Pharmaceutical Grade Lactose Market Report Scope & Overview:

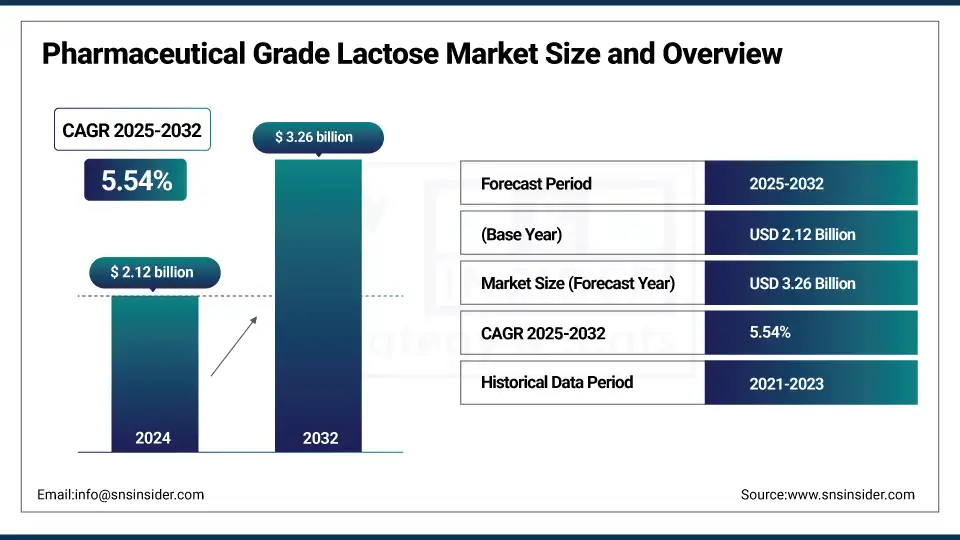

The Pharmaceutical Grade Lactose Market size was valued at USD 2.12 billion in 2024 and is expected to reach USD 3.26 billion by 2032, growing at a CAGR of 5.54% over 2025-2032.

The pharmaceutical grade lactose market is witnessing significant momentum due to increasing demand from drug formulation processes, especially in oral solid dosage forms such as tablets and capsules. The global pharmaceutical grade lactose market is expanding, driven by rising drug production volumes, especially in emerging economies and the expanding generic drug sector. According to industry estimates, nearly 60–70% of oral solid drugs utilize lactose as an excipient, showcasing the compound's widespread utility. As per industry publications, the U.S. pharmaceutical grade lactose market is particularly prominent, with well-established pharmaceutical manufacturing hubs and increasing demand for high-purity excipients.

Pharmaceutical Grade Lactose Market Size and Forecast:

-

Market Size in 2024: USD 2.12 billion

-

Market Size by 2032: USD 3.26 billion

-

CAGR: 5.54% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Pharmaceutical Grade Lactose Market - Request Free Sample Report

On the supply side, investments in cGMP-compliant production facilities have increased, with companies like Kerry Group and DFE Pharma enhancing production capabilities. Rising R&D spending, such as the USD 238 billion in global pharma R&D in 2024, also supports pharmaceutical grade lactose market growth, as lactose continues to be integral in formulation optimization. Furthermore, regulatory emphasis by the FDA and EMA on excipient quality and traceability has fueled the demand for pharmaceutical-grade variants. Increasing demand for pediatric and geriatric drugs, which prefer lactose due to its compressibility and safety profile, is also a major contributor to the pharmaceutical grade lactose market trends.

Pharmaceutical Grade Lactose Market Trends:

-

Increasing demand for oral solid dosage forms such as tablets and capsules is driving the adoption of pharmaceutical grade lactose as a key excipient in drug formulations.

-

Growth in the global pharmaceutical industry, particularly in generic drug manufacturing, is boosting the consumption of lactose due to its cost-effectiveness and excellent compressibility properties.

-

Rising prevalence of chronic diseases is leading to higher drug production volumes, thereby supporting the demand for high-quality excipients like pharmaceutical grade lactose.

-

Advancements in lactose processing technologies are improving purity, particle size distribution, and functionality, enhancing its application across various pharmaceutical formulations.

-

Expanding use of lactose in dry powder inhalers (DPIs) is contributing to market growth, especially with the increasing incidence of respiratory disorders such as asthma and COPD.

-

Stringent regulatory standards and quality requirements are encouraging manufacturers to invest in high-grade lactose production and compliance with pharmacopeia standards.

