Polyimide Film Market Report Scope & Overview:

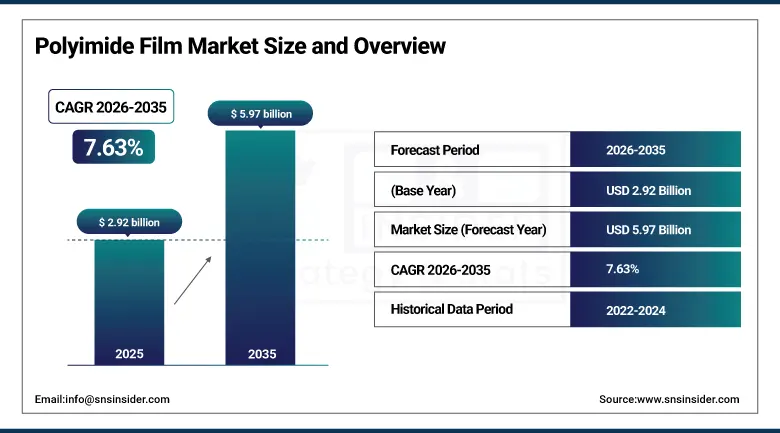

The Polyimide Film Market was valued at USD 2.92 billion in 2025 and is expected to reach USD 5.97 billion by 2035, growing at a CAGR of 7.63% from 2026–2035.

Polyimide film represents one of the most technically demanding and commercially valuable categories within the advanced polymer materials market, where the unique combination of extreme thermal stability up to 400 degrees Celsius continuous operating temperatures, outstanding dielectric strength enabling reliable electrical insulation in high-voltage and high-frequency applications, excellent mechanical properties including tensile strength, elongation, and dimensional stability maintained across wide temperature ranges, and inherent chemical resistance to solvents, fuels, and industrial fluids collectively create a material whose performance envelope cannot be matched by competing polymer film alternatives across the most technically demanding application environments in electronics, aerospace, automotive, and energy. Polyimide film is synthesised through the polycondensation reaction of aromatic dianhydrides with aromatic diamines to form a polyamic acid intermediate that is subsequently imidised through thermal or chemical treatment to produce the final polyimide polymer chain whose aromatic ring backbone and imide linkage provide the structural basis for the material's exceptional thermal and chemical stability.

The International Data Corporation's 2025 global device shipment data confirming annual shipment volumes of 1.4 billion smartphones, 170 million tablets, and 350 million laptop computers, each incorporating multiple flexible printed circuit assemblies that use polyimide film as the substrate material, provides the most direct quantification of the consumer electronics-driven polyimide film demand base whose continued growth with each device product generation cycle sustains fundamental market expansion independent of any individual application or end-use industry trend.

Market Size and Forecast

- Market Size in 2026E: USD 3.14 Billion

- Market Size by 2035: USD 5.97 Billion

- CAGR: 7.63% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: Asia Pacific

To Get more information on Polyimide Film Market - Request Free Sample Report

Polyimide Film Market Trends

- Accelerating adoption of polyimide film in electric vehicle battery systems where its combination of thermal stability, dielectric strength, and chemical resistance to battery electrolyte enables reliable inter-cell insulation, cell-to-module separator applications, and flexible circuit integration for battery management system electronics whose performance requirements in the battery thermal environment exceed the capability of alternative insulation film materials.

- Growing demand for low-dielectric constant polyimide film variants incorporating fluorine substituents or porous microstructure modifications that reduce dielectric constant below the standard 3.4 of conventional polyimide toward 2.6 to 2.9 values that improve signal transmission speed and reduce cross-talk in high-frequency 5G antenna circuits, millimetre-wave communications modules, and advanced semiconductor packaging substrates.

- Increasing adoption of colourless or transparent polyimide film in flexible OLED display substrate applications, where the conventional yellow-brown colour of standard polyimide film is incompatible with the optical requirements of transparent or see-through flexible display architectures, driving development of colourless polyimide film incorporating bulky substituents or aliphatic segments that reduce aromatic chromophore concentration while maintaining acceptable thermal stability.

- Rising use of polyimide film in solar photovoltaic module backsheet and encapsulant applications, where its combination of UV stability, moisture barrier properties, and thermal cycling endurance addresses the 25-year outdoor exposure performance requirement that solar panel component materials must satisfy, creating a renewable energy application growing in parallel with global solar capacity expansion.

