Genomics Services Market Report Scope & Overview:

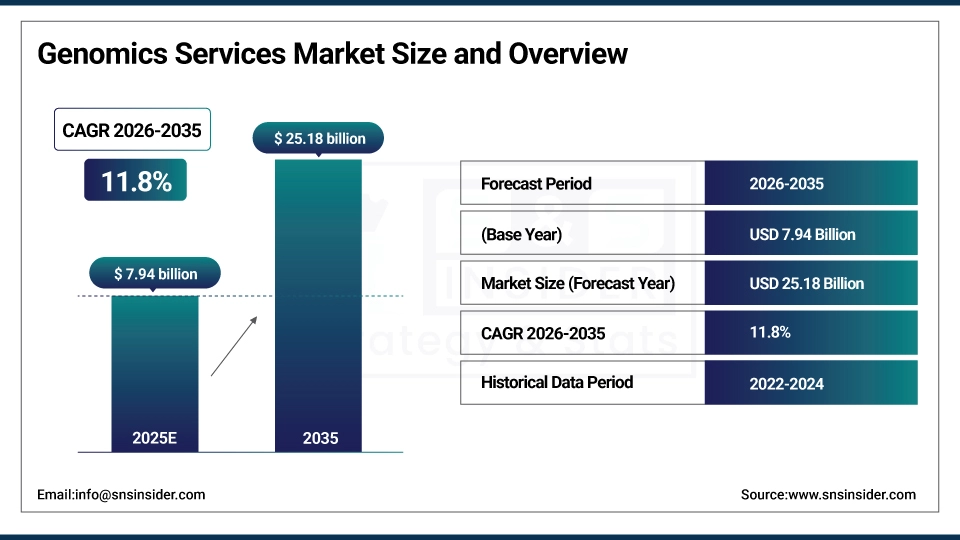

The Genomics Services Market size is estimated at USD 7.94 billion in 2025 and is expected to reach USD 25.18 billion by 2035, growing at a CAGR of 11.8% over the forecast period of 2026-2035.

The global genomic services market trend is a growing demand for advanced genomic solutions such as next-generation sequencing (NGS), gene expression profiling, and epigenomics services. The growth of the market is driven by increasing prevalence of genetic disorders, government funding for precision medicine initiatives, and rising adoption of genomic data in clinical diagnostics and pharmaceutical research. This trend is also driven by a growing adoption of value-based healthcare models and the growing focus on personalized medicine as pharmaceutical companies, research institutes, and contract research organizations become more focused on improving clinical trial efficiency and patient stratification and are more willing to invest in genomic technologies, resulting in growth in the domestic and international market for sequencing-based and microarray-based genomic services across diagnostics and research applications.

For instance, in March 2024, growing awareness of precision medicine and expanded reimbursement coverage for genomic diagnostics drove a 19% increase in next-generation sequencing service orders across healthcare facilities and diagnostic centers in North America, boosting genomic data utilization and personalized treatment adoption.

Genomics Services Market Size and Forecast:

-

Market Size in 2025E: USD 7.94 billion

-

Market Size by 2035: USD 25.18 billion

-

CAGR: 11.8% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Genomics Services Market - Request Free Sample Report

Genomics Services Market Trends

-

Genomic services are being adopted because research institutes and pharmaceutical companies demand faster turnaround for whole genome sequencing, genotyping, and RNA sequencing data to accelerate drug discovery and biomarker identification.

-

Customized genomic profiling tools based on disease indication, patient population, and sample type to improve precision diagnostics outcomes and treatment stratification in oncology and rare disease management.

-

The development of AI-powered bioinformatics platforms, cloud-based genomic data management tools, and automated library preparation workflows to improve turnaround speed and reduce the cost per sample for sequencing services.

-

Epigenomics services, methylation profiling, and chromatin accessibility assays are all gaining demand to ensure comprehensive characterization of gene regulation and disease mechanisms across translational research programs.

-

Increased demand for cloud-based genomic data storage, multi-omics integration platforms, and HIPAA-compliant data security frameworks to support large-scale population genomics studies and clinical research applications.

