Specialty Insurance Market Report Scope & Overview:

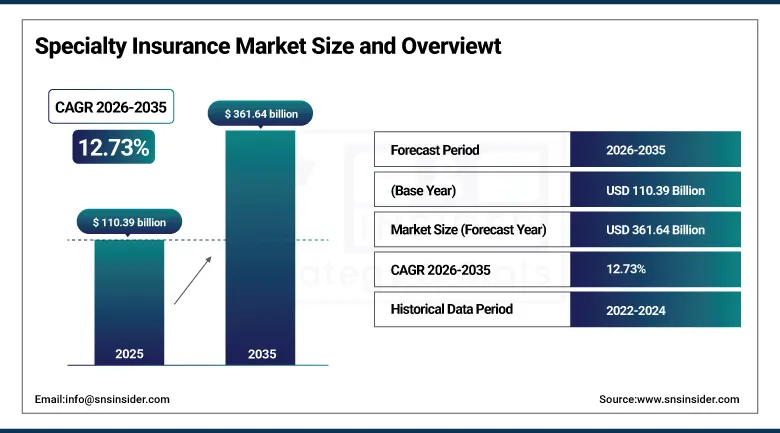

The Specialty Insurance Market was valued at USD 110.39 Billion in 2025 and is expected to reach USD 361.64 Billion by 2035, growing at a CAGR of 12.73% from 2026 to 2035.

The specialty insurance market occupies a strategically critical position within the broader global insurance and financial risk management industry, providing bespoke, non-standard coverage solutions for complex, high-value, or emerging risk categories that conventional insurance products cannot adequately address. These include cyber liability, energy sector exposures, marine and aviation perils, parametric weather risks, professional indemnity, entertainment and sports-related contingencies, and unique financial lines. As businesses across industries face increasingly intricate operational, regulatory, and technological risk environments, the structural demand for tailored specialty insurance programs delivered through sophisticated underwriting platforms, broker networks, and InsurTech-enabled channels continues to expand significantly.

In 2025, sustained global digitalization, accelerating climate-related risk exposure, and expanding regulatory frameworks across financial services, healthcare, and technology sectors collectively sustained strong structural demand for specialty insurance coverage solutions. During this period, several leading insurance carriers and InsurTech platforms introduced new specialty risk products through collaborative development programs. Lloyd's of London, in partnership with Munich Re, launched an expanded parametric cyber risk insurance program designed for mid-market enterprises across North America and Europe. Additionally, AXA XL and IBM jointly developed an AI-powered underwriting platform for specialty liability coverage, enabling more precise risk stratification and faster policy issuance.

Market Size and Forecast

-

Market Size in 2026E: USD 122.99 Billion

-

Market Size by 2035: USD 361.64 Billion

-

CAGR: 12.73% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Specialty Insurance Market - Request Free Sample Report

Specialty Insurance Market Trends

-

Rising frequency of cyberattacks, ransomware incidents, and data breaches is driving strong demand for cyber specialty insurance coverage across enterprises of all sizes.

-

Increasing exposure to climate-related catastrophes such as floods, hurricanes, and wildfires is accelerating adoption of parametric and catastrophe insurance solutions.

-

Growing complexity of global supply chains and cross-border trade is boosting demand for marine, aviation, and trade credit specialty insurance products.

-

Expanding offshore energy,renewable energy, and infrastructure investments is increasing uptake of energy specialty insurance for high-risk operational environments.

-

Rapid digital transformation and cloud adoption are leading to higher demand for professional liability, E&O, and D&O insurance coverage across technology-driven businesses.

-

Rising integration of AI, IoT, and data analytics in underwriting is improving risk assessment accuracy and enabling more dynamic, usage-based insurance models.

