Photoelectric Sensor Market Report Scope & Overview:

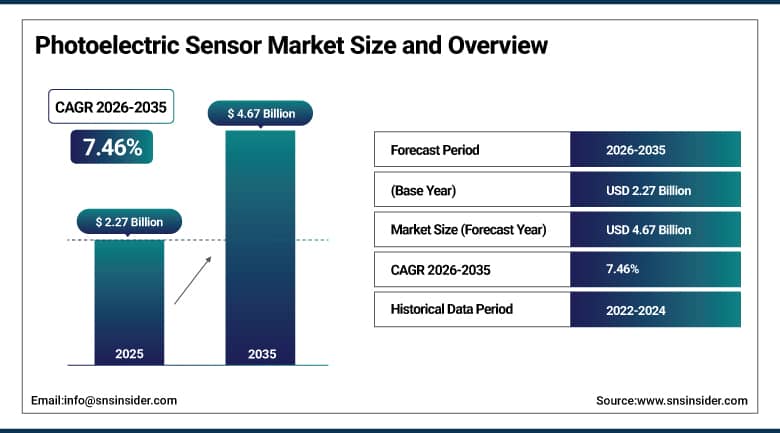

The Photoelectric Sensor Market was valued at USD 2.27 Billion in 2025 and is expected to reach USD 4.67 Billion by 2035, growing at a CAGR of 7.46% from 2026–2035.

The Photoelectric Sensor Market is experiencing considerable growth because of the fast pace of industrial automation and the rising use of intelligent manufacturing systems in different industries. High demand for highly accurate sensing and noncontact measuring solutions is one of the key factors that drives market development. Development in robotics, automation technologies in the packing industry, and automotive assembly lines also encourages adoption of sensors. Furthermore, new advances in sensors include higher accuracy, reduced size, and IoT connectivity, which help boost the efficiency of production. Moreover, growing needs in industrial safety and real-time monitoring in manufacturing environments also promote demand growth.

According to the International Federation of Robotics, more than 4 million industrial robots are operating worldwide, all of which depend heavily on sensing and detection systems such as photoelectric sensors for precision control and automation efficiency. Furthermore, the United Nations Industrial Development Organization reports that manufacturing contributes around 16% of global GDP, reinforcing the strong industrial foundation driving demand for advanced sensing technologies used in automation, monitoring, and process optimization.

Photoelectric Sensor Market Size and Forecast:

-

Market Size in 2026E: USD 2.44 Billion

-

Market Size by 2035: USD 4.67 Billion

-

CAGR: 7.46% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Photoelectric Sensor Market - Request Free Sample Report

Photoelectric Sensor Market Trends:

-

Rising adoption of industrial automation and Industry 4.0 technologies driving demand for high-precision photoelectric sensors in manufacturing processes

-

Growing integration of smart sensing solutions in packaging, logistics, and material handling systems to improve detection accuracy and operational efficiency

-

Increasing use of photoelectric sensors in automotive production lines for position sensing, object detection, and quality control applications

-

Expanding deployment in consumer electronics, food & beverage, and pharmaceutical industries for non-contact sensing and process automation

-

Continuous advancements in sensor miniaturization, detection range, and connectivity features such as IoT integration enhancing performance and real-time monitoring capabilities

U.S. Photoelectric Sensor Market Outlook:

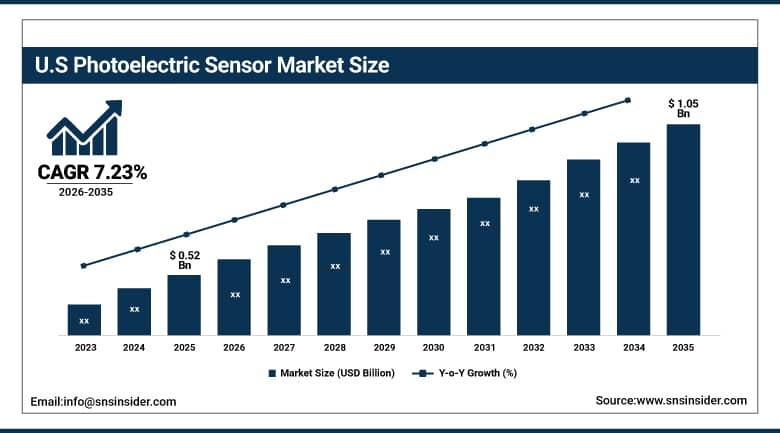

The U.S. Photoelectric Sensor Market was valued at USD 0.52 Billion in 2025 and is expected to reach USD 1.05 Billion by 2035, growing at a CAGR of 7.23% from 2026–2035.