-

Growing focus on excipient innovation and multifunctional ingredients is promoting the development of co-processed lactose to improve drug delivery performance and manufacturing efficiency.

In May 2024, Kerry Group announced a €30 million investment in its Charleville facility to expand lactose production, highlighting the rising demand for pharmaceutical excipients in North America and Europe.

In July 2024, DFE Pharma launched “BioHale Sucrose and BioHale Trehalose,” enhancing its excipient portfolio and signaling a broader trend of innovation in excipient technologies, indirectly boosting pharmaceutical-grade lactose companies and the pharmaceutical-grade lactose market analysis.

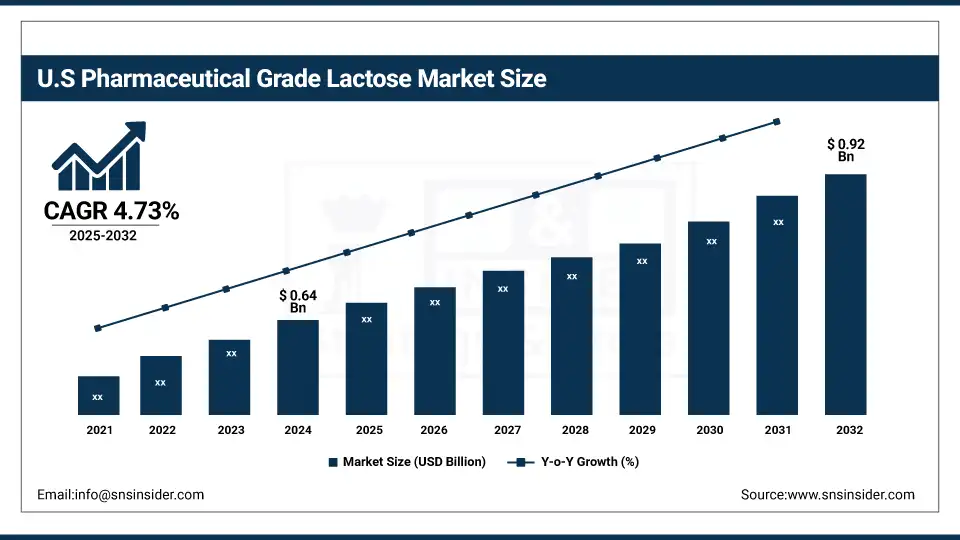

The U.S. pharmaceutical grade lactose market size was valued at USD 0.64 billion in 2024 and is expected to reach USD 0.92 billion by 2032, growing at a CAGR of 4.73% over 2025-2032. The U.S. dominates the region due to advanced pharmaceutical infrastructure, a high volume of drug production, and significant outsourcing by major pharma firms. Canada is witnessing growth due to expanding nutraceutical and CDMO sectors. The fastest-growing segment in this region is inhalation-grade lactose, supported by increasing demand for dry powder inhalers for respiratory diseases.

Market Dynamics:

Drivers:

-

Increased Pharmaceutical Production, Stringent Quality Requirements, and Demand for Excipient Consistency Are Fueling Growth in the Pharmaceutical Grade Lactose Market

The global pharmaceutical grade lactose market is witnessing substantial momentum due to the growing need for high-quality excipients in tablet formulation, especially in solid oral dosage forms. With over 60% of oral solid drugs requiring lactose as a primary filler or binder, the demand is being fueled by the expanding generic drug segment and complex formulation advancements.

According to the European Federation of Pharmaceutical Industries and Associations (EFPIA), the pharmaceutical R&D expenditure in Europe alone reached €41.5 billion in 2023, a 12.7% increase from 2022, reflecting greater innovation in drug formulation and excipient use. The U.S. FDA and EMA have also emphasized GMP-compliant excipients like pharmaceutical grade lactose, boosting its adoption. Furthermore, companies like Kerry Group and MEGGLE are investing in lactose particle engineering technologies to meet pharma-grade consistency demands. These trends, combined with rising demand for orally disintegrating tablets (ODTs) and pediatric formulations, are bolstering the pharmaceutical grade lactose market growth.

Restraints:

-

Raw Material Volatility, Growing Intolerance to Lactose, And Competition from Lactose-Free Excipients Challenge the Growth Trajectory

One significant challenge is the rising prevalence of lactose intolerance globally, impacting the suitability of lactose-based excipients, especially in pediatric and elderly populations. According to NIH, approximately 68% of the global population exhibits some degree of lactose malabsorption.

