Platelet Aggregation Devices Market Report Scope & Overview:

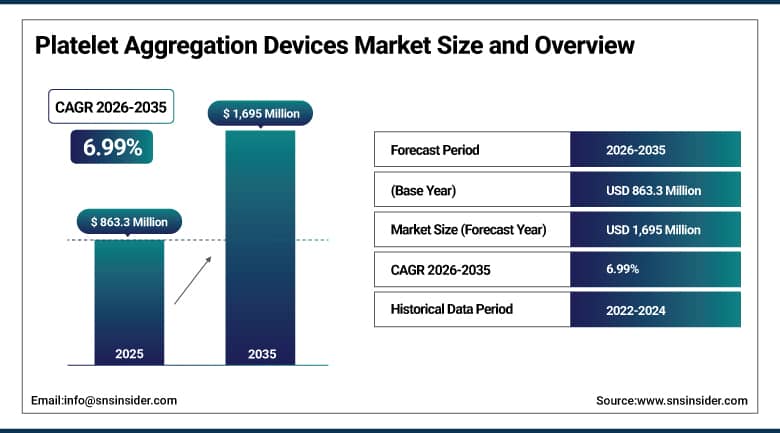

The Platelet Aggregation Devices Market size was USD 863.3 Million in 2025 and is expected to reach USD 1,695 Million by 2035, growing at a CAGR of 6.99% from 2026–2035.

Platelet Aggregation Devices Market is growing owing to an increased incidence of cardiovascular diseases, bleeding disorders, and thrombotic disorders, where there is a need for proper determination of platelet function. The increasing requirement for early diagnosis and detection along with the increasing use of platelet aggregation tests in hospitals, diagnostic centers, and research laboratories is propelling market growth. The developments in automation and high throughput analyzers are boosting testing accuracy and efficiency. Additionally, the increased funding in clinical research and pharmaceuticals and personalized medicine is boosting the requirement of platelet function analysis.

Supporting this trend, the World Health Organization reports that cardiovascular diseases are responsible for approximately 17.9 million deaths annually, accounting for around 32% of all global deaths. Furthermore, the International Society on Thrombosis and Haemostasis estimates that venous thromboembolism affects nearly 10 million people worldwide each year, reinforcing the growing need for advanced platelet function and coagulation testing solutions.

Platelet Aggregation Devices Market Size and Forecast:

-

Market Size in 2026E: USD 923.3 Million

-

Market Size by 2035: USD 1,695 Million

-

CAGR: 6.99% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Platelet Aggregation Devices Market - Request Free Sample Report

Platelet Aggregation Devices Market Trends:

-

Automated platelet function analyzers are replacing manual optical aggregometry in high-volume clinical laboratories.

-

Point-of-care platelet function testing is expanding beyond hospitals into diagnostic centers and specialty clinics.

-

Growing antiplatelet therapy monitoring demand, particularly for P2Y12 inhibitors, is reinforcing device adoption.

-

Miniaturized, portable platelet aggregation systems are broadening access to smaller and rural healthcare facilities.

-

Integration of platelet function testing data with electronic health records is improving clinical workflow efficiency.

U.S. Platelet Aggregation Devices Market Outlook:

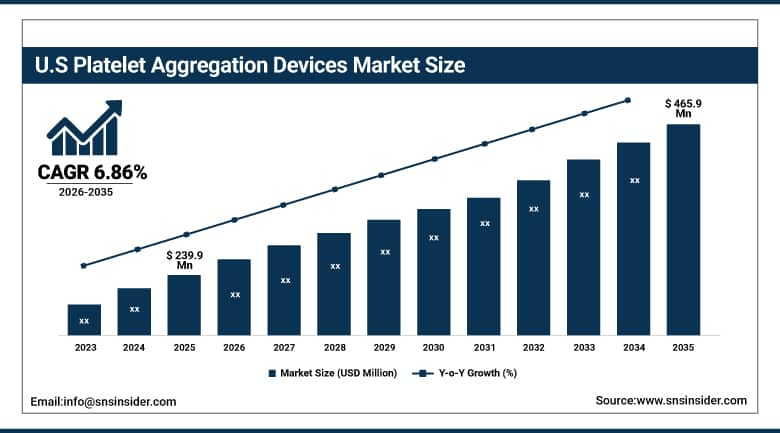

The U.S. Platelet Aggregation Devices Market was valued at approximately USD 239.9 Million in 2025. It is expected to reach approximately USD 465.9 Million by 2035, growing at a CAGR of approximately 6.86%.

The U.S. market is expanding owing to the higher incidence of cardiovascular diseases, bleeding problems, and increased surgical operations. Growing demand for better diagnostic products in the areas of hematology and thrombosis is also contributing to market growth. Advancements in technology in platelet function tests and adoption of automated analyzers are helping increase efficiency in diagnostics. Higher awareness regarding the coagulation problems and the requirement of an early diagnosis are also encouraging the adoption of platelet aggregation instruments in U.S. health care centers.

