Stethoscope Market Report Scope & Overview:

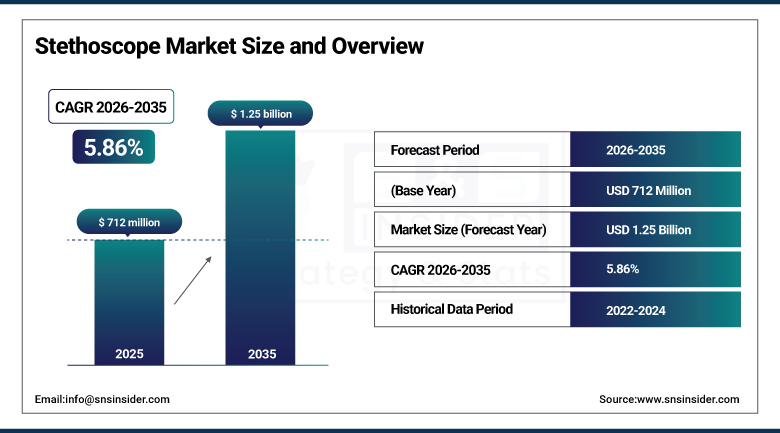

The Stethoscope Market was valued at USD 712 million in 2025 and is expected to reach USD 1.25 billion by 2035, growing at a CAGR of 5.86% from 2026–2035.

The stethoscope is among the most widely known symbols of medicine and, even after more than two centuries since its invention, it remains an essential tool in the daily lives of healthcare practitioners everywhere. The industry is changing drastically, with the adoption of digital and electronic stethoscopes becoming more widespread than their acoustic predecessors. The modern technology allows for sound amplification, noise reduction, sound recording, and even synchronization with smart devices such as phones and computers. Increasing incidence of heart and lung disorders ensures constant demand for stethoscopes in hospital wards, outpatient clinics, emergency rooms, and even home-based health care.

Cardiovascular disease remains the leading cause of death globally, with over 17 million deaths annually. Every physician, nurse practitioner, and paramedic who screens, diagnoses, or monitors heart conditions needs a stethoscope. This creates a large and stable baseline of demand that is unlikely to diminish regardless of other technology changes.

Market Size and Forecast

-

Market Size in 2025: USD 712 Million

-

Market Size by 2035: USD 1.25 Billion

-

CAGR: 5.86% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Stethoscope Market - Request Free Sample Report

Market Trends

-

Electronic and digital stethoscopes with noise cancellation and amplification are gaining market share from traditional acoustic models.

-

AI integration in digital stethoscopes is enabling automatic detection of murmurs, arrhythmias, and abnormal breath sounds.

-

Telemedicine is creating demand for digital stethoscopes with wireless transmission capabilities that can share recordings remotely.

-

Home healthcare growth is expanding the market for consumer-friendly stethoscopes and remote patient monitoring devices.

-

Medical education programs are adopting smart stethoscopes with recording and playback features for training purposes.

-

Wireless Bluetooth stethoscopes are making it easier to store and share recordings in electronic health records.

-

Growing prevalence of COPD, asthma, and heart failure in aging populations is sustaining demand for auscultation tools.

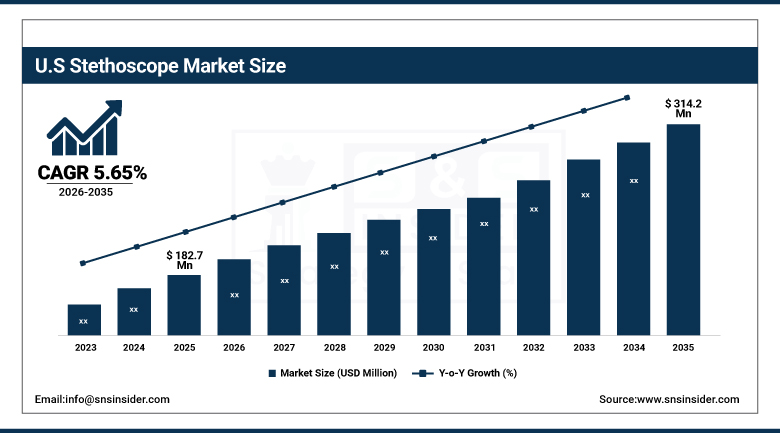

U.S. Stethoscope Market was valued at USD 182.7 million in 2025 and is expected to reach USD 314.2 million by 2035, growing at a CAGR of 5.65% from 2026 to 2035.

