Peptide Synthesis Market Report Scope & Overview:

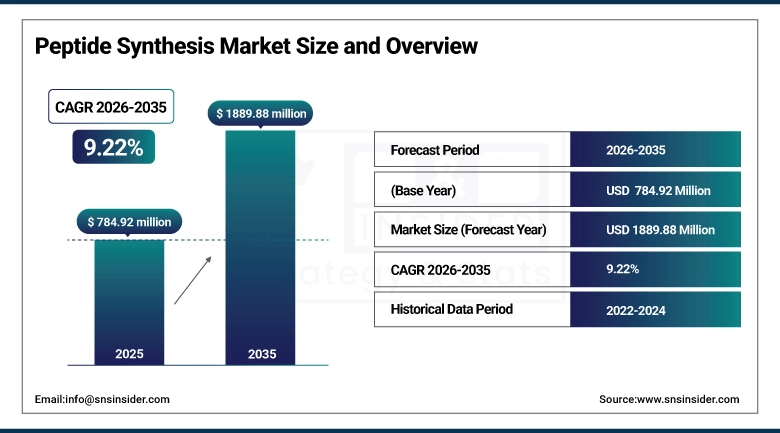

The Peptide Synthesis Market was estimated at USD 784.92 Million in 2025 and is expected to reach USD 1,889.88 Million by 2035, growing at a CAGR of 9.22% over the forecast period of 2026-2035.

The Peptide Synthesis Market encompasses the global industry ecosystem dedicated to the production, supply, and application of synthetic peptides—short chains of amino acids produced through chemical or biotechnological synthesis processes—for use across pharmaceutical drug development and manufacturing, in vitro diagnostics, biological research, and emerging cosmetic active ingredient applications. The market covers the full value chain from raw chemical reagents including amino acid building blocks, coupling reagents, resins, protecting groups, and deprotection agents through automated synthesis equipment such as peptide synthesizers, preparative HPLC purification systems, and lyophilizers, to the contract synthesis services provided by specialized CDMOs and CROs that manufacture custom and GMP-grade peptide active pharmaceutical ingredients for clinical and commercial use.

The global pipeline of peptide-based therapeutics in clinical development is among the most robust in the biopharmaceutical industry, with more than 630 active clinical trials involving peptide candidates as of early 2025, encompassing 80+ already-approved peptide drugs across multiple therapeutic categories that collectively generate over USD 50 billion in annual pharmaceutical revenues and create continuous upstream demand for peptide synthesis raw materials and services.

Market Size and Forecast:

-

Market Size in 2025: USD 784.92 Million

-

Market Size by 2035: USD 1,889.88 Million

-

CAGR: 9.22% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Peptide Synthesis Market - Request Free Sample Report

Peptide Synthesis Market Trends:

- Explosive commercial and pipeline demand for GLP-1 receptor agonist peptide therapies for obesity and type 2 diabetes, led by semaglutide and tirzepatide, is driving unprecedented CDMO capacity expansion investments across Bachem, PolyPeptide Group, and CordenPharma that are reshaping the competitive landscape and supply chain architecture of the global peptide synthesis market.

- Growing adoption of automated, high-throughput peptide synthesizers incorporating microwave-assisted and flow chemistry technologies is dramatically reducing synthesis cycle times and improving yield efficiency for complex therapeutic peptide sequences, enabling pharmaceutical companies and CDMOs to scale production capacity while maintaining GMP quality standards at reduced per-unit manufacturing costs.

- Accelerating integration of artificial intelligence and machine learning into peptide drug discovery is enabling the systematic optimization of peptide sequences for target binding affinity, oral bioavailability, metabolic stability, and reduced immunogenicity, expanding the chemical space accessible to peptide drug development and generating new categories of complex modified peptides that require advanced synthesis capabilities.

- Expanding application of synthetic peptides in precision oncology as neoantigen vaccine components for personalized cancer immunotherapy is creating a new high-value market segment for custom peptide synthesis services that require rapid turnaround, extreme sequence accuracy, and patient-specific GMP manufacturing capabilities from specialized CDMO partners.

