Ammonium Sulfate Market Report Scope & Overview:

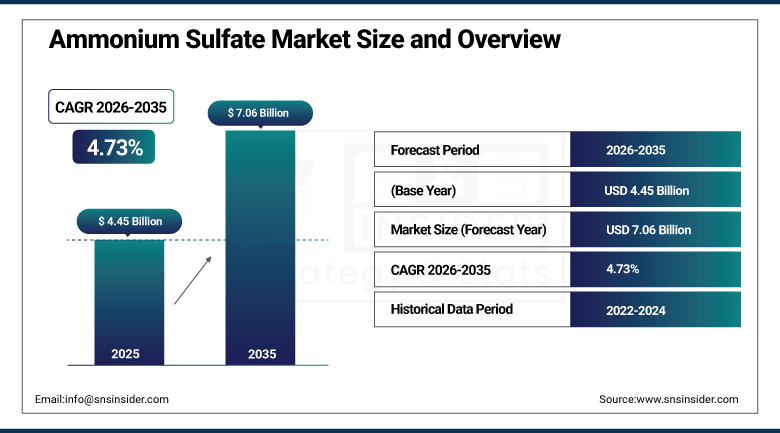

The Ammonium Sulfate Market was valued at USD 4.45 Billion in 2025 and is expected to reach USD 7.06 Billion by 2035, growing at a CAGR of 4.73% from 2026–2035.

The global ammonium sulfate market is growing at a steady pace. Ammonium sulfate ((NH₄)₂SO₄) is an inorganic salt produced as a byproduct of caprolactam manufacturing, synthetic ammonia-sulfuric acid neutralization, and coke oven recovery. The market is driven by widespread use in fertilizers, water treatment, and industrial applications, with REACH and EPA regulatory frameworks creating compliance investment that shapes production economics and trade flows. The report explores cost structure analyzing raw material, energy, and labor expenses shaping production economics, strategic investment and ROI, and consumer perception and buying behavior revealing shifting demand in agriculture and industry.

In 2025, AdvanSix completed the expansion of its ammonium sulfate granulation capacity at its Hopewell, Virginia integrated nylon intermediates facility, adding annual ammonium sulfate granule production whose premium granular specification commands above-standard pricing in the specialty fertilizer market. The expansion capitalizes on AdvanSix’s integrated caprolactam production creates commercially advantaged production economics relative to synthetic route producers.

Market Size and Forecast:

-

Market Size in 2026E: USD 4.66 Billion

-

Market Size by 2035: USD 7.06 Billion

-

CAGR: 4.73% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Ammonium Sulfate Market- Request Free Sample Report

Ammonium Sulfate Market Trends:

-

Granular ammonium sulfate demand is rising due to better handling, precision farming compatibility, and improved agronomic performance.

-

Coated and enhanced efficiency formulations improve nutrient release control, increasing fertilizer efficiency and reducing environmental nutrient losses.

-

Asia-Pacific caprolactam expansion is increasing byproduct ammonium sulfate supply, creating cost pressure on synthetic production routes globally.

-

Water treatment applications are growing as ammonium sulfate supports biological treatment processes and improves drinking water coagulation efficiency.

-

Soil sulfur deficiency correction in Europe and North America is increasing ammonium sulfate usage as a combined nitrogen and sulfur fertilizer source.

