Polymer Dispersions Market Report Scope & Overview:

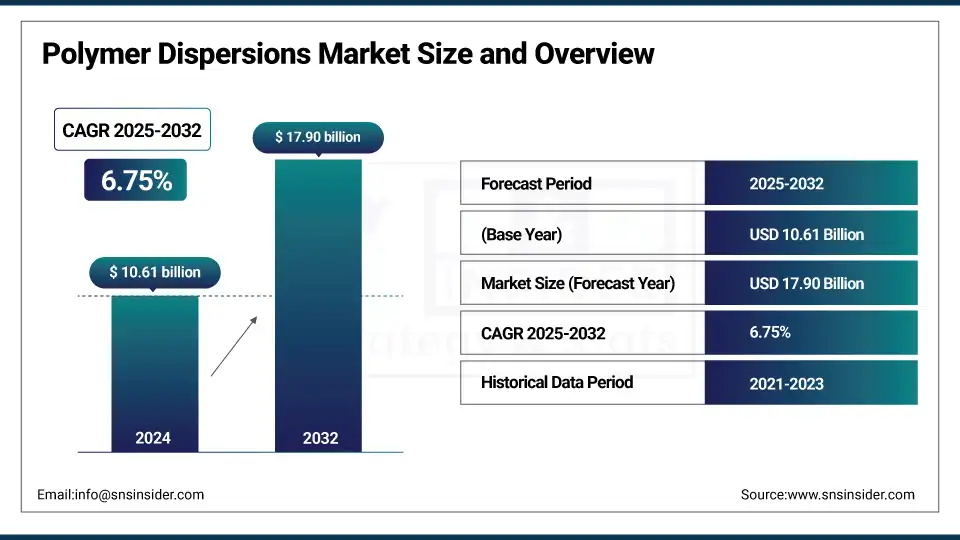

The polymer dispersions market size was valued at USD 10.61 billion in 2024 and is expected to reach USD 17.90 billion by 2032 and grow at a CAGR of 6.75% over the forecast period 2025-2032.

Polymer dispersions market analysis indicates that the increasing usage in the nonwovens industry is a major factor, which is expected to drive the market growth. Nonwoven materials are widely used in hygiene, medical, filtration, and geotextile applications, necessitating coatings and binders to improve performance. Polymer dispersions provide good adhesion, flexibility, and durability, which are great for improving the performance properties of nonwoven fabrics. The demand for disposable hygiene products like diapers, sanitary and incontinence pads is growing, especially in developing countries, where focus has increased towards healthcare and sanitation and has led to more polymer dispersions in nonwovens. And this growth potential is likely to persist shortly, which is a major factor driving the global polymer dispersions market growth.

In April 2022, Engineered Polymer Solutions (EPS), a U.S.-based specialist in engineered elastomeric and polymeric coatings, introduced EPS 2436, a self-crosslinking acrylic dispersion tailored for premium wood coatings, including cabinetry, furniture, and flooring.

Market Size and Forecast:

-

Market Size in 2024: USD 10.61 Billion

-

Market Size by 2032: USD 17.90 Billion

-

CAGR: 6.75% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Polymer Dispersions Market - Request Free Sample Report

Polymer Dispersions Market Trends:

-

Increasing demand from the paints and coatings industry is driving the adoption of water-based polymer dispersions due to their low VOC content and environmental compliance.

-

Growing construction and infrastructure activities worldwide are boosting the use of polymer dispersions in architectural coatings and adhesives.

-

Rising application in packaging, textiles, and paper industries is expanding market opportunities across diverse end-use sectors.

-

Stringent environmental regulations encouraging eco-friendly and sustainable formulations are accelerating the shift from solvent-based systems to water-based dispersions.

-

Technological advancements in acrylic, vinyl, polyurethane, and styrene-butadiene dispersions are enhancing performance characteristics such as durability, flexibility, and chemical resistance.

-

Expansion of automotive and industrial manufacturing sectors is increasing demand for high-performance coatings and specialty adhesive solutions.

