Microfluidics Market Report Scope & Overview:

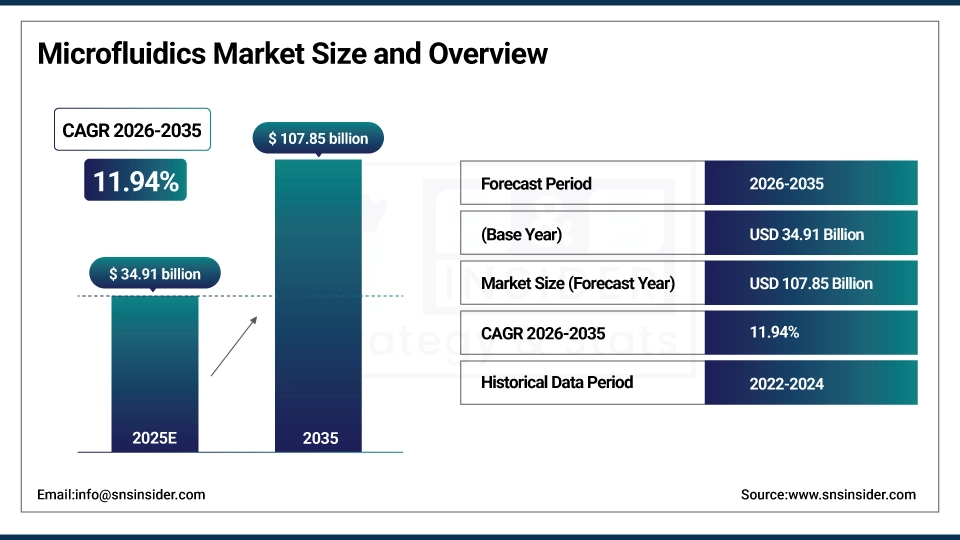

The Microfluidics Market size was valued at USD 34.91 billion in 2025 and is expected to reach USD 107.85 billion by 2035, growing at a CAGR of 11.94% over the forecast period of 2026-2035.

The global microfluidics market trend is a growing demand for miniaturized analytical solutions such as lab-on-a-chip devices, point-of-care diagnostics platforms, and organs-on-chips technologies as the growth of the market is driven by increasing adoption of precision medicine, rising demand for rapid diagnostic testing, and expanding investment in life sciences research and drug discovery. This trend is also driven by a growing adoption of polymer-based and PDMS microfluidic fabrication methods and the growing focus on portable, low-cost healthcare solutions as pharmaceutical companies, academic research institutions, and clinical diagnostics providers become more focused on improving throughput and accuracy of biological assays and are more willing to invest in advanced microfluidic platforms, resulting in growth in the domestic and international market for medical and non-medical microfluidics applications across PCR, gel electrophoresis, microarrays, and ELISA workflows.

For instance, in March 2024, growing investment in point-of-care diagnostics and lab-on-a-chip development drove a 19% increase in microfluidics platform deployments across clinical and research laboratories in North America, boosting rapid test throughput and decentralized diagnostics adoption.

Microfluidics Market Size and Forecast:

-

Market Size in 2025E: USD 34.91 billion

-

Market Size by 2035: USD 107.85 billion

-

CAGR: 11.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Microfluidics Market - Request Free Sample Report

Microfluidics Market Trends

-

Microfluidics solutions are being adopted because researchers and clinicians demand faster turnaround for molecular diagnostics, including PCR, RT-PCR, and ELISA assay workflows in point-of-care and laboratory settings.

-

Customized organ-on-a-chip and tissue-on-a-chip platforms based on patient-specific cell models and disease biology to improve drug screening accuracy and reduce reliance on animal testing in pharmaceutical R&D.

-

The development of polymer and PDMS-based fabrication techniques, 3D-printed microfluidic devices, and digital microfluidics platforms to improve manufacturing scalability and reduce per-unit production costs.