-

Collaboration between contract research organizations, genomic service providers, and healthcare facilities to develop integrated sequencing workflows and improve data standardization and cross-platform interoperability.

-

NIH, FDA, and national genomics programs promoting standards for genomic data sharing, clinical-grade sequencing validation, laboratory-developed test (LDT) oversight, and patient genomic data access rights.

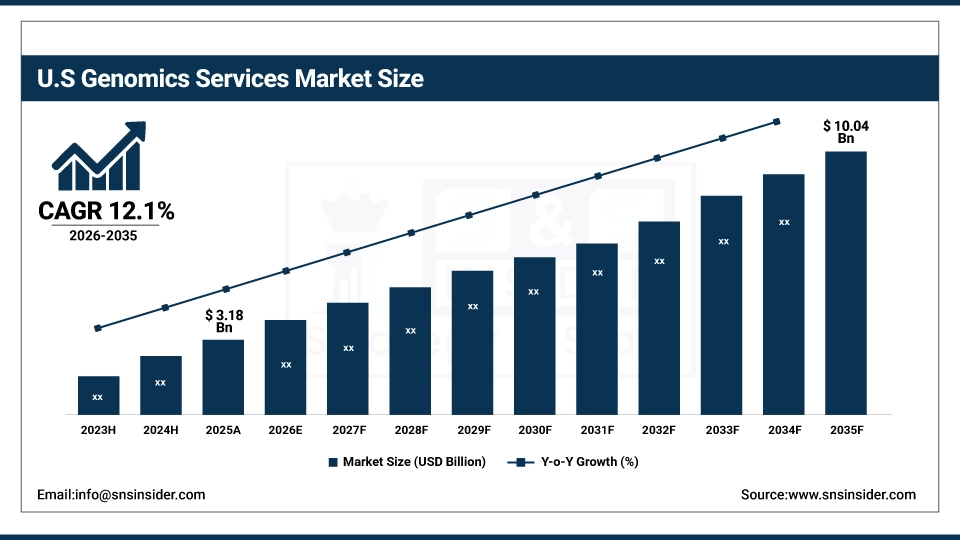

The U.S. Genomics Services Market is estimated at USD 3.18 billion in 2025 and is expected to reach USD 10.04 billion by 2035, growing at a CAGR of 12.1% from 2026-2035. The United States represents the largest market for genomic services, primarily driven by the high concentration of genomic research activity, federal funding through NIH and NCI programs, and well-developed clinical laboratory infrastructure. Government investment in precision medicine, moderately high levels of insurance reimbursement for molecular diagnostics, and increased pharmaceutical and biotech spending on genomic research and companion diagnostics help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory clarity and swift adoption of NGS-based and PCR-based genomic services across diagnostics and research end-users.

Genomics Services Market Growth Drivers:

-

Rising Adoption of Precision Medicine and Companion Diagnostics is Driving the Genomics Services Market Growth

Rising adoption of precision medicine and companion diagnostics take the center stage as a growth driver for the genomic services market share, and are driven by the expanding use of next-generation sequencing in oncology treatment selection, rare disease diagnosis, and pharmacogenomics testing across hospital systems and specialized diagnostic laboratories. These genomic applications for clinical decision-making and drug development are expanding the base of the market, the penetration of NGS-based and microarray-based service platforms, and adding to the overall market share globally.

For instance, in June 2024, NGS-based companion diagnostic testing and clinical genomic profiling services accounted for ~62% of the total U.S. molecular diagnostics laboratory revenue investments, reflecting growing institutional reliance and expanding genomic services market share.

Genomics Services Market Restraints:

-

High Cost of Genomic Sequencing and Data Interpretation Challenges are Hampering the Genomics Services Market Growth

High cost of genomic sequencing workflows and data interpretation challenges also restrict the genomic services market growth, as a large number of healthcare facilities and research institutes that have access to sequencing instruments remain limited by bioinformatics expertise gaps or face difficulties translating raw genomic data into actionable clinical insights. This might lead to underutilization of sequencing capacity, extended project timelines, and reduced return on investment for diagnostic laboratories and pharmaceutical partners. As a result, clinical adoption lags and market growth is stunted in regions where genomic infrastructure is underdeveloped and reimbursement coverage for genomic testing remains limited.

