Paper Diagnostics Market Overview

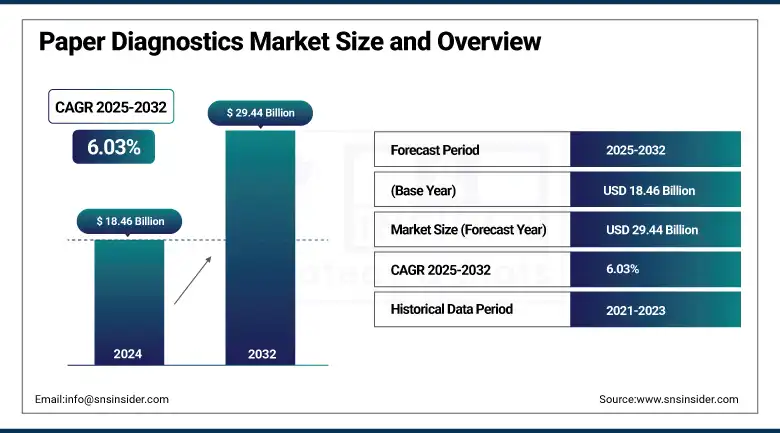

The Paper Diagnostics Market size was valued at USD 18.46 billion in 2024 and is expected to reach USD 29.44 billion by 2032, growing at a CAGR of 6.03% over 2025-2032.

The global paper diagnostics market is gaining stellar traction on account of its cost-effective nature, portability, and low infrastructural demands, especially in low-resource regions. The growing global burden of infectious diseases, cancer, and chronic diseases, and that too particularly in developing countries further increases the need for rapid, point-of-care (POC) testing. For instance, the WHO has recently reported more than 247 million malaria cases in 2021, underscoring the demand for affordable diagnostics such as lateral flow tests and microfluidic paper-based analytical devices (µPADs). These tests present a major advantage: they cost between 5 and 10 times less than classical laboratory diagnostics, while providing sensitivity and specificity of similar levels.

To Get more information On Paper Diagnostics Market - Request Free Sample Report

Moreover, growth in R&D expenditure, particularly in microfluidics and nanotechnology, is assisting in innovation. U.S. federal R&D investment exceeded USD 190 billion in 2023, although NIH support is heavily weighted toward diagnostics and preventive health technologies. Companies like Abingdon Health, Diagnostics for the Real World, and LumiraDx are working on paper-based multiplex tests, supported by fast approval pathways and regulators. FDA’s 2020 guidance for diagnostic test reporting has facilitated the regulatory path of new diagnostic platforms. Additionally, the global supply chain has been improved following COVID-19, making access to and the scale-up of paper diagnostics products available. In addition to funding from educational institutions and government, however, it has been reported in the NSF Science & Engineering Indicators Report 2024, governments and educational institutions are also paying closer attention to translational research, increasing market entry for new startups and academic spin-offs.

Growth of the paper diagnostics market is also driven by factors such as rising demand for point-of-care testing and the cost-effectiveness of paper for testing. Other factors driving the market are such as growing awareness about preventive care, decentralized healthcare models, and initiatives by various countries for the development of advanced paper diagnostics are also contributing to the growth of this market. Furthermore, the transition towards personalized diagnostics, the advances in reimbursement of the POC diagnostics (NIH Reimbursement Guide 2024), and the regulatory push for affordable solutions have increased the market acceptance globally.

In April 2024, Research published in the Journal of Intelligent Material Systems and Structures unveils biodegradable paper-based, ink jet-printed, and disposable microfluidic sensor systems for early cancer detection, developed at the Mayo Clinic.