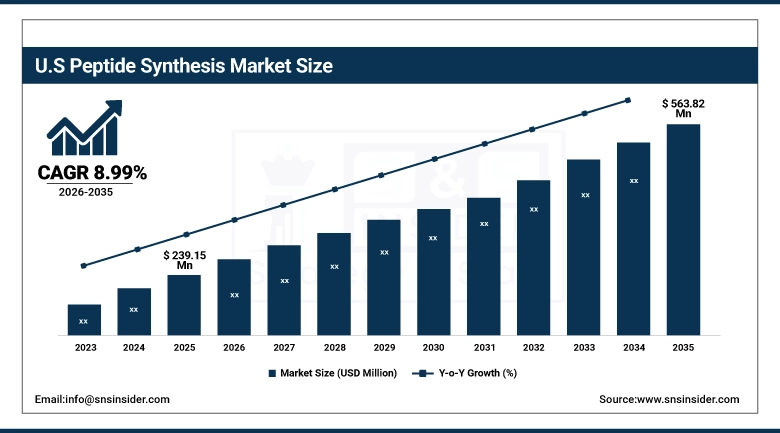

U.S. Peptide Synthesis Market was valued at USD 239.15 Million in 2025 and is expected to reach USD 563.82 Million by 2035, growing at a CAGR of 8.99%.

The U.S. stands out as the single largest country-level market for peptide synthesis globally due to the concentration of pharmaceutical and biotech firms investing in peptides in drugs, a well-established ecosystem of peptide synthesis CDMOs and CROs such as Bachem US Inc., AmbioPharm, and AAPPTec, and leading providers of peptide synthesis instruments including CEM Corporation and CSBio who have set global benchmarks for synthesis technology through automation. The phenomenal success achieved by GLP-1 receptor agonist peptide drugs like semaglutide from Novo Nordisk and tirzepatide from Eli Lilly in generating multi-billion-dollar revenues in the U.S. market has led to high upstream demand for peptide synthesis which has triggered substantial investments being made in both domestic and offshore expansions of CDMOs. The stringent quality assurance measures required in the process of manufacture of peptide API per the FDA guidelines on peptides in compliance with ICH Q11 and 21 CFR part 211 creates a strong demand for state-of-the-art synthesis instruments and QA services from suppliers based in the U.S. On June 2025, the FDA granted approval for liraglutide for treating type 2 diabetes in children thereby opening up a new market segment for GLP-1 peptide drugs.

Peptide Synthesis Market Segment Insights:

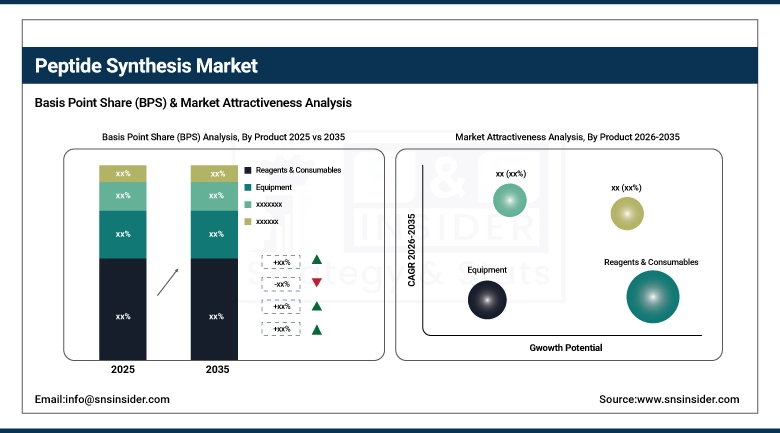

- By Product, Reagents & Consumables dominated with approximately 46.29% revenue share in 2025; Equipment is expected to be the fastest-growing product segment driven by accelerating adoption of automated synthesizers and next-generation purification systems.

- By Technology, Liquid-Phase Peptide Synthesis (LPPS) held the largest market share in 2025 at approximately 46.2%; Hybrid & Recombinant methods are expected to be the fastest-growing technology segment during the forecast period.

