Lateral Flow Assays Market Report Scope & Overview:

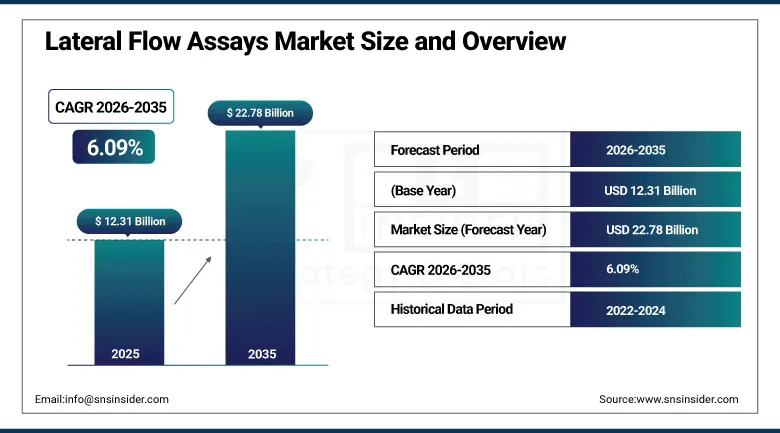

The Lateral Flow Assays Market was valued at USD 12.31 Billion in 2025 and is expected to reach USD 22.78 Billion by 2035, growing at a CAGR of 6.09% from 2026 to 2035.

The Lateral Flow Assays Market is growing owing to the increasing need for fast and portable tests at the point of care in terms of infectious diseases, pregnancy testing, and screening of chronic diseases. The increasing incidence rate of infectious diseases worldwide and the necessity of fast and easy-to-use testing tools are some key growth factors. Rising usage in food safety, veterinary diagnosis, and pharmaceutical industries will act as additional growth factors for this market. Advances in technology, which improve test sensitivity, multi-testing capacity, and digitization, are adding to the test accuracy.

According to the World Health Organization (WHO), infectious diseases remain among the leading global causes of mortality, with lower respiratory infections alone accounting for approximately 2.5 million deaths annually worldwide, highlighting the critical need for rapid diagnostic tools such as lateral flow assays. Furthermore, WHO data indicates that tuberculosis affected around 10.6 million people and caused approximately 1.3 million deaths in 2022, reinforcing its position as one of the most widely screened diseases using rapid antigen- and antibody-based diagnostic platforms, including lateral flow technologies.

Market Size and Forecast

-

Market Size in 2026E: USD 13.06 Billion

-

Market Size by 2035: USD 22.78 Billion

-

CAGR: 6.09% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Lateral Flow Assays Market - Request Free Sample Report

Lateral Flow Assays Market Trends

-

Rising demand for rapid point-of-care diagnostics driving widespread adoption of lateral flow assays in infectious disease detection and clinical testing

-

Growing integration of multiplex lateral flow technologies enabling simultaneous detection of multiple biomarkers from a single sample

-

Increasing use of digital readers and smartphone-based platforms enhancing result accuracy, connectivity, and remote diagnostic capabilities

-

Expanding applications in food safety, veterinary diagnostics, environmental monitoring, and drug testing supporting broader market adoption beyond healthcare

-

Continuous advancements in assay sensitivity, novel biomarkers, and nanotechnology-based detection methods improving the performance and reliability of lateral flow assays

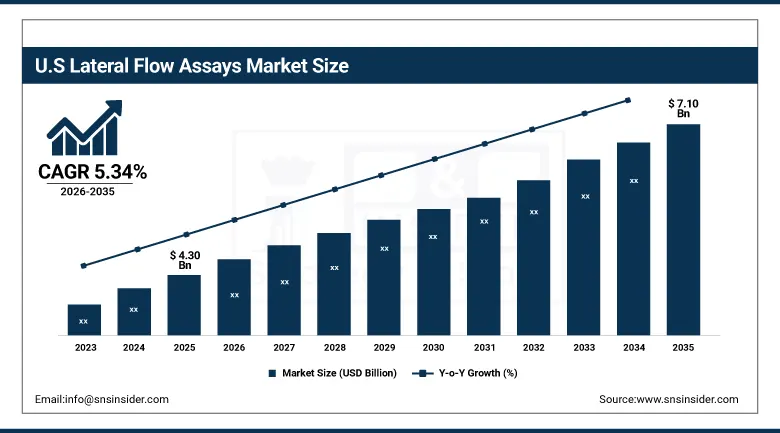

The U.S. Lateral Flow Assays Market Outlook

The U.S. Lateral Flow Assays Market was valued at approximately USD 4.30 Billion in 2025 and is expected to reach approximately USD 7.10 Billion by 2035, growing at a CAGR of approximately 5.34%.