U.S. Specialty Insurance Market Outlook

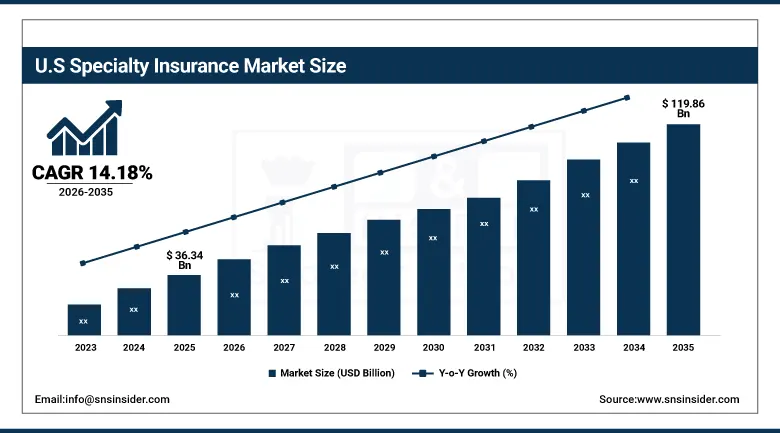

The U.S. specialty insurance market was valued at approximately USD 36.34 Billion in 2025 and is expected to reach approximately USD 119.86 Billion by 2035, growing at a CAGR of approximately 14.18%.

The United States commands the largest individual national share of the global specialty insurance market, driven by the unparalleled scale and complexity of its corporate, financial, healthcare, energy, and technology sector risk ecosystems, all of which generate structural demand for non-standard insurance solutions that address exposures beyond the coverage parameters of conventional commercial property and casualty programs. The U.S. specialty insurance market is underpinned by the Lloyd's of London U.S. platform, Bermuda and London market capacity, and a deep domestic surplus lines insurance infrastructure, collectively providing underwriting capacity for the most complex and high-value risk categories including directors and officers liability, environmental impairment liability, cybercrime, aviation hull.

The U.S. Department of the Treasury's Federal Insurance Office (FIO), under its National Insurance Development Framework 2025, co-sponsored a joint risk assessment initiative with Zurich North America and Marsh McLennan to develop a standardized enterprise cyber risk quantification methodology for critical infrastructure operators across the energy, utilities, and financial services sectors. The program, deployed across 47 qualifying U.S. critical infrastructure entities in 2025, demonstrated a 28% improvement in cyber risk quantification accuracy, a 19% reduction in specialty cyber coverage procurement lead time, and aggregate risk transfer optimization savings of approximately USD 240,000 per entity annually, directly supporting the administration's national cyber resilience and insurance market development objectives.

Specialty Insurance Market Segment Analysis

-

By Type, the property specialty insurance segment dominated the specialty insurance market with 30.74% share in 2025, while the cyber specialty insurance segment is the fastest growing type with the highest CAGR of 14.82% from 2026 to 2035.

-

By Coverage Area, the energy & offshore insurance segment dominated the specialty insurance market with 28.64% share in 2025, while the parametric insurance segment is the fastest growing material type with the highest CAGR of 14.26% from 2026 to 2035.

-

By End User, the large enterprises segment dominated the specialty insurance market with 40.55% share in 2025, while the SMEs segment is the fastest growing application with the highest CAGR of 14.04% from 2026 to 2035.

-

By Distribution Channel, the insurance brokers segment dominated the specialty insurance market with 58.61% share in 2025, while the digital/insurtech Platforms s segment is the fastest growing end user category with the highest CAGR of 14.52% from 2026 to 2035.

By Type, property specialty insurance dominates, cyber specialty insurance Grows Fastest

Property specialty insurance accounted for 30.74% of specialty insurance market revenue in 2025, reflecting its foundational role as the largest and most established product line within the global specialty insurance ecosystem. This segment covers non-standard, high-value, or uniquely exposed physical assets that cannot be accommodated within conventional property insurance frameworks, including large industrial complexes, offshore platforms, landmark real estate, cultural heritage properties, and critical infrastructure assets whose replacement values, loss concentrations, and risk profiles require bespoke underwriting solutions from specialist carriers. The segment's dominance is reinforced by continued demand from energy, mining, utilities, and manufacturing sectors, all of which require high-limit, manuscript-form property coverage programs.