- By Application, Therapeutics dominated with the largest revenue share in 2025; Diagnostics is expected to register the fastest CAGR of 10.21% during the forecast period.

- By End-User, Pharmaceutical & Biotechnology Companies led with the largest end-user revenue share in 2025; CDMOs/CROs segment is growing at significant pace driven by outsourcing trends.

Peptide Synthesis Market Segment Analysis:

By Product: Reagents & Consumables dominate, Equipment fastest-growing

The Reagents & Consumables segment accounted for around 46.29% of the Peptide Synthesis Market in 2025, due to its core importance in providing continuous consumption inputs necessary for every cycle of peptide synthesis irrespective of the type of technology platform utilized, scale of production, or therapeutic purpose. It includes raw materials like amino acid residues, protected amino acids, coupling reagents such as HBTU, HATU, and DIC, deprotection reagents, cleavage cocktail constituents, resins like Wang, Rink amide, and specialized linker resins, and analytical standards used during both research and manufacturing synthesis processes. Due to their high usage rate and repetitive nature, reagents & consumables make up the largest and most reliable market segment, since their sales directly depend on the volumes of synthesis operations. Key players such as Merck KGaA Sigma-Aldrich business unit, Thermo Fisher Scientific, and Bachem are advantaged by existing client relationships, regulatory master file submissions, and economies of scale in logistics, which form significant competitive barriers in this segment.

Equipment market segment is expected to exhibit highest CAGR growth rate throughout the forecast period, attributed to the increasing investments in automated peptide synthesizers, preparative HPLC purification systems, and lyophilization systems made by both pharma companies investing heavily in developing their own peptide synthesis capabilities, as well as CDMOs ramping up their capacities to meet rising peptide APIs demand. Transition from manual synthesis process conducted on batch-wise basis to fully automated and high throughput peptide synthesizers that can run parallel synthesis processes in hundreds at one time is leading to substantial equipment investments.

By Technology: LPPS dominates, Hybrid & Recombinant fastest-growing

Liquid-Phase Peptide Synthesis (LPPS) held the largest technology segment share in 2025 at approximately 46.2%, reflecting the technology established dominance in large-scale commercial manufacturing of short-to-medium length therapeutic peptides where its advantages in scalability, cost-effectiveness for bulk production, and compatibility with existing pharmaceutical manufacturing infrastructure create compelling commercial justification for its continued deployment. LPPS is particularly well-suited for the manufacturing of commercially mature peptide APIs produced at multi-kilogram to multi-ton scales, including insulin analogs, GLP-1 agonists, and other high-volume metabolic disease peptide therapeutics where manufacturing cost optimization is a primary competitive differentiator among CDMO suppliers.

Hybrid & recombinant methods are expected to be the fastest-growing technology segment during the forecast period owing to their ability to combine the advantages of chemical synthesis and biological production techniques for manufacturing complex and long-chain peptides with higher efficiency and scalability. These technologies enable improved yield, reduced production costs, and enhanced purity compared to conventional synthesis approaches, making them highly suitable for next-generation peptide therapeutics. The growing demand for peptide-based drugs in oncology, metabolic disorders, and rare disease treatment, along with increasing investments in biologics and personalized medicine, is further accelerating segment growth. In addition, advancements in recombinant DNA technology, continuous-flow synthesis, and automated peptide manufacturing platforms are supporting wider adoption of hybrid peptide synthesis methods across pharmaceutical and biotechnology companies.

By Application: Therapeutics dominates, Diagnostics fastest-growing

Therapeutics held the largest application segment share in 2025, driven by the extraordinary expansion of the global peptide drug market across oncology, metabolic disease, infectious disease, cardiovascular disorders, and rare genetic conditions. The therapeutic applications segment encompasses the synthesis of peptide APIs for both approved commercial peptide drugs and the large and growing pipeline of investigational peptide drug candidates spanning more than 630 active clinical trials as of early 2025. The segment dominance reflects both the established commercial revenue from mature peptide drug classes including insulin analogs, GLP-1 agonists, somatostatin analogs, and antimicrobial peptides, and the substantial growth contribution from the emerging wave of novel peptide therapeutics including neoantigen cancer vaccines, cell-penetrating peptide delivery systems, and bicyclic peptide precision oncology agents.