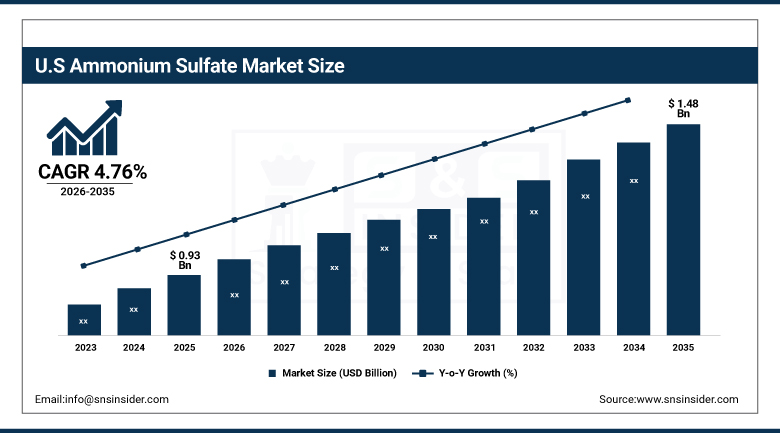

U.S. Ammonium Sulfate Market Outlook:

The U.S. Ammonium Sulfate Market was valued at approximately USD 0.93 Billion in 2025 and is expected to reach approximately USD 1.48 Billion by 2035, growing at a CAGR of approximately 4.76%.

The U.S. is the most commercially significant ammonium sulfate market within the fastest-growing North American region. AdvanSix, Honeywell’s integrated nylon operations, and imported supply from BASF, OCI, and Asian producers collectively serve the domestic market. The U.S. Corn Belt’s progressive soil sulfur depletion from Clean Air Act SO₂ emission controls creates growing corn and soybean ammonium sulfate procurement whose dual nitrogen and sulfur supply creates agronomic ROI. Industrial procurement from water utilities, chemical manufacturers, and textile processors creates consistent non-agricultural demand that diversifies the U.S. market’s seasonal agricultural procurement concentration.

Nutrien Ltd. expanded its ammonium sulfate product offering in 2024 with a new controlled-release ammonium sulfate granule line for the U.S. precision agriculture market, providing nitrogen and sulfur in a single slow-release granule. The product launch reflects the commercial opportunity in the premium U.S. fertilizer market whose precision agriculture adoption creates willingness to pay for enhanced efficiency products that conventional crystalline ammonium sulfate alternatives cannot provide equivalently.

Ammonium Sulfate Market Segment Analysis:

-

By Production Process, the caprolactam byproduct process segment dominated the ammonium sulfate market with 62% share in 2025, while the synthetic/saturation process segment is the fastest growing.

-

By Form, the solid/granular/crystalline segment dominated the ammonium sulfate market in 2025, while the liquid/solution segment is the fastest growing.

-

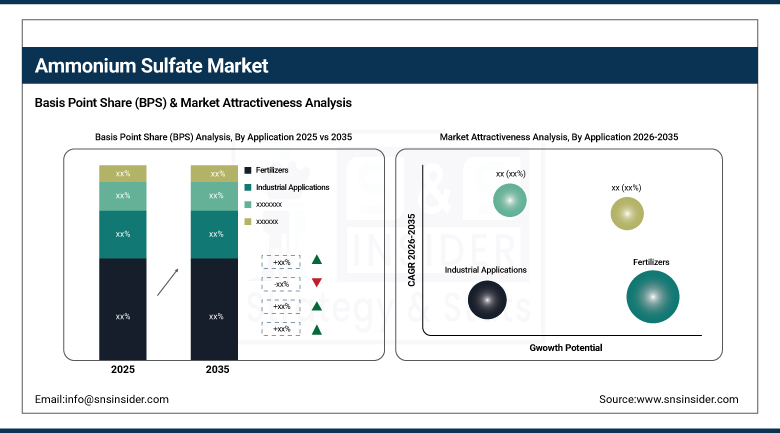

By Application, the fertilizers segment dominated the ammonium sulfate market with 75.4% share in 2025, while the industrial applications segment is the fastest growing.

-

By End Use, the agriculture/crop nutrition segment dominated the ammonium sulfate market with approximately 72% share in 2025, while the water treatment segment is the fastest growing.