-

Continuous flow microfluidics, optofluidics, and acoustofluidics systems are all increasingly deployed to ensure precise fluid manipulation, cell sorting, and particle separation in clinical and industrial applications.

-

Increased demand for glass and silicon-based microfluidic chips with enhanced chemical resistance and optical clarity to support high-sensitivity microarray and electrophoresis applications in genomics and proteomics research.

-

Collaboration between microfluidics device manufacturers, semiconductor companies, and life sciences instrument makers to develop fully integrated lab-on-a-chip systems and improve standards of assay miniaturization and automation.

-

FDA, NIH, and DARPA promoting standards for microfluidic device validation, biocompatibility testing, and regulatory pathways for organ-on-chip platforms as alternative preclinical models in drug safety evaluation.

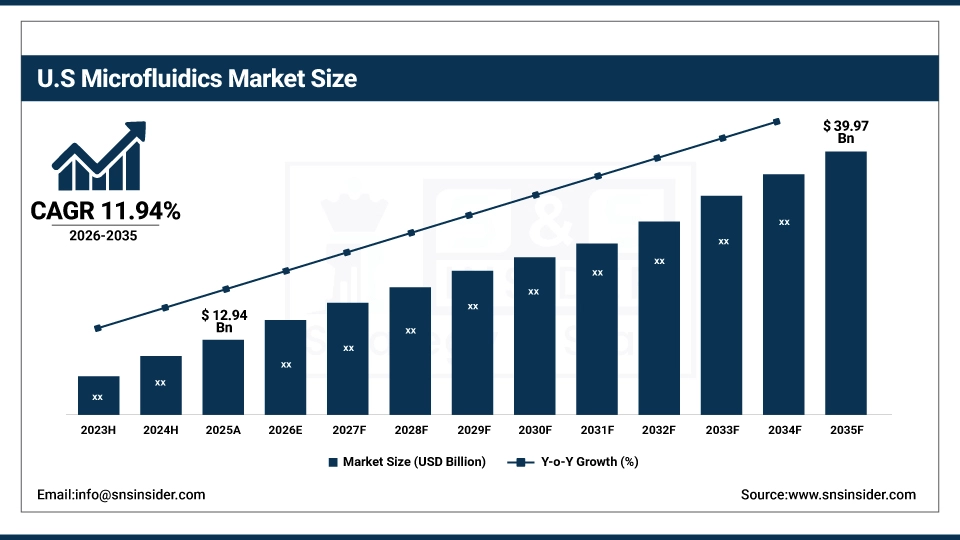

The U.S. Microfluidics Market was valued at USD 12.94 billion in 2025 and is expected to reach USD 39.97 billion by 2035, growing at a CAGR of 11.94% from 2026-2035. The United States represents the largest market for microfluidics, primarily driven by the concentration of leading pharmaceutical and biotechnology companies, robust federal funding for life sciences research, and a well-developed clinical diagnostics infrastructure. Government investment through NIH and DARPA, moderately high levels of healthcare R&D spending, and increased adoption of microfluidic platforms in drug discovery and molecular diagnostics help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of lab-on-a-chip and point-of-care microfluidics solutions.

Microfluidics Market Growth Drivers:

-

Rising Demand for Point-of-Care Diagnostics and Rapid Molecular Testing is Driving the Microfluidics Market Growth

Rising demand for point-of-care diagnostics and rapid molecular testing takes the center stage as a growth driver for the microfluidics market share, and are driven by the increasing burden of infectious diseases, growing need for decentralized healthcare delivery, and expanded adoption of PCR and RT-PCR-based microfluidic assays in clinical and field settings. These platforms for miniaturized diagnostics and high-throughput screening are expanding the base of the market, the penetration of lab-on-a-chip and polymer microfluidic device markets, and adding to the overall market share globally.

For instance, in May 2024, lab-on-a-chip and integrated microfluidic diagnostic platforms accounted for ~62% of the total U.S. point-of-care diagnostics technology investments, reflecting growing institutional preference and expanding market share.

