Autocollimators Market Report Scope & Overview:

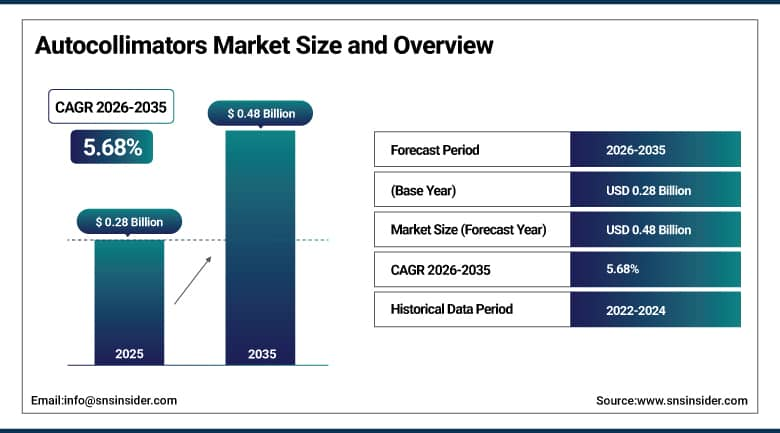

The Autocollimators Market was valued at USD 0.28 Billion in 2025 and is expected to reach USD 0.48 Billion by 2035, growing at a CAGR of 5.68% from 2026 to 2035.

The global autocollimators market is strategically positioned in the field of precision optical metrology and angular measurement instrumentation as the primary measurement technology for industries where sub-arc-second angular accuracy is the difference between the safety, performance, and quality compliance of manufactured components, assembled systems, and calibrated research equipment. Autocollimators project a collimated beam of light onto a reflective surface and measure the angular displacement of the returned beam with respect to the emitted reference. The non-contact angular measurement with extremely high resolution is unobtainable with conventional mechanical gauging methods. The market consists of visual, digital and laser-based autocollimators for precision alignment and angle measurement with advanced systems providing real-time analysis and ultra-high accuracy of less than 0.01 arc seconds.

Autocollimators are capable of achieving angular measurement resolutions below 0.01 arc-seconds, while advanced digital systems can perform over 1,000 measurements per second, enabling real-time precision alignment in aerospace, semiconductor, and optical manufacturing environments.

Market Size and Forecast:

-

Market Size in 2026E: USD 0.29 Billion

-

Market Size by 2035: USD 0.48 Billion

-

CAGR: 5.68% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Autocollimators Market - Request Free Sample Report

Autocollimators Market Trends:

-

Integration of digital autocollimators with Industry 4.0 and automated inspection systems is accelerating demand for real-time measurement solutions.

-

Miniaturized CCD and CMOS sensors are enabling compact autocollimators for portable calibration and on-machine metrology applications.

-

Rising aerospace, defense, and space program investments are boosting demand for ultra-high-precision sub-arc-second alignment systems.

-

Adoption of laser autocollimators for long-range alignment in telescopes, accelerators, and shipbuilding is expanding market opportunities.

-

Growing ISO 17025 accreditation requirements are driving investments in traceable angular measurement and calibration equipment.

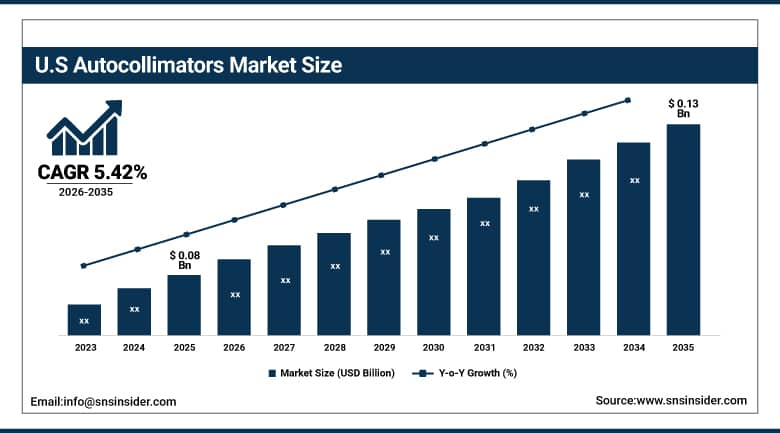

U.S. Autocollimators Market Outlook:

The U.S. Autocollimators Market was valued at USD 0.08 Billion in 2025 and is expected to reach USD 0.13 Billion by 2035, growing at a CAGR of 5.42%.