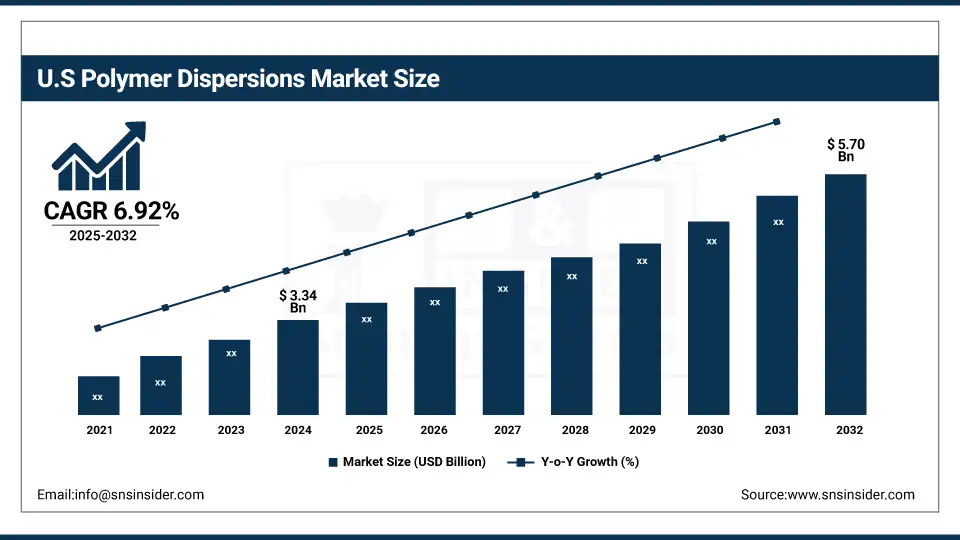

The U.S. Polymer Dispersions market size was USD 3.34 billion in 2024 and is expected to reach USD 5.70 billion by 2032 and grow at a CAGR of 6.92% over the forecast period of 2025-2032. It is due to the advanced formulation needs and strong sustainability mandates. U.S.-based dispersion manufacturers enjoy tight integration with automotive giants and coating formulators, as well as significant access to R&D talent. Domestic capacity expansions and green chemistry trends continue to strengthen the supply chain.

Polymer Dispersions Market Dynamics:

Key Drivers:

-

Rise of Water‑Based & Low‑VOC Solutions Drive the Market Growth

Stringent environmental laws (such as the U.S. Clean Air Act and the EPA) are forcing industries to move away from solvent-based formulations to water-based polymer dispersions. These provide reduced VOC emissions, increased safety during handling, and lower risk of fire, helping to ease regulatory and corporate sustainability requirements. They have been widely embraced across the paint, coatings, adhesives, and sealants marketplace, and are backed by ongoing research and development (R&D) efforts to further optimize performance and maintain their environmentally friendly profile. This regulatory stress is an ongoing growth driver for manufacturers and formulators.

For instance, in 2022, Cabot Corporation announced an investment of USD 50 million to develop a new production line in Haverhill, Massachusetts for color aqueous pigment dispersions, which would allow for low-VOC ink production in line with growing demand.

Restrain:

-

Fluctuating Raw Material Prices May Hamper the Market Growth

Petrochemical-based products, which include butadiene, styrene, acrylates, and vinyl acetate, are widely used in polymer dispersions. Fluctuations of raw material prices, typically influenced by changes in crude oil and supply chain interruptions, have a material impact on production costs and the level of margin to be achieved. As most dispersion formulations are driven by price, many stability issues such as these are difficult to budget for and cripple the ability to roll out to scale. Further, it’s hard for manufacturers to hand off price increases to cost-conscious end-users, which is cramping overall expansion.

Opportunities:

-

Bio‑Based & Functional Coatings Offer Untapped Market Potential for Polymer Dispersions Materials.

Sustainability goals and consumer demand are fueling new products like bio-based and specialty polymer dispersions, including antimicrobial, anti-corrosion, and self-cleaning coatings. These formulations have a carbon benefit and are in line with legislative expectations as they are made from renewables. Sophisticated dispersion technology is also facilitating to tailoring of coatings for technical textiles, packaging, and digital printing, creating new market niches and added value opportunities which drive the polymer dispersions market trends.

In July 2022, BASF announced the start-up of a new acrylics dispersion line at its Dahej site, which will produce ‘acrylics dispersion for the construction industry, as well as the coatings and adhesives markets throughout South Asia’, the company said in a release – a commitment to sustainable and high-performance product capacity futureproofing.

Polymer Dispersions Market Segment Analysis:

By Type

Acrylic dispersions hold the largest polymer dispersions market share of the market, around 32% in 2024, owing to their excellent weatherability, durability, and cost-effectiveness. These acrylic polymer dispersions are extensively used in architectural and industrial coatings due to their strong film-forming ability and environmental compatibility. Their dominance is reinforced by the growing demand for water-based and low-VOC coating systems across developed regions.