Cyber specialty insurance is the fastest-growing segment in the specialty insurance market, driven by rapid global digitalization and rising enterprise exposure to cyber risks across industries. Increasing reliance on cloud infrastructure, AI systems, and connected digital ecosystems has expanded vulnerability to data breaches, ransomware, and operational disruptions. Regulatory frameworks such as the U.S. NIST Cybersecurity Framework 2.0, EU NIS2 Directive, and UK National Cyber Strategy are transforming cyber insurance from optional protection into a compliance-driven requirement. In 2025, innovation accelerated as Beazley and Microsoft launched an integrated cyber resilience and insurance solution combining real-time monitoring with automated coverage triggers.

By Coverage Area, energy & offshore insurance dominates, parametric insurance grows fastest

Energy and offshore insurance accounted for 28.64% of specialty insurance coverage revenue in 2025, supported by the scale and complexity of global oil, gas, and emerging offshore renewable energy infrastructure. Demand is driven by upstream and downstream hydrocarbon operations, LNG terminals, petrochemical assets, and expanding offshore wind projects requiring high-limit, technically advanced risk coverage. Policies typically address physical damage, business interruption, pollution liability, and control of well exposures. Growth is further reinforced by NOC-led developments in the Middle East, deepwater exploration in Brazil and West Africa, and rising offshore wind and subsea infrastructure investments across Europe and Asia Pacific.

Parametric insurance is the fastest-growing coverage area in the specialty insurance market due to its ability to address risks that are difficult to model and settle under traditional indemnity-based structures. Unlike conventional policies, parametric products trigger predefined payouts based on measurable events such as wind speed, rainfall levels, or seismic activity, enabling faster claims settlement and reduced administrative complexity. This structure minimizes disputes, basis risk uncertainty, and underwriting delays. In 2025, the World Bank’s Global Shield initiative, backed by G7 nations and supported by insurers such as Swiss Re, Allianz, and AXA, expanded sovereign parametric coverage to 58 climate-vulnerable countries, strengthening global climate resilience.

By End User, large enterprises dominate, SMEs grow fastest

Large enterprises accounted for 40.55% of specialty insurance market revenue in 2025, reflecting the dominance of complex, high-value risk portfolios managed by multinational corporations across energy, financial services, manufacturing, aviation, and technology sectors. These organizations maintain structured risk management frameworks that identify and transfer diverse exposures, including operational liability, directors and officers liability, cyber risk, and global asset protection needs. Demand is driven by board-level governance standards, investor requirements, and regulatory compliance obligations that mandate comprehensive insurance coverage. Large enterprise programs generate substantial premium volumes, often ranging from multi-million-dollar placements to large-scale global risk transfer arrangements across interconnected business operations.

SMEs represent the fastest-growing end-user segment in the specialty insurance market, driven by expanding access to coverage through digital distribution platforms, broker-led packaged solutions, and government-backed risk mitigation programs across North America, Europe, and Asia Pacific. Growth is fueled by rising exposure of small and mid-sized businesses to cyber threats, professional liability claims, supply chain disruptions, and regulatory compliance requirements, which were traditionally concentrated among large enterprises. In 2025, Lloyd’s of London and Salesforce launched an SME-focused specialty insurance marketplace integrating CRM-based risk profiling and automated coverage recommendations, enabling faster, simplified access to tailored cyber, liability, and business interruption insurance products globally.