The U.S. has a robust healthcare system that is an important market for the purchase of stethoscope variants such as digital versions. 3M Littmann and Eko Health, companies based in the U.S., are considered global market leaders for each variant of the stethoscope segment, respectively. Investments made to enhance primary care facilities and integrate telemedicine have opened up new markets. The U.S. is also ahead in using AI-enabled digital stethoscopes for detecting heart anomalies, which is the highest value segment in the market.

AI-enhanced digital stethoscopes like the Eko CORE 500 are particularly compelling in the U.S. context where physician time is expensive and shortage is significant. A tool that can help a primary care doctor flag a potential cardiac issue that might have been missed without specialist expertise has clear clinical and economic value.

Market Segment Insights

-

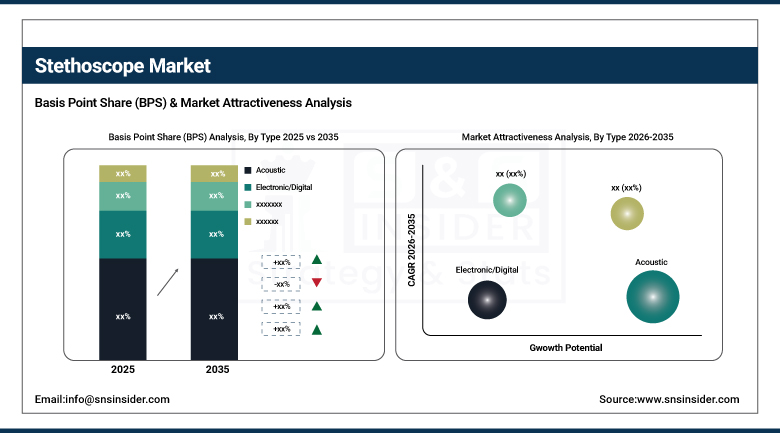

Based on Type, Acoustic Stethoscopes dominated with 73.0% market share in 2025; Electronic/Digital stethoscopes are growing at the highest CAGR.

-

Based on Application, Cardiology is the largest application segment followed by Pulmonology.

-

Based on End-Use, Hospitals and Clinics account for the largest share; Home Healthcare is an emerging fast-growing segment.

-

Fetal stethoscopes serve a specific niche in prenatal care and obstetrics, growing steadily with rising birth rates in developing countries.

Market Segment Analysis

By Type: Acoustic Leads, Digital Growing Fastest

Acoustic stethoscopes comprised 73.0% of the market revenue share in 2025. The benefits of using acoustic stethoscopes include their simple construction, durability, absence of batteries, lack of charging needs, and very low cost. They are absolutely reliable and can be used by any doctor regardless of experience level, from a medical student to a professor. Acoustic stethoscopes have been and will continue to be used in resource-poor countries, where they can still serve as the only diagnosis option in the coming years.

Electrical and digital stethoscopes represent the emerging market segment. The main advantage of electronic stethoscopes compared to acoustic ones is that they enable amplification of the sounds up to 40 times, eliminate background noise in crowded hospital environments, and save recordings. Moreover, the usage of electronic stethoscopes helps older doctors with hearing problems to continue diagnosing patients. One of the biggest breakthroughs in this market segment is the implementation of artificial intelligence that is able to detect unusual sounds.

By Application: Cardiology Biggest, Pulmonology Consistent

The market growth will be primarily driven by cardiology applications. Diagnosing heart function is very important as it gives information about the health of the heart valves, rate, rhythm, and even murmurs. All cardiologists, internists, emergency doctors, and general practitioners require the use of a stethoscope in their cardiac diagnosis. As heart failure, valvular heart disease, and atrial fibrillation become increasingly prevalent among older people around the world, there is a sustained need.