Microfluidics Market Restraints:

-

High Fabrication Costs and Scalability Challenges are Hampering the Microfluidics Market Growth

High fabrication costs and scalability challenges of microfluidic devices also restrict the microfluidics market growth, as a large number of research institutions and small diagnostics companies that have developed prototype microfluidic systems remain unable to transition to commercial-scale manufacturing or face difficulties standardizing chip production at volume. This might lead to limited commercialization, delayed market entry, and reduced return on investment for academic spinouts and early-stage microfluidics startups. As a result, technology adoption suffers and market growth is stunted in regions where precision microfabrication infrastructure is limited and regulatory approval pathways for novel microfluidic diagnostics remain complex.

Microfluidics Market Opportunities:

-

Expansion of Organ-on-Chip Platforms and Pharmaceutical Drug Discovery Applications Drive Future Growth Opportunities for the Microfluidics Market

The opportunity in organ-on-chip platforms and pharmaceutical drug discovery applications in the microfluidics market is in the form of physiologically relevant in vitro models, predictive toxicology screening, and personalized medicine research. These solutions provide for early-stage identification of drug candidates, individualized disease modeling capabilities, and real-time monitoring of cellular responses under controlled microenvironments. Through enhanced preclinical screening accuracy, reduced animal testing dependency, and expanded application in rare disease research, particularly in areas with high unmet clinical need and active pharmaceutical pipeline activity, these technologies may improve drug development outcomes, reduce time-to-approval, and expand the market.

For instance, in April 2024, the FDA reported that organ-on-chip and microfluidic preclinical testing platforms were actively used in approximately 38% of novel drug submissions from major U.S. pharmaceutical companies, highlighting rising platform credibility and increasing demand for microfluidics-based drug development tools.

Microfluidics Market Segment Analysis

-

By application, medical/healthcare held the largest share of around 72.46% in 2025E, and the non-medical segment is expected to register the highest growth with a CAGR of 12.87%.

-

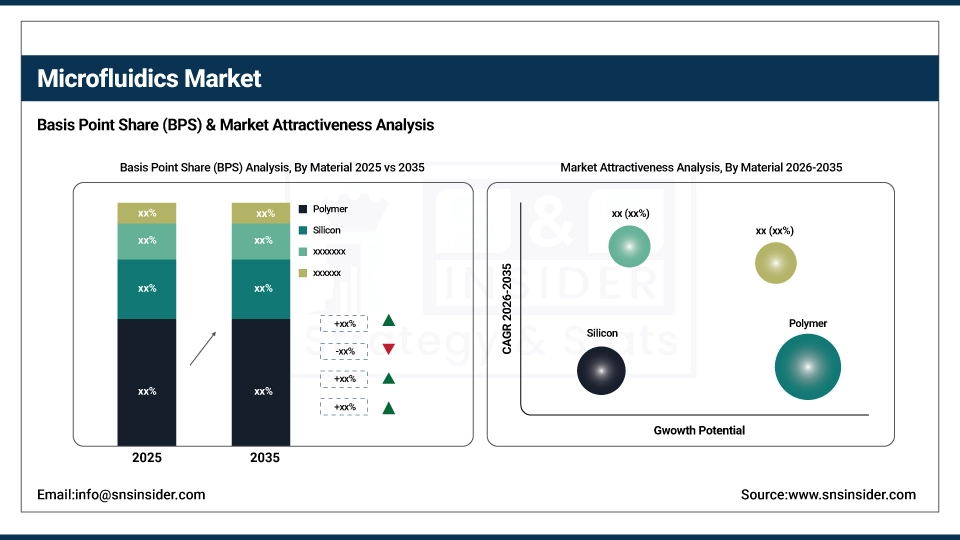

By material, polymer dominated the market with approximately 41.38% share in 2025E, while the PDMS segment is expected to register the highest growth with a CAGR of 13.21%.

-

By technology, lab-on-a-chip accounted for the leading share of nearly 38.62% in 2025E, and organs-on-chips is expected to register the highest growth with a CAGR of 14.53%.

