3D Eye Tracking Software Market Report Scope & Overview:

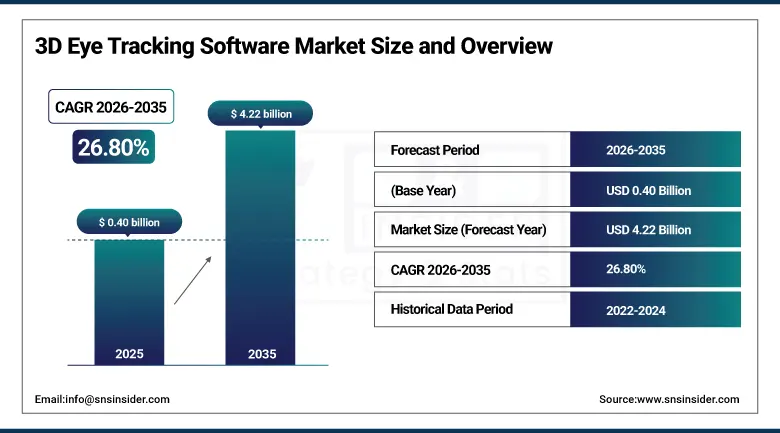

The 3D Eye Tracking Software Market was valued at USD 0.40 Billion in 2025 and is expected to reach USD 4.22 Billion by 2035, growing at a CAGR of 26.80% from 2026 to 2035.

The global 3D eye tracking software market has emerged as one of the fastest growing segments in the broader human-computer interaction and behavioural analytics technology space, driven by the convergence of advanced computer vision algorithms, real-time gaze mapping capabilities, and the increasing integration of eye tracking functionality into enterprise-level research, automotive safety, medical diagnostics, and immersive consumer entertainment platforms. Three-dimensional eye tracking software provides depth-aware fixation mapping, precise vergence and saccade analysis, and robust performance across variable ambient lighting and head-pose conditions, enabling application-grade accuracy that simultaneously satisfies the stringent technical requirements of clinical neuroscience, military pilot monitoring and extended reality user experience optimisation, unlike legacy two-dimensional gaze estimation systems.

Tobii AB reported that more than 5,000 organizations worldwide utilize its eye-tracking technologies across research, healthcare, automotive, gaming, and human-computer interaction applications, highlighting the broad commercial penetration of software-enabled gaze analytics platforms and the growing enterprise demand for behavioral data insights derived from eye movement tracking.

Market Size and Forecast

-

Market Size in 2026E: USD 0.50 Billion

-

Market Size by 2035: USD 4.22 Billion

-

CAGR: 26.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on 3D Eye Tracking Software Market - Request Free Sample Report

3D Eye Tracking Software Market Trends

-

Integration with XR headsets and spatial computing platforms is accelerating adoption across gaming, training, and immersive digital experiences.

-

AI-powered gaze analytics and cognitive load assessment are transforming eye tracking software into advanced behavioural intelligence platforms.

-

Growing deployment of driver monitoring systems (DMS) in vehicles is creating strong demand for eye tracking software in the automotive sector.

-

Cloud-based platforms are lowering implementation costs and expanding adoption among enterprises, researchers, and academic institutions.

-

Increasing use of eye-tracking biomarkers for neurological and cognitive assessment is driving growth in healthcare-focused software solutions.

