing investment in platinum-palladium substitution research within the automotive catalytic converter application, as the significant price premium that palladium has historically commanded over platinum has created commercial motivation for catalytic converter manufacturers.

-

Expanding palladium demand from the chemical processing industry’s growing use of palladium-based catalysts in pharmaceutical synthesis, fine chemical production, and petrochemical refining applications.

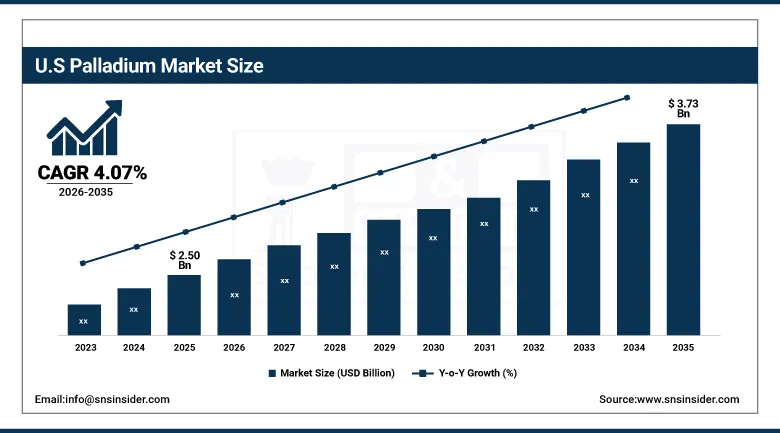

U.S. Palladium Market Outlook

The U.S. Palladium Market was valued at approximately USD 2.50 Billion in 2025 and is expected to reach approximately USD 3.73 Billion by 2035, growing at a CAGR of approximately 4.07%.

The United States palladium market is shaped by its dual character as both a major palladium consuming nation, whose automotive manufacturing sector, advanced electronics industry, and growing chemical processing operations collectively sustain substantial annual palladium fabrication demand, and a palladium producing nation through Sibanye Stillwater’s Stillwater and East Boulder mines in Montana that represent the only economically significant primary palladium mining operations outside of Russia and South Africa.

The U.S. government’s Inflation Reduction Act’s requirements for domestic content in vehicle components qualifying for electric vehicle tax credits is creating indirect palladium market implications through its acceleration of U.S. domestic vehicle manufacturing investment, whose production scale growth increases the total palladium catalyst demand from domestically manufactured hybrid and gasoline vehicles while the EV share of production simultaneously reduces the average palladium content per vehicle across the total production mix as the domestic fleet progressively electrifies.

Palladium Market Segment Analysis

-

By Form, refined palladium dominated with approximately 59% revenue share in 2025 owing to strong demand from automotive and jewellery applications requiring high-purity metal for catalytic converter catalyst washcoat preparation and premium alloy jewellery fabrication; palladium alloys are the fastest-growing form segment at a CAGR of approximately 7.13%.

-

By Application, automotive catalytic converters dominated with approximately 49% market share in 2025 owing to the requirement for palladium’s specific catalytic activity in three-way converter systems for gasoline and hybrid vehicle emission compliance under tightening regulatory standards globally; electronics and electrical is the fastest-growing application segment.

-

By End User, the automotive industry dominated the palladium market in 2025 through its automotive catalytic converter demand that represents the foundational commercial basis for the global palladium supply chain; the chemical industry is the fastest-growing end user.

By Form, refined palladium dominates, palladium alloys grow fastest

Refined palladium retained the dominant form position with approximately 59% of the palladium market in 2025, reflecting its fundamental role as the high-purity metal form required by the two largest palladium application categories: automotive catalytic converters, whose washcoat preparation processes require palladium in high-purity powder or sponge precursor forms that are processed into catalytic material at catalyst manufacturing facilities, and jewellery fabrication whose palladium-gold and palladium-silver alloy applications require high-purity palladium input for the controlled alloy formulation that achieves the colour, hardness, and tarnish resistance specifications of finished jewellery products. The refined palladium market’s supply structure is defined by the primary smelting and refining operations at Norilsk Nickel’s Norilsk and Kola operations in Russia, Anglo American Platinum and Implats’ processing facilities in South Africa, and the secondary refining capacity at precious metal refiners including Heraeus, BASF Catalysts, and Umicore whose processing of spent catalytic converters and electronic scrap provides a growing secondary refined palladium supply stream whose quality is equivalent to primary refined metal for virtually all application requirements.