Additionally, favorable reimbursement policies and increasing awareness regarding early disease detection contribute to the widespread adoption of advanced platelet aggregation systems. Supporting this trend, the Centers for Disease Control and Prevention reports that heart disease remains the leading cause of death in the United States, accounting for approximately 702,000 deaths annually.

Platelet Aggregation Devices Market Segment Analysis:

-

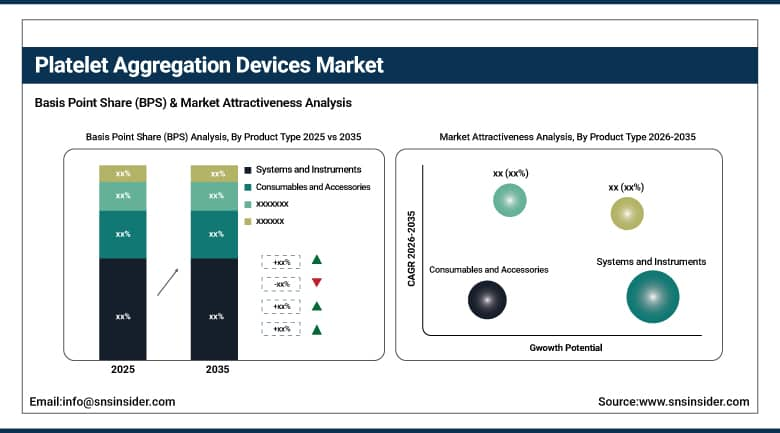

By Product Type, Systems and Instruments segment dominated the Platelet Aggregation Devices Market in 2025 with 64% share; Consumables and Accessories segment is the fastest growing segment.

-

By Application, Clinical Applications segment dominated the market in 2025 with 71% share; Research Applications segment is the fastest growing segment.

-

By End-use, Hospital segment dominated the market in 2025 with 58% share; Research and Academic Institutes segment is the fastest growing segment.

By Product Type, systems and instruments segment dominates the market, while consumables and accessories segment is the fastest-growing segment

The Systems and Instruments segment dominated the Platelet Aggregation Devices Market due to its important contribution in performing the platelet functions test accurately and reliably. Such instruments are used by healthcare centers and laboratories in routine tests, monitoring the antiplatelet therapy process, and detecting the blood disorders. The constant evolution of technology, their ability to be automated, along with the need for standardization of the procedure for diagnosing, has increased the demand. The long-lasting applicability and importance of these devices contribute significantly to maintaining the segment's leading market position.

The Consumables and Accessories segment is the fastest growing owing to continuous requirements for reagents, test kits, electrodes, cuvettes, and other consumable materials necessary for platelet aggregation test. Growing volume of tests being conducted, expansion of healthcare services and increasing number of installed platelet aggregometers are generating the need for the product consumption. Continuous replenishment of the laboratories with these materials is needed for smooth testing process.

By Application, clinical applications segment dominates the platelet aggregation devices market, while research applications segment is the fastest-growing segment

The Clinical Applications segment dominated the market because of the widespread application of platelet aggregation tests in diagnosing platelet function disorders, antiplatelet drug monitoring, and assessing bleeding risks. More healthcare professionals are employing such tests in order to aid in making treatment decisions for heart and blood diseases. This is largely because of increasing prevalence of chronic illnesses, awareness of personalized medicine, and increased need for patient monitoring.

The Research Applications segment is experiencing the fastest growth as a result of increasing investments in biomedical research, drug discovery, and research associated with platelet function. There is an increasing tendency by pharmaceutical and biotechnology companies, as well as academic centers, to apply advanced platelet aggregation testing tools in order to study disease pathology and effectiveness of treatments. Increasing number of clinical research programs, funding for research, and popularity of precision medicine are prompting the use of platelet function tests in research applications.

By End-use, hospital segment dominates the platelet aggregation devices market, while research and academic institutes segment is the fastest-growing segment.

The Hospital segment dominated the Platelet Aggregation Devices Market owing to the high volume of procedures undertaken at hospitals, which involved the determination of platelet function. The presence of advanced infrastructure, highly qualified personnel, and other healthcare facilities ensured high adoption rate of platelet aggregation devices in these institutions. Increased incidences of cardiovascular diseases, hemophilia, bleeding disorders, and surgeries further augmented the need for tests, thereby making hospitals the key end-user for these devices.