Polyurethane dispersions are expected to witness the fastest growth during the forecast period. Their superior flexibility, chemical resistance, waterborne polymer dispersions, and adhesion properties make them ideal for high-performance applications in automotive interiors, leather finishing, and furniture coatings. The rising shift toward sustainable and solvent-free technologies further supports their accelerated adoption.

By Technology

Water-based dispersions are the most widely used technology, primarily due to increasing environmental regulations targeting VOC emissions. These systems offer safety, easy cleanup, and reduced toxicity, making them a preferred choice in coatings, adhesives, and textiles. Their high adoption across North America and Europe strengthens their leadership in the market.

UV-cured dispersions are anticipated to grow at a robust pace owing to their energy efficiency, rapid curing time, and enhanced performance attributes. Their expanding usage in electronics, automotive, and packaging sectors is driven by the demand for high-gloss finishes and scratch-resistant surfaces. Ongoing innovations in UV-curable resin systems are further propelling their market penetration.

By Application

The paints and coatings segment accounts for the largest application share, around 38% in 2024 driven by strong demand in the construction and automotive industries. Polymer dispersions enhance coating properties such as durability, adhesion, and environmental compliance. Increasing infrastructure development and renovation projects globally continue to boost this segment’s growth.

Adhesives and sealants are projected to be the fastest-growing application area due to the rising use of waterborne dispersion adhesives in packaging, electronics, and construction. These products are gaining popularity for their eco-friendliness and high bonding strength. The surge in e-commerce and green building practices is fueling additional demand for low-emission adhesives.

By End-Use Industry

The construction industry dominates the market, holding around 32% market share and it’s supported by robust demand for dispersion-based paints, sealants, and concrete additives. Increasing urbanization, particularly in emerging economies, and stricter environmental norms around building materials are key contributors to the segment's dominance. Government infrastructure initiatives further augment its growth.

The automotive industry is emerging as the fastest-growing end-use segment, driven by rising production and demand for lightweight, durable, and aesthetic components. Polymer dispersions are increasingly used in automotive coatings, interiors, and adhesives due to their superior performance and regulatory compliance. Rapid industrialization in Asia-Pacific is a major growth driver for this segment.

Polymer Dispersions Market Regional Analysis:

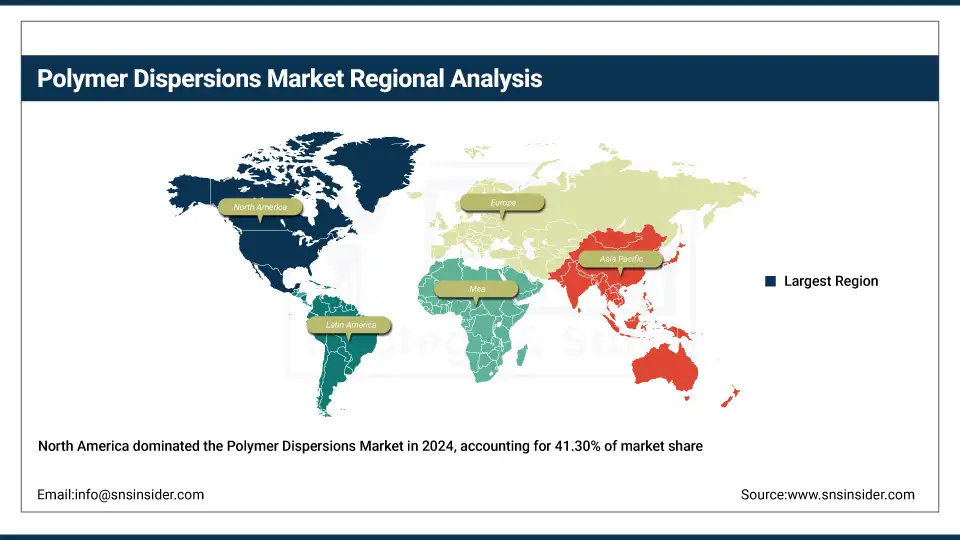

North America dominated the polymer dispersions market in 2024 with the largest revenue share of approximately 41.30%, This is due to an established regulatory environment, well-developed industry, and the need for high-performance, low-VOC products in the region. Since most significant formulators of industrial aqueous coatings, adhesives, and automotive adhesives have long adopted or will adopt waterborne and particular dispersions that are accustomed to qualify for the rigorous US and Canadian environmental requirements. North American producers also have the advantage of access to petrochemical feedstocks and world-class R&D canters.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific region is expected to grow at the fastest CAGR of about 7.82% from 2025 to 2032. It is due to the rapid urbanization, industrial expansion, and infrastructural growth that underpin its rising polymer dispersions demand. Countries like China, India, and Southeast Asian nations are scaling up construction, packaging, and consumer-goods sectors that rely heavily on dispersions. Local investments in manufacturing capacity and innovation hubs also support the area’s growth trajectory.