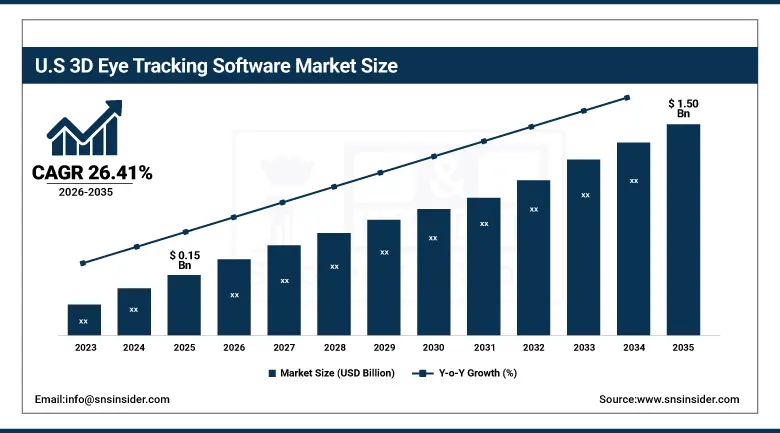

U.S. 3D Eye Tracking Software Market Outlook

The U.S. 3D Eye Tracking Software Market was valued at USD 0.15 Billion in 2025 and is expected to reach USD 1.50 Billion by 2035, growing at a CAGR of 26.41%.

The United States is the single largest national market worldwide for 3D eye tracking software, owing to the country’s unmatched concentration of enterprise technology buyers, federally funded neuroscience and human factors research programs, leading automotive and aerospace original equipment manufacturers, and the world’s most developed extended reality developer and consumer ecosystem. The structural demand drivers in the U.S. market are based on an exceptionally broad range applications, including the Department of Defence and contractors investing in eye tracking-enabled pilot fatigue monitoring and threat assessment systems. Academic medical centers are adopting gaze analysis software to support neurological disorder assessment and cognitive health research. Consumer technology companies are integrating gaze-contingent rendering into VR/XR headsets to enhance visual quality while reducing processing demands.

The U.S. National Institutes of Health allocated over USD 45 billion in research funding in fiscal year 2024, with neuroscience and vision research among the prioritized areas, representing a significant institutional funding base for clinical eye tracking software applications across academic medical research centers that are major enterprise buyers for precision 3D gaze analysis platforms.

3D Eye Tracking Software Market Segment Analysis

-

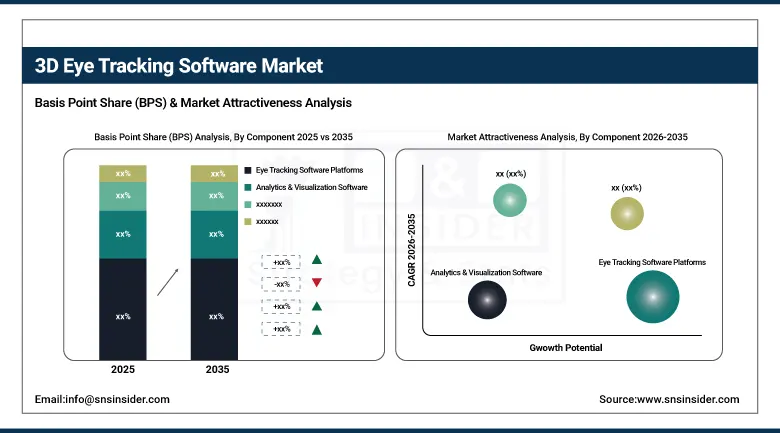

By Component, eye tracking software platforms dominated the market with 42.03% share in 2025, while SDKs & integration tools are the fastest growing component with the highest CAGR of 27.91% from 2026 to 2035.

-

By Deployment Mode, cloud-based deployment dominated the market with 58.09% share in 2025, while cloud-based is also the fastest growing deployment mode with the highest CAGR of 27.22% from 2026 to 2035.

-

By Tracking Type, remote eye tracking dominated the market with 34.06% share in 2025, while wearable eye tracking is the fastest growing tracking type with the highest CAGR of 27.37% from 2026 to 2035.

-

By Application, healthcare & medical research dominated the market with 28.15% share in 2025, while gaming & entertainment is the fastest growing application with the highest CAGR of 28.35% from 2026 to 2035.

By Component, eye tracking software platforms dominate the 3D eye tracking software market, while SDKs & integration tools are the fastest-growing segment.

