Physical AI Market Report Scope & Overview:

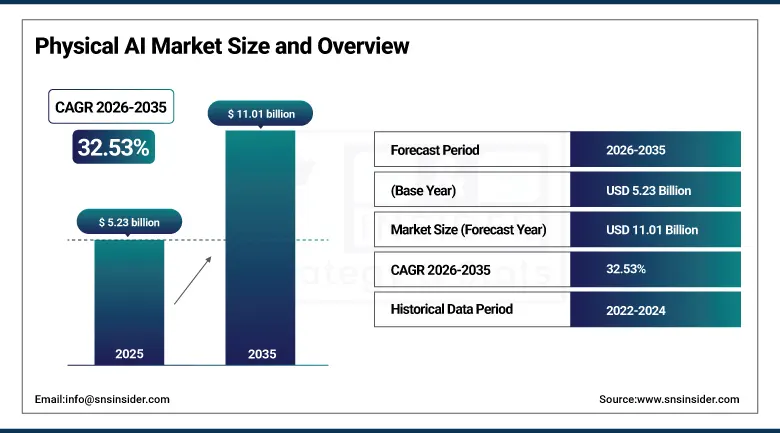

The Physical AI Market was valued at USD 5.23 billion in 2025 and is expected to reach USD 87.43 billion by 2035, growing at a CAGR of 32.53% from 2026–2035.

Physical AI represents the convergence of advanced artificial intelligence with embodied mechanical systems, enabling real-time computational architectures, and precisely controlled actuators. Unlike conventional software AI whose outputs are purely informational, physical AI systems produce consequences in the material world: a collaborative robot that adjusts its grip force in response to a deformable object, an autonomous mobile robot that re-plans its path around an unexpected obstacle, a surgical system that compensates for patient breathing motion during a minimally invasive procedure, or a humanoid robot that navigates an unstructured home environment while carrying out domestic tasks. The fusion of deep learning perception, multimodal language models, and high-performance edge computing into compact, power-efficient robotic platforms distinguishes physical AI from earlier generations of industrial automation.

NVIDIA's articulation of Physical AI as the next frontier of artificial intelligence, expressed through its Jetson Thor humanoid robot compute platform and Isaac simulation environment, combined with the extraordinary commercial success of Boston Dynamics' Spot and Stretch robots and start-ups including Figure AI, Agility Robotics, and Apptronik, signals that the physical AI market is transitioning from a research domain into a commercially significant industry.

Physical AI Market Size and Forecast

-

Market Size in 2026E: USD 6.93 Billion

-

Market Size by 2035: USD 49.73 Billion

-

CAGR: 32.53% from 2026 to 2033

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Physical AI Market - Request Free Sample Report

Physical AI Market Trends

- Foundation AI models are enabling robots to understand natural language instructions and perform diverse physical tasks with minimal reprogramming.

- Humanoid robot commercialization is accelerating as human-like form factors operate effectively in existing workplaces and infrastructure.

- Autonomous mobile robots are seeing wider adoption in warehouses due to e-commerce growth and labor shortages.

- Digital twin simulations are improving robot training efficiency by enabling large-scale virtual testing before deployment.

- Government and defense investments are increasing demand for autonomous robotic systems in logistics, surveillance, and hazardous operations.

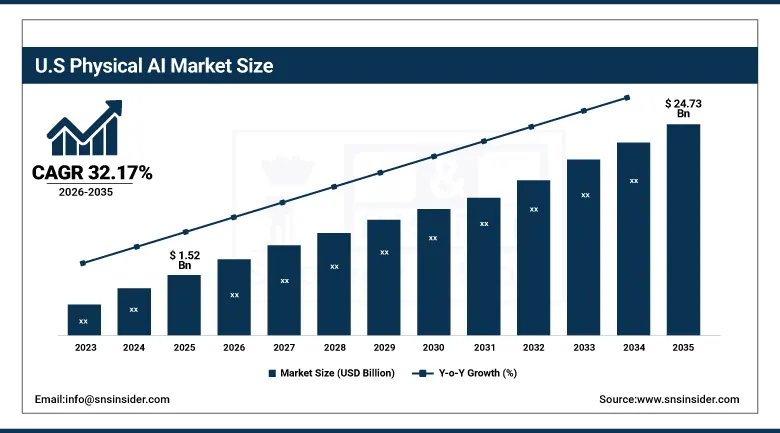

U.S. Physical AI Market Outlook

The U.S. Physical AI Market was valued at approximately USD 1.52 billion in 2025 and is expected to reach approximately USD 24.73 billion by 2035, growing at a CAGR of 32.17%, driven by high rates of automation adoption across manufacturing, logistics, healthcare, and defense sectors.