- Growing integration of polyimide film in aerospace composite structures and space-qualified spacecraft thermal insulation multilayer blankets where the material's vacuum-compatible outgassing properties, wide operational temperature range spanning cryogenic to high solar flux conditions, and radiation resistance meet the unique performance requirements of space system thermal management applications.

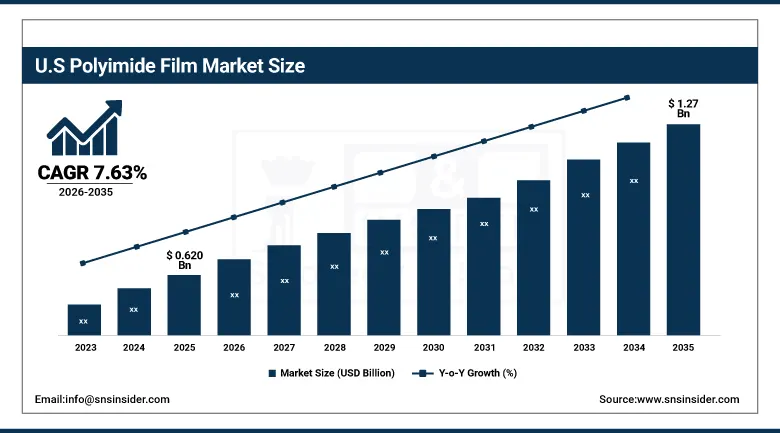

The U.S. Polyimide Film Market Outlook

The U.S. polyimide film market was valued at approximately USD 0.620 billion in 2025 and is expected to reach approximately USD 1.27 billion by 2035, growing at a CAGR of 7.63%, driven by advanced electronics manufacturing, aerospace and defence applications requiring high-performance insulation materials, growing automotive electric vehicle demand for EV battery insulation, and the presence of DuPont, the world's leading polyimide film manufacturer, whose domestic manufacturing and R&D operations sustain U.S. market supply and innovation leadership.

The United States is the world's largest national polyimide film market by revenue outside Asia, where DuPont's Kapton product line has been the foundational commercial reference for polyimide film performance standards since the material's commercial introduction in the 1960s, and where the concentration of aerospace and defence electronics manufacturing, semiconductor back-end packaging operations, and advanced automotive research create sustained premium-grade polyimide film demand that supports above-average price per kilogram relative to the volume-driven consumer electronics markets that dominate Asian polyimide film consumption. The U.S. Department of Defense's extensive use of polyimide film in military aircraft electronics, spacecraft components, and missile systems creates a defence-specific demand segment that sustains domestic polyimide film procurement independent of commercial market cycles, providing price stability and volume predictability that supports domestic manufacturing capacity maintenance.

The U.S. CHIPS and Science Act's substantial investment in domestic semiconductor manufacturing infrastructure is creating significant new demand for high-performance polyimide film in semiconductor package substrate applications where the advanced chip packaging technologies including fan-out wafer-level packaging and 2.5D/3D packaging require polyimide film as a redistribution layer dielectric material whose thermal stability during package assembly processing and reliability under chip operating conditions distinguish it from competing organic dielectric alternatives.

Polyimide Film Market Segment Analysis

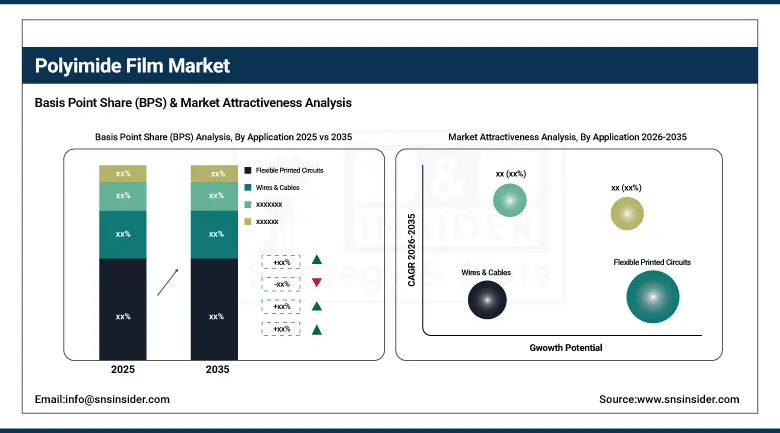

- By Application, Flexible Printed Circuits dominated with approximately 40% of revenues in 2025 driven by extensive use in consumer electronics, industrial equipment, and automotive applications requiring high thermal stability and durability; Wires & Cables held approximately 25% through adoption in automotive, aerospace, and energy applications; Pressure-Sensitive Tapes held approximately 15% for insulation and bonding purposes in high-temperature manufacturing.