The United States lateral flow assays market benefits from its position as the global epicentre of point-of-care diagnostic innovation, owing to the abundance of FDA emergency use authorization and 510(k) clearance processes that have made it possible to develop rapid diagnostic tests in infectious disease testing, cardiac and chronic diseases testing. This growing preference for home-based digital glucose meters, rapid coronavirus detection kits, rapid influenza diagnosis tests, and multi-disease rapid panels is anticipated to continue gaining momentum, as more Americans resort to self-testing for illness and chronic disease monitoring.

In November 2023, Becton Dickinson introduced a smartphone-integrated lateral flow reader in India, enabling digital result capture and teleconsultation linkage that connects point-of-care test results directly with remote clinical decision-making capability across India's expanding telemedicine infrastructure.

Lateral Flow Assays Market Segment Analysis

-

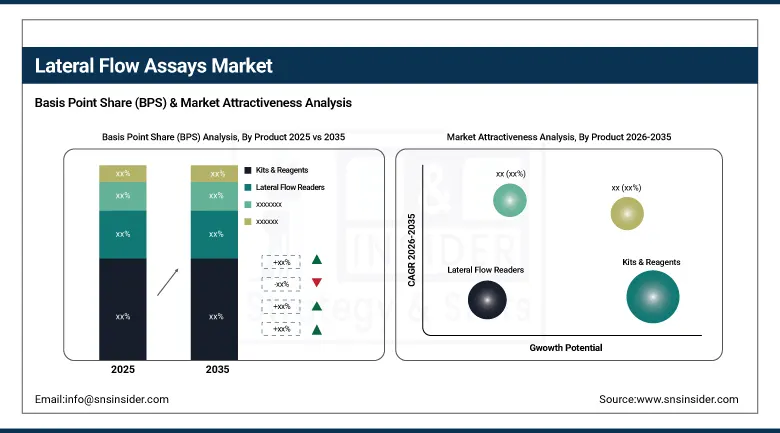

By Product, Kits & Reagents segment dominated the Lateral Flow Assays Market in 2025 with 79% share; Lateral Flow Readers segment is the fastest growing segment.

-

By Application, Clinical Testing segment dominated the market in 2025 with 58% share; Food Safety & Environment Testing segment is the fastest growing segment.

-

By Technique, Sandwich Assays segment dominated the market in 2025 with 63% share; Multiplex Detection Assays segment is the fastest growing segment.

-

By Therapy, Lateral Flow Immunoassay segment dominated the market in 2025 with 87% share; Nucleic Acid Lateral Flow Assay segment is the fastest growing segment.

-

By End-Use, Hospitals & Clinics segment dominated the market in 2025 with 41% share; Home Care segment is the fastest growing segment.

By Product, Kits & Reagents segment dominates the Lateral Flow Assays Market, Lateral Flow Readers segment expected to grow fastest

The Kits & Reagents segment dominated the Lateral Flow Assays Market owing to their frequent use in diagnostic testing, screening for diseases, and other point-of-care applications. The need for constant supply of test kits and reagents among healthcare professionals and labs has fueled continuous demand for these products. Their user-friendliness, fast results, affordability, and availability in diagnosing infections, pregnancy, and chronic diseases have further boosted the market share of this segment.

The Lateral Flow Readers segment is the fastest growing in the Lateral Flow Assays Market owing to rising demand for more precise, digital, and quantitative reading of test results. Lateral flow readers help in improving the sensitivity of the results, eliminating human errors, and recording data digitally. The growing integration with healthcare systems, increased usage of decentralized diagnostics, and point-of-care devices are boosting the demand for lateral flow readers.

By Application, Clinical Testing segment dominates the Lateral Flow Assays Market, Food Safety & Environment Testing segment expected to grow fastest

The Clinical Testing segment dominated the Lateral Flow Assays Market as lateral flow assays are widely used for the rapid detection of infections, pregnancies, cardiovascular disease and other medical conditions. The rapid results delivered by the assay coupled with their convenience and relatively low costs have contributed to their wide popularity. High patient test volumes, increasing access to healthcare services, and rising demand for point-of-care tests have further boosted their leading position in the market.