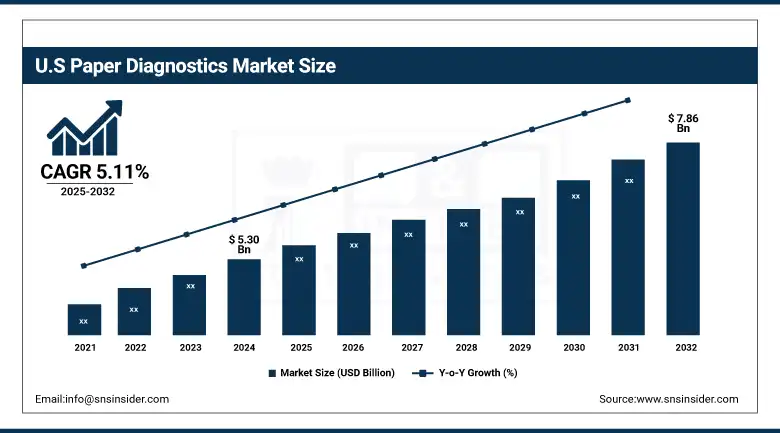

The U.S. paper diagnostics market size was valued at USD 5.30 billion in 2024 and is expected to reach USD 7.86 billion by 2032, growing at a CAGR of 5.11% over 2025-2032.

Paper Diagnostics Market Dynamics

Drivers:

-

Rising Demand for Affordable, Rapid, And Decentralized Diagnostic Solutions Across Both Clinical and Non-Clinical Settings

The growing burden of disease, in particular NCDs and outbreaks, has driven demand for efficient tools that can be scaled rapidly. With more than 60% of U.S. adults affected by one or more chronic diseases, there is an urgent need for regular and low-cost screening techniques. Paper-based approaches offer the advantages of being lightweight, easy to store and carry, requiring no electricity, and providing rapid results, making them appealing for adoption in rural and resource-limited settings. Increasing investments in point-of-care testing technologies are also supporting the market growth. For instance, more than USD 1.5 billion in COVID-19 diagnostic innovations, including paper-based tests, through the RADx initiative.

Additionally, the FDA’s Breakthrough Devices Program and revised guidelines (2020) for diagnostic reporting have accelerated approvals for novel diagnostic platforms. There is also increasing interest from the private sector in the market; venture capital investment in diagnostic start-ups grew by 14% in 2023, with a focus on low-cost, multiplex testing options. This jibes with the current sustainability zeitgeist, as paper diagnostics can cut down on the biomedical waste of plastic-heavy kits. This is poised to promote the continued growth of the long-term paper diagnostics market as digitization of healthcare, miniaturization, and public health continue to combine to boost the growth of the market over the forecast period.

Restraints:

-

Regulatory, Technical, and Scalability Limitations Hinder the Market Expansion

One of the biggest impediments is the absence of standardized validation guidelines for paper-based diagnostic devices, resulting in poor clinical performance and regulatory approval. The U.S. Food and Drug Administration (FDA) criteria for a diagnostic device rely heavily on sensitivity, specificity, and reproducibility, areas where paper-based platforms have been known to lose ground because of a lack of environmental control (i.e., humidity/temperature). Also, funding support from NIH SEED programs is limited to early-stage research, and there are bottlenecks in obtaining financing for large-scale commercialization. The scale-up of manufacturing is also a concern for paper-based diagnostics, where paper substrates must undergo rigorous quality control and make production more complex. More than one-third (30%) of paper-based diagnostic prototypes currently in use never make it into mass production owing to issues related to the reproducibility of assay performance, as demonstrated in the report of a 2023 study published in NPJ Diagnostics.

In addition, the lack of established reimbursement mechanisms, particularly in developing markets, weakens the commercial case for these tests. The absence of skilled manpower and ease of use interfaces in many complex formats is also a bottleneck for proliferation in underserved areas. Different regulations from organizations such as the FDA, EMA, and WHO Prequalification Program add a layer of complexity to worldwide deployment, leading to extended time-to-market. These challenges cumulatively limited the share of the paper diagnostics market share even though there is an increasing interest and R&D focus.