BASF inaugurated a second polymer dispersions line at its Daya Bay (Guangdong, China) plant, set to start in early 2024, targeting architectural coatings and emerging battery binder segments.

Europe commands a strong position in polymer dispersions driven by early VOC regulations, sustainability mandates like EU Ecolabel, and substantial coating and construction industries in Germany, France, and the Nordics. European players have therefore led technology adoption, especially in specialty dispersions for durable, low-emission applications. While expansion is moderate compared to APAC, the focus remains on high-quality, eco-friendly products and circular economy integration.

Wacker Chemie expanded its global footprint by opening its new U.S. headquarters in Ann Arbor but continued investing in European operations in Bavaria, maintaining innovation across adhesives and dispersion technologies.

Polymer Dispersions Market Key Players:

The Polymer Dispersions Companies are BASF SE, Dow Chemical Company, Arkema S.A., Covestro AG, Wacker Chemie AG, Synthomer plc, Celanese Corporation, DIC Corporation, Trinseo, Alberdingk Boley GmbH, Michelman, Inc., Hexion Inc., Ashland Global Holdings Inc., Chase Corporation, Lubrizol Corporation, Scott Bader Company Ltd., Mallard Creek Polymers, OMNOVA Solutions Inc., Organik Kimya, Mitsui Chemicals, Inc.

Recent Development in the Polymer Dispersions Market:

-

In February 2024, Dow Chemical expanded its portfolio of polymer dispersions with the launch of a new series of eco-friendly and water-based products designed for adhesives and coatings, highlighting the broader move towards “green”, low-VOC alternatives.

-

In December 2023, BASF released a class of new polymer dispersions for textiles and construction, concentrating on durability and environmental performance.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 10.61 Billion |

| Market Size by 2032 | USD 17.90 Billion |

| CAGR | CAGR of6.75% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Acrylic Dispersions, Polyurethane Dispersions (PUDs), Vinyl Dispersions, Styrene-Butadiene Dispersions, Others (e.g., epoxy dispersions, silicone dispersions) • By Technology (Water-Based Dispersions, Solvent-Based Dispersions, UV-Cured Dispersions, Others (e.g., powder dispersions, high-solid system) • By Application (Paints & Coatings, Adhesives & Sealants, Nonwovens, Printing Inks, Others (e.g., textiles, construction additives)) • By End-Use Industry (Automotive, Construction, Packaging, Textile, Others (e.g., electronics, healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | BASF SE, Dow Chemical Company, Arkema S.A., Covestro AG, Wacker Chemie AG, Synthomer plc, Celanese Corporation, DIC Corporation, Trinseo, Alberdingk Boley GmbH, Michelman, Inc., Hexion Inc., Ashland Global Holdings Inc., Chase Corporation, Lubrizol Corporation, Scott Bader Company Ltd., Mallard Creek Polymers, OMNOVA Solutions Inc., Organik Kimya, Mitsui Chemicals, Inc. |

Frequently Asked Questions

Ans The global push for low-VOC and water-based technologies significantly accelerates polymer dispersion demand. Regulatory compliance (e.g., EPA, REACH), green building certifications, and corporate sustainability goals are driving the replacement of solvent-based systems.

Ans North America currently holds a significant share due to regulatory frameworks supporting water-based systems and strong industrial infrastructure. However, Asia Pacific is the largest and fastest-growing consumer region, driven by rapid urbanization, infrastructure development, and expanding manufacturing sectors in China, India, and Southeast Asia.

Ans The market is highly competitive and fragmented, with both global giants and regional manufacturers active. Key players include BASF SE, Arkema, DIC Corporation, Wacker Chemie AG, Synthomer plc, and Covestro AG. These companies compete based on innovation, sustainability, product performance, and regional expansion strategies.

Ans The key demand drivers include paints and coatings, adhesives and sealants, printing inks, and nonwoven textiles. The paints and coatings segment leads due to growing construction, automotive, and industrial maintenance needs.

Ans. Acrylic dispersions dominate the market due to their excellent film-forming ability, UV resistance, and cost-effectiveness. They are widely used in paints, coatings, and adhesives for both industrial and decorative applications.

Get in Touch