By Material, Polymer Dominates, while PDMS Segment Shows Rapid Growth

By 2025, the polymer segment contributed the largest revenue share of 41.38% due to its low cost, ease of fabrication, optical transparency, and compatibility with a wide range of biological fluids and assay chemistries, making it the preferred material for disposable microfluidic cartridges and high-volume diagnostic applications. Growing adoption of injection-molded and hot-embossed polymer microfluidic chips, coupled with their suitability for mass production, is driving continued material dominance. The PDMS segment is projected to grow at the highest CAGR of about 13.21% between 2026 and 2035 due to its unmatched flexibility, gas permeability, and biocompatibility that make it uniquely suited for organ-on-chip fabrication and academic research applications. Some of the reasons include superior surface modification capabilities, better optical clarity for live-cell imaging, and life sciences researchers’ preference for PDMS in complex microfluidic network prototyping.

By Application, Medical/Healthcare Leads the Market, While Non-Medical Registers Fastest Growth

The medical/healthcare segment accounted for the highest revenue share of approximately 72.46% in 2025, owing to widespread adoption of microfluidic platforms across PCR and RT-PCR molecular diagnostics, gel electrophoresis workflows, microarray-based genomics, and ELISA immunoassay applications in hospitals, clinical laboratories, and research centers. Emerging trends, including increasing demand for multiplexed assay capabilities and the growing focus on rapid infectious disease diagnostics and personalized medicine. In comparison, the non-medical segment is anticipated to achieve the highest CAGR of nearly 12.87% during the 2026–2035 period, driven by the increasing adoption of microfluidics in environmental monitoring, food safety testing, chemical synthesis, and energy applications. Drivers include rising demand for portable field-deployable analytical devices, the preference for miniaturized sensor platforms in industrial quality control, and growing investment in microfluidic fuel cells and water quality analysis tools.

By Technology, Lab-on-a-Chip Leads, and Organs-on-Chips Registers Fastest Growth

The lab-on-a-chip segment accounted for the largest share of the microfluidics market with about 38.62%, owing to its established role in integrating multiple laboratory functions onto a single miniaturized chip for clinical diagnostics, drug screening, and genomic analysis applications. Reasons driving the lab-on-a-chip segment include increasing adoption across decentralized diagnostic settings, growing demand for fully automated sample-to-answer workflows, and strong commercial product availability from leading instrument vendors. In addition, the organs-on-chips segment is slated to grow at the fastest rate with a CAGR of around 14.53% throughout the forecast period of 2026–2035, as pharmaceutical companies and contract research organizations seek physiologically accurate human organ models for toxicology screening, disease modeling, and personalized drug response prediction. Increased focus on reducing preclinical trial failures and regulatory pressure to reduce animal testing in drug safety assessment contribute to their adoption, while improved funding from government agencies and venture capital for organ-on-chip platform development drives continued investment.

Microfluidics Market Regional Highlights:

North America Microfluidics Market Insights:

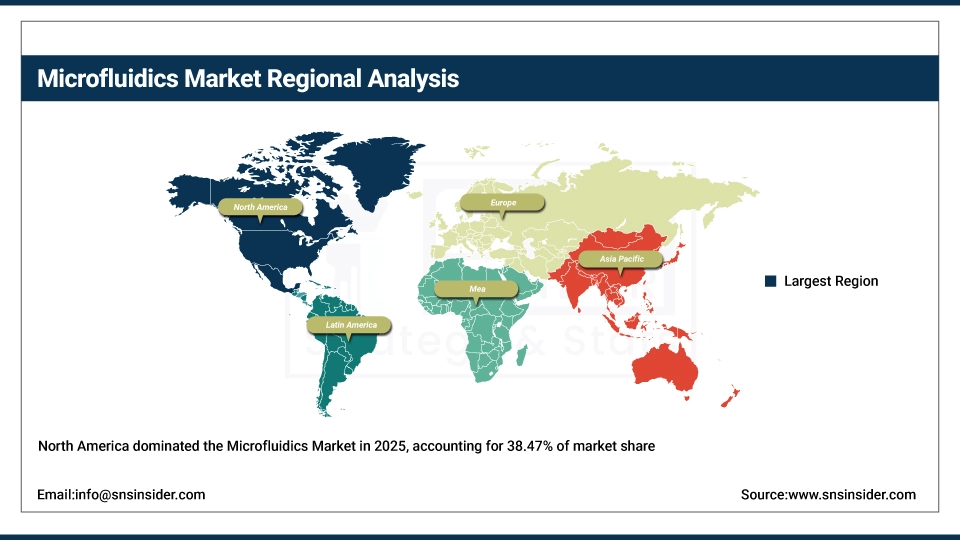

North America held the largest revenue share of over 38.47% in 2025 of the microfluidics market due to a well-established life sciences research ecosystem, strong federal funding from NIH, DARPA, and NSF for microfluidic technology development, and increased clinical adoption of lab-on-a-chip diagnostic platforms across hospitals and reference laboratories. Drivers include the concentration of leading microfluidics companies and academic research institutions, an advanced biomedical device manufacturing infrastructure, growing adoption of continuous flow and digital microfluidics in pharmaceutical drug discovery, and greater acceptance of organ-on-chip models as regulatory-grade preclinical testing tools. At the same time, various government initiatives promoting innovation in precision diagnostics and enormous investments from pharmaceutical and diagnostics companies are anchoring microfluidics platforms and services in the market, and ensuring multibillion dollar revenues across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Microfluidics Market Insights:

Asia Pacific is the fastest-growing segment in the microfluidics market with a CAGR of 13.76%, as the awareness about miniaturized diagnostics solutions, government investment in life sciences and biotechnology research, and healthcare infrastructure modernization in countries such as China, Japan, South Korea, and India is growing. Factors including rapid expansion of pharmaceutical manufacturing, rising incidence of infectious and chronic diseases driving diagnostic demand, and growing uptake of point-of-care testing in clinical and community health settings are stimulating the market growth. National biotechnology development programs and academic-industry research partnerships have been instrumental in advancing microfluidic chip fabrication capabilities and expanding access to lab-on-a-chip diagnostics, especially in urban research and hospital environments. Public-private partnerships and government programs also help in advancing life sciences innovation and digital health transformation. Increase in demand in the Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing affordability and accessibility of polymer-based microfluidic diagnostic platforms.

Europe Microfluidics Market Insights:

The microfluidics market in Europe is the second-dominating region after North America on account of an increase in the adoption of lab-on-a-chip diagnostic devices, robust regulatory frameworks governing in vitro diagnostic (IVD) products under the EU IVDR, and increasing investment in organ-on-chip and precision medicine research across leading academic and pharmaceutical institutions. Rising implementation of Horizon Europe-funded microfluidics research programs, advanced national biotechnology strategies, favorable government funding for health technology projects, and cross-border life sciences collaboration initiatives are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Microfluidics Market Insights:

In Latin America, and Middle East & Africa, the growing healthcare infrastructure investment and increase in internet connectivity with expanding laboratory diagnostics capacity support the microfluidics market growth. The rising popularity of affordable polymer-based microfluidic diagnostic kits and multilingual platform capabilities, along with public health awareness campaigns around infectious disease management, will aid healthcare accessibility and decentralized diagnostics adoption. The increasing urban population and improving clinical laboratory infrastructure in these regions are continuing to encourage market growth.

Microfluidics Market Competitive Landscape:

Hoffmann-La Roche Ltd. (est. 1896) is a global leader in in vitro diagnostics and pharmaceutical research that focuses on integrated microfluidic diagnostic platforms for molecular testing and personalized healthcare. It uses its extensive clinical diagnostics portfolio and global laboratory network to deliver cutting-edge lab-on-a-chip and PCR-based microfluidic solutions with seamless integration into hospital and reference laboratory workflows.