By Distribution Channel, insurance brokers dominate, digital/insurtech Platforms grow fastest

Insurance brokers accounted for 58.61% of specialty insurance distribution channel revenue in 2025, underscoring their central role in structuring and placing complex risk programs across global insurance markets. Specialty brokers such as Marsh McLennan, Aon, Willis Towers Watson, and Gallagher act as key intermediaries between corporate clients and capacity providers across Lloyd’s, London, Bermuda, and global surplus lines markets. Their dominance is driven by expertise in risk engineering, program design, claims advocacy, and multi-line policy structuring. Brokers are especially critical for large enterprises requiring tailored, multi-carrier placements, manuscript policy development, and coordinated international insurance solutions across diverse and highly technical risk categories.

Digital and InsurTech platforms represent the fastest-growing distribution channel in the specialty insurance market, driven by rapid digitalization of insurance infrastructure, data-driven underwriting models, and rising demand for seamless, API-enabled procurement experiences. These platforms are transforming how specialty risks are assessed, priced, and bound in real time, particularly for SME-focused cyber and professional liability coverage. In 2025, Coverwallet (backed by Aon) and Guidewire introduced AI-integrated underwriting systems enabling instant risk evaluation and policy issuance, reducing processing time from days to hours. Regulatory support from initiatives such as the UK FCA Digital Sandbox and Singapore MAS FinTech framework is further accelerating innovation and adoption globally.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.41% |

|

Europe |

Germany |

34.16% |

|

Asia Pacific |

China |

37.75% |

|

Middle East & Africa |

UAE |

19.68% |

|

Latin America |

Brazil |

25.61% |

North North America Specialty Insurance Market Insights

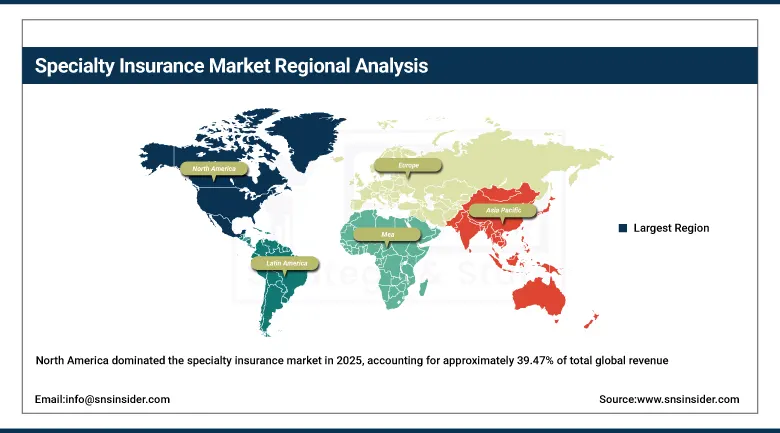

North America dominated the specialty insurance market in 2025, accounting for approximately 39.47% of total global revenue. This leadership is supported by a highly mature insurance ecosystem, advanced underwriting capabilities, and strong concentration of large enterprises across energy, aviation, construction, marine, and cybersecurity sectors. The United States acts as the primary growth engine due to stringent regulatory frameworks, sophisticated risk management practices, and extensive demand for customized coverage solutions addressing complex operational exposures. Rising cyber incidents, increasing climate-related losses, and accelerated digital transformation are further driving demand across property, liability, and parametric insurance lines. The region is also strengthened by leading global insurers, robust reinsurance capacity, and rapid adoption of AI-driven analytics and InsurTech platforms, enhancing pricing accuracy, claims efficiency, and overall market competitiveness.