Palladium alloys are the fastest-growing form segment at a CAGR of approximately 7.13% through 2035, driven by the expanding range of high-performance electronics, medical device, and dental application requirements whose performance specifications require the specific combination of properties that palladium alloy formulations uniquely deliver. Palladium-silver alloys’ use in multi-layer ceramic capacitor inner electrodes, whose combination of electrical conductivity, sinterability, and oxidation resistance during firing provides the electrode performance that Class I and Class II MLCC specifications require for automotive and industrial electronics applications, represents the most commercially significant electronics-sector palladium alloy demand category whose growth reflects both the MLCC volume growth driven by electronic content per vehicle growth and the specific performance advantages of palladium-silver electrode systems over alternative base metal electrode formulations in the high-reliability, high-temperature applications where automotive-grade component specifications are most demanding.

By Application, automotive dominates, electronics grows fastest

Automotive catalytic converters retained the dominant application position with approximately 49% of the palladium market in 2025, a dominance that reflects both the market’s historical development where palladium’s commercial significance was established through the automotive emission control application and the continuing central importance of gasoline and hybrid vehicle production to global palladium demand despite the progressive electrification of the vehicle fleet that is beginning to reshape the longer-term automotive palladium demand trajectory. The catalytic converter application’s demand dynamics are shaped by the interaction between global vehicle production volumes that determine the total number of converter-equipped vehicles being manufactured annually, the average palladium loading per converter that emission regulation stringency determines with tighter standards requiring higher catalyst metal content to achieve compliance, and the hybrid vehicle fleet’s growing proportion of global production that maintains internal combustion engine and catalytic converter requirements while adding electric drivetrain components in a production configuration that creates potentially higher per-vehicle palladium demand than conventional gasoline vehicles whose smaller engines and simpler emission management requirements can be achieved at lower catalyst loading. The China VI and Euro 7 emission standard implementation timelines are particularly significant for automotive palladium demand development, as both regulatory frameworks mandate substantially lower allowable emission limits that catalyst manufacturers are achieving through increased precious metal loading including higher palladium content in the catalytic washcoat formulations that achieve compliance.

Electronics and electrical is the fastest-growing application segment in the palladium market, propelled by the extraordinary growth of electronic device production whose miniaturisation trend is simultaneously increasing the electronic content per device and driving demand for the high-performance connector, capacitor electrode, and surface finish materials that palladium and palladium alloy specifications uniquely provide in the reliability-critical applications where base metal alternatives’ inferior corrosion resistance and contact stability do not satisfy the performance lifetime requirements. The 5G infrastructure deployment wave is creating a particularly significant new demand driver for palladium in the high-frequency connector and filter applications of 5G base station equipment, where palladium’s high-frequency electrical performance characteristics and corrosion resistance provide specification advantages over competing contact materials in the demanding outdoor telecommunications infrastructure environment whose component lifetime expectations and maintenance cost sensitivity favour the higher upfront material cost of palladium specifications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

South Africa |

52.4% |

|

Latin America |

Brazil |

44.2% |

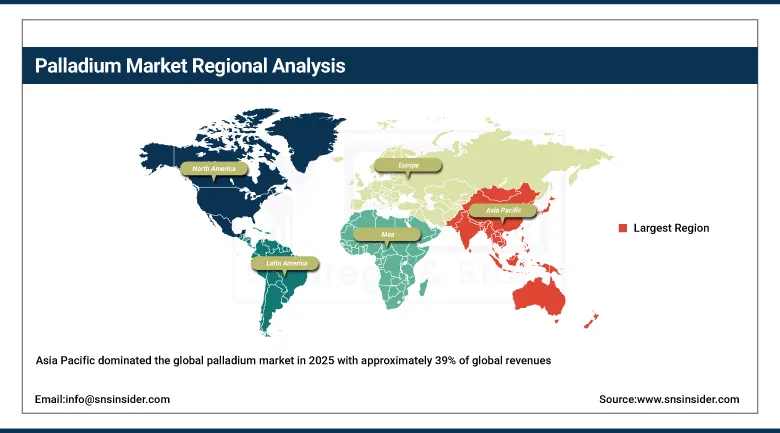

Asia Pacific Palladium Market Insights

Asia Pacific dominated the global palladium market in 2025 with approximately 39% of global revenues, driven by the region’s status as the world’s largest automotive production centre, the largest electronics manufacturing base, and the fastest-growing chemical processing industry, whose combined palladium demand across all three primary application categories creates the highest total regional palladium consumption of any geographic area globally. China accounts for approximately 61.7% of Asia Pacific palladium revenues through its extraordinary combination of the world’s largest vehicle production volume, which generates palladium catalytic converter demand that is progressively increasing as China’s China VI emission standards require higher catalyst loading for compliance, the world’s largest consumer electronics manufacturing sector whose MLCC, connector, and surface finish palladium applications generate substantial annual demand, and a rapidly growing pharmaceutical and fine chemical industry whose palladium catalyst application is expanding as domestic API manufacturing capacity increases. Japan and South Korea represent sophisticated secondary Asian palladium markets where automotive, electronics, and chemical industry applications sustain meaningful and technically demanding palladium consumption across multiple application categories whose quality specifications require the highest-purity refined palladium input.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Palladium Market Insights