The United States leads North American photoelectric sensor revenues through its large industrial manufacturing base’s automation upgrade investment, the automotive sector’s assembly line quality inspection and robotic system integration, and the warehouse logistics sector’s growing material handling automation. Rockwell Automation, Banner Engineering, and Cognex sustain U.S. market leadership through their comprehensive photoelectric sensor portfolios serving automotive, electronics, and food and beverage manufacturing customers across diverse detection range and environmental requirements.

According to the U.S. Bureau of Labor Statistics, manufacturing productivity has increased significantly due to automation and advanced sensing systems, highlighting the growing role of intelligent technologies in improving industrial efficiency.

Photoelectric Sensor Market Segment Analysis:

-

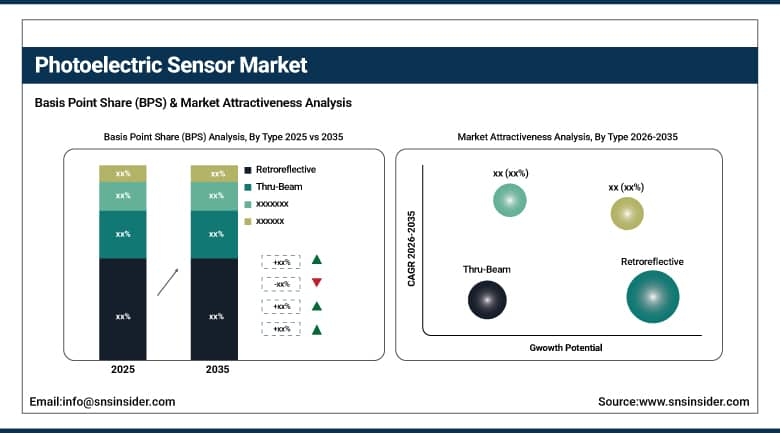

By Type, Retroreflective segment dominated the Photoelectric Sensor Market in 2025 with 41% share; Thru-Beam segment is the fastest growing segment.

-

By Light Source, Infrared segment dominated the market in 2025 with 46% share; Laser Beam segment is the fastest growing segment.

-

By Range, 100–1000mm segment dominated the market in 2025 with 38% share; Above 10000mm segment is the fastest growing segment.

-

By Application, Industrial Manufacturing segment dominated the market in 2025 with 44% share; Automotive & Transportation segment is the fastest growing segment.

By Type, retroreflective photoelectric sensors segment dominates the photoelectric sensor market, while thru-beam sensors segment is the fastest-growing segment

Retroreflective photoelectric sensors dominated the market in 2025 owing to its cost-effective nature, simple installation process, and single-unit working along with a reflector. These types of sensors are extensively employed in various industrial applications, particularly automation, packaging, and material handling applications where detection of objects at a moderate distance is needed. The smaller size, ease of installation, and ability to function well in multiple settings have made them a popular choice in manufacturing operations and contributed to their leadership in the market.

Thru-Beam sensors are the fastest growing segment owing to its precision, long-range detection, and superior reliability in extreme conditions prevalent in the industries. Through the employment of two distinct units for transmitter and receiver, these sensors provide accurate results without any problem. Growing use in automated systems, logistics applications, and even safety applications has raised the demand for these sensors.