The Food Safety & Environment Testing segment is the fastest growing in the Lateral Flow Assays Market due to the rising significance of contamination monitoring, food safety, and environmental testing. The use of rapid testing procedures for detecting contaminants and other substances is being increasingly adopted by regulatory bodies and food producers. Public health awareness and stringent safety guidelines have been boosting the market growth.

By Technique, Sandwich Assays segment dominates the Lateral Flow Assays Market, Multiplex Detection Assays segment expected to grow fastest

The Sandwich Assays segment dominated the Lateral Flow Assays Market as this method provides good sensitivity and specificity for detection of proteins, pathogens, and large biomolecules. This assay is highly used for the purpose of diagnosis in the clinical diagnostics due to its effectiveness, easy procedure, and accurate results of the identification of small amount of the target substance.

The Multiplex Detection Assays segment is the fastest growing in the Lateral Flow Assays Market because this method allows detection of several biomarkers in one test. Such feature provides more efficient diagnostics, decreases the cost of testing and saves time on diagnosis process. The rising need of such tests, the development of technologies and high adoption in clinical, veterinary, and food testing are factors that drive the growth of this segment.

By Therapy, Lateral Flow Immunoassay segment dominates the Lateral Flow Assays Market, Nucleic Acid Lateral Flow Assay segment expected to grow fastest

The Lateral Flow Immunoassay segment dominated the Lateral Flow Assays Market owing to its wide application in the detection of infectious diseases, hormones, cardiac markers, and pregnancy markers. The assays provide simple-to-use technology with rapid results, high reliability, and low cost; hence, they are ideal for hospitals, clinics, and POC applications. Constant growth of diagnostic applications and worldwide acceptance has kept the segment in market leadership.

The Nucleic Acid Lateral Flow Assay segment is the fastest growing in the Lateral Flow Assays Market owing to increasing demand for high-sensitivity molecular tests that can detect genetic material more precisely. Increasing usage in infectious disease testing, antimicrobial resistance testing, and precision diagnostics is fueling the growth of the segment. Technical developments of incorporating nucleic acid amplification to lateral flow technology are also contributing towards wide-scale clinical adoption.

By End-Use, Hospitals & Clinics segment dominates the Lateral Flow Assays Market, Home Care segment expected to grow fastest

The Hospitals & Clinics segment dominated the Lateral Flow Assays Market owing to the huge amount of quick tests being performed in these centers for various infectious disease diagnosis, pregnancy test, cardiac disorders, and emergencies. The requirement of quick decisions along with efficient patient management and effective point-of-care testing has fueled adoption. The development of healthcare infrastructure along with constant integration of rapid diagnostics has also helped consolidate its dominance.

The Home Care segment is the fastest growing in the Lateral Flow Assays Market due to the rising preference for convenient and self-test diagnostic products away from healthcare facilities. Rising awareness regarding health monitoring, availability of easy-to-use testing kits at home, and rising demand for rapid diagnosis of various infections and chronic diseases are among the other factors behind the strong growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Lateral Flow Assays Market Insights

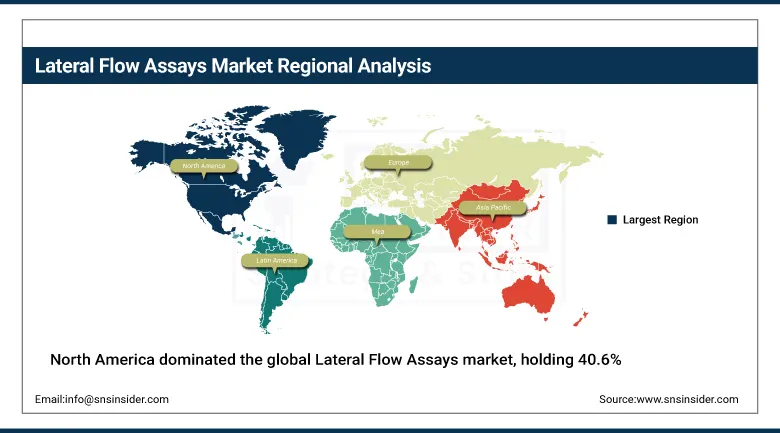

North America dominated the global Lateral Flow Assays market, holding 40.6% revenue share in 2025, driven by advanced healthcare infrastructure, strong over-the-counter testing adoption, and powerful industry presence from Abbott, Becton Dickinson, Quidel, and other established manufacturers.