The Diagnostics segment is expected to register the fastest CAGR of approximately 10.21% during the forecast period, driven by expanding use of synthetic peptides as diagnostic biomarker assay components, immunoassay calibrators and controls, mass spectrometry internal standards for quantitative clinical proteomics, and as antigens for antibody detection assays across infectious disease, autoimmune disorder, and cancer biomarker testing applications.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~81% |

|

Europe |

Germany |

~31% |

|

Asia Pacific |

China |

~44% |

|

Middle East & Africa |

UAE |

~26% |

|

Latin America |

Brazil |

~41% |

North America Peptide Synthesis Market Insights

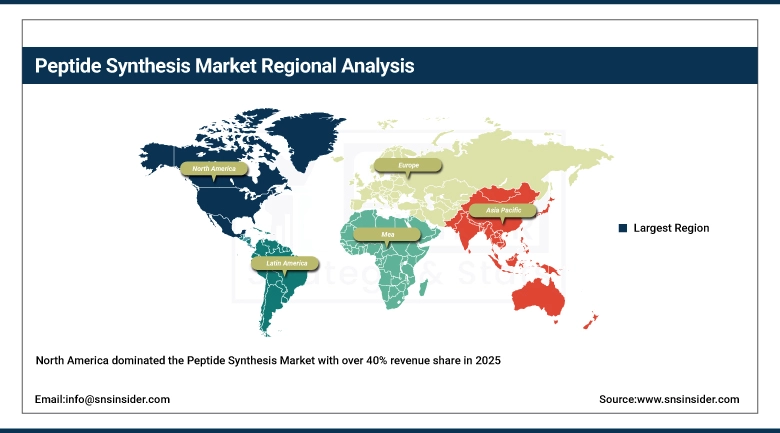

North America dominated the Peptide Synthesis Market with over 40% revenue share in 2025, anchored by the United States; unparalleled concentration of pharmaceutical and biotechnology companies investing in peptide-based drug development, a mature and technically advanced network of CDMOs and CROs providing custom synthesis and GMP manufacturing services, and the world leading concentration of peptide synthesis equipment manufacturers and reagent suppliers. The U.S. FDA well-established regulatory pathway for peptide APIs and the country robust funding environment for biomedical research and biopharmaceutical development sustain continuous investment in peptide synthesis capabilities across both commercial and academic settings. The extraordinary commercial success of GLP-1 peptide therapeutics in the U.S. obesity and diabetes market has created unprecedented upstream demand for CDMO manufacturing capacity that is driving capital investment across the peptide synthesis supply chain.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Peptide Synthesis Market Insights

Europe represents a major and technically advanced peptide synthesis market, characterized by the presence of the world leading specialized peptide CDMO companies including Bachem Holding AG in Switzerland and Bubendorf, PolyPeptide Group across multiple European sites, and CordenPharma International in Switzerland and Germany. Switzerland functions as the global center of gravity for peptide manufacturing expertise and capacity, with Bachem and CordenPharma collectively representing the largest concentration of pharmaceutical-grade peptide synthesis infrastructure in the world. Germany is the largest national market within the broader European geography, supported by Merck KGaA Sigma-Aldrich reagent division, a sophisticated chemical manufacturing base, and deep academic-industry partnerships in peptide chemistry and drug development.

Asia Pacific Peptide Synthesis Market Insights

Asia Pacific is the fastest-growing regional Peptide Synthesis Market, expected to grow at a CAGR of 9.87% during the forecast period, driven by the rapid expansion of pharmaceutical and biotechnology sectors in China, India, South Korea, and Japan. China represents the largest national market within Asia Pacific, underpinned by government-backed initiatives to expand domestic pharmaceutical manufacturing capabilities, a large and growing network of CDMOs providing peptide synthesis services including GenScript Biotech Corporation and the expanded WuXi AppTec peptide manufacturing facilities in Changzhou and Taixing that collectively added over 32,000 liters of solid-phase synthesis reactor capacity in early 2024. India is the fastest-growing national market, supported by the country expanding CDMO sector, government pharmaceutical manufacturing incentive programs, and the cost-competitive synthesis capabilities of companies including Syngene International that serve global pharmaceutical clients.

