Pitch Based Carbon Fiber Market Report Scope & Overview:

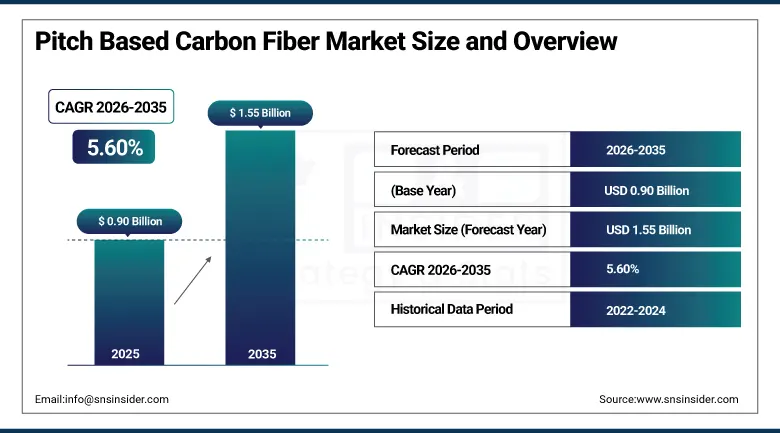

The Pitch Based Carbon Fiber Market was valued at approximately USD 0.90 billion in 2025 and is expected to reach around USD 1.55 billion by 2035, growing at a CAGR of 5.60% from 2026–2035.

The pitch based carbon fiber market is witnessing steady growth in the global market owing to increasing demand for high modulus carbon materials. Aerospace & defense applications are driving adoption across structural and thermal systems. Rising use in electronics and semiconductor thermal management is supporting expansion. Continuous fibers and ultra-high modulus grades are gaining strong traction in advanced engineering applications. Investments in lightweight materials and high-performance composites are accelerating market penetration. Growing industrial automation and energy-efficient material demand are further supporting market growth.

According to the U.S. Geological Survey Mineral Commodity 2025 and industry capacity disclosures compiled in official materials, pitch-based carbon fiber accounts for approximately 4–5% of total global carbon fiber production, while PAN-based fibers dominate at over 90%.

As per advanced materials production data, mesophase pitch fiber manufacturers in Japan and the United States collectively control more than 60% of high-modulus pitch fiber capacity in 2025. Additionally, China’s 14th Five-Year Plan for advanced materials reports expansion of new carbon fiber production lines adding over 4,000 metric tons of annual capacity between 2022 and 2025, reflecting measurable industrial scaling in strategic composites manufacturing.

Market Size and Forecast

-

Market Size 2026E: USD 0.95 billion

-

Market Size 2035: USD 1.55 billion

-

CAGR (2026 - 2035): 5.60%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Pitch Based Carbon Fiber Market - Request Free Sample Report

Pitch Based Carbon Fiber Market Trends

-

-

Rapid expansion of 5G networks and AI driven infrastructure is increasing demand for advanced thermal management materials globally across electronics industry

-

Growing deployment of high-performance computing systems is accelerating usage of pitch-based carbon fiber in semiconductor cooling applications worldwide

-

Increasing construction of hyperscale data centers is driving strong requirement for efficient heat dissipation solutions in electronic components and systems

-

Rising aerospace and defense modernization programs are boosting adoption of lightweight high strength carbon fiber materials for advanced structural applications

-

Strong shift toward fuel efficient aircraft and spacecraft design is increasing preference for pitch-based carbon fiber in critical components

-

Expanding use of advanced composites in industrial engineering is supporting demand for materials offering high stiffness thermal stability and durability

-

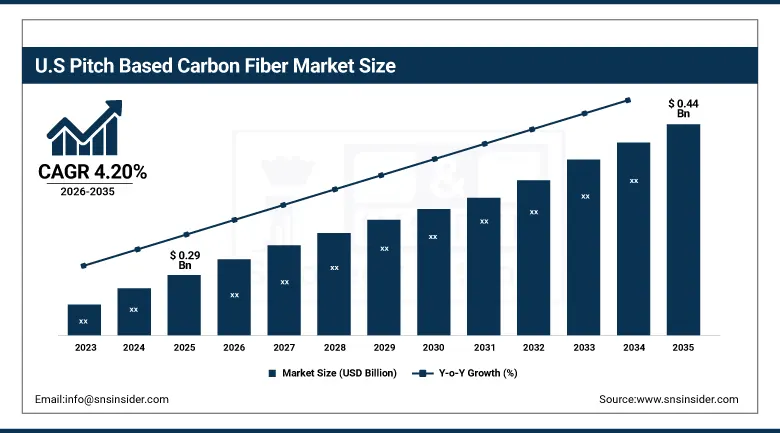

U.S. Pitch Based Carbon Fiber Market Size Outlook.