The Research and Academic Institutes segment is the fastest growing owing to increased scientific research in the fields of thrombosis, hemostasis, and blood disorders. These institutions have been using the platelet aggregation devices for conducting experiments and developing therapies. High investments in research, collaboration between academia and companies, and innovation in diagnosis technology are driving the adoption of platelet aggregation testing solution, leading to high growth potential of the segment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Platelet Aggregation Devices Market Insights

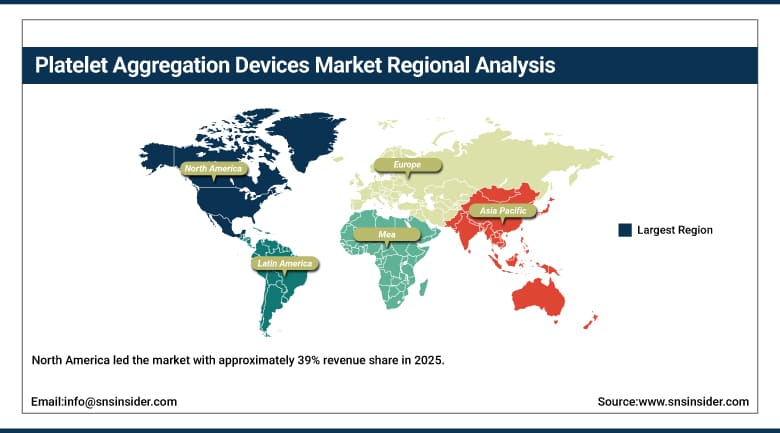

North America led the market with approximately 39% revenue share in 2025. Developed healthcare infrastructure, high cardiovascular disease awareness, and high research expenditures all support this lead. Strong healthcare systems combined with growing demand for diagnostic equipment in clinical environments drive this market leadership. Robust reimbursement policies and high adoption of advanced technologies in research institutions and hospitals further enhance market growth. The U.S. FDA has cleared multiple next-generation platelet function analyzers in recent years, further reinforcing domestic technology adoption.

The United States accounts for approximately 82.5% of North American revenue. The domestic market benefits from the presence of major device manufacturers including Medtronic, Beckman Coulter, Abbott, and Thermo Fisher. This combination of clinical demand and vendor presence keeps North America firmly in the lead.

Furthermore, the American Heart Association estimates that nearly 127 million U.S. adults live with at least one cardiovascular condition. The Centers for Medicare & Medicaid Services also reports healthcare spending exceeding USD 4.9 trillion, reflecting substantial investments in advanced hemostasis, coagulation, and platelet function testing technologies across the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Platelet Aggregation Devices Market Insights

Europe represents a meaningful platelet aggregation devices market, supported by strong pharmaceutical research and well-developed clinical laboratory infrastructure. Germany leads the regional market, backed by strong clinical diagnostics investment and pharmaceutical manufacturing. France and the UK contribute meaningful demand through their own well-funded clinical research and hospital sectors.

Germany accounts for approximately 24.6% of European revenue. European guidelines for cardiovascular disease management and antiplatelet therapy monitoring continue reinforcing demand. This regulatory environment should keep supporting steady European market growth.

Supporting this trend, the European Society of Cardiology reports that cardiovascular diseases cause approximately 1.7 million deaths annually within the European Union and nearly 3.9 million deaths across Europe.

Furthermore, Eurostat estimates that around 21% of the EU population is aged 65 years or older, increasing the prevalence of thrombotic disorders and the need for antiplatelet therapy monitoring. The European Commission also reports healthcare expenditure exceeding 10% of GDP in many member states, supporting investments in advanced laboratory diagnostics and coagulation testing systems.

Asia Pacific Platelet Aggregation Devices Market Insights

Asia Pacific is anticipated to expand at the fastest CAGR of approximately 8.61% through the forecast period. Enhanced healthcare infrastructure and growing awareness of cardiovascular diseases drive this rapid expansion. With sustained economic growth, there is an escalating need for sophisticated diagnostic solutions in the region. Government emphasis on healthcare accessibility and investments in medical technologies, combined with a fast-growing patient population, are key drivers.

China accounts for approximately 40.6% of Asia Pacific revenue. Rising cardiovascular disease burden and improving clinical laboratory infrastructure keep expanding regional demand. As healthcare spending and clinical diagnostics investment keep growing, this growth trajectory should continue strengthening.

Supporting this trend, the World Health Organization reports that cardiovascular diseases account for more than 10 million deaths annually across Asia, making cardiovascular diagnostics a major healthcare priority. In China, the National Health Commission estimates that over 330 million people are living with cardiovascular diseases, driving substantial demand for platelet and coagulation testing.

Additionally, India's Ministry of Health and Family Welfare reports that cardiovascular diseases account for approximately 28% of all deaths in the country, further increasing the need for advanced diagnostic testing solutions.

MEA & Latin America Platelet Aggregation Devices Market Insights

The UAE leads MEA revenue at approximately 22.8%. Growing healthcare infrastructure investment and rising cardiovascular disease awareness both support regional demand. Saudi Arabia is also expanding its clinical diagnostics capabilities as part of broader healthcare modernization.