The United States has the world’s largest national autocollimator market with the world’s largest aerospace and defence R&D and manufacturing ecosystem, one of the world’s most advanced semiconductor and photonics manufacturing bases, and the world’s most extensive network of nationally accredited precision metrology laboratories and calibration service providers. The U.S. market’s exceptional depth is reflective of the country’s concurrent leadership in a number of end-use sectors that depend on the precision of autocollimator-grade angular measurement, such as manufacturing of military optical systems, fabrication of commercial satellites and space telescopes, inspection of advanced automotive powertrains and chassis, and the photonics and laser technology industry, which requires sub-arc-second validation of the alignment of optical cavities and beam delivery systems during assembly.

The U.S. Precision machine tool alignment using autocollimators can reduce geometric positioning errors by up to 40–60% compared with conventional alignment methods. Aerospace, defense, semiconductor, and optical engineering industries collectively account for over 65% of global autocollimator equipment demand, reflecting the need for sub-micron manufacturing accuracy.

Autocollimators Market Segment Analysis

-

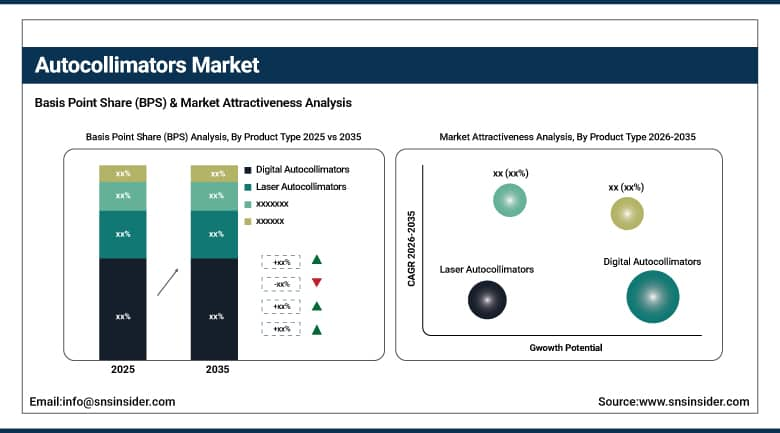

By Product Type, digital autocollimators dominated the market with 36.15% share in 2025, while laser autocollimators are the fastest growing product type with the highest CAGR of 6.40% from 2026 to 2035.

-

By Measurement Range, up to 100 arc seconds dominated the market with 48.21% share in 2025, while above 500 arc seconds is the fastest growing range with the highest CAGR of 5.99% from 2026 to 2035.

-

By Application, angle measurement dominated the market with 30.15% share in 2025, while optical component testing is the fastest growing application with the highest CAGR of 7.10% from 2026 to 2035.

-

By End-Use Industry, aerospace & defense dominated the market with 33.06% share in 2025, while healthcare & medical devices are the fastest growing end-use industry with the highest CAGR of 8.35% from 2026 to 2035.

-

By Technology, CCD-based autocollimators dominated the market with 41.06% share in 2025, while CMOS-based autocollimators are the fastest growing technology with the highest CAGR of 6.36% from 2026 to 2035.

By Product Type, digital autocollimators dominate the autocollimators market, while laser autocollimators are the fastest-growing segment.

Digital autocollimators segment dominated the market with the highest revenue share of about 36.15% in 2025 due to their superior measurement resolution, real-time digital output compatibility with computer-integrated quality management systems, and their ability to provide objective, operator-independent angular measurement data that satisfies the documentation and traceability requirements of ISO 9001, AS9100, and IATF 16949 quality management standards. The segment's leadership reflects the broad-based migration of precision manufacturing quality assurance operations from subjective visual measurement techniques toward digital instrument platforms that enable automated data logging, statistical process control integration, and seamless connectivity with enterprise metrology software ecosystems.