The U.S. Pitch Based Carbon Fiber Market was valued at approximately USD 0.29 billion in 2025 and is expected to reach around USD 0.44 billion by 2035, growing at a CAGR of 4.20% from 2026–2035.

The U.S. pitch based carbon fiber market is growing steadily owing to strong aerospace & defense demand. Advanced structural applications are driving adoption of high modulus carbon materials. Increasing use in thermal management systems and electronics is supporting market expansion. Continuous fibers are widely utilized in high-performance manufacturing sectors. Rising investments in lightweight composite technologies and defense modernization programs are strengthening demand. Growing focus on energy efficiency and advanced industrial materials is further accelerating the U.S. market growth.

According to the U.S. Department of Energy & Carbon Fiber Technology Facility and Oak Ridge National Laboratory materials scale-up programs, domestic pilot-scale production of advanced carbon fiber precursors, including pitch-based systems, has been demonstrated at controlled continuous processing rates up to 75 pounds per hour in 2025–2026 development facilities.

As per the U.S. Geological Survey Mineral Commodity Summaries 2025 framework, over 90 nonfuel mineral commodity datasets track the U.S. production and supply chain dependencies, while DOE-supported programs confirm increasing transition of pitch-based carbon fiber from laboratory validation to pilot-scale manufacturing for aerospace, defense, and energy applications in the United States.

Pitch Based Carbon Fiber Market Segment Analysis

-

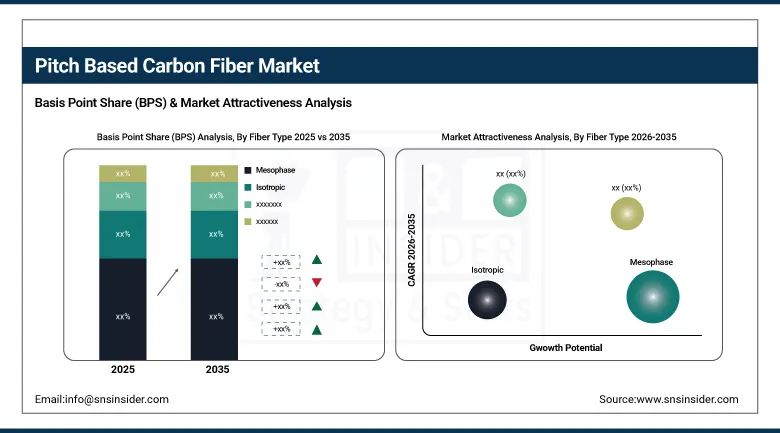

By Fiber Type, mesophase dominated the market with 54.20% share in 2025; while hybrid is the fastest growing segment with CAGR of 8.88% during 2026 to 2035.

-

By Performance Grade, intermediate modulus grade dominated the market with 42.80% share in 2025; while ultra-high modulus grade is the fastest growing segment with CAGR of 9.69% during 2026 to 2035.

-

By Form, continuous fibers dominated the market with 46.70% share in 2025; while prepreg materials are the fastest growing segment with CAGR of 10.79% during 2026 to 2035.

-

By End-Use Industry, aerospace & defense dominated the market with 38.90% share in 2025; while electronics & semiconductor are the fastest growing segment with CAGR of 10.56% during 2026 to 2035.

By Fiber Type, mesophase dominated the pitch based carbon fiber market, while hybrid is the fastest growing segment.

Mesophase segment was the leading segment with the dominated share in pitch based carbon fiber market revenues in 2025. The reason behind its dominance is attributed to its excellent molecular alignment and higher percentage of carbon atoms in it. Excellent thermal conductance, rigidity, and extremely high modulus characteristics make the segment more popular in aerospace, defense, and industrial applications. Higher adoption of lightweight materials with high strength attributes is another driving factor behind the success of Mesophase in market.

Hybrid segment would see the fastest CAGR during 2026–2035 owing to the ability of hybrid fibers to have the qualities of various fibers. Superiority over traditional fibers in terms of strength, versatility, and cost-efficiency makes it more suitable for different applications. Automotive, electronic, and energy applications would contribute to increasing demands for hybrid segments during the coming years. Growing interest in composite material technology and multifunctional performance of the material is fueling Hybrid segment growth.