Genomics Services Market Opportunities:

-

Expanding Population Genomics Programs and Direct-to-Consumer Testing Drive Future Growth Opportunities for the Genomics Services Market

The opportunity in expanding population genomics programs and direct-to-consumer genomic testing in the genomic services market is in the form of large-scale genotyping studies, national biobank initiatives, and consumer health genetics platforms. These solutions provide for broad disease risk identification, ancestral genomic data generation, and population-level pharmacogenomics insights. Through enhanced data volume at reduced per-sample sequencing costs, growing public awareness of genetic health risks, and expanding government-funded genomic cohort programs, particularly in regions with active national precision medicine strategies, these trends may improve disease surveillance capabilities, enable drug target discovery, and expand the market.

For instance, in April 2024, the NIH reported that over 1 million participants had enrolled in the All of Us Research Program genomic cohort, highlighting rising platform demand and increasing utilization of large-scale genomic sequencing and genotyping services across the United States.

Genomics Services Market Segment Analysis

-

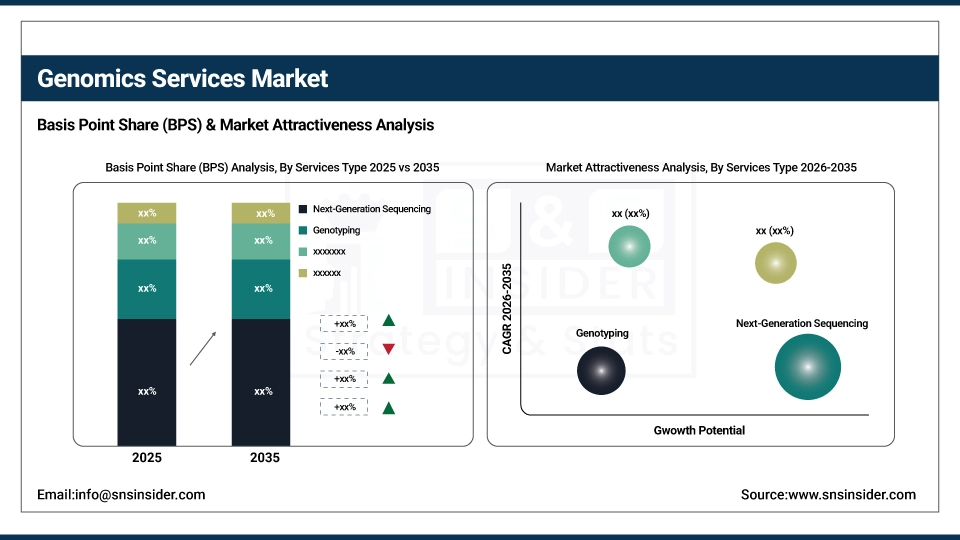

By services type, next-generation sequencing held the largest share of around 38.42% in 2025E, and the epigenomics services segment is expected to register the highest growth with a CAGR of 13.27%.

-

By technology, the next-generation sequencing (NGS) segment dominated the market with approximately 44.18% share in 2025E, while the microarray segment is expected to register steady growth over the forecast period.

-

By application, diagnostics accounted for the leading share of nearly 52.36% in 2025E, and the research segment is expected to register the highest growth with a CAGR of 12.64%.

-

By end-user, pharmaceutical & biotechnological companies accounted for a significant revenue share in 2025E, and contract research organizations (CROs) are expected to register the highest growth over the forecast period.