- By End-Use Industry, Electronics dominated with approximately 54% in 2025 through rising adoption in smartphones, tablets, wearable devices, and consumer electronics requiring lightweight, high-performance insulating materials; Automotive held approximately 15% driven by increasing use in electric vehicle battery systems, wiring harnesses, and motor insulation; Aerospace represented a significant premium segment through thermal insulation blankets, aircraft wiring, and spacecraft applications.

By Application, flexible printed circuits dominate, wires & cables are a key growth segment

Flexible Printed Circuits retained the dominant application position with approximately 40% of the Polyimide Film Market in 2025, as the universal adoption of flex circuit assemblies across consumer electronics, industrial controls, medical devices, and automotive electronics creates the highest-volume individual application in the polyimide film market whose per-unit film consumption is modest but whose aggregate volume across billions of annual device productions creates the largest total demand. Polyimide film serves as the substrate material for flexible printed circuits in two configurations: as a single-sided or double-sided substrate onto which copper conductor traces are laminated or plated, providing the structural support and electrical insulation between conductor layers; and as a cover layer laminated over the outer conductor surface providing the mechanical protection, chemical resistance, and electrical insulation of the circuit's exterior surface. The technical requirements for FPC substrate polyimide film include dimensional stability during the high-temperature lamination and reflow soldering operations of circuit assembly, surface smoothness for fine-pitch copper trace adhesion, and flexural endurance under the repeated bending cycles that flexible circuit connectors must survive in their operational service life within the product.

Wires and Cables represent a substantial application segment holding approximately 25% of revenues in 2025, serving the high-temperature wiring requirements of aerospace, military, industrial, and increasingly automotive electric vehicle applications where conventional PVC and cross-linked polyethylene wire insulation materials cannot maintain dielectric integrity at the continuous operating temperatures that aircraft, spacecraft, industrial motors, and EV powertrain components generate. Magnet wire insulation in electric motor and transformer windings represents a particularly technically demanding wires and cables polyimide film application where multiple thin overlapping wraps of polyimide film around the copper conductor provide the combined flexibility, dielectric strength, and thermal stability that motor winding operations require, with the polyimide's superior thermal class enabling motor designs that achieve higher power density through tighter winding configurations operating at temperatures that conventional insulation materials cannot withstand.

By End-Use, electronics dominates, automotive is a key growing segment

Electronics retained the dominant end-use industry position with approximately 54% of the Polyimide Film Market in 2025, encompassing the full range of consumer electronics, industrial electronics, and semiconductor applications that individually constitute the world's largest volume polyimide film consumption context, where the aggregated demand from the billions of flexible printed circuits, hundreds of millions of semiconductor packages, and tens of millions of display substrates produced annually creates a demand base whose continued expansion with each electronic device product generation cycle sustains fundamental volume growth. The semiconductor packaging application of polyimide film is growing with particular dynamism as the advanced heterogeneous integration packaging architectures that the semiconductor industry is adopting to overcome the physical limits of monolithic chip scaling create new polyimide film demand for redistribution layer dielectrics, inter-chiplet insulation, and flexible substrate structures that contain multiple integrated circuit dies in configurations that optimise performance and power efficiency beyond what single-chip designs achieve.

Automotive is a strongly growing end-use segment at approximately 15% of revenues in 2025, with growth acceleration driven by the electric vehicle market's expansion creating new high-performance polyimide film demand across battery cell insulation, EV drive system wiring, and automotive flexible circuit applications where the thermal and chemical environment of battery and motor systems requires insulation material performance that polyimide provides and commodity automotive insulation alternatives cannot match. Each battery electric vehicle contains substantially more flexible circuit cabling than an equivalent internal combustion engine vehicle, driven by the battery management system's need to monitor and balance individual cell voltages and temperatures across large battery pack arrays using sensor wiring that must operate reliably in the battery's electrochemical environment over the vehicle's service life.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.7% |