North America is the fastest-growing regional palladium market due to the clean energy investment surge and advanced vehicle manufacturing that have accelerated palladium adoption in catalytic converter, hydrogen technology, and electronics applications, combined with the growing domestic palladium supply from Sibanye Stillwater’s Montana mining operations and secondary recovery from the region’s automotive recycling sector that provides supply chain resilience independent of Russian and South African primary supply. The United States accounts for approximately 87.4% of North American palladium revenues through its combination of substantial automotive manufacturing, advanced electronics industry, and growing hydrogen technology research and commercialisation investment. Canada contributes approximately 12.6% of North American revenues through its automotive sector, mining industry, and growing clean energy technology development programmes whose hydrogen fuel cell and electrolysis applications create incremental palladium demand in the emerging energy transition technology category.

Europe Palladium Market Insights

Europe is a major palladium consuming market where the automotive manufacturing sector’s substantial production of gasoline and hybrid vehicles, the sophisticated electronics and chemical industries, and the region’s world-leading precious metal refining and recycling infrastructure collectively define the market’s commercial character. Germany accounts for approximately 22.3% of European palladium revenues as the region’s largest national market, driven by its world-class automotive manufacturing sector encompassing Volkswagen, BMW, Mercedes-Benz, Stellantis, and their global supply chains whose emission compliance requirements sustain substantial palladium catalyst purchasing, combined with the German chemical and electronics industries’ palladium catalyst and component applications. The European Union’s strategic autonomy agenda, which identifies palladium as a critical raw material whose supply security is inadequate given its concentration in Russian and South African primary sources, is creating institutional investment in European recycling infrastructure and alternative supply development that may influence the market’s supply dynamics through the forecast period.

MEA & Latin America Palladium Market Insights

The Middle East and Africa region’s palladium market is dominated by South Africa’s extraordinary position as both the world’s second-largest primary palladium producer and a significant domestic refining centre for platinum group metals, with South Africa accounting for approximately 52.4% of regional revenues through the processing and export operations of Anglo American Platinum, Implats, Sibanye Stillwater’s South African operations, and Northam Platinum whose Bushveld Complex mining and beneficiation activities define the country’s commercial relationship with the global palladium market. Brazil leads Latin American palladium revenues at approximately 44.2% of the regional total through its automotive manufacturing sector, whose substantial production of gasoline and flex-fuel vehicles generates catalytic converter palladium demand, and its growing electronics and pharmaceutical manufacturing industries whose palladium applications create secondary demand categories alongside the dominant automotive use.

Market Dynamics

Growth Drivers: Tightening global vehicle emission standards increasing palladium loading per catalytic converter, growing electronics miniaturisation driving connector and capacitor electrode demand

The primary structural growth drivers for the palladium market are the progressive tightening of global vehicle emission standards whose implementation across China, the EU, and other major automotive markets requires progressively higher precious metal loading in catalytic converter washcoat formulations to achieve compliance, creating per-vehicle palladium demand growth that partially offsets the volume impact of electric vehicle penetration in the overall vehicle fleet. The electronics miniaturisation trend’s impact on palladium demand is simultaneously growing as the increasing electronic content per vehicle, per smartphone, and per industrial system creates proportionally growing demand for the MLCC electrode, connector contact, and PCB surface finish applications where palladium’s performance advantages over base metal alternatives are most commercially compelling. The emerging hydrogen economy’s development is creating a nascent but potentially significant new palladium demand category, as palladium membrane technology for hydrogen purification and palladium catalyst applications in fuel cell electrode and reforming catalyst manufacturing represent application developments whose commercial scale is growing as hydrogen production and utilisation infrastructure investment accelerates under global clean energy transition investment programmes.

Restraints: Electric vehicle transition reducing per-vehicle palladium content at fleet level, geopolitical supply concentration in Russia creating import dependency risk and price volatility

The most significant structural restraint on the palladium market’s demand trajectory is the electric vehicle transition’s progressive impact on automotive catalytic converter demand, as battery electric vehicles that produce zero tailpipe emissions require no catalytic converter and therefore generate zero palladium catalyst demand per vehicle, meaning that every percentage point increase in BEV’s share of new vehicle production removes a portion of the automotive palladium demand that has historically defined the market’s commercial scale. The geopolitical supply concentration risk represented by Russia’s role as the world’s largest primary palladium producer creates persistent price volatility exposure for consuming industries whose supply chains are structurally dependent on Russian palladium exports whose availability is subject to geopolitical and sanctions risk that the Ukraine conflict has made concretely significant in ways that previously seemed theoretical.