Paper Diagnostics Market Segmentation Analysis

By Kit Type

The global paper diagnostics market was dominated by the lateral flow assays in 2024 for its large market share of generating revenue, followed by the lateral flow assays for wide acceptance in rapid testing of infectious diseases, pregnancy testing, and cardiac markers. It is widely used because it is cheap, simple, and offers results in minutes, suitable for clinical and home applications. Paper-based microfluidics, on the other hand, will see the fastest growth, to be used in multiplexing, integration with smartphone-based readouts, and complex assays at low cost. Such devices are more and more considered for use in, e.g., cancer screening, metabolite monitoring, and biomarker screening, particularly in remote regions.

By Device Type

Diagnostic devices were the largest application in 2024 as a consequence of high usage in early disease diagnosis, especially for infectious and chronic diseases. The sector is also gaining from global initiatives to improve preventive health. Monitoring devices are projected to increase rapidly, as the health care industry booms and struggles to respond to real-time patient health data, a boon to people with chronic diseases and an aging population that needs to be constantly monitored at home.

By Application

Clinical diagnostics was the leading application in 2024 as it is instrumental in the diagnosis and management of various diseases, including infections and chronic illnesses. Its supremacy is even stimulated by the world demand for early diagnosis and point-of-care platforms. Environmental monitoring is also the largest and fastest-growing application market, reflecting the growing demand for low-cost, portable means to monitor pollution, pathogens, and toxins in water and soil, especially in developing countries.

By End-Use

The hospitals and clinics held the largest share of the market in 2024, owing to high patient inflow and availability of advanced diagnostic infrastructure and electronic medical record systems. These hospital laboratories continue to play a key role in comprehensive and emergency diagnostics. On the other hand, assisted living healthcare facilities are the most rapidly growing end-use segment, with the rise in the geriatric population and their growing need for simple, on-site diagnostic devices for age-related disorders. The home healthcare market is also witnessing significant potential growth with an increasing preference by patients towards at-home care, supported by paper diagnostics, for managing chronic disease and following up on post-acute care.