Pulmonary applications come in second place for being the most prevalent stethoscope applications. In such applications, the stethoscope helps diagnose conditions involving the lungs such as asthma, COPD, pneumonia, and pulmonary edema. The stethoscope is used in emergency rooms, intensive care units, respiratory therapy, and in general practice in this application. During the COVID-19 pandemic, auscultating the lung condition was especially important.

By End-Use: Hospitals Lead, Home Healthcare Emerging

Hospitals and clinics represent the major purchasers of stethoscopes both by volume and by value. Large hospitals acquire hundreds or even thousands of stethoscopes yearly as part of equipping their clinical personnel, replacing old instruments, and equipping emergency carts. High quality and robustness are the most important characteristics when buying stethoscopes within this market segment.

There has been an increase in the share of purchases for the purpose of use in the home healthcare environment in recent years. Chronic heart disease, COPD, and hypertension patients have begun receiving remote monitoring services using telehealth platforms that allow them to record themselves using digital stethoscopes that they use in their homes. This tendency became especially pronounced during the period of the pandemic.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

53% |

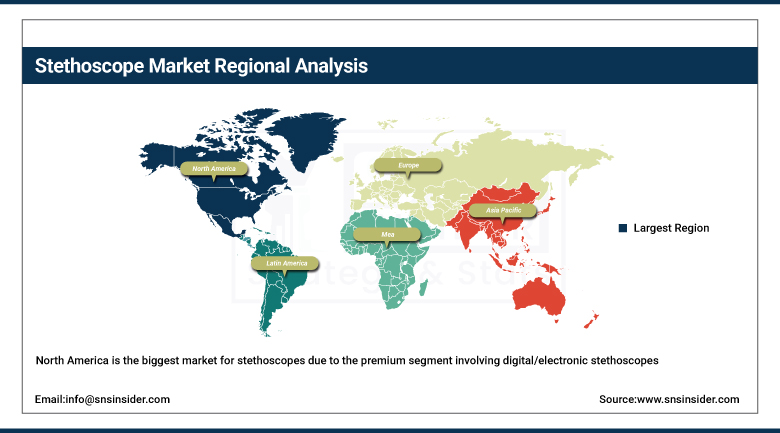

North America

North America is the biggest market for stethoscopes due to the premium segment involving digital/electronic stethoscopes. North America has a higher density of health care practitioners and advanced use of medical equipment. Similarly, Canada has a highly developed health care system. This region is at the forefront in terms of integrating AI-enabled digital stethoscopes into their facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe

The European stethoscope market is highly developed and stable owing to the existence of universal health care facilities in many countries such as Germany, France, Italy, and the UK. The medical universities in Europe graduate many doctors each year, and each of them needs a stethoscope as a part of their kit. There is also rising demand for advanced medical diagnostic equipment in the region.

Asia Pacific

Asia Pacific is not only a high-volume market for low-cost acoustic stethoscopes but also a developing market for electronic stethoscopes due to increased investment in healthcare. The nations of China, India, and Southeast Asia are constructing primary care facilities that ensure steady demand. The healthcare system in Japan and South Korea is highly developed with widespread use of high-end medical equipment. India, with its large healthcare industry, is a particularly crucial market for diagnostic devices.

Middle East & Africa

The investment in healthcare infrastructure in the Middle East through initiatives such as the Vision 2030 program in Saudi Arabia and health services development initiatives in the UAE has brought about a constant need for various types of medical instruments like the stethoscope. The market size in Africa is high based on the sheer number of people in the region who have very minimal healthcare infrastructure. Acoustic stethoscopes are purchased in bulk by organizations such as the World Health Organization.

Latin America

Latin America has a growing healthcare sector with significant needs in both urban hospitals and rural primary care. Brazil, Mexico, Colombia, and Argentina all have substantial markets. Brazil's large public health system (SUS) is a major institutional buyer. The region has a mix of demand for affordable acoustic models for primary care and higher-end electronic models for private hospital and specialist use. Medical education is expanding across the region, creating a consistent stream of new stethoscope purchasers.