By Light Source, infrared-based sensors segment dominates the photoelectric sensor market, while laser beam sensors segment is the fastest-growing segment

Infrared-based photoelectric sensors dominated the market in 2025 owing to their cost-effectiveness, efficiency, and versatility within industrial automation systems. The technology ensures accurate object detection and is not susceptible to environmental light conditions, which makes it ideal for use in packaging, manufacturing, and material handling operations. With features such as high energy efficiency, durability, and suitability for different environments, the infrared sensors have become the preferred choice in industrial sensing applications.

Laser beam sensors are the fastest growing segment because of their accuracy, high detection range, and ability to detect small and rapidly moving objects. Laser beam sensors are becoming more popular because of their accuracy in identifying objects and detecting defects in manufacturing processes and quality assurance applications. The increasing need for smart factories and Industry 4.0 initiatives in the automation industry has been fueling their demand.

By Range, 100–1000mm range segment dominates the photoelectric sensor market, while above 10000mm range segment is the fastest-growing segment

The 100–1000mm range segment dominated the market in 2025 owing to its compatibility with most industrial applications of automation, which usually require medium distance detection capabilities. The segment is popular in assembly line, packaging machine, and conveyor line monitoring applications. Due to its versatility and affordable cost, this range of sensors finds widespread use in a number of industrial applications making it the most dominant range segment.

The above 10000mm range segment is the fastest growing as a result of growing demand for long-range detection applications in large-scale industrial operations, logistics facilities, and infrastructure automation. Such sensors are important for monitoring of vast regions, big machineries, and fast moving transportation systems. Increased need for warehouse automation, smart infrastructures, and enhanced safety systems are fuelling the usage of this range.

By Application, industrial manufacturing segment dominates the photoelectric sensor market, while automotive & transportation segment is the fastest-growing segment

Industrial Manufacturing dominated the Photoelectric Sensor Market in 2025 owing to the wide deployment of automation systems, robots, and smart manufacturing lines. The applications of photoelectric sensors include object detection, positioning, and control processes in manufacturing environments. As they offer increased productivity, improved precision, and low downtime, they play a vital role in industrial applications. The trend of industrial automation and adoption of smart factories has helped this segment gain the market leadership position.

The Automotive & Transportation segment is the fastest growing owing to the deployment of sensing technology in automotive manufacturing and transportation. Applications of photoelectric sensors in this segment involve automation of assembly lines, safety systems, and development of smart vehicle technologies. With the rising use of electric vehicles, autonomous driving solutions, and smart transport systems, their adoption rate will only continue to increase.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

44.8% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Mexico |

38.4% |

Asia Pacific Photoelectric Sensor Market Insights

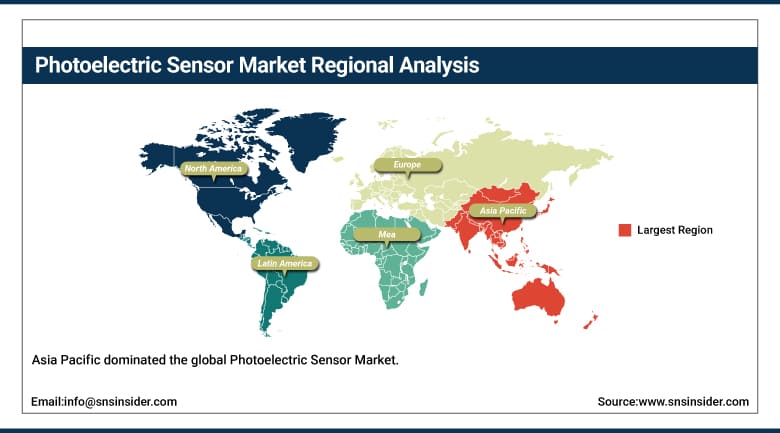

Asia Pacific dominated the global Photoelectric Sensor Market through rapid industrialisation, expanding manufacturing capacity, and high investments in automation technologies across China, Japan, South Korea, and India. China accounts for approximately 44.8% of Asia Pacific revenues through its massive manufacturing base’s automation investment and growing penetration of IIoT across numerous industrial facilities, where rising use of enhanced technology and strong government support for digitalisation across the industrial sector drive continued sensor procurement growth.