The United States accounts for approximately 82.47% of regional revenue through its extensive home testing infrastructure, strong FDA emergency use authorisation framework that has accelerated rapid diagnostic test commercialisation, and the world's most extensive over-the-counter retail distribution network for consumer health products. Canada contributes supplementary demand through its universal healthcare system's point-of-care testing investment and growing home healthcare adoption whose trajectory parallels broader North American market development patterns.

The Centers for Disease Control and Prevention (CDC) reports that influenza alone causes approximately 9–41 million illnesses annually in the United States, significantly driving demand for rapid antigen testing technologies and point-of-care diagnostic solutions. Additionally, during the COVID-19 pandemic, the CDC highlighted the widespread deployment of rapid antigen tests, with hundreds of millions of tests used across the country, which substantially accelerated the adoption and acceptance of lateral flow technologies in both home-based and clinical diagnostic settings.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Lateral Flow Assays Market Insights

Europe held a significant share of global Lateral Flow Assays revenues, with the region's market expected to be worth substantially more by 2035 due to the wide-scale use of point-of-care testing, particularly in Western European healthcare settings. Germany, the United Kingdom, and France lead European national markets through their established healthcare infrastructure and comprehensive point-of-care testing protocols, while the European Union's IVDR regulatory framework's full implementation, despite earlier industry-driven delays, has created a more demanding but ultimately stabilising compliance environment that favours established lateral flow assay manufacturers with proven regulatory track records over smaller or less experienced market entrants.

The European Centre for Disease Prevention and Control (ECDC) reports that influenza causes millions of infections annually across Europe, necessitating continuous seasonal surveillance and widespread use of rapid diagnostic testing systems to monitor outbreaks and guide public health responses.

Asia Pacific Lateral Flow Assays Market Insights

Asia Pacific is the fastest-growing regional Lateral Flow Assays market, with growth reflecting rising healthcare spending, improved diagnostic capabilities, and government-backed genomic and infectious disease research across the region. China, India, and Japan are key growth engines due to expanding point-of-care testing infrastructure and increased awareness of personalised medicine, with China accounting for approximately 38.47% of Asia Pacific revenues through its growing R&D efforts and robust government interest in molecular diagnostics. India's expanding healthcare infrastructure investment and rapidly growing diagnostic laboratory network are creating accelerating lateral flow assay demand whose growth trajectory exceeds the regional average.

According to the World Health Organization (WHO), the Western Pacific and South-East Asia regions account for a substantial share of the global infectious disease burden, including high incidences of tuberculosis, dengue fever, and other communicable diseases, underscoring the need for scalable and rapid diagnostic solutions.

MEA & Latin America Lateral Flow Assays Market Insights

Middle East and Latin America are growing Lateral Flow Assays markets where expanding healthcare infrastructure, growing point-of-care testing awareness, and rising infectious disease surveillance investment are creating increasing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its world-class hospital infrastructure and growing investment in advanced diagnostic capability across its healthcare system. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large public hospital network, growing diagnostic laboratory sector, and increasing point-of-care testing adoption across both clinical and home care settings.

Market Dynamics

Drivers: Rising infectious and chronic diseases plus point-of-care testing shift drive strong market growth.

The growth of the lateral flow test kits market continues to be fuelled structurally as a result of the emergence of trends such as an increase in the incidence of infections and chronic diseases worldwide and the development of a trend towards decentralized, self-administrated point-of-care testing whose cost efficiency and convenience increasingly makes traditional diagnostic tests obsolete.

Structural growth in demand for lateral flow test kits is ensured as a result of increasing numbers of people affected by cardiovascular diseases, diabetes, and other chronic diseases, which require rapid detection of biomarkers, in addition to constant threats of outbreaks of infectious diseases, and a lateral flow-based capability to detect these outbreaks, which has been endorsed by the WHO and CDC for surveillance purposes.

Restraints: Regulatory fragmentation and accuracy limitations hinder global commercialization and market expansion.