The United States is home to the established robotics leaders including Boston Dynamics, iRobot, Intuitive Surgical, and Covariant and the technology platform providers NVIDIA and Google DeepMind whose AI compute and model capabilities underpin a growing proportion of intelligent robotic systems. DARPA's sustained investment in autonomous ground vehicle, aerial drone, and humanoid robot research has generated the foundational technology demonstrations that have transferred into commercial physical AI products over successive technology maturation cycles, and the Department of Defense's growing procurement interest in autonomous logistics, surveillance, and tactical robotic systems.

The extraordinary concentration of venture capital investment in U.S. physical AI companies, including Amazon, Microsoft, and major automotive manufacturers, is creating a commercialisation pipeline that will expand the addressable physical AI product market in manufacturing, warehousing, retail, and home service applications over the 2026 to 2033 forecast period.

Physical AI Market Segment Analysis

-

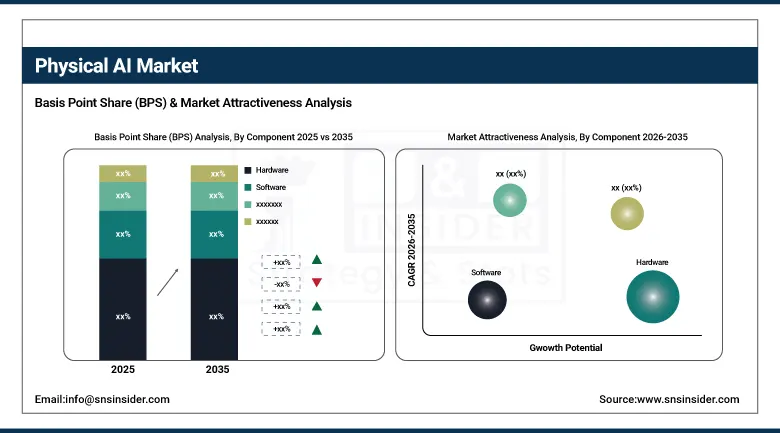

By Component, Hardware dominated with approximately 56.40% of revenues in 2025 as the foundational layer of robotic and autonomous systems encompassing sensors, actuators, mobility units, AI chips, and integrated mechatronic assemblies; Software is the fastest-growing segment at a CAGR of 34.10%.

-

By Technology, Computer Vision held the largest share at approximately 45.02% in 2025 as the fundamental enabling technology for object detection, navigation, inspection, and environment mapping across virtually all physical AI systems; Reinforcement Learning & Control Systems is the fastest-growing technology segment at a CAGR of 31.14%.

-

By Form Factor, Industrial Robots dominated with approximately 36.12% of revenues in 2025 through their established role in manufacturing, automotive, electronics, and heavy engineering; Cobots are the fastest-growing form factor at a CAGR of 35.12%.

-

By Deployment, On-device led with approximately 51.24% of revenues in 2025 as real-time processing, low-latency decision-making, and high reliability requirements for safety-critical operations favour edge-deployed AI; Cloud-based AI is the fastest-growing deployment at a CAGR of 38.61%.

-

By Application, Manufacturing & Automotive dominated with approximately 45.20% of revenues in 2025 through extensive robotics deployment for assembly, welding, inspection, and material handling; Healthcare is the fastest-growing application at a CAGR of 34.90%.

By Component, Hardware dominates, Software is expected to grow fastest

Hardware retained the dominant component position with approximately 56.40% of the Physical AI Market in 2025. The hardware layer of physical AI encompasses an extraordinary diversity of technology categories including vision sensors ranging from standard RGB cameras through stereo depth cameras, structured light sensors, LiDAR point cloud scanners, and thermal imagers; force and torque sensors that give manipulators the sense of touch needed for compliant assembly and human-safe collaboration; motor drives, servo actuators, and pneumatic systems that convert electrical signals into physical motion; and the AI inference accelerators, system-on-chip platforms, and edge computing modules that process sensor data at the speeds that real-time robot control requires.

Software is the fastest-growing component at a CAGR of 34.10% through 2035. The software layer spans real-time operating systems and robotic middleware frameworks such as ROS 2, perception stacks integrating sensor fusion from multiple modality inputs, motion planning algorithms that generate collision-free robot trajectories in dynamic environments, task and behaviour planning systems that interpret high-level goals into sequences of physical actions, and digital twin simulation environments that allow robot software to be trained and validated at scale before physical deployment. Foundation model providers including NVIDIA through its Isaac Lab simulation platform and Google DeepMind through its Gemini Robotics model family are establishing software platforms with the potential to become the dominant interfaces.