According to the International Federation of Robotics, China installs more industrial robots annually than any other country, significantly driving demand for advanced sensing technologies, including photoelectric sensors, across automated production systems.

Furthermore, the National Bureau of Statistics of China reports that China accounts for over 25% of global manufacturing output, reinforcing its position as the world’s largest industrial base and further supporting large-scale adoption of industrial automation and sensing solutions in manufacturing environments.

Japan’s advanced manufacturing sector’s precision automation requirements, South Korea’s electronics and automotive industries’ sensor-intensive production lines, and India’s rapidly growing manufacturing investment under government industrial policy collectively sustain Asia Pacific’s dominant and fastest-growing regional trajectory. The region’s combination of established manufacturing leadership and accelerating automation adoption in emerging Southeast Asian markets creates structural demand growth above global average rates.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Photoelectric Sensor Market Insights

North America is a significant photoelectric sensor market where the United States’ large industrial manufacturing base, advanced robotics adoption, and early implementation of industrial IoT technology create substantial sensor procurement. The United States accounts for approximately 82.5% of North American revenues through Rockwell Automation, Banner Engineering, and Cognex’s comprehensive photoelectric sensor portfolios serving automotive, electronics, and logistics manufacturing customers across the region.

The U.S. Department of Commerce notes that manufacturing contributes approximately 11% of U.S. GDP, underscoring the sector’s dependence on high levels of automation and advanced control systems.

In addition, the National Institute of Standards and Technology emphasizes smart manufacturing initiatives that prioritize real-time sensing, machine vision, and automated quality control systems, further reinforcing the importance of photoelectric sensors in modern industrial environments.

Canada contributes supplementary North American revenues through its automotive parts manufacturing sector’s assembly line sensor procurement, the growing food and beverage processing industry’s automated packaging line investment, and the warehouse logistics sector’s material handling automation adoption tracking broader North American e-commerce fulfilment infrastructure expansion.

Europe Photoelectric Sensor Market Insights

Europe is a technically advanced photoelectric sensor market where the automotive industry’s sophisticated production line automation, the pharmaceutical and food processing sectors’ hygienic detection requirements, and the strong presence of leading sensor manufacturers create consistent regional demand. Germany accounts for approximately 24.6% of European revenues through its large automotive and industrial machinery manufacturing sectors and the commercial presence of Sick AG, Leuze Electronic, and Pepperl+Fuchs’ German manufacturing operations.

According to Eurostat, manufacturing accounts for approximately 15–16% of EU GDP, reinforcing strong investments in industrial automation and advanced production technologies. Furthermore, the European Commission highlights ongoing Industry 4.0 initiatives focused on smart factories, digital twins, and automated production systems, accelerating the adoption of advanced sensing solutions such as photoelectric sensors across modern manufacturing environments.

MEA & Latin America Photoelectric Sensor Market Insights

The UAE leads MEA revenues at approximately 22.8% through its advanced manufacturing and logistics infrastructure investment, the growing food and beverage processing sector’s automated packaging line adoption, and the region’s broader digital transformation programmes creating industrial automation procurement. Saudi Arabia’s Vision 2030 manufacturing diversification creates growing regional sensor demand.

Mexico leads Latin American revenues at approximately 38.4% through its large automotive manufacturing sector serving North American export markets, whose assembly line automation and quality inspection requirements create substantial photoelectric sensor procurement from global Tier 1 suppliers. Brazil’s growing manufacturing automation investment contributes secondary regional demand.

Market Dynamics:

Growth Drivers: Industrial automation expansion and Industry 4.0 adoption creating structured photoelectric sensor procurement across manufacturing sectors

The photoelectric sensor market’s growth is driven by the structural alignment between accelerating industrial automation investment and photoelectric sensors’ fundamental role as the detection layer enabling automated material handling, quality inspection, and process control across manufacturing operations. As industries strive to enhance efficiency, reduce errors, and cut down on labour costs, the adoption of automation technologies becomes crucial, with photoelectric sensors playing a vital role in automating processes by enabling precise object detection, counting, and positioning that integrate seamlessly into robotic systems, conveyor belts, and assembly lines ensuring seamless operations and high productivity.

