Cell Reprogramming Market Report Scope And Overview:

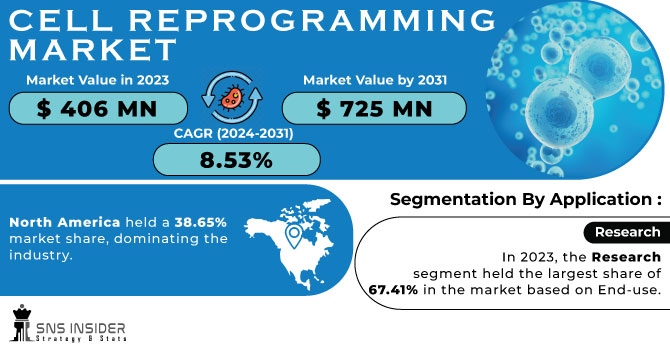

The Cell Reprogramming Market size was valued at US$ 406 million in 2023 and is projected to reach over US$ 725 million by 2031 with an increasing CAGR of 8.53% during the forecast period 2024-2031.

The human cell-based models, which have undergone reprogramming, demonstrate temporal dynamics akin to the processes involved in brain development. Therefore, using cellular models created from reprogrammed human cells could help to reduce the need for animal testing in lab settings and accelerate the development of neuropathy treatments.

Get More Information on Cell Reprogramming Market - Request Sample Report

In addition, corporations are pursuing diverse business endeavours, like joint ventures and alliances, with the aim of promoting the process of cell reprogramming. For example, in January 2023, bit.bio and Automata, a life sciences-focused robotics and automation company, announced a partnership to automate a crucial step in the production process of Automata's iPSC-derived human cell products.

The market for cell reprogramming is expanding steadily and is anticipated to do so throughout the forecast period as a result of numerous successful studies and developments in the cell reprogramming field. The End-use segment's drug development is anticipated to generate the majority of revenue over the projection period thanks to technological advancements and successful clinical trials.

MARKET DYNAMICS

DRIVERS

-

Growing interest of scientists and researchers in the field of human cell development and innovations.

The primary driver of the global market for cellular reprogramming tools is the growing interest of scientists and researchers in the field of human cell development and innovations. Moreover, growing industry focus on cellular reprogramming and related research, rising government funding, and rising public awareness of stem cell and cellular reprogramming tools will all help to propel the market during the forecast period. Additionally, expanding research outsourcing and medical tourism will help to propel the market forward. Over the projection period, however, the market growth for cellular reprogramming tools will be hampered by high costs associated with these kinds of research and increased bureaucratic restrictions.

RESTRAINT

-

Inefficiency of cell reprogramming and differences in gene expression profiling

Significant barriers to the market's expansion include the inefficiency of cell reprogramming and differences in gene expression profiling. The significant financial outlay and expenses associated with stem cell research and development initiatives are another important aspect that is anticipated to impede the market's expansion during the forecast period. In addition, a shortage of skilled labour is another issue impeding market expansion.

OPPORTUNITY

-

Regenerative medicine holds great promise for the End-use of cellular reprogramming techniques.

Tools for cellular reprogramming hold great promise for the field of regenerative medicine. The tools for cellular reprogramming have the capacity and potential to create different kinds of human cells, including liver, heart, brain, and pancreatic cells. For research and translational purposes, the cellular reprogramming tools provide a selection of integration-free reprogramming technologies and services. It is possible to tailor these cells to the patient's genetic composition. It is effective and proven that cellular reprogramming tools can rejuvenate old cells. Additionally, tools for cellular reprogramming aid in the early understanding of human development, providing a chance to increase the number of transplantable, rejection-proof cells and tissues.

-

Technological advancement

Technological developments and ongoing research and development efforts related to cell reprogramming are anticipated to present new growth opportunities for the market over the course of the forecast period. Additionally, it is anticipated that the pharmaceutical industry will utilize the iPSC approach extensively to produce effective cell sources, such as functional cells derived from iPSC to facilitate drug screening and toxicity assessment. This will raise demand for cell reprogramming technology. Over the course of the forecast period, the market is anticipated to witness new growth opportunities as a result of the influx of new players with advanced technologies looking to capitalise on unexplored opportunities in the industry and meet the growing demand.

CHALLENGES

-

Use of various cellular reprogramming tools

The use of various cellular reprogramming tools is accompanied by a high degree of bureaucratic restrictions. Additionally, strict regulatory requirements and the high cost of sophisticated equipment used in stem cell research are anticipated to significantly impede the market's growth over the course of the forecast period.