By Performance Grade, intermediate modulus grade dominated the pitch based carbon fiber market, while ultra-high modulus grade is the fastest growing segment.

The Intermediate Modulus Grade segment held the leading position in the global market with dominated revenue share in 2025 owing to its optimum performance, low cost, and diverse applicability in aerospace, industrial, and automotive applications. It combines excellent mechanical strength with adequate flexibility, rendering it ideal for use in structural parts. Rising requirement for lightweight materials in commercial applications is further contributing to the rising adoption of this segment among the manufacturing industries across the world.

The Ultra-High Modulus Grade segment would witness the fastest CAGR during 2026-2035 owing to rising demand for aerospace applications, spacecrafts, and high-end electronic equipment. This grade is characterized by exceptional properties such as stiffness, high thermal conductivity, and dimensional stability. Increasing adoption in satellites, defense equipment, and thermal management applications is boosting its demand. The introduction of advanced composite materials and growing investments in engineering applications are fueling its growth significantly.

By Form, continuous fibers dominated the pitch based carbon fiber market, while prepreg materials is the fastest growing segment.

The Continuous Fibers Segment accounted for the dominated revenue share in the pitch based carbon fiber market in 2025. The major factor behind the dominance of this segment includes high usage in aerospace structural parts, high-performance industrial segments, etc. It provides superior mechanical strength, thermal stability, and consistency in its properties. It is used extensively in load-bearing systems. Well-established manufacturing procedures and high demand from military & defense applications, advanced engineering sector, etc. have been driving the dominance of the Continuous Fibers Segment in the market.

The Prepreg Materials Segment is projected to witness the fastest CAGR from 2026 to 2035 owing to the increasing demand for precise composite manufacturing applications. These materials provide better resin control, time-saving and high-quality results in manufacturing. The increased adoption in the aerospace industry, automotive, electronics, and others has been driving the growth of the segment. The increasing needs of lightweight materials and automation in composite material manufacturing will boost the demand for prepreg materials. High performance design requirements will further drive the growth of this segment in the market.

By End-Use Industry, aerospace & defense dominated the pitch based carbon fiber market, while electronics & semiconductor is the fastest growing segment.

Aerospace & Defense was the dominated market segment in terms of revenue share in 2025, owing to increasing demands for lightweight, high strength, and heat resistance materials in the manufacturing of aircraft parts and defense equipment. Pitch Based Carbon Fiber is used extensively in satellites, missiles, and other sophisticated equipment for the aerospace and defense industry. In addition, increasing modernization of defense systems and growth in aircraft production boost consistent use of pitch-based carbon fibers.

The Electronics & Semiconductors sector is projected to record the fastest CAGR during the forecast period owing to growing demand for heat-resistant and efficient materials for thermal management in electronic devices. Pitch Based Carbon Fibers are utilized in the manufacturing of heat sinks and semiconductors. Rising usage of miniaturized and powerful electronics is fueling innovations in materials. Further growth in 5G, Artificial Intelligence hardware, and data centers is boosting the demand for heat-resistant materials globally.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

85.50% |

|

Europe |

Germany |

28.40% |

|

Asia Pacific |

China |

18.60% |

|

Middle East & Africa |

UAE |

17.80% |

|

Latin America |

Brazil |

46.50% |

North America Pitch Based Carbon Fiber Market Insights.

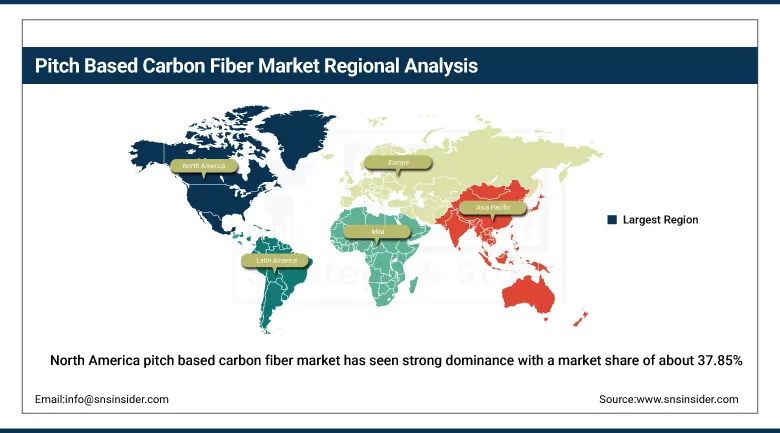

North America pitch based carbon fiber market has seen strong dominance with a market share of about 37.85% in 2025 due to advanced aerospace and defense manufacturing ecosystem. The region benefits from high demand for high modulus carbon materials used in satellites, aircraft structures, and defense components. Increasing adoption in thermal management and electronics applications is further supporting growth. Strong presence of leading composite manufacturers and continuous R&D investments are strengthening regional market leadership across advanced material technologies.