By Services Type, Next-Generation Sequencing Leads the Market, While Epigenomics Services Registers Fastest Growth

The next-generation sequencing segment accounted for the highest revenue share of approximately 38.42% in 2025, owing to its widespread adoption across oncology diagnostics, rare disease research, and infectious disease surveillance applications that require high-throughput, cost-efficient genomic data generation at clinical and research scale. Emerging trends, including increasing requirements for whole exome and whole genome sequencing in clinical trial patient stratification and growing regulatory acceptance of NGS-based companion diagnostics. In comparison, the epigenomics services segment is anticipated to achieve the highest CAGR of nearly 13.27% during the 2026–2035 period, driven by the increasing demand from cancer epigenetics research, aging biology studies, and drug mechanism-of-action characterization programs. Drivers include rising adoption among academic and pharmaceutical research teams, the preference for comprehensive methylation profiling and chromatin accessibility service packages, and growing interest in epigenomic biomarker discovery for early disease detection. Gene expression services (RNASeq) and genotyping segments are also sustaining strong demand, supported by single-cell transcriptomics growth and large-scale GWAS studies requiring cost-effective genotyping arrays across population cohorts.

By Technology, NGS Dominates, while PCR Maintains Steady Clinical Relevance

By 2025, the next-generation sequencing technology segment contributed the largest revenue share of 44.18% due to its scalability across whole genome, whole exome, targeted panel, and RNA sequencing applications, combined with rapidly declining sequencing costs and growing availability of benchtop NGS instruments. Growing adoption of short-read and long-read sequencing platforms coupled with data analysis automation is encouraging both clinical laboratories and research institutions to transition from legacy methods to NGS-centric workflows. The polymerase chain reaction (PCR) segment maintains a significant and stable market presence due to its established role in clinical diagnostics, infectious disease testing, and genotyping validation, particularly in settings where rapid turnaround and low infrastructure requirements are priorities. Microarray-based services continue to serve population genomics and SNP genotyping applications, with sustained demand from biobank programs and agricultural genomics research alongside the human health segment.

By Application, Diagnostics Leads, and Research Registers Fastest Growth

The diagnostics segment accounted for the largest share of the genomic services market with about 52.36%, owing to the direct clinical utility of genomic testing in cancer diagnosis, inherited disease screening, prenatal testing, and pharmacogenomics-guided therapy selection across hospital systems and specialized diagnostic centers. Reasons driving the diagnostics segment include growing physician adoption of genomic panel testing, expanding reimbursement coverage for molecular diagnostics, and regulatory approval of NGS-based companion diagnostic assays for targeted oncology therapies. In addition, the research segment is slated to grow at the fastest rate throughout the forecast period of 2026–2035, as academic research institutes, pharmaceutical companies, and contract research organizations increase investment in functional genomics, single-cell sequencing, and multi-omics data integration to accelerate drug target identification and translational research programs. Increased focus on biomarker discovery and mechanistic disease characterization contributes to their adoption, while reduced sequencing costs and improved bioinformatics accessibility drive continued expansion of genomics-based research services globally.

By End-User, Pharmaceutical & Biotechnological Companies Lead, and CROs Register Fastest Growth

Pharmaceutical and biotechnological companies accounted for the leading end-user share of the genomic services market in 2025, owing to their extensive reliance on genomic services for drug discovery, clinical trial patient stratification, biomarker validation, and companion diagnostic co-development across oncology, rare disease, and immunology pipelines. Reasons driving this segment include increasing genomic data requirements at all stages of drug development, growing adoption of NGS in IND-enabling studies, and the rising number of gene therapy and cell therapy programs requiring comprehensive genomic characterization. In addition, contract research organizations (CROs) are slated to grow at the fastest rate throughout the forecast period of 2026–2035, as sponsors increasingly outsource genomic testing workflows to specialized CROs with established sequencing infrastructure, bioinformatics capabilities, and regulatory compliance expertise. Research institutes and healthcare facilities & diagnostic centers also contribute significantly to market revenues, supported by academic grant funding, national genomics initiatives, and expanding clinical genomics programs within hospital laboratory networks.