Laser autocollimators segment is estimated to register the highest CAGR of 6.40% during the forecast period of 2026–2035 owing to the expanding range of applications that require angular measurement over working distances exceeding the practical limits of conventional LED-source autocollimators, including large-scale machine tool geometric error assessment, accelerator beamline alignment, shipbuilding structural alignment verification, and large telescope primary mirror panel positioning. The superior beam coherence and intensity of laser light sources enable laser autocollimators to maintain measurement accuracy over working distances of tens of meters, extending the instrument's operational envelope into large-scale civil and industrial infrastructure alignment applications that are experiencing growth through global manufacturing facility expansion and scientific research infrastructure investment.

By Measurement Range, up to 100 arc seconds dominates the autocollimators market, while above 500 arc seconds is the fastest-growing segment.

Up to 100 arc seconds segment dominated the market with the largest revenue share of about 48.21% in 2025 attributed to the concentration of the highest-value precision metrology applications within this measurement range, including aerospace optical system alignment, semiconductor lithography optic calibration, precision telescope mirror positioning, and research-grade angular measurement tasks where sub-arc-second resolution determines the functional adequacy of the measurement system. The segment's dominance reflects the premium pricing commanded by high-resolution autocollimator instruments relative to lower-precision alternatives and the structural depth of buyer demand within aerospace, defense, and advanced research sectors that consistently specify high-resolution angular measurement capability as a mandatory instrument requirement.

Above 500 arc seconds segment is projected to witness the fastest CAGR of 5.99% during 2026–2035 due to the expanding industrial adoption of autocollimators for general-purpose machine tool inspection, construction equipment alignment, and quality assurance tasks in medium-precision manufacturing environments where wider measurement range instruments accommodate the larger angular deviations characteristic of less precisely controlled manufacturing processes. The segment's growth is further supported by the cost advantage of wider-range instruments that makes autocollimator technology economically accessible to a broader industrial buyer base beyond the specialized precision metrology and aerospace sectors that have historically driven market development.

By Application, angle measurement dominates the autocollimators market, while optical component testing is the fastest-growing segment.

Angle measurement segment emerged as the market leader with a dominant share of around 30.15% in 2025 owing to its fundamental role as the primary application driver across virtually all autocollimator-using industries, encompassing machine tool axis squareness and straightness verification, prism and polygon face angle calibration, precision rotation stage angular position measurement, and angular encoder calibration. The segment's comprehensive coverage of both the highest-precision research and defense applications and the broader industrial machine tool inspection market provide it with the widest buyer base and most diverse revenue foundation of any autocollimator application category.

Optical component testing segment is anticipated to record the fastest CAGR of 7.10% throughout the forecast period of 2026–2035 driven by the accelerating expansion of photonics, fiber optic communications, LiDAR sensor manufacturing, augmented reality optics production, and defense electro-optical system fabrication, all of which require rigorous lens and mirror surface form and angular alignment verification using autocollimator-based wavefront measurement techniques. The compound growth in photonic component demand from telecommunications infrastructure upgrades to 5G and 6G networks, the automotive LiDAR market expansion enabled by autonomous driving system development, and defense investment in high-power laser system optics is creating a broad and diversifying buyer base for autocollimator optical testing applications.

By End-Use Industry, aerospace & defense dominates the autocollimators market, while healthcare & medical devices are the fastest-growing segment.

Aerospace & defense segment dominated the autocollimators market with the highest revenue share of about 33.06% in 2025 owing to the sector's uniquely stringent angular measurement requirements, the high per-instrument procurement values associated with defense-specification autocollimator systems, and the breadth of alignment and calibration applications spanning aircraft inertial navigation system boresighting, guided munition seeker head optical alignment, space telescope mirror co-phasing, and satellite attitude sensor calibration. The segment's purchasing power and specification-driven procurement behaviour have historically shaped the performance benchmark for the entire autocollimator market, with defense program requirements driving instrument manufacturers to develop technological capabilities that subsequently diffuse into commercial precision manufacturing and research applications.

Healthcare & medical devices segment is projected to witness the fastest CAGR of 8.35% during the forecast period of 2026–2035 due to the growing precision optics content in surgical laser systems, ophthalmic diagnostic and treatment instruments, medical endoscope optical assemblies, and radiotherapy beam delivery systems that require autocollimator-grade angular alignment verification during manufacturing and periodic calibration cycles.