As per the U.S. Geological Survey Mineral Commodity Summaries 2025, the United States remains fully import-dependent for natural graphite feedstock used in high-performance carbon materials supply chains. Additionally, DOE industrial decarbonization initiatives report that over 60% of federally funded advanced materials projects target aerospace, defense, and energy applications where high-modulus pitch-based carbon fiber is prioritized.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Pitch Based Carbon Fiber Market Insights.

Europe pitch based carbon fiber market is characterized by steady growth in 2025 owing to strict environmental regulations and strong aerospace engineering base. Major contributing countries include Germany, France, United Kingdom, and Italy. Rising demand for lightweight and fuel-efficient aircraft is supporting adoption. Growth in renewable energy applications and industrial equipment is also contributing to market expansion. Increasing focus on sustainable advanced materials and high-performance composites is strengthening regional demand across Europe.

According to the European Commission and the European Environment Agency, Europe’s demand base for pitch-based carbon fiber is supported by aerospace, renewable energy, and electrification sectors. In 2025, the European Union maintained a legally binding target of at least 42.5% renewable energy share by 2030, while Eurostat reported that manufacturing accounted for approximately 15% of EU gross value added.

Asia Pacific Pitch Based Carbon Fiber Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the pitch based carbon fiber market during the forecast period with a market share of about 7.69% in 2025. Rapid industrialization and expansion of electronics and semiconductor manufacturing are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Growing automotive lightweighting and energy applications are further accelerating adoption. Rising investments in advanced manufacturing technologies and composites production are supporting regional growth momentum.

In accordance with the International Energy Agency and the Japanese Ministry of Economy, Trade and Industry, Asia-Pacific continues to be an important center of manufacture for innovative carbon materials thanks to its large presence of aircraft, electronic and energy manufacturing industry. In 2025, China was responsible for around 31% of the world’s manufacturing value-added, whereas Japan continued to have an advantage in producing high-performance carbon fiber technologies. Moreover, the IEA statistics revealed that in 2025 Asia-Pacific accounted for more than 60% of the world’s electric vehicle sales.

Middle East & Africa and Latin America Pitch Based Carbon Fiber Market Insights.

The Middle East & Africa along with Latin America are experiencing steady growth in the pitch based carbon fiber market due to expanding industrial infrastructure and increasing adoption of advanced materials. Key countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Rising investments in aerospace maintenance, energy systems, and industrial equipment are supporting demand. Growth in lightweight materials for construction and transportation applications is further contributing to regional market expansion.

As per the International Energy Agency indicators 2025 and World Bank infrastructure, demand drivers for pitch-based carbon fiber in the Middle East, Africa, and Latin America are becoming robust due to expansion in energy and industries. In 2025, 35% electricity generation is generated from renewable energy in Latin America, and Middle Eastern nations have aimed at utilizing more than 50% renewable energy by 2030 as a part of national strategy. In addition, World Bank figures reveal that more than 81% of urban population exists in Latin America and 44% in Sub-Saharan Africa.

Market Dynamics

Growth Drivers: Rising demand for high performance lightweight materials across aerospace defense and advanced engineering applications worldwide

High demands for high strength lightweight material are being witnessed throughout the world in aerospace and defense industries. Carbon fibers made from pitch exhibit excellent properties in terms of stiffness and thermal stability. Aircrafts, spacecrafts and defense systems need to have materials that help to lower their weight but without compromising on the quality of the materials. Rising concern for higher fuel efficiency and performance are contributing towards increased use.

According to the International Air Transport Association and the Stockholm International Peace Research Institute 2025, global air passenger traffic reached 103.9% of pre-pandemic levels in 2024, driving sustained aircraft production demand, while worldwide military expenditure increased by 9.4%, marking the tenth consecutive year of growth.

Restraints: Limited availability of raw pitch feedstock and supply chain constraints restricting production scalability and global expansion

Shortage in supply of superior quality pitch is an issue that greatly impacts capacity utilization and growth. The use of pitch from petroleum and coal makes the supply vulnerable. The processing of the pitch requires the adoption of technology to ensure the quality of output. Any disruption in the supply chain disrupts the production schedule and causes cost implications. There are limitations posed by geographic concentration of raw material suppliers.