Genomics Services Market Regional Highlights:

North America Genomics Services Market Insights:

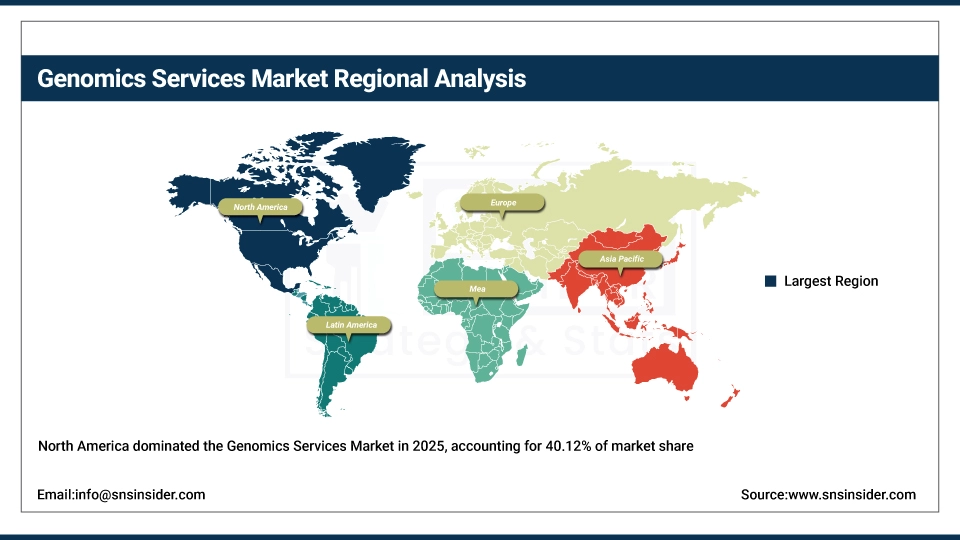

North America held the largest revenue share of over 40.12% in 2025 of the genomic services market due to an established genomics research ecosystem, high concentration of pharmaceutical and biotechnology companies, and increased laboratory adoption of clinical-grade NGS sequencing platforms for oncology and rare disease diagnostics. Drivers include ubiquitous use of genomic data in clinical trials, an improved regulatory framework for NGS-based diagnostics, growing reimbursement coverage for molecular testing, and greater acceptance of pharmacogenomics-guided prescribing across large health systems. At the same time, various NIH-funded research programs, precision medicine mandates, and enormous investments in genomics infrastructure from academic medical centers and commercial laboratories are anchoring genomic services platforms in the market, and ensuring multibillion dollar revenues across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Genomics Services Market Insights:

Asia Pacific is the fastest-growing segment in the genomic services market with a CAGR of 13.84%, as the awareness about precision medicine, government-funded genomics programs, and healthcare infrastructure modernization in countries such as China, India, Japan, and South Korea is growing. Factors including rapid expansion of biobanking initiatives, rising pharmaceutical R&D investment, and growing uptake of NGS-based clinical diagnostics in tertiary care hospitals are stimulating the market growth. National genomics programs and academic-industry partnerships have been instrumental in improving access to advanced sequencing services, especially in urban research and clinical centers. Public sector investments and government programs also help in advancing genomic data infrastructure and personalized medicine adoption. Increase in demand in the Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing affordability and accessibility of cloud-based genomic data analysis platforms.

Europe Genomics Services Market Insights:

The genomic services market in Europe is the second-dominating region after North America on account of an increase in the adoption of next-generation sequencing in national health systems, robust data protection regulations including GDPR governing genomic data handling, and increasing patient participation in national genomics initiatives across the UK, France, Germany, and the Netherlands. Rising implementation of the Genomics England 100,000 Genomes Project outcomes, national precision medicine strategies, favorable government funding for genomic research programs, and cross-border genomic data sharing frameworks are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Genomics Services Market Insights:

In Latin America, and Middle East & Africa, the growing healthcare digitization efforts and increase in genomic research funding with improving laboratory infrastructure support the genomic services market growth. The rising popularity of affordable sequencing platforms and multilingual bioinformatics support capabilities, along with public awareness campaigns around genetic disease prevalence, will aid genomic diagnostics accessibility and research program development. The increasing investment in academic genomics capacity and improving clinical laboratory standards in these regions are continuing to encourage market growth.

Genomics Services Market Competitive Landscape:

Illumina, Inc. (est. 1998) is a global leader in genomics instrumentation and sequencing services that focuses on high-throughput NGS platforms and integrated genomic service solutions for clinical and research customers. It uses its comprehensive sequencing technology portfolio and global laboratory partnerships to deliver industry-leading genomic services with seamless bioinformatics workflow integration.