In 2025, the U.S. Cybersecurity and Infrastructure Security Agency (CISA), in collaboration with AIG and Resilience Insurance, launched the Critical Infrastructure Cyber Risk Transfer Framework, a structured specialty cyber insurance product designed specifically for operators of critical national infrastructure across energy, water, and transportation sectors. Deployed across 62 qualifying infrastructure entities, the program achieved a 33% improvement in cyber risk coverage adequacy, a 21% reduction in average claims resolution time through integrated incident response coordination protocols, and demonstrated aggregate risk transfer efficiency improvements equivalent to USD 310,000 per entity annually, directly advancing national critical infrastructure cyber resilience objectives.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Specialty Insurance Market Insights

Europe accounted for approximately 26.47% of global specialty insurance revenue in 2025. The region is supported by a mature and highly sophisticated insurance ecosystem anchored by Lloyd’s of London and the broader London market, alongside strong domestic underwriting hubs in Germany, France, Switzerland, and Scandinavia. Regulatory frameworks such as the EU NIS2 Directive, Solvency II capital requirements, EU Taxonomy for Sustainable Finance, and environmental liability laws are driving mandatory and compliance-linked specialty insurance adoption across industries. Growth is further supported by the rapid expansion of offshore wind energy projects across the North Sea, Baltic Sea, and Irish Sea, generating rising demand for marine, engineering, and renewable energy insurance solutions across Europe’s evolving risk landscape.

The European Commission's Digital Finance Strategy, which committed EUR 500 Billion toward digital infrastructure and cybersecurity resilience through 2030, directly catalyzed a joint product development initiative between Allianz Global Corporate & Specialty and SAP in 2025, resulting in the launch of an ERP-integrated cyber specialty insurance solution that combines real-time digital risk monitoring with automated coverage limit adjustments for enterprise technology sector clients across Germany, France, and the Netherlands. Field deployment across 38 European enterprise clients demonstrated a 26% improvement in cyber risk detection speed and a 19% reduction in specialty cyber premium expenditure through dynamic risk-based pricing adjustments enabled by continuous platform-level threat monitoring.

Asia Pacific Specialty Insurance Market Insights

Asia Pacific is the emerged as fastest growing regional market, accounting for 13.94% CAGR expanding at a steady growth rate through 2035. China represents 37.75% of regional demand, driven by large-scale onshore and offshore drilling programs led by CNPC, CNOOC, and Sinopec across the Tarim, Ordos, and Sichuan basins, as well as the South China Sea. These extensive well construction activities make China the largest drilling market in the region. Additional demand comes from Southeast Asia, Australia, and South Korea through active offshore and onshore operations. Growing geothermal development in Indonesia, the Philippines, and New Zealand further supports demand for high-temperature stabilizer systems.

China Banking and Insurance Regulatory Commission (CBIRC), under the 14th Five-Year Financial Services Development Plan, co-sponsored a joint specialty insurance product development program with Swiss Re and China Re in 2025 to engineer parametric catastrophe insurance solutions for Chinese SMEs exposed to typhoon, flood, and earthquake perils. Deployed across pilot programs in Guangdong, Zhejiang, and Sichuan provinces, the parametric program achieved 100% claims settlement within 72 hours of trigger events, covering 14,200 SME policyholders and demonstrating a 41% improvement in post-disaster business recovery speed compared with traditional indemnity program benchmarks, establishing a scalable model for government-backed parametric specialty insurance across high-growth Asian markets.

Middle East & Africa and Latin America Specialty Insurance Market Insights

Middle East & Africa and Latin America represent among the most dynamic growth regions in the Specialty Insurance market, driven by expanding national oil company capital expenditure, renewed offshore development programs, and sustained onshore exploration drilling activity. These regions are experiencing above-average growth compared to more mature markets due to large-scale upstream investment cycles and increasing deployment of complex directional and deepwater drilling technologies. In Latin America, Brazil accounts for approximately 25.61% of regional revenue, supported by Petrobras’s extensive pre-salt deepwater drilling operations in the Santos and Campos basins. These ultra-deepwater wells, characterized by high pressure and complex wellbore geometries, generate strong demand for advanced, high-performance stabilizer systems.