Opportunities: Hydrogen membrane and fuel cell catalyst applications creating new demand category, automotive recycling technology improvement increasing secondary supply recovery

The hydrogen economy represents the most commercially significant long-term opportunity for palladium demand development beyond its established automotive and electronics applications, as palladium’s unique ability to absorb hydrogen at elevated temperatures and release it upon cooling creates a natural fit for hydrogen purification membrane applications whose commercial development in the growing hydrogen production infrastructure market could establish a meaningful new demand category that provides demand base diversification away from the automotive application whose EV-driven contraction represents the market’s most significant structural risk through the forecast period.

Recent Developments:

-

2025: Sibanye Stillwater commissioned an advanced automated palladium recycling unit at its Montana operation in March 2025, increasing recovery efficiency by 15% through improved sorting, pre-processing, and hydrometallurgical extraction technologies that enable more complete palladium capture from spent catalytic converter material, strengthening the domestic U.S. secondary palladium supply and improving the company’s circular economy positioning.

-

2025: Anglo American Platinum released its 2025 palladium market outlook confirming its investment in beneficiation technology improvements at South African processing facilities aimed at increasing palladium recovery yields from platinum group metal concentrate processing, improving the efficiency of converting mined ore into refined palladium and reducing the energy consumption per troy ounce of refined production.

-

2025: Heraeus Precious Metals expanded its palladium refining and recycling capacity across its European operations to serve the growing secondary palladium recovery market from end-of-life catalytic converters and electronic scrap, investing in advanced sorting technology and chemical processing infrastructure that improves recovery rate and reduces processing time for the growing volumes of palladium-bearing secondary material entering the recycling stream.

-

2025: BASF Catalysts invested in expanded palladium catalyst manufacturing capacity for automotive and chemical process applications, incorporating advanced washcoat formulation technology that achieves equivalent catalytic performance with reduced palladium loading for specific automotive application types, improving precious metal efficiency and reducing per-unit palladium consumption for compliant emission performance.

-

2025: Umicore expanded its precious metal recycling network for electronic waste processing across Asia Pacific, establishing new collection and pre-processing partnerships with electronics manufacturers and recyclers in China, South Korea, and Japan that increase the capture rate of palladium-bearing electronic scrap from the region’s extraordinary consumer electronics production and consumption volume.

Palladium Market Key Players

-

PJSC MMC Norilsk Nickel

-

Anglo American Platinum Ltd.

-

Impala Platinum Holdings Ltd. (Implats)

-

Sibanye Stillwater Ltd.

-

Northam Platinum Holdings Ltd.

-

Heraeus Holding GmbH

-

BASF SE (Catalysts division)

-

Umicore SA

-

Johnson Matthey plc

-

Vale SA

-

Vedanta Resources Ltd.

-

Russian Platinum

-

Stillwater Mining Company (Sibanye)

-

Ivanhoe Mines Ltd.

-

Palladium One Mining Inc.

-

Platinum Group Metals Ltd.

-

Sprott Physical Platinum and Palladium Trust

-

Royal Bafokeng Platinum Ltd.

-

Sylvania Platinum Ltd.

-

Excello Technology (precious metals processing)

Palladium Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.88 Billion |

| Market Size by 2035 | USD 24.84 Billion |

| CAGR | CAGR of 3.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form (Refined Palladium, Palladium Alloys, Palladium Sponge, Palladium Powder) • By Application (Automotive Catalytic Converters, Electronics & Electrical, Chemical Catalysts, Jewellery, Hydrogen & Fuel Cells, Others) • By End User (Automotive Industry, Electronics Industry, Chemical Industry, Jewellery Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | PJSC MMC Norilsk Nickel, Anglo American Platinum Ltd., Impala Platinum Holdings Ltd. (Implats), Sibanye Stillwater Ltd., Northam Platinum Holdings Ltd., Heraeus Holding GmbH, BASF SE (Catalysts division), Umicore SA, Johnson Matthey plc, Vale SA, Vedanta Resources Ltd., Russian Platinum, Stillwater Mining Company (Sibanye), Ivanhoe Mines Ltd., Palladium One Mining Inc., Platinum Group Metals Ltd., Sprott Physical Platinum and Palladium Trust, Royal Bafokeng Platinum Ltd., Sylvania Platinum Ltd., Excello Technology (precious metals processing) |

Frequently Asked Questions

The Palladium Market is expected to grow at a CAGR of 3.34% from 2026 to 2035.

The Palladium Market was valued at USD 17.88 Billion in 2025.

Tightening global vehicle emission standards requiring higher palladium loading per catalytic converter to achieve compliance, growing electronics miniaturisation driving demand for palladium connector, capacitor electrode, and surface finish applications.

Refined Palladium dominated with approximately 59% of revenues in 2025.

Asia Pacific dominated the Palladium Market in 2025, accounting for approximately 39% of global revenues, with China as the leading national market.

Get in Touch