US FDA, European Union's IVDR, and Health Canada all have different approaches for the fast track process for test approvals with different standards concerning validation, manufacture, and post-marketing surveillance which make the process difficult for manufacturers and prevent manufacturers from pursuing a simultaneous approach to launch their products into different markets. Low-income and middle-income countries do not have strong regulatory authorities, making the distribution of substandard and/or unvalidated lateral flow tests a possibility which is very risky because of the variable performance of these tests. At the same time, the Emergency Use Listing programme by the WHO's careful evaluation of diagnostics products, where all submitted products do not meet the minimum performance standards, speaks about real challenges for lateral flow assays manufacturers.

Opportunities: Multiplex assays and digital integration expand applications beyond single-analyte testing systems.

The invention of multiplex lateral flow tests which are capable of detecting more than one pathogen or biomarker at a time within a single test strip is a noteworthy scientific advance whose commercial significance is in the provision of diagnostic information that is greater compared to the increased cost of conducting the test. Paper chips which compartmentalize radially and use smartphone readers to detect several genes within ten minutes constitute an example of the technological path which is increasing the information density of lateral flow tests to molecular class levels previously attainable only in laboratories, thus presenting a huge commercial potential to the manufacturers of such products.

Recent Developments:

-

2024: SENSIStrip launched its Gluten PowerLine Lateral Flow Device, offering a highly sensitive monoclonal antibody-based test for detecting gluten residues in food matrices with hook line technology that prevents false negatives in highly contaminated samples.

-

2024: Bio-Rad Laboratories launched a new line of veterinary lateral flow assays for bovine diseases in collaboration with Thai agricultural authorities, expanding lateral flow technology's veterinary diagnostics application in Southeast Asian livestock health surveillance programmes.

-

2023: Becton Dickinson introduced a smartphone-integrated lateral flow reader in India, enabling digital result capture and teleconsultation linkage that connects point-of-care test results with remote clinical decision-making across India's growing telemedicine infrastructure.

Lateral Flow Assays Market Key Players are:

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd.

-

Becton, Dickinson and Company

-

Thermo Fisher Scientific Inc.

-

Danaher Corporation

-

bioMerieux SA

-

Quidel Corporation (QuidelOrtho)

-

Bio-Rad Laboratories Inc.

-

Hologic Inc.

-

PerkinElmer Inc.

-

Bioeasy Biotechnology Inc.

-

OPERON S.A.

-

Eurofins Technologies

-

Cambridge Molecular Diagnostics Limited

-

Inflammatix Inc.

-

EDX Medical Group PLC

-

SD Biosensor Inc.

-

Siemens Healthineers AG

-

Orasure Technologies Inc.

-

Chembio Diagnostics Inc.

Lateral Flow Assays Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.31 Billion |

| Market Size by 2035 | USD 22.78 Billion |

| CAGR | CAGR of 6.09% from 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Kits & Reagents, Lateral Flow Readers) • By Application (Clinical Testing, Veterinary Diagnostics, Food Safety & Environment Testing, Drug Development & Quality Testing) • By Technique (Sandwich Assays, Competitive Assays, Multiplex Detection Assays) • By Therapy (Lateral Flow Immunoassay, Nucleic Acid Lateral Flow Assay) • By End-Use (Hospitals & Clinics, Diagnostic Laboratories, Home Care, Pharmaceutical & Biotechnology Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, F Hoffmann-La Roche Ltd, Danaher Corporation, Thermo Fisher Scientific Inc, QIAGEN N.V., Becton, Dickinson and Company, Siemens Healthineers AG, Bio-Rad Laboratories, Inc, bioMérieux SA, QuidelOrtho Corporation, PerkinElmer, Inc, Merck KGaA (MilliporeSigma), Trinity Biotech plc, ACON Laboratories, Inc, OraSure Technologies, Inc, Chembio Diagnostics, Inc, Abingdon Health plc, DCN Dx, NG Biotech, LumiraDx Limited |

Frequently Asked Questions

The Lateral Flow Assays Market was valued at USD 12.31 Billion in 2025.

North America dominated the Lateral Flow Assays Market in 2025.

The kits & reagents segment dominated the Lateral Flow Assays Market.

Rising disease burden, point-of-care shift, digital innovation, drug monitoring demand, and government-supported rapid diagnostics drive lateral flow assays market growth.

The Lateral Flow Assays Market is expected to grow at a CAGR of 6.09% from 2026 to 2035.

Get in Touch