|

Europe |

Germany |

27.4% |

|

Asia Pacific |

China |

53.2% |

|

Middle East & Africa |

UAE |

26.8% |

|

Latin America |

Brazil |

43.4% |

North America Polyimide Film Market Insights

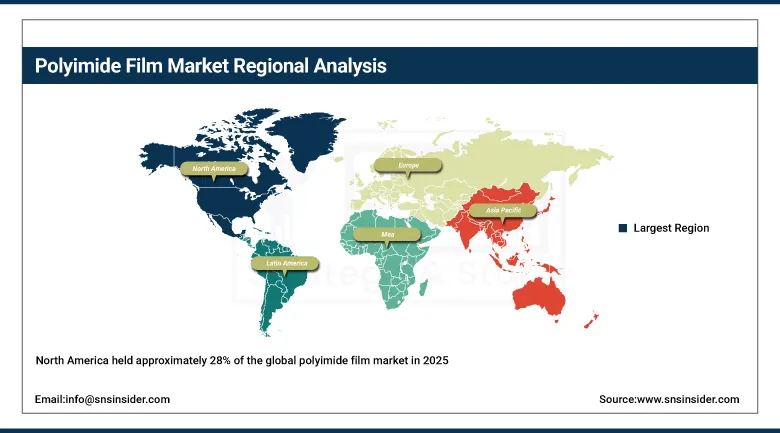

North America held approximately 28% of the global polyimide film market in 2025, with the United States accounting for approximately 84.7% of North American revenues. The region's market position reflects the concentration of high-value aerospace, defence electronics, and semiconductor manufacturing applications that consume premium-grade polyimide film at above-average prices compared with the volume-driven consumer electronics applications dominating Asian consumption. DuPont's U.S.-headquartered Kapton polyimide film operations sustain domestic manufacturing and innovation investment that provides supply chain reliability advantages for U.S. defence and aerospace customers whose procurement specifications require domestic sourcing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Polyimide Film Market Insights

Europe is a technically sophisticated polyimide film market driven by aerospace and defence applications from Airbus, MBDA, and European spacecraft manufacturers, industrial electronics and motor manufacturing in Germany and Central Europe, and automotive wiring system production across the European vehicle manufacturing base that includes a rapidly growing electric vehicle production segment creating new polyimide film demand. Germany accounts for approximately 27.4% of European polyimide film revenues as the region's largest industrial economy whose combination of automotive manufacturing, industrial electronics, and advanced materials research creates consistent demand for performance-grade polyimide film across multiple application categories.

Asia Pacific Polyimide Film Market Insights

Asia Pacific dominated the global polyimide film market in 2025 with approximately 39.13% of revenues and is simultaneously the fastest-growing regional market, reflecting the region's extraordinary concentration of consumer electronics manufacturing, the most rapidly expanding electric vehicle production in China, and the semiconductor back-end packaging operations across Taiwan, South Korea, Japan, and increasingly Vietnam and Malaysia that collectively generate the world's largest aggregate polyimide film consumption. China accounts for approximately 53.2% of Asia Pacific revenues through its position as the world's largest consumer electronics manufacturer, the largest EV producer, and a rapidly developing domestic polyimide film manufacturing industry that competes with Japanese and American imports in the mid-tier quality segment while developing toward the premium applications that historically required imported material.

MEA & Latin America Polyimide Film Market Insights

The Middle East and Africa and Latin America are developing polyimide film markets where industrial manufacturing development, growing electronics assembly operations, and expanding automotive production are creating initial but growing demand. UAE leads MEA polyimide film revenues at approximately 26.8% of regional revenues through its growing electronics assembly, aerospace MRO, and advanced manufacturing sectors. Brazil leads Latin American revenues at approximately 43.4% through its electronics manufacturing, automotive production including growing EV assembly, and aerospace industry represented by Embraer's aircraft manufacturing operations that use polyimide film in aircraft wiring and avionics applications.

Market Dynamics

Growth Drivers: Electric vehicle market expansion creating large-scale new polyimide film demand for battery insulation

The primary structural growth drivers for the polyimide film market are the electric vehicle market's extraordinary global expansion that is creating substantial new polyimide film demand across battery cell insulation, EV wiring systems, and automotive electronics circuits where the electrical and thermal environment of battery-electric powertrains requires insulation material performance that polyimide provides and commodity alternatives cannot reliably deliver, combined with the continued expansion of consumer electronics production volumes whose flexible printed circuit assemblies create the market's largest-volume polyimide film demand base that grows with each generational product upgrade cycle. The emergence of 5G network infrastructure, millimetre-wave communications modules, and advanced semiconductor packaging as growth areas for low-dielectric polyimide film variants whose specialised optical, electrical, and thermal properties command meaningful price premiums over standard material is sustaining revenue growth above the volume growth rate.