By Technology, Computer Vision dominates, Reinforcement Learning & Control Systems is expected to grow fastest

Computer Vision retained the largest technology share at approximately 45.02% of Physical AI Market revenues in 2025. Modern robotic computer vision systems combine convolutional neural networks for object detection and classification and specialised depth estimation algorithms that extract three-dimensional geometric information from camera images or LiDAR point clouds, collectively enabling robots to identify objects, infer their properties, estimate their precise positions. The maturity of computer vision relative to other physical AI technologies, combined with its applicability across virtually every physical AI application from quality inspection through autonomous navigation, explains its dominant market share and its position as the first AI technology module integrated into new robotic system designs.

Reinforcement Learning & Control Systems is the fastest-growing technology segment at a CAGR of 31.14% through 2035. The commercial deployment of sim-to-real transfer pipelines, where robots trained in physics simulation environments using reinforcement learning are directly deployed in physical environments with minimal additional training, is making reinforcement learning-based control practical at commercial scale for the first time. OpenAI's robotic dexterous manipulation research, Covariant's AI-powered pick-and-place systems, and Boston Dynamics' learned locomotion controllers all represent commercially significant reinforcement learning applications in physical AI that are establishing proof of value for the technology.

By Form Factor, Industrial Robots dominate, Cobots are expected to grow fastest

Industrial Robots retained the dominant form factor position with approximately 36.12% of Physical AI Market revenues in 2025, as the installed base of traditional industrial robots in automotive, electronics, metal fabrication, and consumer goods manufacturing represents the largest existing robotic hardware fleet available for AI capability upgrades. The six-axis articulated robot arm remains the workhorse format of industrial automation, deployed by thousands of manufacturers worldwide for welding, painting, and material handling applications where the combination of high speed, large payload capacity, and repeatability in structured environments delivers demonstrable productivity advantage. The transition of conventional industrial robots toward AI-enhanced versions capable of handling part variation, unstructured bin picking, and flexible manufacturing scenarios is one of the most immediately large upgrade cycles in the physical AI market.

Cobots are the fastest-growing form factor at a CAGR of 35.12% through 2035. Universal Robots' UR series, Fanuc's CRX family, and ABB's GoFa and SWIFTI cobots are the established leaders in a cobot market that is now being joined by AI-native cobot platforms from start-ups including Machina Labs and Vention that integrate physical AI capabilities from the ground up rather than adding AI modules to conventional cobot architectures. The application of physical AI to cobots is particularly transformative because cobots' physical proximity to human workers makes natural language instruction, gesture recognition, and learning by demonstration interaction modalities practically achievable in ways that are not relevant for caged industrial robots.

By Application, Manufacturing & Automotive dominates, Healthcare is expected to grow fastest

Manufacturing & Automotive retained the dominant application position with approximately 45.20% of Physical AI Market revenues in 2025, as the global automotive industry's transition toward electric vehicle production is simultaneously demanding higher precision in battery cell and pack assembly than conventional automation can reliably deliver and creating significant re-tooling investment cycles that manufacturing AI is positioned to address with flexible, reprogrammable robotic systems replacing dedicated hard automation. The electronics manufacturing sector's requirement for sub-millimetre precision in printed circuit board assembly, semiconductor packaging, and display panel bonding is driving adoption of AI vision-guided robotic systems . Toyota, BMW, and Volkswagen has announced substantial investments in AI-enabled flexible manufacturing systems.

Healthcare is the fastest-growing application segment at a CAGR of 34.90% through 2035, as the combination of aging populations creating increasing demand for surgical and rehabilitation services, clinical staff shortages limiting healthcare system capacity. Intuitive Surgical's da Vinci system has demonstrated over two decades of commercial operation that surgeons and patients will choose robot-assisted minimally invasive approaches for an expanding range of procedures as the evidence base for outcome advantages accumulates. The next generation of surgical physical AI is moving beyond teleoperation, where a surgeon controls every instrument movement in real time, toward semi-autonomous surgical assistance while the surgeon supervises and manages the non-routine elements.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Physical AI Market Insights