IMPACT OF RUSSIA-UKRAINE WAR

Global food and fuel insecurity, increased suffering and death in the nation, and a decrease in donor funding for other health-related concerns are all results of Russia's war in Ukraine.

A chain of tragic events has been triggered by Russia's invasion of Ukraine. The most vulnerable citizens of Russia will suffer directly from economic sanctions, which include a reduction in pharmaceutical imports. The long-term effects of population displacement both within and across national borders, the destruction of healthcare facilities, the displacement of healthcare workers, and the harm to healthcare logistics will be grave for Ukraine and won't be lessened until the conflict is resolved and the country's healthcare system is rebuilt.

IMPACT OF ECONOMIC DOWNTURNS

A recession is more likely to affect healthcare providers, which will force them to bargain for higher contract prices. Payers will need to look into ways to counteract any increases in prices. This may result in a rise in the outsourcing and offshoring of conventional procedures, like claims and provider management, in order to guarantee reduced administrative costs and improved operational effectiveness.

Members who are concerned about costs might switch to higher deductible plans and forego care, especially preventive services, which would result in decreased utilization. Long-term effects may result from this, especially for family members who have several chronic illnesses. Payers should identify vulnerable individuals, make investments in fields like social determinants of health (SDoH), and develop plans that avoid care gaps and discontinuities in order to counteract this.

With robust financial backing, a number of payers can launch digital transformation projects to replace antiquated systems and transition to interoperable, linked ecosystems that will enhance both administrative and clinical results. This may, however, only apply to payers who see lower payouts and lower utilisation as a result of the downturn.

Government Initiative

-

Through a number of Departments and Institutions, including the Indian Council of Medical Research (ICMR), the Department of Biotechnology (DBT), and the Department of Science and Technology (DST), the Indian government has supported basic and clinical stem cell research.

-

The Government has notified the New Drugs and Clinical Trial Rules, and presented in Lok Sabha (India) in 2022 for regulation of clinical trials and New Drugs including cell & stem cell derived product, gene therapeutics product and xenografts for human use, which contains various provisions for improving transparency and accountability for the approval process and to promote research and development of the new drugs.

KEY MARKET SEGMENTATION

By Technology

-

Sendai Virus-based Reprogramming

-

mRNA Reprogramming

-

Episomal Reprogramming

-

Other

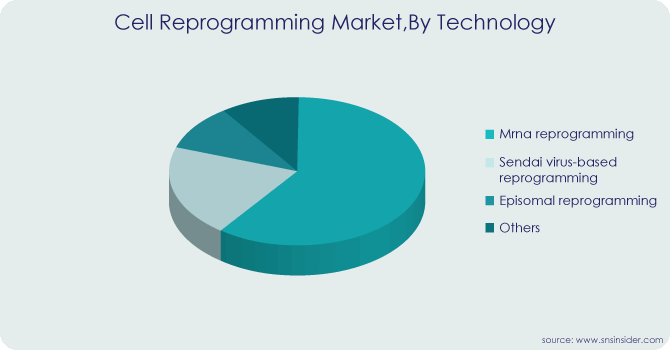

With a share of 32.67% in 2023, the mRNA reprogramming technology segment held the largest share. Using somatic tissue, clinical-grade human iPS cells can be generated quickly, safely, and effectively thanks to developments in the mRNA reprogramming technique. It seems that mRNA-based reprogramming is the only nonviral, non-integrating method available for creating efficient, safe, and therapeutically relevant human iPS cell lines. This method is therefore widely considered to be the most effective and approAs a result; this will spur further market expansion and raise demand for mRNA reprogramming. From 2024 to 2030, the sendai virus-based reprogramming market is anticipated to expand at a noteworthy compound annual growth rate of 8.59%. The End-use of the Sendai viral vector in cell engineering, regenerative medicine, and cell therapy shows great promise.

By Application

-

Research

-

Therapeutic

In 2023, the research segment held the largest share of 67.41% in the market based on End-use. The quickest and most effective method for creating cell cultures from patient tissue samples is cell reprogramming. This makes it possible for researchers to determine whether cancers respond well to immunotherapies or anticancer medications. From 2024 to 2030, the therapeutic segment is anticipated to grow at the quickest rate, 9.44%. In addition to the current surge in scientific inquiry into cell reprogramming therapies, companies seeking to commercialise the technology have made a number of notable strides.