Eye tracking software platforms segment dominated the market with the highest revenue share of about 42.03% in 2025 due to their role as the foundational commercial layer through which enterprise buyers license core gaze estimation, fixation analysis, and data visualization capabilities from leading platform vendors. The platforms' comprehensive feature sets encompassing stimulus presentation, AOI analysis, heatmap generation, and real-time biometric data export have made them the preferred procurement category for academic researchers, clinical trial operators, and automotive human factors laboratories that require validated, regulatory-aligned software solutions with established vendor support ecosystems.

SDKs & integration tools segment is estimated to register the highest CAGR of 27.91% during the forecast period of 2026–2035 owing to the explosive growth of the eye tracking developer community across consumer electronics, automotive software engineering, healthcare application development, and extended reality content creation. The proliferation of eye tracking-enabled hardware platforms including XR headsets, automotive cabin sensing modules, and consumer laptops with integrated cameras is generating structurally growing demand for SDKs that enable software developers to embed gaze functionality into custom applications without procuring full enterprise platform licenses, substantially expanding the total addressable developer market for 3D eye tracking software.

By Deployment Mode, cloud-based deployment dominates the 3D eye tracking software market, while cloud-based is also the fastest-growing segment.

Cloud-based segment dominated the market with the largest revenue share of about 58.09% in 2025 attributed to the significant operational and financial advantages it delivers relative to on-premise alternatives, including elastic scalability for large-scale research panel data processing, elimination of on-site server infrastructure capital expenditures, and the ability to support geographically distributed research teams accessing shared gaze datasets through centralized cloud analytics dashboards. The segment's dominance is further reinforced by the migration of enterprise research operations toward SaaS-based software procurement models that align software expenditure with usage-based subscription pricing rather than perpetual licensing capital commitments.

Cloud-based deployment is simultaneously the fastest-growing segment, projected to maintain the highest CAGR of 27.22% during 2026–2035, driven by the growing volume of remote and hybrid research study designs that require cloud-native data collection infrastructure, the expansion of real-time collaborative analytics capabilities enabled by cloud processing, and the increasing availability of edge-to-cloud gaze data pipelines that reconcile the low-latency requirements of interactive eye tracking applications with the analytical scale advantages of cloud computing architectures.

By Tracking Type, remote eye tracking dominates the 3D eye tracking software market, while wearable eye tracking is the fastest-growing segment.

Remote eye tracking segment emerged as the market leader with a dominant share of around 34.06% in 2025 owing to its widespread adoption across consumer research, usability testing, and clinical assessment applications where non-invasive, camera-based gaze measurement without head-mounted hardware is operationally preferred. The segment benefits from the progressive improvement in webcam-grade remote tracking accuracy enabled by deep learning-based gaze estimation models that have substantially narrowed the performance gap between remote and contact-based tracking modalities, enabling large-scale online research panel deployments at per-participant costs that support commercial viability for corporate marketing research applications.

Wearable eye tracking segment is anticipated to record the fastest CAGR of 27.37% throughout the forecast period of 2026–2035 driven by the rapid consumer adoption of extended reality headsets incorporating integrated eye tracking hardware, the growing military and aerospace investment in helmet-mounted gaze tracking for pilot and combat systems operator monitoring, and the rising clinical deployment of wearable gaze sensors for real-world neurological assessment outside controlled laboratory environments. The convergence of miniaturized eye tracking sensors with spatial computing platforms is creating a fundamentally new product category with a substantially larger addressable market than traditional laboratory-grade wearable eye trackers.

By Application, healthcare & medical research dominates the 3D eye tracking software market, while gaming & entertainment is the fastest-growing segment.

Healthcare & medical research segment dominated the 3D eye tracking software market with the highest revenue share of about 28.15% in 2025 owing to the clinical and scientific community's long-established adoption of precision gaze analysis for neurological disorder assessment, surgical training simulation, pharmaceutical attention research, and visual rehabilitation therapy. The segment's sustained leadership reflects the high average contract values associated with clinical-grade eye tracking software deployments, the institutional procurement stability provided by hospital and university research center buyers, and the growing evidence base linking 3D gaze biomarkers to early detection of conditions including Alzheimer's disease, autism spectrum disorder, multiple sclerosis, and concussion, which is driving expanded clinical trial investment in gaze-based diagnostic tools.