-

In February 2025, it expanded its microfluidics-based molecular diagnostics portfolio with next-generation lab-on-a-chip PCR cartridges featuring AI-assisted result interpretation and multiplexed pathogen detection, targeting hospital laboratories and decentralized testing sites across North America and Europe.

Agilent Technologies, Inc. (est. 1999) is a well-known global life sciences instrumentation and analytical solutions company focused on microfluidic chip electrophoresis, microarray analysis, and genomics research platforms. It invests in silicon and glass-based microfluidic chip technologies and integrated analytical instruments with the hopes of revolutionizing genomics, proteomics, and molecular biology workflows with high-sensitivity and high-throughput capabilities.

-

In June 2024, launched an enhanced Bioanalyzer microfluidic chip platform featuring expanded RNA integrity analysis and single-cell sequencing library quality control capabilities, deployed across leading genomics research institutions and biopharma organizations globally.

Emulate, Inc. (est. 2013) is a leading organ-on-chip technology company in the field of human biology emulation platforms for pharmaceutical drug discovery, safety testing, and disease modeling. The company’s organ-on-chip product portfolio focuses on physiologically accurate microfluidic tissue models, and features a strong commitment to regulatory science collaboration and continuous innovation to complement a strong market presence among global pharmaceutical companies and academic research centers.

-

In October 2024, introduced an expanded Human Emulation System platform with new organ-chip models for liver toxicity and lung inflammation research, strengthening preclinical drug testing capabilities and expanding commercial adoption among top-20 global pharmaceutical companies.

Microfluidics Market Key Players:

-

F. Hoffmann-La Roche Ltd.

-

Agilent Technologies, Inc.

-

Emulate, Inc.

-

Dolomite Microfluidics

-

Fluidigm Corporation

-

Bio-Rad Laboratories, Inc.

-

Becton, Dickinson and Company

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

Illumina, Inc.

-

Micralyne Inc.

-

Microfluidic ChipShop GmbH

-

RainDance Technologies

-

10x Genomics, Inc.

-

Sphere Fluidics Limited

-

Micronit B.V.

-

IDEX Health & Science LLC

-

Hamamatsu Photonics K.K.

-

MilliporeSigma

-

Caliper Life Sciences

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 34.91 billion |

| Market Size by 2035 | USD 107.85 billion |

| CAGR | CAGR of 11.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Historical Data | 2022–2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Medical/Healthcare, Non-medical) • By Material (Silicon, Glass, Polymer, PDMS, Others) • By Technology (Lab-on-a-chip, Organs-on-chips, Continuous Flow Microfluidics, Optofluidics and Microfluidics, Acoustofluidics and Microfluidics, Electrophoresis and Microfluidics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | F. Hoffmann-La Roche Ltd., Agilent Technologies Inc., Emulate Inc., Dolomite Microfluidics, Fluidigm Corporation, Bio-Rad Laboratories Inc., Becton, Dickinson and Company, Thermo Fisher Scientific Inc., Abbott Laboratories, Illumina Inc., Micralyne Inc., Microfluidic ChipShop GmbH, RainDance Technologies, 10x Genomics, Inc., Sphere Fluidics Limited, Micronit B.V., IDEX Health & Science LLC, Hamamatsu Photonics K.K., MilliporeSigma, Caliper Life Sciences |

Frequently Asked Questions

Ans: The Microfluidics Market is expected to grow at a CAGR of 11.94% over the forecast period.

Ans: The Microfluidics Market size was valued at USD 34.91 billion in 2025 and is expected to reach USD 107.85 billion by 2035.

Ans: Rising Demand for Point-of-Care Diagnostics and Rapid Molecular Testing is Driving the Microfluidics Market Growth.

Ans: Asia Pacific is the fastest-growing region with a CAGR of 13.76%.

Ans: North America dominated the Microfluidics Market in 2025.

Get in Touch