Restraints: Price competition from emerging market manufacturers and integration complexity with legacy industrial control systems limiting premium sensor adoption

Intense price competition from emerging market photoelectric sensor manufacturers whose lower-cost commodity sensor offerings create margin pressure on established premium brands, particularly in price-sensitive applications where basic detection functionality without advanced diagnostic capability meets customer requirements, constrains average selling price growth across the commodity segment of the photoelectric sensor market. Each manufacturing customer whose procurement decision prioritises acquisition cost over advanced sensor capability creates competitive pressure that favours lower-cost alternatives over premium IO-Link enabled sensor offerings.

Opportunities: Packaging automation expansion and emerging market industrialisation creating substantial photoelectric sensor market growth frontiers

Packaging automation’s rapid expansion driven by e-commerce volume growth, food and beverage production scaling, and pharmaceutical regulatory compliance requirements creates substantial photoelectric sensor demand growth whose addressable market scales with global packaging line automation investment. Each new automated packaging line commissioned to serve growing e-commerce fulfilment or food and beverage production capacity creates photoelectric sensor procurement for product positioning, fill-level verification, and label placement confirmation whose growth trajectory the SNS Insider analysis identifies as the market’s fastest-growing application category.

Recent Developments:

-

2025: RS Group and Banner Engineering partnered to enhance Industry 4.0 accessibility by offering advanced photoelectric and Q90R radar sensors through RS’s distribution network, improving automation, precision, and performance monitoring across industrial applications.

-

2024: Banner Engineering expanded its Q5X series photoelectric sensor line with enhanced IO-Link diagnostic capability, providing real-time sensor health monitoring and predictive maintenance alerting that reduces unplanned production line downtime.

-

2023: Keyence Corporation launched a high-precision reflective photoelectric sensor for industrial automation, enabling improved object detection performance in challenging environments including high-vibration and variable lighting manufacturing conditions.

Photoelectric Sensor Market Key Players are:

-

Omron Corporation

-

SICK AG

-

Keyence Corporation

-

Rockwell Automation

-

Schneider Electric

-

Siemens AG

-

Pepperl+Fuchs SE

-

Banner Engineering Corp.

-

ifm electronic gmbh

-

Panasonic Industry Co., Ltd.

-

Honeywell International Inc.

-

Balluff GmbH

-

Autonics Corporation

-

Datalogic S.p.A.

-

Turck GmbH & Co. KG

-

Leuze electronic GmbH + Co. KG

-

Baumer Group

-

Eaton Corporation

-

Cognex Corporation

-

Wenglor Sensoric Group

Photoelectric Sensor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.27 Billion |

| Market Size by 2035 | USD 4.67 Billion |

| CAGR | CAGR of 7.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Retroreflective, Thru-Beam, Diffuse Reflective, Others) • By Light Source (Laser Beam, Infrared, LED) • By Range (Less than 100mm, 100–1000mm, 1001–10000mm, Above 10000mm) • By Application (Automotive & Transportation, Industrial Manufacturing, Packaging, Electronics, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Omron Corporation, SICK AG, Keyence Corporation, Rockwell Automation, Schneider Electric, Siemens AG, Pepperl+Fuchs SE, Banner Engineering Corp., ifm electronic gmbh, Panasonic Industry Co., Ltd., Honeywell International Inc., Balluff GmbH, Autonics Corporation, Datalogic S.p.A., Turck GmbH & Co. KG, Leuze electronic GmbH + Co. KG, Baumer Group, Eaton Corporation, Cognex Corporation, Wenglor Sensoric Group |

Frequently Asked Questions

The Photoelectric Sensor Market is expected to grow at a CAGR of 7.46% from 2026 to 2035.

The Photoelectric Sensor Market was valued at USD 2.27 Billion in 2025.

Industrial automation, Industry 4.0, e-commerce packaging, and industrialisation drive photoelectric sensor demand globally.

The Industrial Manufacturing segment dominated the Photoelectric Sensor Market.

Asia Pacific dominated the Photoelectric Sensor Market in 2025.

Get in Touch