Gaming & entertainment segment is projected to witness the fastest CAGR of 28.35% during the forecast period of 2026–2035 due to the mass-market proliferation of eye tracking-enabled gaming peripherals and extended reality headsets, the integration of foveated rendering technology dependent on real-time gaze tracking to optimize GPU rendering performance, and the growing adoption of gaze-contingent gameplay mechanics by AAA game studios seeking to differentiate premium titles through novel interaction modalities. The segment's exceptional growth trajectory is further amplified by the consumer metaverse platform development programs of major technology companies that are embedding eye tracking as a foundational interaction primitive across their spatial computing ecosystems.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.90% |

|

Europe |

Germany |

29.50% |

|

Asia Pacific |

China |

38.80% |

|

Middle East & Africa |

UAE |

29.40% |

|

Latin America |

Brazil |

42.20% |

North America 3D Eye Tracking Software Market Insights

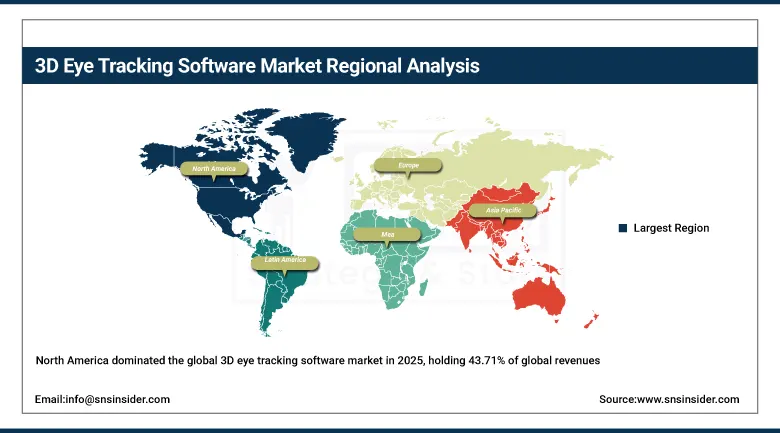

North America dominated the global 3D eye tracking software market in 2025, holding 43.71% of global revenues, with the United States accounting for 83.90% of regional revenue. The region's market leadership reflects the unparalleled concentration of technology innovation investment, the world's largest defense and aerospace research and development budgets that include significant eye tracking software procurement for pilot and operator monitoring applications, and the most advanced XR developer ecosystem globally where gaze-contingent software capabilities are an increasingly standard feature requirement across consumer and enterprise headset platforms. The U.S. regulatory environment, particularly NHTSA's advancing driver monitoring system standards and FDA guidance on digital health technologies, is creating compliance-driven software procurement demand that strengthens the region's structural growth foundation.

Over 200 universities and research hospitals across North America utilize eye-tracking software for neuroscience, cognitive science, and behavioural research. The region accounts for over 40 active automotive driver monitoring (DMS) development programs, supporting demand for gaze analytics platforms. More than 75% of premium VR/XR headset developers maintain R&D operations in North America, driving software integration opportunities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe 3D Eye Tracking Software Market Insights

In 2025, Europe is the second largest regional market with a revenue share of 23.41%, with Germany accounting higher in regional revenue. The continent's significant global automotive industry, where German, Swedish and French OEMs are integrating driver monitoring systems across their production vehicle platforms in line with the European Union General Safety Regulation that mandated driver drowsiness and attention warning systems across new vehicle categories from 2022, with advanced eye tracking-based DMS increasingly replacing camera-only alertness monitoring systems, supports Europe's market position. Europe has a long tradition of research and commercialisation in the field of gaze technology and remains a magnet for venture capital investment and enterprise software development talent.

Europe produces approximately 16 million passenger vehicles annually, making it a major market for eye-tracking-enabled driver monitoring software. The region hosts 100+ dedicated human-computer interaction and usability research laboratories utilizing gaze analytics tools.