Restraints: Premium pricing relative to competing polymer films limiting adoption in cost-sensitive applications

A significant restraint on the polyimide film market is the cost disadvantage of polyimide film relative to competing polymer film materials including polyethylene naphthalate, polyethylene terephthalate, and liquid crystal polymer whose manufacturing costs are substantially lower and whose performance in less demanding temperature and chemical exposure environments is adequate for the application requirement, creating systematic displacement pressure from polyimide in applications where its performance margin over less expensive alternatives exceeds what the cost premium justifies from an application engineering perspective. The supply chain concentration of premium polyimide film production in a small number of manufacturers including DuPont, Kaneka, Kolon, and Ube Industries creates procurement risk for major users in aerospace, defence, and semiconductor applications where qualified source requirements and product qualification timelines make supply chain disruption particularly consequential.

Opportunities: Colourless polyimide for flexible OLED displays creating premium new application

The commercialisation of colourless polyimide film for flexible and foldable OLED display applications represents the most commercially significant near-term product innovation opportunity in the polyimide film market, as the foldable smartphone category whose display architectures require transparent high-temperature polymer substrates has created a technically demanding and commercially premium demand for colourless polyimide film whose synthesis complexity and processing difficulty currently limit supply to a small number of capable manufacturers who command significant price premiums over standard amber-coloured polyimide film in this specialised application. Samsung's Galaxy Z Fold series and competing foldable devices from Huawei and Motorola have established a commercially growing product category whose display substrate requirements create sustained colourless polyimide film demand that is expected to scale significantly as foldable device price points decline toward mainstream consumer affordability.

Recent Developments:

- 2025: DuPont expanded its Kapton polyimide film production capacity at its Circleville, Ohio manufacturing facility to address growing demand from EV battery insulation and semiconductor packaging applications, investing in new production lines designed to manufacture both standard and specialty low-dielectric polyimide film grades serving the expanding high-performance electronics markets.

- 2025: Kaneka Corporation announced development of its next-generation colourless polyimide film for flexible display applications, achieving improved optical transparency and colour neutrality while maintaining the thermal stability required for backplane transistor manufacturing processes that require substrate exposure to temperatures exceeding 300 degrees Celsius during thin-film transistor deposition.

- 2025: Kolon Industries expanded its polyimide film production capacity in South Korea to serve growing domestic demand from Samsung Display's foldable OLED display manufacturing and LG Electronics' flexible display panel production, positioning the company as a preferred domestic supply source for South Korean display manufacturers seeking to reduce import dependency.

Polyimide Film Market Key Players are:

- DuPont de Nemours Inc. (Kapton)

- Kaneka Corporation

- Kolon Industries Inc.

- Ube Industries Ltd.

- Taimide Tech Inc.

- SKC Kolon PI

- Toray Industries Inc.

- Nitto Denko Corporation

- Sumitomo Electric Industries Ltd.

- Arakawa Chemical Industries Ltd.

- Nexolve Holdings LLC

- Saint-Gobain S.A.

- I.S.T. Corporation

- Anabond Limited

- Shinmax Technology Ltd.

- Isovolta AG

- FLEXcon Company Inc.

- Krempel GmbH

- Pi Advanced Materials Co. Ltd.

- Zhongke Funeng Co. Ltd.

Polyimide Film Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.92 Billion |

| Market Size by 2035 | USD 5.97 Billion |

| CAGR | CAGR of 7.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Application (Flexible Printed Circuits, Wires & Cables, Pressure-Sensitive Tapes, Specialty Fabricated Products, Motors & Generators, Others) •By End-Use Industry (Electronics, Automotive, Aerospace, Labeling, Solar, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DuPont de Nemours Inc. (Kapton), Kaneka Corporation, Kolon Industries Inc., Ube Industries Ltd., Taimide Tech Inc., SKC Kolon PI, Toray Industries Inc., Nitto Denko Corporation, Sumitomo Electric Industries Ltd., Arakawa Chemical Industries Ltd., Nexolve Holdings LLC, Saint-Gobain S.A., I.S.T. Corporation, Anabond Limited, Shinmax Technology Ltd., Isovolta AG, FLEXcon Company Inc., Krempel GmbH, PI Advanced Materials Co. Ltd., and Zhongke Funeng Co. Ltd. |

Frequently Asked Questions

Get in Touch