By Technology, CCD-based autocollimators dominate the autocollimators market, while CMOS-based autocollimators are the fastest-growing segment.

CCD-based autocollimators segment dominated the market with the highest revenue share of about 41.06% in 2025 due to the superior image uniformity, low noise characteristics, and established measurement performance record of charge-coupled device detector technology that has made CCD-based systems the trusted standard for highest-precision angular measurement in defense, aerospace, and research metrology applications. CCD detector arrays offer the spatial uniformity and measurement repeatability required for sub-arc-second resolution autocollimator systems, and the segment benefits from decades of application validation data across critical measurement programs that create institutional preference for proven CCD-based instrument platforms in high-stakes procurement decisions.

CMOS-based autocollimators segment is projected to witness the fastest CAGR of 6.36% during 2026–2035 driven by the rapid advancement of complementary metal-oxide-semiconductor detector technology that is progressively closing the image quality gap relative to CCD sensors while delivering significant advantages in readout speed, power consumption, on-chip processing capability, and manufacturing cost that make CMOS-based systems increasingly attractive for high-throughput production environment autocollimator applications.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

88.54% |

|

Europe |

Germany |

32.50% |

|

Asia Pacific |

China |

43.80% |

|

Middle East & Africa |

UAE |

28.40% |

|

Latin America |

Brazil |

44.20% |

North America Autocollimators Market Insights

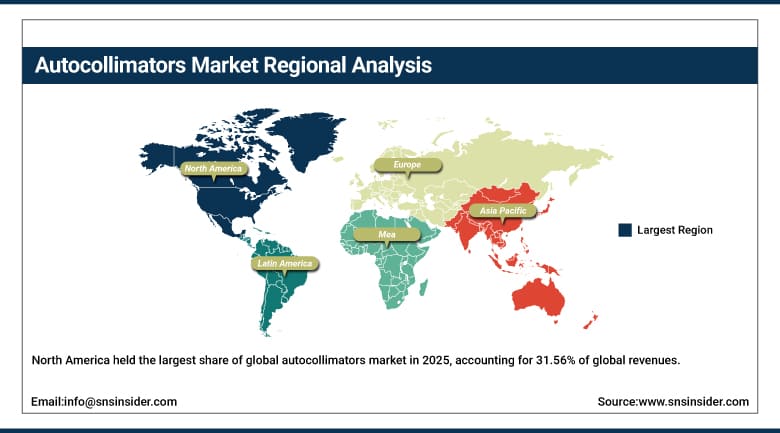

North America held the largest share of global autocollimators market in 2025, accounting for 31.56% of global revenues. United States accounted for 88.54% of regional revenue. The region’s market leadership is based on legendary concentration of aerospace and defence prime contractors and their ecosystems of suppliers; the world’s most sophisticated manufacturing base for semiconductors and photonics; and a national precision metrology infrastructure at NIST that sets the standards for angular measurement that American industrial and research institutions calibrate against. This creates stable and technically demanding institutional market for high performance autocollimator systems, which directly contributes to the revenue concentration witnessed in North America. The U.S. defence procurement system’s steady investment in advanced optical sensor, directed energy, and precision guidance technologies.

68% of aerospace calibration labs use autocollimators for angular alignment validation, Driven by high defense and aircraft manufacturing precision requirements across the U.S. ecosystem. Automated alignment systems reduce inspection cycle time by ~35–45% in machine tool calibration High industrial automation penetration improves throughput in precision engineering workflows. Over 70% of ISO/IEC 17025 accredited metrology labs utilize optical angular measurement tools

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Autocollimators Market Insights

Europe is the second-largest regional autocollimators market in terms of revenue share in 2025, where Germany has a higher share in regional revenue. The worldwide importance of the continent in the world of precision engineering and machine tool manufacturing has, historically, contributed to influence both the technical development of autocollimator instrumentation and the extent of European industrial demand for high-precision angular measurement capability, which has been reflected in the continued market position of Europe. The world’s leading autocollimator manufacturers are based in Germany, Switzerland, and the United Kingdom including Taylor Hobson, Möller-Wedel Optical, whose market presence reflects the scientific and engineering depth of European optical metrology expertise and the sustained domestic industrial demand that has supported continuous instrument development investment.