Latin America & Middle East and Africa Peptide Synthesis Market Insights

Latin America and the Middle East & Africa represent nascent but growing Peptide Synthesis Markets where pharmaceutical industry development, growing healthcare infrastructure investment, and increasing domestic demand for peptide-based therapeutics are beginning to generate market presence. Brazil is the dominant national market within Latin America, driven by its large pharmaceutical manufacturing sector and the Fiocruz government research institution investment in peptide-based vaccine and therapeutic research programs. Mexico and Argentina contribute secondary markets supported by pharmaceutical API manufacturing activities. The Middle East & Africa region is primarily driven by research and development activity in academic and government research institutions in Saudi Arabia, Egypt, and South Africa, where peptide synthesis capabilities are being established to support domestic pharmaceutical R&D programs and reduce dependency on international API supply chains.

Market Dynamics:

Growth Drivers: Surging global demand for peptide-based therapeutics in oncology and metabolic disease and unprecedented GLP-1 agonist commercial success driving CDMO capacity expansion and synthesis technology investment

The primary structural growth driver for the Peptide Synthesis Market is the extraordinary commercial and clinical success of peptide-based therapeutics that has established synthetic peptides as one of the pharmaceutical industry most productive drug modality classes. The global GLP-1 receptor agonist market, encompassing semaglutide and tirzepatide for obesity and type 2 diabetes, generated over USD 50 billion in combined annual revenues in 2024 and is projected to continue growing at exceptional rates through the forecast period, creating continuous upstream demand for peptide API manufacturing capacity that is compelling CDMOs including Bachem, PolyPeptide Group, and CordenPharma to invest billions of dollars in synthesis capacity expansion. Beyond GLP-1 therapeutics, the oncology peptide pipeline including neoantigen cancer vaccines, peptide-drug conjugates, and peptide receptor radionuclide therapy agents are generating new categories of complex synthesis demand.

Restraints: High synthesis and purification costs, peptide stability and bioavailability limitations, complex regulatory requirements, and technical expertise scarcity constraining market expansion

The Peptide Synthesis Market faces several structural constraints that moderate growth rates below the technology full potential. The high per-unit cost of GMP-grade peptide synthesis and purification, arising from expensive protected amino acid building blocks, reagent consumption, preparative HPLC purification requirements, lyophilization, and extensive analytical testing, creates significant price barriers for peptide-based drug development compared to small molecule alternatives, particularly for early-stage programs where synthesis cost uncertainty adds to development risk. The inherent metabolic instability of many peptide sequences through proteolytic degradation, short plasma half-lives, and poor oral bioavailability requirements that necessitate subcutaneous or intravenous administration routes creates formulation and delivery challenges that add development complexity and cost. The shortage of highly trained peptide chemists and synthesis specialists with expertise in GMP manufacturing, analytical characterization, and regulatory affairs creates capacity constraints that limit the rate of market expansion.

Opportunities: Oral peptide drug development, neoantigen personalized cancer vaccine synthesis, AI-driven peptide design, and emerging market CDMO capacity creation opening substantial growth avenues

The Peptide Synthesis Market presents compelling growth opportunities across multiple strategic dimensions. The development of oral peptide drug delivery technologies using conjugation, cyclization, lipophilic modification, and non-natural amino acid incorporation strategies to overcome bioavailability limitations represents a transformative opportunity that would expand the addressable patient population for peptide therapeutics far beyond current injectable administration constraints, requiring synthesis capabilities for structurally complex modified peptides at scales currently unanticipated in commercial planning. The emerging neoantigen personalized cancer vaccine market, where patient-specific tumor mutation-derived peptide antigens must be synthesized under GMP conditions within weeks of tumor sequencing, represents a high-value and technically demanding new application domain for specialized peptide synthesis CDMOs. The integration of AI-driven peptide design platforms with automated synthesis and analytical characterization workflows creates opportunities for dramatic acceleration of peptide drug discovery timelines, expanding the range of biological targets addressable through peptide therapeutics and generating new categories of novel peptide compounds requiring synthesis development.