Asia Pacific 3D Eye Tracking Software Market Insights

Asia Pacific is the fastest-growing regional 3D eye tracking software market at a CAGR of 27.72% through 2035. China accounts for 36.80% of Asia Pacific revenues, driven by the country's aggressive investment in artificial intelligence, smart mobility, and digital health sectors under national technology development programs that include eye tracking-enabled applications across autonomous vehicle human machine interface validation, neurological healthcare diagnostics, and educational technology. Japan represents a significant market through its automotive and industrial robotics sectors, where gaze tracking software supports advanced driver assistance system validation, human-robot collaboration safety certification, and industrial worker attention monitoring for manufacturing quality assurance.

China accounts for over 35% of global AR/VR hardware manufacturing capacity, creating a substantial ecosystem for eye-tracking software integration. Japan and South Korea together operate over 500 industrial robots per 10,000 manufacturing workers in leading facilities, supporting human-machine interface research.

MEA & Latin America 3D Eye Tracking Software Market Insights

Emerging market opportunities for the 3D eye tracking software industry include Middle East and Africa and Latin America. Both regions have early-stage adoption in healthcare technology, academic research infrastructure investment, and automotive sector modernisation programs. The UAE, contributing higher in MEA regional revenues, serves as the regional entry market for enterprise eye tracking software vendors, through its advanced healthcare technology procurement programs, smart city infrastructure initiatives, and the presence of internationally affiliated academic and research institutions that adopt globally standardised behavioural research software platforms.

Brazil’s higher ranking in regional revenues in Latin America is due to its more developed university research infrastructure, the presence of international automotive manufacturing facilities that purchase globally standardised driver monitoring software, and the increasing corporate investment in consumer behaviour and neuromarketing research applications by Brazil’s large fast-moving consumer goods and retail sector. Mexico represents the most dynamic growth opportunity in the region, with the automotive manufacturing sector becoming integrated into global OEM supply chains that are increasingly requiring compliance with DMS software across production facilities serving North-American and European vehicle platform programs.

More than 300 universities across Latin America participate in digital learning and behavioural research programs that increasingly utilize attention analytics tools. Internet penetration exceeds 75% in several major economies, supporting cloud-based eye-tracking software adoption.

Growth Drivers: Surging XR adoption and automotive DMS regulatory mandates

The dual structural catalysts of extended reality platform proliferation and automotive driver monitoring system regulatory mandates are driving simultaneous high-volume demand for 3D eye tracking software in two of the technology industry’s highest-growth sectors. Major technology platform operators investing tens of billions of dollars in spatial computing hardware and software ecosystems have propelled eye tracking from an optional research tool to a core interaction technology in the consumer XR headset market enabling foveated rendering, social presence through avatar eye animation, and gaze-based user interface navigation each requiring robust software platforms that accurately resolve three-dimensional gaze vectors in real time across diverse user populations.

Restraints: Privacy regulations and data sensitivity concerns

The 3D eye tracking software market is experiencing significant headwinds from the growing worldwide regulatory environment related to biometric data privacy, which treats gaze data as a sensitive personal data with heightened restrictions on consent, storage, and processing under the European Union General Data Protection Regulation, the California Consumer Privacy Act, and an increasing number of national biometric data protection laws that impose material compliance costs and operational constraints on enterprise eye tracking software deployments. Gaze data is inherently sensitive and has the potential to reveal medical conditions, cognitive states, emotional responses, and unconscious attentional biases.

Opportunities: Healthcare diagnostics expansion and edge AI deployment

A key commercial opportunity for 3D eye tracking software vendors arises from the clinical validation of eye tracking biomarkers as early diagnostic markers for neurological and psychiatric diseases such as Parkinson's disease, Alzheimer's disease, autism spectrum disorder, attention deficit hyperactivity disorder, and traumatic brain injury. This is driven by the massive size of global neurology diagnostics markets and the willingness of healthcare payers to fund technology adoption that demonstrably improves diagnostic efficiency and patient outcome trajectories.