Additionally, alternative excipients like mannitol, microcrystalline cellulose, and calcium phosphate are gaining traction, especially in formulations where non-reactivity or higher solubility is preferred. Another major constraint is raw milk supply fluctuation, which directly affects pharmaceutical lactose production. As per the FAO, global milk production saw a decline of 0.5% in 2023 due to climate disruptions and rising feed costs, impacting lactose availability. Regulatory constraints such as stringent allergen labeling and compliance with monographs like USP/NF and Ph. Eur. add to manufacturing burdens. These restraints are compelling pharmaceutical companies to diversify excipient portfolios, limiting reliance on lactose.

Segmentation Analysis:

By Type

Crystalline monohydrate lactose held the largest share of the pharmaceutical lactose market in 2024, accounting for over 35.6% of the global revenue. Its dominance stems from its excellent compressibility, superior flow properties, and broad applicability in solid oral dosage forms. Widely used as a filler or diluent in tablets and capsules, it meets pharmacopeial standards (USP, EP, JP), making it a preferred choice for regulated pharmaceutical manufacturing. Its stability in formulation and high compatibility with active pharmaceutical ingredients (APIs) further drive its demand in commercial-scale drug production.

Inhalation grade lactose is witnessing the fastest growth due to rising demand for dry powder inhalers (DPIs) in treating respiratory conditions like asthma and COPD. It is expected to experience accelerated demand owing to its stringent particle size control, low microbial content, and excellent dispersibility required for pulmonary drug delivery.

By Application

Tablet manufacturing was the dominant application in 2024, capturing over 48.2% of the market share. Tablets remain the most commonly used dosage form due to ease of administration, cost-effectiveness, and patient compliance. Lactose is extensively utilized as an excipient in direct compression and wet granulation processes due to its consistent particle size and compressibility, which supports high-speed tablet production lines across the pharmaceutical industry.

DPIs represent the fastest-growing application segment due to the increasing prevalence of respiratory disorders and growing patient preference for needle-free, rapid-acting therapies. Lactose is crucial as a carrier in DPIs, enabling efficient drug deposition in the lungs. Advances in inhaler technology and formulation science are further boosting lactose demand in this segment.

By Functionality

As a filler/diluent, lactose dominated the functionality segment in 2024, contributing to around 41.3% of total usage. Its high compatibility with a wide range of APIs, excellent binding capabilities, and ease of availability make it a widely adopted diluent in both solid and semi-solid dosage forms. It ensures uniform content distribution and helps maintain the integrity of the final drug product, particularly in low-dose medications.

The carrier for inhalation drugs is the fastest-growing functionality due to the increasing use of lactose in pulmonary drug delivery systems. Its role in enhancing drug dispersion and deposition in targeted areas of the lungs is critical for therapeutic efficacy, especially in DPI formulations.

By End-User

Pharmaceutical companies dominated the end-user segment in 2024 with over 55.7% share, driven by their large-scale production of oral solid dosage forms and growing investment in advanced drug formulation. These companies extensively rely on lactose for their consistent performance, regulatory approval status, and broad functionality in generic and branded drugs.

CDMOs are the fastest-growing end-users, fueled by the rising trend of outsourcing pharmaceutical production and formulation development. Their increasing role in supporting biopharma firms with cost-effective, scalable lactose-based formulations is contributing to segment growth, particularly in emerging economies and small- to mid-sized pharma companies.

Regional Analysis:

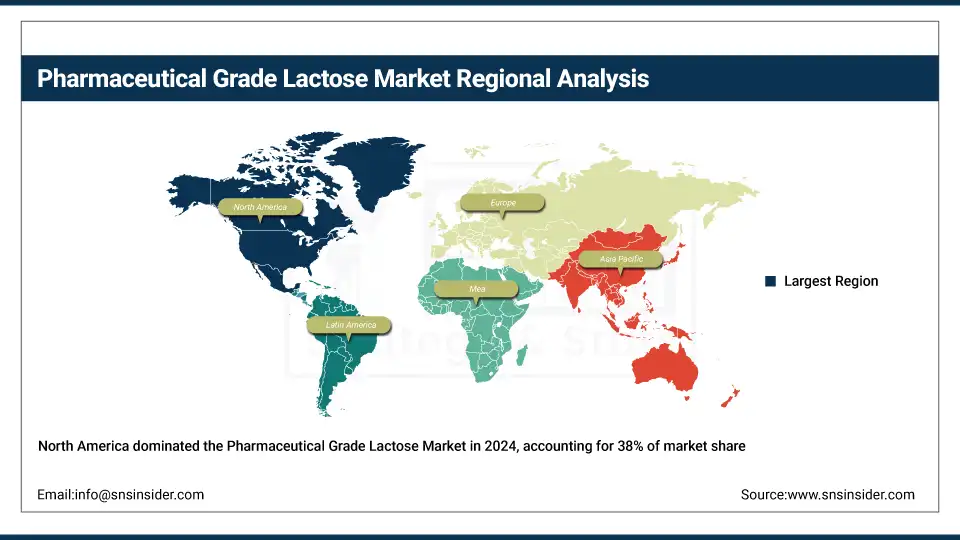

North America held the dominant share in the pharmaceutical lactose market in 2024, accounting for 38% of global revenue. The dominance is driven by the strong presence of major pharmaceutical companies, high adoption of tablet and capsule formulations, and growing investments in R&D and generic drug manufacturing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing regional market, expected to grow significantly due to the increasing demand for generic drugs, cost-efficient manufacturing, and an expanding CDMO landscape. In 2024, the region held a market share of 22.6%. India is the dominant country in the Asia Pacific due to its status as the largest global supplier of generic pharmaceuticals, a vast number of drug manufacturers, and growing investments in CDMOs. China is also gaining momentum owing to rapid pharmaceutical industrialization and a shift towards high-purity excipients. The fastest-growing segment in the region is spray-dried lactose, supported by rising demand for consistent granulation in tablets and capsule formulations.

Key Players:

Leading pharmaceutical grade lactose companies in the market include DMV-Fonterra Excipients, DFE Pharma India Pvt. Ltd., Molkem Chemicals Pvt. Ltd., Sheffield Bio-Science, Beneo-Palatinit GmbH, Armor Pharma, Parmar Chemicals, Hilmar Ingredients, Synprotech Lifesciences, Kandlakunta Pharma, Bharat Lactose, Jigs Chemical, Kshipra Biotech Pvt. Ltd., Vikash Industries, Shreeji Pharma International, JRS Pharma, DFE Pharma GmbH & Co. KG, DMV International, Sudeep Pharma Pvt. Ltd., and KLEPTOSE by Roquette.

Recent Developments:

In March 2024, MEGGLE Group announced the expansion of its pharmaceutical lactose production facility in Germany to meet rising demand for high-purity lactose used in dry powder inhalers (DPIs) and oral solid dosage forms. The upgrade aims to enhance production efficiency and quality compliance.

In June 2024, DFE Pharma launched a new high-flow lactose excipient specifically designed for DPI formulations. This innovation is targeted at improving patient compliance and drug delivery efficiency in respiratory therapies.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.12 billion |

| Market Size by 2032 | USD 3.26 billion |

| CAGR | CAGR of 5.54% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Crystalline Monohydrate Lactose, Granulated Lactose, Spray Dried Lactose, Inhalation Grade Lactose) • By Application (Tablet Manufacturing, Capsule Manufacturing, Dry Powder Inhalers (DPIs), Parenteral and Lyophilized Formulations) • By Functionality (Filler/Diluent, Binder, Stabilizer, Carrier for Inhalation Drugs) • By End-User (Pharmaceutical Companies, Contract Development & Manufacturing Organizations, Nutraceutical Manufacturers, Research & Academic Institutions) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | DMV-Fonterra Excipients, DFE Pharma India Pvt. Ltd., Molkem Chemicals Pvt. Ltd., Sheffield Bio-Science, Beneo-Palatinit GmbH, Armor Pharma, Parmar Chemicals, Hilmar Ingredients, Synprotech Lifesciences, Kandlakunta Pharma, Bharat Lactose, Jigs Chemical, Kshipra Biotech Pvt. Ltd., Vikash Industries, Shreeji Pharma International, JRS Pharma, DFE Pharma GmbH & Co. KG, DMV International, Sudeep Pharma Pvt. Ltd., and KLEPTOSE by Roquette. |

Frequently Asked Questions

It is segmented into tablet manufacturing, capsule manufacturing, dry powder inhalers, and parenteral/lyophilized formulations.

Lactose acts as a filler/diluent and binder, improving compressibility, flowability, and tablet integrity in oral solid formulations.

Key players include BASF Corporation, DFE Pharma, Kerry Group, Meggle GmbH, and Lactose (India) Limited, among others.

Pharmaceutical lactose is widely used in tablet and capsule manufacturing, dry powder inhalers, and lyophilized formulations as a filler, binder, or carrier.

The rising use of dry powder inhalers (DPIs) and oral solid dosage forms, along with the demand for high-purity excipients, is fueling market growth.

Get in Touch