Recent Developments:

-

May 2025: Bachem Holding AG announced significant capital investments to expand production capacities across its global network including facilities in Bubendorf (Switzerland), Vista (California, USA), and St Helens (UK), in response to escalating pharmaceutical demand for peptide-based API manufacturing services, reinforcing Bachem position as the world leading specialized peptide CDMO.

-

August 2025: Vapourtec Ltd launched the Peptide-Builder, a compact benchtop flow chemistry peptide synthesizer, and Gyros Protein Technologies (now part of Biotage) introduced the PurePep Sonata+, a next-generation automated synthesizer offering improved speed, accuracy, and operational efficiency over previous platforms, reflecting the continuing innovation momentum in synthesis equipment technology.

Peptide Synthesis Market Key Players:

-

Bachem Holding AG

-

Thermo Fisher Scientific Inc.

-

Merck KGaA (Sigma-Aldrich)

-

GenScript Biotech Corporation

-

CEM Corporation

-

Biotage AB

-

PolyPeptide Group AG

-

Syngene International Limited

-

CordenPharma International

-

Lonza Group AG

-

AAPPTec LLC

-

CPC Scientific Inc.

-

Novo Nordisk A/S

-

AmbioPharm Inc.

-

Gyros Protein Technologies AB

-

Kaneka Corporation

-

Creative Diagnostics

-

AnaSpec Inc.

-

CSBio Company Inc.

-

Advanced ChemTech

Peptide Synthesis Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 784.92 Million |

| Market Size by 2035 | USD 1,889.88 Million |

| CAGR | CAGR of 9.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Reagents & Consumables, Equipment, Others) • By Technology (Solid-Phase Peptide Synthesis (SPPS), Liquid-Phase Peptide Synthesis (LPPS), Hybrid & Recombinant Methods) • By Application (Therapeutics, Diagnostics, Research, Cosmetics, Others) • By End-User (Pharmaceutical & Biotechnology Companies, CDMOs/CROs, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Bachem Holding AG, Thermo Fisher Scientific Inc., Merck KGaA (Sigma-Aldrich), GenScript Biotech Corporation, CEM Corporation, Biotage AB, PolyPeptide Group AG, Syngene International Limited, CordenPharma International, Lonza Group AG, AAPPTec LLC, CPC Scientific Inc., Novo Nordisk A/S, AmbioPharm Inc., Gyros Protein Technologies AB, Kaneka Corporation, Creative Diagnostics, AnaSpec Inc., CSBio Company Inc., and Advanced ChemTech |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 9.87% during the forecast period, driven by China expanding CDMO sector, India government-backed pharmaceutical manufacturing initiatives, and the growing domestic biotechnology industries of South Korea and Japan.

North America dominated the Peptide Synthesis Market with over 40% revenue share in 2025, led by the United States with its unparalleled concentration of pharmaceutical and biotechnology companies, mature CDMO network, and leading-edge synthesis equipment and reagent manufacturers.

Liquid-Phase Peptide Synthesis (LPPS) dominated the technology segment with approximately 46.2% market share in 2025, driven by its established advantages in large-scale commercial manufacturing of short-to-medium length peptide APIs including GLP-1 agonists and insulin analogs.

Reagents & Consumables dominated with approximately 46.29% revenue share in 2025, driven by their foundational role as continuous-consumption inputs required for every peptide synthesis cycle across research, development, and commercial manufacturing workflows.

The Peptide Synthesis Market was valued at USD 784.92 million in 2025.

The Peptide Synthesis Market is expected to grow at a CAGR of 9.22% from 2026 to 2035.

Get in Touch