The concurrent growth of edge artificial intelligence processing capabilities in embedded system-on-chip platforms allows for real-time 3D gaze computation without dependence on cloud connectivity, thus enabling new deployment scenarios in automotive, industrial and wearable applications where latency and data sovereignty requirements have previously precluded the use of eye tracking software.

Recent Developments

-

2026: iMotions A/S released iMotions 11, featuring enhanced cloud-based multi-modal biometric data synchronization, real-time 3D eye tracking integration with major remote webcam tracking providers, and expanded support for automated attention KPI reporting across consumer research panel deployments.

-

2026: Pupil Labs GmbH introduced Pupil Cloud 2.0, a cloud-native gaze analytics platform supporting wearable 3D eye tracking data from its Neon headset, featuring automated AOI mapping, scene understanding through computer vision, and enterprise-grade research collaboration workflows for clinical and field research deployments.

-

2025: Tobii AB launched its Tobii Eye Tracker 5X SDK for Windows and Linux platforms, enabling game developers and XR application creators to integrate high-precision 3D gaze tracking with sub-degree accuracy into consumer software titles using a unified cross-platform API.

-

2025: Smart Eye AB expanded its automotive driver monitoring software portfolio with a new AI-powered interior sensing platform integrating 3D gaze tracking, head pose estimation, and occupant classification for NCAP five-star safety compliance across multiple global automotive OEM programs

3D Eye Tracking Software Market Key Players

-

Tobii AB

-

Smart Eye AB

-

EyeTech Digital Systems Inc.

-

Seeing Machines Limited

-

SR Research Ltd.

-

Gazepoint Research Inc.

-

iMotions A/S

-

Lumen Research Ltd.

-

RealEye sp. z o.o.

-

EyeSee NV

-

Bitbrain Technologies S.L.

-

Mirametrix Inc.

-

Eyeware Tech SA

-

Pupil Labs GmbH

-

Sticky by Tobii AB

-

Noldus Information Technology BV

-

Ergoneers GmbH

-

SensoMotoric Instruments (SMI)

-

LC Technologies Inc.

-

Interactive Minds Dresden GmbH (IMD)

3D Eye Tracking Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.40 Billion |

| Market Size by 2035 | USD 4.22 Billion |

| CAGR | CAGR of 26.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Eye Tracking Software Platforms, Analytics & Visualization Software, SDKs & Integration Tools, Support & Professional Services) • By Deployment Mode (Cloud-Based, On-Premise) • By Tracking Type (Remote Eye Tracking, Screen-Based Eye Tracking, Mobile Eye Tracking, Wearable Eye Tracking) • By Application (Healthcare & Medical Research, Consumer Behavior & Marketing Research, Automotive & Transportation, Gaming & Entertainment, Education & Training, Aerospace & Defense) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tobii AB, Smart Eye AB, EyeTech Digital Systems Inc., Seeing Machines Limited, SR Research Ltd., Gazepoint Research Inc., iMotions A/S, Lumen Research Ltd., RealEye sp. z o.o., EyeSee NV, Bitbrain Technologies S.L., Mirametrix Inc., Eyeware Tech SA, Pupil Labs GmbH, Sticky by Tobii AB, Noldus Information Technology BV, Ergoneers GmbH, SensoMotoric Instruments (SMI), LC Technologies Inc., Interactive Minds Dresden GmbH (IMD) |

Frequently Asked Questions

The 3D eye tracking software market was valued at USD 0.40 Billion in 2025.

The primary growth drivers include increasing integration of eye tracking in XR devices and automotive driver monitoring systems, alongside rising clinical adoption for neurological diagnostics.

Wearable Eye Tracking is the fastest-growing tracking type in the 3D Eye Tracking Software Market, with a CAGR of 27.37% from 2026 to 2035.

North America dominated the 3D Eye Tracking Software Market in 2025, holding 43.71% of global revenues, with the United States accounting for 83.90% of North American revenues.

Get in Touch