The UAE specialty insurance market is evolving rapidly under the UAE Net Zero 2050 Strategy and the Abu Dhabi Global Market (ADGM) Insurance Regulatory Framework 2025, which are strengthening the region’s position in renewable energy risk coverage. In 2025, the UAE Insurance Authority supported a joint initiative between AXA Gulf and Masdar to develop specialty insurance solutions for offshore wind, solar, and green hydrogen infrastructure across the GCC. The program covered 22 renewable energy projects with a combined insured value of USD 8.4 billion, improving placement efficiency by 29%. This reflects the growing capability of GCC markets to support large-scale clean energy investments and complex specialty insurance requirements.

Growth Drivers: Expanding global cyber risk exposure and government-mandated specialty coverage frameworks are generating sustained structural demand

The accelerating global digitalization of commercial operations and rising cyber threat activity are key structural drivers of the specialty insurance market. Increasing enterprise exposure to ransomware, data breaches, business interruption, and technology errors and omissions liability is expanding across all industries. This growth is fueled by rising cloud adoption, supply chain digitalization, IoT expansion, and the use of generative AI, which introduces new liability risks beyond traditional commercial coverage. Regulatory frameworks such as the U.S. SEC cyber disclosure rules, the EU NIS2 Directive, and the UK Cyber Security and Resilience Bill are transforming cyber insurance into a governance-mandated requirement, driving compulsory adoption among enterprises, financial institutions, and critical infrastructure operators globally.

The U.S. Small Business Administration (SBA), in partnership with Chubb and Travelers, launched the National SME Specialty Risk Protection Initiative in 2025, providing co-subsidized cyber liability and professional indemnity specialty insurance access to over 125,000 qualifying small businesses across manufacturing, healthcare, and professional services sectors. Program deployment demonstrated a 37% increase in SME specialty coverage uptake, a 24% reduction in average specialty insurance procurement costs through SBA-negotiated group capacity arrangements, and aggregate risk transfer adequacy improvements valued at USD 1.8 Billion in enhanced SME coverage across participating businesses, directly supporting national economic resilience and small business sector stability objectives.

Restraints: Capacity constraints in peak-zone catastrophe and cyber accumulation risk segments and complex regulatory harmonization challenges create underwriting and market development friction

The specialty insurance market faces significant structural challenges related to underwriting capacity concentration and accumulation risk management, particularly across cyber, property catastrophe, and liability segments. These risks arise when correlated events trigger simultaneous large-scale claims across multiple policyholders, creating systemic loss exposure for insurers. Cyber insurance is especially vulnerable to accumulation risk from cloud infrastructure outages, software supply chain failures, and coordinated state-sponsored cyberattacks that can impact thousands of insured entities at once. As a result, major carriers are increasingly tightening underwriting standards, reducing sub-limits, and expanding exclusions. This has contributed to coverage gaps and affordability pressures, particularly for mid-market enterprises requiring comprehensive cyber risk protection.

Opportunities: Climate risk monetization through parametric insurance innovation and AI-powered underwriting platform development represent transformative market expansion frontiers

The accelerating global recognition of climate risk as a systemic financial threat is creating significant growth opportunities for specialty insurers developing parametric, index-based, and structured risk transfer solutions. These products address protection gaps left by traditional indemnity insurance across climate-vulnerable regions, agricultural systems, sovereign risk pools, and infrastructure-intensive industries. Parametric insurance enables rapid, pre-agreed payouts based on measurable triggers, supporting faster post-disaster recovery and liquidity access. At the same time, the integration of machine learning, satellite imagery, IoT sensors, and alternative data is enhancing underwriting precision. This is expanding insurability into historically underserved segments such as agriculture, supply chain disruption, and emerging climate-related and technology risks.

Brazil's Conselho Nacional de Seguros Privados (CNSP), under the government's National Agricultural Insurance Expansion Program jointly developed with Swiss Re and Bradesco Seguros in 2025, deployed a large-scale parametric crop insurance platform covering 68,000 smallholder agricultural producers across Mato Grosso, Paraná, and Rio Grande do Sul states. The program delivered 100% parametric claims automation triggered by satellite-monitored drought and excess rainfall indices, achieving a 47% reduction in claims processing time, a 31% improvement in post-drought agricultural recovery funding speed, and an aggregate crop insurance penetration increase of 23% across participating rural communities, establishing a replicable model for government-sponsored parametric specialty insurance expansion across Latin American agricultural risk markets.