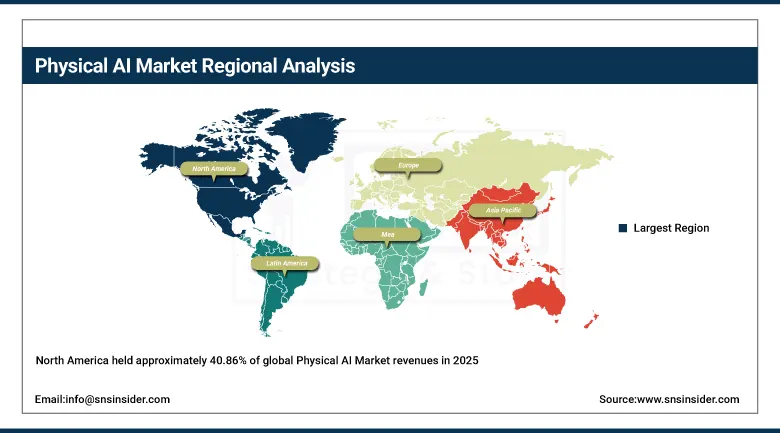

North America held approximately 40.86% of global Physical AI Market revenues in 2025, with the United States accounting for approximately 87.4% of North American revenues. The region's market position reflects the co-location of the most advanced AI research organisations and the presence of the major technology platform providers NVIDIA, Intel, and Qualcomm whose AI hardware and software tools power a large proportion of global physical AI deployments. The U.S. Department of Defense's investments in autonomous systems through DARPA programmes, the Army Research Laboratory, and direct procurement of unmanned ground and aerial vehicles create a defence market for physical AI that sustains technology development at capability levels beyond what commercial economics currently justify.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Physical AI Market Insights

Asia Pacific is the fastest-growing physical AI market with a projected CAGR of 33.51% from 2026 to 2035, driven by China's extraordinary investment in industrial robotics as part of its Made in China 2025 and robot density improvement initiatives and the rapid growth of e-commerce logistics automation across the region. China accounts for approximately 61.7% of Asia Pacific physical AI revenues, reflecting its position as both the world's largest industrial robot deployment market by annual unit volume and the home of significant physical AI technology companies including DJI in drone systems, Mech-Mind Robotics in AI vision, and UBTECH Robotics in humanoid robot development. The Chinese government's explicit policy support for robot manufacturing and deployment through subsidies, preferential procurement, and research funding creates a policy-driven demand environment that reinforces commercial adoption incentives.

Europe Physical AI Market Insights

Europe is a technically sophisticated physical AI market anchored by Germany's world-leading automotive and machine tool manufacturing industries. KUKA, acquired by China's Midea Group, and ABB, headquartered in Switzerland, are the dominant European industrial robot and cobot manufacturers with global market positions, while Siemens' industrial automation and digital twin platforms provide the software infrastructure within which European manufacturers integrate physical AI capabilities. The European Union's regulatory approach to AI through the AI Act's provisions on high-risk autonomous systems creates a compliance environment that raises deployment standards for physical AI in safety-critical applications including surgical robots, autonomous vehicles, and industrial collaborative robots operating near human workers.

Latin America and MEA Physical AI Market Insights

Latin America and the Middle East and Africa are emerging physical AI markets where the combination of manufacturing sector modernisation investment, infrastructure development programmes, and in the case of MEA, substantial sovereign wealth fund-backed technology investment, is creating initial demand for intelligent robotic systems across production, logistics, and construction applications. Brazil leads Latin American physical AI adoption with approximately 44.2% of regional revenues, primarily through automotive manufacturing automation investment from established OEM facilities and growing food and beverage processing automation.

Saudi Arabia leads MEA physical AI investment at approximately 38.4% of regional revenues through its Vision 2030 programme's commitments to manufacturing sector development, smart city infrastructure, and logistics automation in support of its economic diversification strategy.

Market Dynamics

Growth Drivers: Foundation model breakthroughs enabling generalised robotic intelligence across tasks, combined with labour market structural pressures

The primary structural growth driver for the physical AI market is the convergence of two independent forces that are reinforcing each other to create an unprecedented expansion of robotic system deployment. On the technology side, the maturation of deep learning perception, the development of foundation models that provide robots with generalisable world knowledge and instruction-following capability, and the dramatic improvement in edge AI compute performance per watt delivered by successive NVIDIA Jetson, Qualcomm Robotics RB, and Intel Meteor Lake generations are collectively enabling physical AI systems to perform tasks that were computationally infeasible or too economically costly to deploy at commercial scale just three to five years ago. On the economic side, structural labour shortages in manufacturing and the demonstrated productivity, quality, and operational continuity advantages of robotic automation are creating financial justifications for physical AI investment.