Market Growth Drivers

-

Rising cardiovascular and respiratory disease burden drives sustained demand

The rate of occurrences of heart and lung diseases has continued to rise annually due to the aging population and increased occurrence of risk factors such as obesity, smoking, and lack of exercise. These types of illnesses need regular clinical checks that depend heavily on the use of stethoscopes. With the increasing number of people needing heart and lung assessments regularly, the number of times stethoscopes are worn increases accordingly.

Healthcare expansion in developing countries is a powerful structural growth driver. As governments in Asia, Africa, and Latin America invest in primary care networks, community health workers, and rural clinics, demand for affordable and reliable diagnostic tools grows proportionally. The stethoscope is typically one of the first purchases for any new clinical facility.

Market Restraints

-

Cybersecurity risks from digital devices and limited battery life concern some users

With the move to digitization and connectivity of stethoscopes, cybersecurity in the medical industry becomes another concern. The digital stethoscope which records the sounds of patients will have to conform to such policies like HIPAA and GDPR regarding data confidentiality. In addition, the risk of a cyber-attack exposing the data stored can cause great harm to the organization. The other challenge with digital stethoscopes is that they require frequent charges.

Market Opportunities

AI-powered cardiac screening for remote and underserved populations

There is an interesting application involving the use of AI-assisted digital stethoscopes to provide specialized cardiac screening in places where specialists such as cardiologists do not exist. With AI-based digital stethoscopes, one may be able to train a healthcare provider to detect valvular heart disease, which otherwise goes undetected in most African, Asian countries, as well as some other rural locations. Such innovations can make a considerable contribution towards public health and have immense potential in the market.

Recent Developments

-

2025: Eko Health launched its CORE 500 digital stethoscope with onboard AI that can detect atrial fibrillation, murmurs, and other cardiac abnormalities in real time during a clinical examination without requiring any specialist interpretation from the examining clinician.

-

2024: 3M Littmann launched the CORE Digital Stethoscope series with improved Bluetooth range, 40x sound amplification, and integration with the Eko app for recordings and telehealth consultations, expanding the capabilities of the world's most trusted stethoscope brand.

Key Players

Leading companies in the Stethoscope Market:

-

3M Littmann Stethoscopes – Cardiology IV and CORE Digital

-

Eko Health Inc. – CORE 500 AI Digital Stethoscope

-

Welch Allyn (Hillrom/Baxter) – Harvey Elite Cardiophones

-

American Diagnostic Corp. – Adscope Series

-

Heine Optotechnik GmbH – Gamma 3.3 Stethoscope

-

Riester GmbH – Ri-sonic Digital Stethoscope

-

Nasco Healthcare – Education and Training Stethoscopes

-

Rudolf Riester GmbH – Cardio III Stethoscope

-

Prestige Medical – Clinical Lite Stethoscope

-

Ultrascope – Custom Stethoscopes

-

Spirit Medical – Critical Care Stethoscopes

-

Medline Industries Inc. – Clinical Stethoscopes

-

Suzuken Co., Ltd. – Medical Stethoscopes

-

MDF Instruments – Calibra Pro Stethoscope

-

Think Labs Inc. – Electronic Stethoscope Technology

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 712 Million |

| Market Size by 2035 | USD 1.25 Billion |

| CAGR | CAGR of 5.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Acoustic, Electronic/Digital, Fetal Stethoscope, Others) • By Application (Cardiology, Pulmonology, General Diagnosis, Others) • By End-Use (Hospitals & Clinics, Ambulatory Care, Home Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M, Eko Health Inc., Welch Allyn (Hillrom/Baxter), American Diagnostic Corp., Heine Optotechnik GmbH, Riester GmbH, Nasco Healthcare, Rudolf Riester GmbH, Prestige Medical, Ultrascope, Spirit Medical, Medline Industries Inc., Suzuken Co., Ltd., MDF Instruments, Think Labs Inc. |

Frequently Asked Questions

North America leads by value, while Asia Pacific offers the largest volume and fastest growth potential.

Rising prevalence of cardiovascular and respiratory diseases combined with expanding healthcare infrastructure in developing countries.

Acoustic stethoscopes dominate with about 73% market share, while electronic/digital models are growing at the fastest rate.

The market was valued at USD 712 million in 2025.

The market is expected to grow at a CAGR of 5.86% from 2026 to 2035.

Get in Touch