Brazil leads Latin American revenue at approximately 43.8%. Expanding hospital networks and growing clinical laboratory investment both drive regional platelet aggregation device demand. Mexico and Argentina contribute secondary demand through their own expanding healthcare sectors.

Market Dynamics:

Growth Drivers: Rising cardiovascular disease rates driving diagnostic demand

With the increasing prevalence of cardiovascular diseases across the world, the need for advanced devices to diagnose and manage blood clots becomes increasingly important. Platelet aggregation devices are critical in assessing platelet functions and providing treatment for those patients who may suffer from blood clotting that may lead to heart attack and stroke. The increase in CVDs due to aging population, lack of physical activities, and unhealthy eating practices has made the need for diagnosis and treatment more urgent than ever before.

Due to the advancement in the field of diagnostic technology, the healthcare industry is witnessing the need to introduce improved technology to provide better treatment results. As the number of people who require testing and management of CVD conditions increases, the demand for platelet aggregation devices will keep increasing.

Restraints: High device costs limiting adoption in low-budget healthcare settings

The advanced technology incorporated into platelet aggregation equipment is responsible for its costly production and selling prices, which makes it inaccessible to certain healthcare facilities, particularly those operating on tight budgets. Platelet aggregation equipment requires huge investments, and the cost may prevent its availability to hospitals or clinics that have limited budgets.

Small-scale medical centers and developing countries may find it difficult to justify the initial investment in such an equipment. Even though there are numerous advantages of platelet aggregation equipment in practice, the cost factor is one of the biggest obstacles in its wide usage.

Opportunities: Technological innovation improving accessibility and affordability

Innovations in design and functionality, including portable, easy-to-use, and affordable units, are enlarging market development opportunities. These advances allow smaller medical facilities to acquire these devices and offer platelet function testing at lower cost. Reduced complexity also enables usage by a broader range of healthcare providers.

Affordability and smaller device sizes enable broader uptake, especially in emerging markets where cost-effectiveness matters most. As technology keeps advancing, platelet aggregation devices will become more accessible, allowing earlier diagnosis and improved management of blood clotting disorders globally.

Recent Developments:

-

2023: Sysmex Corporation launched the CN-8000 complete automatic platelet aggregation analyzer in November 2023, featuring a new optical system with high-resolution platelet imaging for improved diagnostic precision.

-

2023: Thermo Fisher Scientific launched the Acclaim 1000 platelet aggregation analyzer in July 2023, a fully automated high-throughput system with a new software algorithm providing fast and accurate test results.

-

2024: Medtronic enhanced its VerifyNow platelet function analyzer with updated EHR connectivity, enabling seamless integration of platelet function test results into electronic health record workflows.

Platelet Aggregation Devices Market Key Players are:

-

Werfen

-

Sysmex Corporation

-

Siemens Healthineers

-

Roche Diagnostics

-

Haemonetics Corporation

-

Helena Laboratories Corporation

-

Bio/Data Corporation

-

Chrono-Log Corporation

-

AggreDyne Inc.

-

Diagnostica Stago

-

Sentinel CH. SpA

-

TEM Innovations GmbH

-

Sienco Inc.

-

Drucker Diagnostics

-

Beckman Coulter

-

Abbott Laboratories

-

Thermo Fisher Scientific

-

Medtronic plc

-

Nihon Kohden Corporation

-

Hart Biologicals Ltd.

Platelet Aggregation Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 863.3 Million |

| Market Size by 2035 | USD 1,695 Million |

| CAGR | CAGR of 6.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Systems and Instruments, Consumables and Accessories) • By Application (Clinical Applications, Research Applications) • By End-use (Hospital, Diagnostic Centers, Research and Academic Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Werfen, Sysmex Corporation, Siemens Healthineers, Roche Diagnostics, Haemonetics Corporation, Helena Laboratories Corporation, Bio/Data Corporation, Chrono-Log Corporation, AggreDyne Inc., Diagnostica Stago, Sentinel CH. SpA, TEM Innovations GmbH, Sienco Inc., Drucker Diagnostics, Beckman Coulter, Abbott Laboratories, Thermo Fisher Scientific, Medtronic plc, Nihon Kohden Corporation, Hart Biologicals Ltd. |

Frequently Asked Questions

The Platelet Aggregation Devices Market is expected to grow at a CAGR of 6.99% from 2026 to 2035.

The Platelet Aggregation Devices Market was valued at USD 863.3 Million in 2025.

Rising global cardiovascular disease rates, increasing antiplatelet therapy monitoring needs, and growing research investment are the primary growth factors.

The systems and instruments segment dominated the market.

North America dominated the Platelet Aggregation Devices Market.

Get in Touch