Paper Diagnostics Market Regional Insights

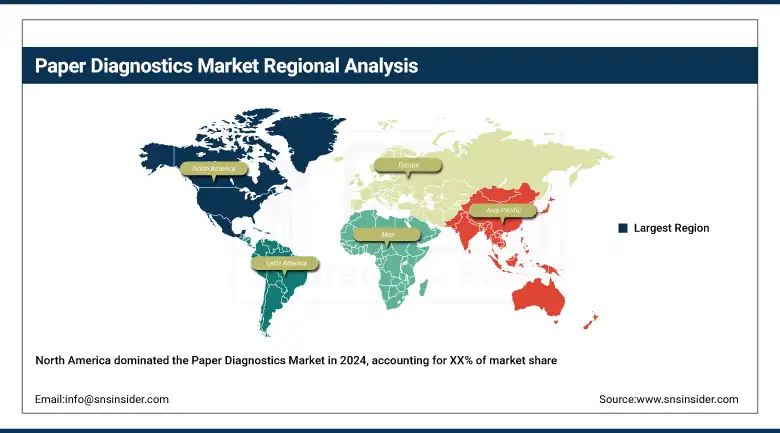

In 2024, North America held a dominant share of the global paper diagnostics market, owing to the presence of leading diagnostic companies, developed health care infrastructure, and a rise in the adoption of point-of-care technologies. The US has the largest market share due to strong R&D investment, supportive FDA regulations, and programs such as NIH’s RADx program, which committed more than USD 1.5 billion to diagnostic innovation. The area is also known for the high incidence of chronic and infectious diseases, which increases the need for home testing applications. Canada is driving the market growth with increasing digitization and upgradation of healthcare and national programs for early disease diagnosis. Mexico is developing as a growing market on account of enhanced access to primary care and growth in awareness of cost-effective diagnostics. The fastest-growing within the regional exploitation is Canada, followed by the USA, supported by the health government spending and R&D collaboration in diagnostics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe has a significant share in the paper diagnostics market owing to favorable government initiatives promoting preventive health and a focus on providing sustainable healthcare. Germany holds a strong position in the regional market due to the presence of a developed diagnostics sector, coupled with robust healthcare spending, which was valued at more than €460 billion in 2023. Increasing geriatric population and the prevalence of chronic diseases are also the very factors driving the use of paper-based diagnostic devices. Both the UK and France are making a substantial contribution. Through research investments and national programmes of screening. Poland comes out on top as the fastest-growing European country, fuelled by EU-funded research initiatives and growing interest in decentralized diagnostics in the countryside. Increasing demand for biodegradable disposable diagnostics formats is also contributing to regional growth. Support by public-private partnerships and organisations such as the European Commission to drive POC diagnostics is expected to further boost the regional landscape.

Among regions, Asia Pacific is projected to witness the fastest growth in the global market for paper diagnostics, supported by a huge population base, increasing disease burden, and a growing healthcare system. China is leading the market because of its strong manufacturing base, government-led healthcare reforms, and growing demand for low-cost diagnostics in rural areas. The country’s National Health Commission has been emphasizing early detection of disease, which has increased demand for fast diagnostic technologies. India is the second fastest growing market by pace, with support from the health initiatives, for instance, Ayushman Bharat, and incredible push towards local manufacturing, under the “Make in India” campaign. Public awareness and insurance coverage, and growing mobile health services, are also factors. Technological developments in Japan and South Korea are well developed, with a focus on investment in microfluidics & biosensor R&D. Such dynamics have made Asia Pacific ripe for innovative and scalable diagnostic solutions.

Key Companies in the Paper Diagnostics Market

Leading paper diagnostics companies operating in the market are Arkray Inc., Acon Laboratories Inc., Abbott (Alere Inc.), Bio-Rad Laboratories Inc., GVS S.p.A., Siemens Healthcare GmbH, Diagnostics For All Inc., FFEI Life Science (Biognostix), Navigene, and Micro Essential Laboratory Inc.

Recent Developments in the Paper Diagnostics Market

-

In March 2025, the ADDf’s Diagnostics Accelerator published a new paper exploring the ocular biomarker landscape, highlighting the potential of eye-based tests for early detection of Alzheimer’s disease, marking a significant advancement in non-invasive diagnostics.

-

In February 2025, BostonGene contributed to Friends of Cancer Research’s initiative aimed at improving clinical outcome endpoints through biomarker-driven insights, reinforcing the company’s role in advancing precision diagnostics and cancer care strategies.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 18.46 billion |

| Market Size by 2032 | USD 29.44 billion |

| CAGR | CAGR of 6.03% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Lateral Flow Assays, Dipstick, Paper-Based Microfluidics) By Device Type (Diagnostic Devices, Monitoring Devices) • By Application (Clinical Diagnostics (Cancer, Infectious Diseases, Liver Disorders, Others), Food Quality Testing, and Environmental Monitoring) • By End-Use (Home Healthcare, Assisted Living Healthcare Facilities, Hospital, and Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Arkray Inc., Acon Laboratories Inc., Abbott (Alere Inc.), Bio-Rad Laboratories Inc., GVS S.p.A., Siemens Healthcare GmbH, Diagnostics For All Inc., FFEI Life Science (Biognostix), Navigene, and Micro Essential Laboratory Inc. |

Frequently Asked Questions

Ans: North America dominated the Paper Diagnostics market.

Ans: Regulatory, technical, and scalability limitations hinder the market expansion.

Ans: Rising demand for affordable, rapid, and decentralized diagnostic solutions across both clinical and non-clinical settings.

Ans: The market is expected to reach USD 29.44 billion by 2032, increasing from USD 18.46 billion in 2024.

Ans: The Paper Diagnostics market is anticipated to grow at a CAGR of 6.03% from 2025 to 2032.

Get in Touch