By End-use

-

Research & Academic Institutes

-

Biotechnology & Pharmaceutical Companies

In 2023, the research and academic institutes segment accounted for the largest share, with 67.41%. The advancement of novel methods for securely reprogramming cells has facilitated biotechnology firms in augmenting the clinical effectiveness and safety of conventional stem cell treatments. Additionally, as a result of ongoing research into alternative sources of cell Technologys for regenerative therapies, industry players and the scientific community are concentrating on iPSCs to produce a broad range of human cell Technologys with therapeutic potential, which is driving market growth.

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

REGIONAL ANALYSIS

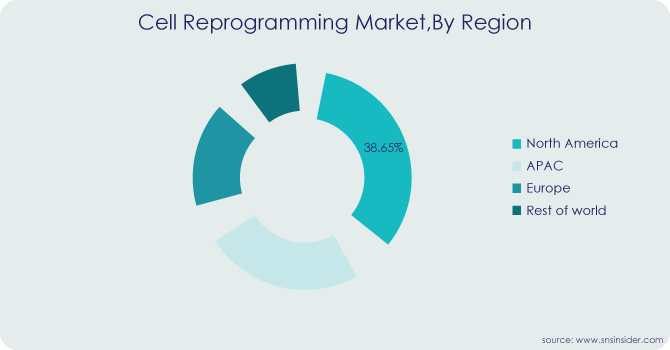

In 2023, North America held a 38.65% market share, dominating the industry. This region's highest revenue share is supported by the presence of important players. Additionally, businesses are launching a variety of projects that support the expansion of the regional industry. For example, Pluristyx, Inc. and Stem Genomics SAS announced a partnership and equity investment in Stem Genomics in July 2023. With the use of Stem Genomics' iCS-digital PSC assay, this partnership seeks to offer a simplified method that will allow clients to evaluate the genomic strength of Pluripotent Stem Cell (PSC) lines from Pluristyx.

Because of the high prevalence of chronic conditions, the widespread adoption of products for analysis and visualisation, technological advancements, and rising R&D investments, the Asia Pacific region is predicted to grow at a significant CAGR of 9.03% between 2023 and 2030.

Key Players

A few prominent entities functioning on a global scale comprise the following: Osiris Therapeutics Inc., Cynata, Astellas Pharma Inc., Sanofi, FUJIFILM Holdings Corporation, EVOTEC, Japan Tissue Engineering Co., Ltd., Mesoblast, Advanced Cell Technology Inc., Human Longevity Inc., Celgene Corporation, and other players.

Osiris Therapeutics Inc-Company Financial Analysis

RECENT DEVELOPMENT

-

Mekonos and bit.bio signed a research agreement in May 2023 to combine Mekonos' cutting-edge ex vivo delivery system with bit.bio's unique opti-oxTM precision cellular reprogramming technology. This partnership also sought to accelerate the use of human cells in cell engineering for research, drug development, and the creation of innovative cell therapies.

-

April 2023: To support the growth of the iPSC reprogramming industry, Ncardia had announced the founding of a new business called Cellistic.

-

Sanofi purchased Tidal Therapeutics in April 2022. Furthermore, the new technology platform will improve Sanofi's research capabilities in immuno-oncology and inflammatory disorders, and it is likely to have broad applicability to other disease areas as well.

| Report Attributes | Details |

| Market Size in 2023 | US$ 406 Million |

| Market Size by 2031 | US$ 725 Million |

| CAGR | CAGR of 8.53 % From 2024 to 2031 |

| Base Year | 2022 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Sendai Virus-Based Reprogramming, MRNA Reprogramming, Episomal Reprogramming, Others) • By Application (Research, Therapeutic) • By End-Use (Research & Academic Institutes, Biotechnology & Pharmaceutical Companies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Osiris Therapeutics Inc., Cynata, Astellas Pharma Inc., Sanofi, FUJIFILM Holdings Corporation, EVOTEC, Japan Tissue Engineering Co., Ltd., Mesoblast, Advanced Cell Technology Inc., Human Longevity Inc., Celgene Corporation |

| Key Drivers | • Growing interest of scientists and researchers in the field of human cell development and innovations. |

| Market Opportunities | • Regenerative medicine holds great promise for the End-use of cellular reprogramming techniques. • Technological advancement |

Frequently Asked Questions

Ans. The cell reprogramming market is segmented on the basis of technology, End-use and end-use.

Ans. The primary driver of the global market for cellular reprogramming tools is the growing interest of scientists and researchers in the field of human cell development and innovations.

Ans. North America stands out as a leading region with significant revenue potential in the market.

Ans. Over the forecast period of 2023 to 2031, the cell reprogramming market is anticipated to expand at a compound annual growth rate (CAGR) of 8.53%.

Ans. According to estimates, the market for cell reprogramming will be valued $406 million on by 2023.

Get in Touch