Recent Developments:

-

2026: Lloyd's of London, in collaboration with Google Cloud, launched an AI-native specialty insurance underwriting platform enabling real-time risk assessment and automated policy structuring for cyber liability and E&O coverage, reducing placement time by 64% and expanding digital access for mid-market buyers across North America and Europe.

-

2026: AXA XL expanded its specialty insurance suite with nature-based risk and biodiversity liability products aligned with EU CSRD and TNFD frameworks, addressing emerging corporate exposure from mandatory natural capital disclosure and environmental reporting requirements.

-

2025: Zurich Insurance Group and Microsoft introduced an integrated enterprise risk intelligence platform combining Azure-based continuous monitoring with automated specialty coverage adjustments for cyber, professional liability, and technology risks in real time.

-

2025: Swiss Re and IFC launched a blended finance parametric insurance facility providing USD 3.2 Billion coverage across 31 climate-vulnerable nations, combining private reinsurance capacity with IFC-backed first-loss protection for sovereign risk transfer.

Specialty Insurance Market Key Players:

-

Allianz Global Corporate & Specialty (AGCS)

-

AIG (American International Group)

-

AXA XL

-

Lloyd's of London

-

Zurich Insurance Group

-

Munich Re

-

Swiss Re

-

Berkshire Hathaway Specialty Insurance

-

Tokio Marine HCC

-

Markel Corporation

-

W.R. Berkley Corporation

-

Aspen Insurance Holdings

-

Everest Re Group

-

Beazley plc

-

Hiscox Ltd.

-

Arch Capital Group Ltd.

-

RenaissanceRe Holdings Ltd.

-

Axis Capital Holdings Limited

Specialty Insurance Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 110.39 Billion |

| Market Size by 2035 | USD 361.64 Billion |

| CAGR | CAGR of 12.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Property Specialty Insurance, Liability Specialty Insurance, Financial Lines Insurance, Marine, Aviation & Transport Insurance, Cyber Specialty Insurance, Others), • By Coverage Area (Energy & Offshore Insurance, Aviation & Aerospace Insurance, Entertainment & Sports Insurance, Parametric Insurance, Professional Liability, Others), • By End User (Large Enterprises, SMEs, Financial Institutions, Energy & Utilities, Healthcare, Government & Public Sector, Others), • By Distribution Channel (Insurance Brokers, Direct Sales, Bancassurance, Digital/InsurTech Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Allianz Global Corporate & Specialty (AGCS), AIG (American International Group), AXA XL, Lloyd's of London, Chubb Limited, Zurich Insurance Group, Munich Re, Swiss Re, Berkshire Hathaway Specialty Insurance, Tokio Marine HCC, Markel Corporation, W.R. Berkley Corporation, Aspen Insurance Holdings, Everest Re Group, Beazley plc, Hiscox Ltd., Lancashire Holdings Limited, Arch Capital Group Ltd., RenaissanceRe Holdings Ltd., Axis Capital Holdings Limited. |

Frequently Asked Questions

The specialty insurance market is expected to grow at a CAGR of 12.73% from 2026 to 2035.

The specialty insurance market was valued at USD 110.39 Billion in 2025.

The primary growth factors include the rising complexity of global risks such as cyber threats, climate-related disasters, and supply chain disruptions, along with increasing demand for customized and non-standard risk coverage across industries.

The energy & offshore insurance segment dominated the specialty insurance market with 28.64% share in 2025.

North America dominated the specialty insurance market in 2025, holding approximately 39.47% of global revenues.

Get in Touch