Asia Pacific Autocollimators Market Insights

Asia Pacific is the fastest growing regional autocollimators market at a CAGR of 6.25% through 2035. China claims a greater proportion of Asia Pacific revenues, boosted by the country's huge and rapidly modernising precision manufacturing industry, substantial government investment in domestic aerospace and satellite program development, and the gradual adoption of internationally recognised metrology standards that requires Chinese manufacturers to buy traceable angular measurement instrumentation to satisfy export market quality demands. Japan is a market of exceptional technical depth with world-class precision machinery, robotics and optical component manufacturing industries.

Domestic instrument manufacturers including Nikon Corporation and Mitutoyo Corporation serve the domestic market as well as global customers with high-performance autocollimator platforms developed to exacting Japanese industrial quality standards.

China's manufacturing sector, which accounts for 28% of global manufacturing output by value, High-speed digital autocollimators used in 60% of automated production lines. Mass manufacturing scale requires rapid alignment and inspection cycles. Measurement throughput exceeding 1,000+ readings/sec in 45% of advanced facilities Supports high-volume electronics and precision component production

MEA & Latin America Autocollimators Market Insights

The Middle East and Africa and Latin America are becoming increasingly important growth markets for the autocollimators industry. New institutional demand for precision angular measurement instrumentation is being driven by regional industrialisation programs, defence modernisation investments and research infrastructure development. The UAE, which contributed more to MEA regional revenues, is the main regional entry market through its highly-developed manufacturing free zone infrastructure, defence technology procurement programs associated with the Abu Dhabi-based defence industry complex, and internationally-affiliated university research centres that use internationally-standardized precision metrology equipment.

Brazil's roughly share of regional revenues in Latin America points to the country's aerospace manufacturing sector, with a focus on Embraer's commercial and defence aircraft programs, its established community of researchers in precision instrumentation centred at the national metrology institute INMETRO, and the growing precision machining and automotive component manufacturing sector in São Paulo state that is increasingly implementing internationally traceable quality assurance practices. Mexico presents the region’s most dynamic opportunity for growth with the expansion of automotive and aerospace component manufacturing within global supply chains increasingly demanding supplier quality management system accreditation with traceable angular measurement capability.

Less than 30% penetration of laser-based systems in industrial applications. Cost sensitivity limits adoption of high-end optical metrology tools in Latin America. 55% of aerospace maintenance centres use autocollimators for alignment verification. Driven by airline hubs in UAE, Saudi Arabia, and South Africa. Oil & gas precision inspection applications account for 50% usage of angular measurement tools used in turbine alignment and rotating equipment calibration

Growth Drivers: Precision manufacturing quality requirements and defense optical system investment

The demand for high-precision angular measurement solutions with the resolution, repeatability and measurement traceability that can only be consistently achieved with autocollimator-class instrumentation, due to increased dimensional and angular tolerance specifications in the aerospace, defence, semiconductor and advanced manufacturing industries, is driving the autocollimator market. The global aerospace industry’s shift to next generation aircraft with composite structural systems, sophisticated avionics and sensor packages and high precision engine components is broadening the scope of manufacturing operations requiring autocollimator grade angular verification as part of their quality assurance process documentation. The need for autocollimators with sub-arc-second accuracy in tough environments is being driven by defence spending on hypersonic vehicles, laser weapons, quantum sensing and satellite optics.

Restraints: High instrument cost and specialized operational expertise requirements

The autocollimators market faces significant demand-side constraints due to the high capital investment required for high-performance digital and laser autocollimator systems, which can command purchase prices ranging from several thousand dollars for basic digital instruments, to well over USD 50,000 for research-grade laser autocollimator systems with full software and calibration packages, creating a financial barrier that limits adoption within smaller precision manufacturing enterprises and research institutions operating under constrained capital equipment budgets. An additional barrier to adoption is the need for operational expertise to properly configure, align, and interpret the autocollimator measurement data as the accuracy of instrument measurements is sensitive to environmental conditions such as vibration, thermal gradients, and air turbulence that experienced metrology personnel must identify and mitigate.