Opportunities: Expansion of advanced electronics 5G infrastructure and AI driven data systems increasing demand for thermal management materials

The rapid growth of the 5G networks, artificial intelligence systems, and high-performance computing platforms is fueling the demand for such products. The pitch-based carbon fiber has an important role in thermal management for the next-generation electronics. The growing trend towards building more data centers along with innovations in semiconductors technology is helping in material usage. The increasing requirement for the efficient dissipation of heat in smaller electronic gadgets is providing huge growth opportunities.

As per the International Telecommunication Union Facts and Figures 2025 and International Energy Agency Electricity 2025, population coverage of 5G network globally will be more than 51% in 2025 and projected to go up to almost 80% by 2030, whereas the energy needs of data centers, artificial intelligence, and digitalization are forecasted to rise by more than two times and reach 945 TWh by 2030. These measurable trends will create a greater heat demand in electronic infrastructure, which will give rise to the greater requirement of heat conducting material like pitch-based carbon fiber.

Recent Developments

-

2026: Teijin Limited announced a new gas co-generation system projected to reduce annual CO₂ emissions by 200,000 tons.

-

2025: Toray Industries, Inc. showcased bio-circular and recycled carbon fiber technologies alongside next-generation composite solutions at JEC World 2025.

-

2025: Mitsubishi Chemical Group Corporation planned phased expansions both in Japan and the United States to increase high quality carbon fiber capacity by around twofold.

-

2024: SGL Carbon SE emphasized the improvements in efficiency and reorganization of industries using graphite and carbon fibers in Europe.

Pitch Based Carbon Fiber Market Key Players are:

-

Mitsubishi Chemical Group Corporation

-

Toray Industries, Inc.

-

Teijin Limited

-

SGL Carbon SE

-

Hexcel Corporation

-

Nippon Graphite Fiber Co., Ltd.

-

Kureha Corporation

-

Nippon Steel Chemical & Material Co., Ltd.

-

Osaka Gas Chemicals Co., Ltd.

-

Jilin Carbon Co., Ltd.

-

Fangda Carbon New Material Co., Ltd.

-

Resonac Holdings Corporation

-

UBE Corporation

-

OCI Company Ltd.

-

Tokai Carbon Co., Ltd.

-

HEG Limited

-

GrafTech International Ltd.

-

Syensqo SA/NV

-

Hyosung Advanced Materials Corporation

-

Zhongfu Shenying Carbon Fiber Co., Ltd.

Pitch Based Carbon Fiber Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.90 Billion |

| Market Size by 2035 | USD 1.55 Billion |

| CAGR | CAGR of 5.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fiber Type (Mesophase, Isotropic, Modified, Hybrid) • By Performance Grade (Low Modulus Grade, Intermediate Modulus Grade, High Modulus Grade, Ultra-High Modulus Grade) • By Form (Continuous Fibers, Short Fibers, Yarns, Fabrics, Prepreg Materials) • By End-Use Industry (Aerospace & Defense, Automotive, Energy & Power, Industrial Equipment, Electronics & Semiconductor, Sporting Goods, Construction) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Mitsubishi Chemical Group Corporation, Toray Industries, Inc., Teijin Limited, SGL Carbon SE, Hexcel Corporation, Nippon Graphite Fiber Co., Ltd., Kureha Corporation, Nippon Steel Chemical & Material Co., Ltd., Osaka Gas Chemicals Co., Ltd., Jilin Carbon Co., Ltd., Fangda Carbon New Material Co., Ltd., Resonac Holdings Corporation, UBE Corporation, OCI Company Ltd., Tokai Carbon Co., Ltd., HEG Limited, GrafTech International Ltd., Syensqo SA/NV, Hyosung Advanced Materials Corporation, Zhongfu Shenying Carbon Fiber Co., Ltd. |

Frequently Asked Questions

The pitch based carbon fiber market is expected to grow at a CAGR of 5.60% from 2026 to 2035.

The pitch based carbon fiber market was valued at approximately USD 0.90 billion in 2025.

Major growth factors include increasing aerospace & defense demand, rising electronics and semiconductor applications, growing investments in advanced composites, expansion of 5G and AI infrastructure, and increasing focus on energy-efficient high-performance engineering materials.

The Aerospace & Defense segment dominated in 2025 due to rising demand for lightweight, high-strength materials in aircraft, satellites, missiles, and defense systems.

North America dominated the pitch based carbon fiber market in 2025 due to strong aerospace manufacturing, high R&D investments, and advanced composite adoption.

Get in Touch