By Production Process, caprolactam byproduct dominates, synthetic grows fastest

Caprolactam byproduct process retained the dominant production position with 62% of the ammonium sulfate market in 2025. The caprolactam process’s commercial primacy reflects the unavoidable byproduct generation economics whose ammonium sulfate co-production creates commercially advantaged production cost relative to dedicated synthetic production routes. Each ton of caprolactam produced for nylon-6 manufacturing generates approximately 4.4 tons of ammonium sulfate whose recovery is economically rational regardless of ammonium sulfate market price, creating a structural supply base whose cost advantage sustains commercial competitiveness.

Synthetic ammonium sulfate production is the fastest-growing process because Asia Pacific’s extraordinary caprolactam capacity expansion is creating above-average byproduct supply in the region while demand in North America and Europe creates market opportunity for purpose-built granular production facilities whose premium product specification creates commercial differentiation from commodity crystalline byproduct alternatives. Each new dedicated ammonium sulfate granulation facility that creates premium granular specification creates per-ton commercial value improvement that sustains investment in synthetic production capacity despite the cost disadvantage relative to byproduct alternatives.

By Application, fertilizers dominate, industrial applications grow fastest

Fertilizers retained the dominant application position with 75.4% of the ammonium sulfate market in 2025. Fertilizer’s commercial primacy reflects ammonium sulfate’s unique agronomic value proposition whose simultaneous supply of 21% nitrogen and 24% sulfur in a single fertilizer product creates dual macronutrient application efficiency that single-nutrient alternatives cannot match without separate sulfur supplementation. Each farmer whose soil sulfur deficiency requires supplementation alongside nitrogen creates ammonium sulfate specification motivation whose combined nutrient delivery efficiency creates per-ton commercial value above equivalent nitrogen content from urea.

Industrial applications are the fastest-growing application because water treatment’s biological nitrogen source, chemical manufacturing’s reaction medium and pH buffering agent, food processing’s yeast nutrient and dough conditioner, and textile dyeing’s mordanting agent collectively create diversified non-agricultural procurement growth that compounds with industrial sector development. Each new wastewater treatment facility that adopts biological nitrogen removal creates ammonium sulfate procurement whose volume scales with the facility’s treatment capacity.

By Form, solid dominates, liquid grows fastest

Solid ammonium sulfate retained the dominant form position in the market in 2025. The solid form’s commercial leadership reflects its compatibility with the global agricultural distribution infrastructure’s bulk storage, transportation, and mechanical application equipment that field crop production requires. Granular and crystalline ammonium sulfate’s ability to blend with other solid granular nutrients including urea, DAP, and MOP in custom blend fertilizer programmes creates distribution efficiency whose commercial scale sustains solid form’s dominant market position.

Liquid ammonium sulfate solution is the fastest-growing form because fertigation’s precision root-zone delivery, liquid fertilizer programme’s tank-mix compatibility, and the water-soluble specification’s complete dissolution without solid residue create growing adoption in irrigated crop production and specialty agriculture. Each drip irrigation system that incorporates ammonium sulfate solution in its fertigation programme creates liquid procurement whose volume scales with irrigated area. The industrial application’s preference for liquid ammonium sulfate in water treatment and process chemistry creates consistent non-agricultural liquid demand that sustains the form segment’s above-average growth.

By End Use, agriculture dominates, water treatment grows fastest

Agriculture and crop nutrition retained the dominant end-use position with approximately 72% of the ammonium sulfate market in 2025. The agricultural sector’s structural procurement reflects ammonium sulfate’s agronomic advantages including acidifying effect on high-pH soils, sulfur supplementation in deficient soils, and nitrogen efficiency in flooded rice production. Each rice paddy that applies ammonium sulfate as the preferred nitrogen source over urea in waterlogged conditions creates agricultural procurement whose aggregate across Asia’s extraordinary rice cultivation area creates commercial scale.