Opportunities: Industry 4.0 integration and photonics sector expansion

The global manufacturing industry’s increasing application of Industry 4.0 principles as they relate to connected measurement instruments, real-time quality data analytics and automated inspection system integration presents a revolutionary opportunity for autocollimator manufacturers to develop digitally connected instrument platforms that deliver measurement data directly into manufacturing execution systems, quality management databases and statistical process control software without the need for manual data transcription. The possibility to develop autocollimator instruments with Ethernet, OPC-UA and industrial wireless connectivity, as well as standardised measurement data output formats compatible with leading metrology software platforms.

Recent Developments

-

2026: Möller-Wedel Optical GmbH announced the ELCOMAT 3000 Pro, an upgraded version of its flagship electronic autocollimator with extended measurement range, improved low-light performance, and enhanced Bluetooth connectivity for wireless integration with production floor quality management networks.

-

2026: Renishaw plc expanded its XL-80 laser measurement system product family with a new autocollimator accessory enabling direct angular measurement alongside linear interferometry within a unified multi-axis machine tool geometric error assessment workflow compatible with its Renishaw Central data management platform.

-

2025: Taylor Hobson Ltd. launched the Talyvel 6 Electronic Level and Autocollimator system with enhanced digital connectivity features, including USB-C data output and compatibility with the company's updated Ultra software platform for real-time straightness and flatness measurement data visualization.

-

2025: TRIOPTICS GmbH introduced the OptiAngle 6 digital autocollimator with integrated CMOS detector technology and an enhanced graphical user interface designed for optical lens and mirror centration measurement in high-volume precision optics manufacturing production environments.

Autocollimators Market Key Players

-

Taylor Hobson Ltd.

-

Möller-Wedel Optical GmbH

-

Davidson Optronics Inc.

-

Micro-Radian Instruments Inc.

-

Nikon Corporation

-

Carl Zeiss AG

-

PLX Inc.

-

Edmund Optics Inc.

-

HAAG-STREIT Group

-

Optodyne Inc.

-

Thorlabs Inc.

-

Newport Corporation

-

Mitutoyo Corporation

-

Renishaw plc

-

SmarAct GmbH

-

Ametek Inc.

-

S-T Industries Inc.

-

KOE Co., Ltd.

Autocollimators Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.28 Billion |

| Market Size by 2035 | USD 0.48 Billion |

| CAGR | CAGR of 5.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Visual Autocollimators, Digital Autocollimators, Electronic Autocollimators, Laser Autocollimators) • By Measurement Range (Up to 100 Arc Seconds, 100–500 Arc Seconds, Above 500 Arc Seconds) • By Application (Angle Measurement, Alignment & Calibration, Surface Flatness Testing, Machine Tool Inspection, Optical Component Testing, Others) • By End-Use Industry (Aerospace & Defense, Automotive, Manufacturing & Industrial Machinery, Research & Metrology Laboratories, Healthcare & Medical Devices, Others) • By Technology (CCD-Based Autocollimators, CMOS-Based Autocollimators, Laser-Based Systems, Optical Lens-Based Systems) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Taylor Hobson Ltd., Möller-Wedel Optical GmbH, TRIOPTICS GmbH, Davidson Optronics Inc., Micro-Radian Instruments Inc., Nikon Corporation, Carl Zeiss AG, PLX Inc., Edmund Optics Inc., HAAG-STREIT Group, Optodyne Inc., Thorlabs Inc., Newport Corporation, Mitutoyo Corporation, Renishaw plc, Hexagon AB, SmarAct GmbH, Ametek Inc., S-T Industries Inc., KOE Co., Ltd. |

Frequently Asked Questions

The autocollimators market is expected to grow at a CAGR of 5.68% from 2026 to 2035.

The autocollimators market was valued at USD 0.28 Billion in 2025.

The primary growth drivers include tightening angular tolerance requirements across aerospace, defense, semiconductor, and advanced manufacturing industries. Additional growth is fuelled by expanding photonics/LiDAR production, rising defense optical programs, and Industry 4.0-enabled digital metrology adoption.

Optical Component Testing is the fastest-growing application segment in the autocollimators market, with a CAGR of 7.10% from 2026 to 2035.

North America dominated the autocollimators market in 2025, holding 31.56% of global revenues, with the United States accounting for 88.54% of North American revenues.

Get in Touch