Restraints: High system integration complexity and cost, hardware reliability challenges in unstructured environments

A significant restraint on the physical AI market is the substantial total cost of ownership that physical AI system deployment entails beyond the visible hardware and software acquisition cost, ongoing support and maintenance contracts, and the productivity loss during installation and commissioning periods. Physical AI systems operating in unstructured real-world environments where lighting conditions, surface textures, object positions, and human colleague behaviour are variable and unpredictable face reliability challenges that do not arise in the structured, controlled conditions for which traditional industrial automation was designed, and managing the long tail of edge cases where physical AI systems encounter situations outside their training distribution requires ongoing human supervision and system refinement investment that adds to operational cost. Safety certification requirements for cobots operating near human workers, surgical robots interacting with patients, and autonomous vehicles operating in public spaces impose rigorous validation and testing obligations that extend development timelines and add regulatory compliance cost that smaller physical AI companies find challenging to absorb.

Opportunities: Humanoid robot commercialisation opening previously unautomatable labour markets, physical AI-as-a-service models lowering adoption barriers

The commercialisation of general-purpose humanoid robots represents the most transformative long-term opportunity in the physical AI market, as the ability to deploy a bipedal, dexterous robot into workspaces designed for human workers addresses the fundamental constraint. If humanoid robots achieve the combination of capability, reliability, and total cost of ownership that makes them commercially competitive with human labour for a broad range of physical tasks, the market for physical AI would expand by orders of magnitude beyond the current industrial and healthcare application base. Physical AI-as-a-service business models, where robot system operators provide robotic automation capability on a subscription or per-task basis rather than requiring customers to purchase and operate robotic equipment themselves, are lowering adoption barriers for mid-market and small enterprise customers who cannot justify capital expenditure on robotic systems but can evaluate operational expenditure-based automation against their existing labour costs on a task-by-task basis.

Recent Developments:

-

2025: NVIDIA launched its Jetson Thor AI chip platform specifically designed for humanoid robot compute requirements, providing the highest performance per watt edge AI processing capability available for on-robot intelligence and positioning NVIDIA as the foundational compute infrastructure provider for the humanoid robot commercialisation wave.

-

2025: Google DeepMind unveiled Gemini Robotics and Gemini Robotics-ER, two robotics-oriented foundation models enabling robots to perform vision-language-action tasks and adapt to new physical tasks without explicit task-specific training, demonstrating that the large multimodal model architectures developed for digital AI applications can be extended to physical world manipulation.

-

2025: Boston Dynamics continued commercial expansion of its Spot quadruped and Stretch logistics robot platforms, adding new AI-powered inspection, data collection, and autonomous navigation capabilities through software updates that extend the operational value of deployed robot fleets without hardware replacement.

-

2025: Figure AI and BMW announced an expanded agreement for Figure's humanoid robots to perform material handling and assembly assistance tasks at BMW's Spartanburg vehicle manufacturing facility, providing one of the first high-profile commercial deployments of humanoid physical AI in an automotive manufacturing environment.

Physical AI Market Key Players

-

SoftBank Robotics Group

-

ABB

-

Toyota Motor Corporation

-

FANUC

-

KUKA AG

-

Siemens

-

Boston Dynamics

-

Tesla

-

NVIDIA

-

Google DeepMind

-

Agility Robotics

-

Mech-Mind Robotics

-

Hanson Robotics

-

Universal Robots

-

iRobot

-

Intuitive Surgical

-

Doosan Robotics

-

Covariant

-

Apptronik

-

UBTech

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.23 Billion |

| Market Size by 2035 | USD 87.43 Billion |

| CAGR | CAGR of 32.53% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Technology (Computer Vision, Reinforcement Learning & Control Systems, Natural Language Processing, Machine Learning & Deep Learning, Others) • By Form Factor (Industrial Robots, Cobots, Autonomous Mobile Robots, Humanoid Robots, Drones & UAVs, Others) • By Deployment (On-device, Cloud-based AI, Hybrid) • By Application (Manufacturing & Automotive, Healthcare, Logistics & Supply Chain, Defense & Security, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | SoftBank Robotics Group, ABB, Toyota Motor Corporation, FANUC, KUKA AG, Siemens, Boston Dynamics, Tesla, NVIDIA, Google DeepMind, Agility Robotics, Mech-Mind Robotics, Hanson Robotics, Universal Robots, iRobot, Intuitive Surgical, Doosan Robotics, Covariant, Apptronik, UBTech |

Get in Touch