-

In February 2025, it expanded its genomic services capabilities with enhanced whole genome sequencing and multi-omics service packages for pharmaceutical and biotech clients, aiming to accelerate drug discovery workflows and companion diagnostic co-development across its global service laboratory network.

Thermo Fisher Scientific Inc. (est. 1956) is a well-known global life sciences company focused on genomic analysis tools, sequencing services, PCR-based assays, and microarray platforms for research and clinical applications. It invests in integrated genomic service workflows and bioinformatics solutions with the hopes of transforming sample-to-insight timelines with scalable, compliant, and data-rich genomic services.

-

In May 2024, launched an enhanced Ion Torrent-based targeted sequencing service panel for oncology biomarker profiling and companion diagnostic development, deployed across CRO and pharmaceutical client networks to improve clinical trial genomic data quality and turnaround speed.

Labcorp (Laboratory Corporation of America Holdings) (est. 1978) is a leading diagnostics and drug development services company in the fields of clinical genomic testing, NGS-based oncology profiling, and pharmacogenomics services. The company's genomic services portfolio focuses on clinically validated sequencing assays and comprehensive genetic testing menus, with a strong commitment to regulatory compliance and continuous innovation to complement its strong market presence across both clinical and research settings.

-

In September 2024, introduced advanced hereditary cancer NGS panel testing and pharmacogenomics reporting features within its Labcorp Genetics platform, strengthening clinical genomic service capabilities and expanding adoption among oncology practices and integrated health system laboratory networks.

Genomics Services Market Key Players:

-

Illumina, Inc.

-

Thermo Fisher Scientific Inc.

-

Labcorp (Laboratory Corporation of America Holdings)

-

Quest Diagnostics Incorporated

-

BGI Genomics Co., Ltd.

-

Eurofins Scientific SE

-

Novogene Corporation

-

Pacific Biosciences of California, Inc. (PacBio)

-

Oxford Nanopore Technologies plc

-

Agilent Technologies, Inc.

-

GENEWIZ (Azenta Life Sciences)

-

CD Genomics

-

Psomagen, Inc.

-

Macrogen Inc.

-

Strand Life Sciences (Strand Genomics)

-

Dante Labs

-

Fulgent Genetics, Inc.

-

Baylor Genetics

-

Ambry Genetics (Konica Minolta)

-

InVitae Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.94 Billion |

| Market Size by 2035 | USD 25.18 Billion |

| CAGR | CAGR of 11.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Services Type (Gene Expression Services (RNASeq), Epigenomics Services, Genotyping, Next-generation Sequencing, Others) • By Technology (Polymerase Chain Reaction (PCR), Next-generation Sequencing (NGS), Microarray, Others) • By Application (Diagnostics, Research, Others) • By End-user (Research Institutes, Healthcare Facilities & Diagnostic Centers, Pharmaceutical & Biotechnological Companies, Contract Research Organizations (CROs)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Illumina, Inc., Thermo Fisher Scientific Inc., Labcorp (Laboratory Corporation of America Holdings), Quest Diagnostics Incorporated, BGI Genomics Co., Ltd., Eurofins Scientific SE, Novogene Corporation, Pacific Biosciences of California, Inc. (PacBio), Oxford Nanopore Technologies plc, Agilent Technologies, Inc., GENEWIZ (Azenta Life Sciences), CD Genomics, Psomagen, Inc., Macrogen Inc., Strand Life Sciences (Strand Genomics), Dante Labs, Fulgent Genetics, Inc., Baylor Genetics, Ambry Genetics (Konica Minolta), InVitae Corporation |

Frequently Asked Questions

Ans: The Genomics Services Market is expected to grow at a CAGR of 11.8% over the forecast period.

Ans: The Genomics Services Market size was USD 7.94 billion in 2025 and is expected to reach USD 25.18 billion by 2035.

Ans: Rising Adoption of Precision Medicine and Companion Diagnostics is Driving the Genomics Services Market Growth.

Ans: By services type, the Next-Generation Sequencing segment dominated the Genomics Services Market in 2025.

Ans: North America dominated the Genomics Services Market in 2025.

Get in Touch