Water treatment is the fastest-growing end use because the global expansion of biological nitrogen removal in wastewater treatment facilities and the growing adoption of sophisticated drinking water treatment processes create structured industrial procurement growth. Each wastewater treatment plant that operates biological nutrient removal creates ammonium sulfate procurement as the nitrogen source for denitrifying bacteria whose biological activity sustains the treatment process.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Ammonium Sulfate Market Insights

North America is the fastest-growing regional ammonium sulfate market, driven by soil sulfur depletion creating growing nitrogen-sulfur combination fertilizer demand, the precision agriculture sector’s premium granular specification adoption, and industrial procurement growth. The United States accounts for approximately 87.4% of North American revenues through AdvanSix’s domestic production, the agricultural sector’s growing sulfur deficiency awareness, and the industrial sector’s water treatment and food processing procurement.

Canada contributes approximately 12.6% of North American revenues through its canola and wheat production’s above-average sulfur requirement creating structured ammonium sulfate procurement, and the industrial sector’s water treatment and chemical manufacturing demand.

Europe Ammonium Sulfate Market Insights

Europe is a technically sophisticated ammonium sulfate market where BASF’s and DOMO Chemicals’ integrated caprolactam production creates domestic supply, EU REACH compliance shapes product specifications, and the agricultural sector’s progressive sulfur deficiency from EU emission controls creates growing fertilizer demand. Germany accounts for approximately 22.3% of European revenues through BASF’s Ludwigshafen operations, the agricultural sector’s precision fertilizer adoption, and the chemical industry’s industrial procurement.

France, Poland, and the Netherlands are significant secondary markets where agricultural demand, industrial water treatment procurement, and food processing create consistent ammonium sulfate consumption that compounds with the progressive EU soil health agenda’s sulfur awareness.

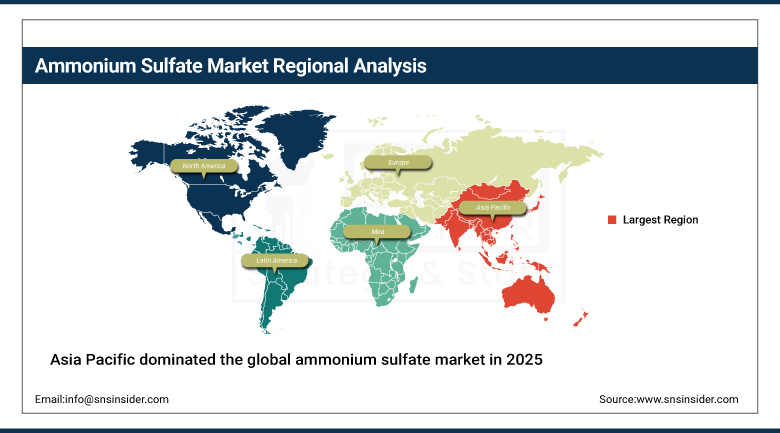

Asia Pacific Ammonium Sulfate Market Insights

Asia Pacific dominated the global ammonium sulfate market in 2025 with 42.7% of global revenues. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world’s largest ammonium sulfate producer and consumer, whose integrated caprolactam and dedicated production capacity creates the most commercially significant supply and demand concentration globally. India’s rice and oilseed production creates above-average ammonium sulfate fertilizer demand, and the rapidly growing industrial sector creates consistent non-agricultural procurement.

Japan’s Sumitomo Chemical’s caprolactam operations and South Korea’s chemical industry create significant secondary markets whose ammonium sulfate production creates both domestic consumption and export procurement. Southeast Asia’s rice cultivation creates consistent ammonium sulfate fertilizer demand that compounds with agricultural intensification investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Ammonium Sulfate Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through SABIC’s chemical manufacturing, the agricultural sector’s irrigation-based crop production ammonium sulfate application, and the industrial sector’s water treatment procurement. Brazil leads Latin American revenues at approximately 44.2% through its soybean and sugarcane production’s fertilizer demand, the industrial sector’s growing procurement, and the agricultural sector’s structured soil nutrition programme investment.

Argentina’s soybean production creates significant secondary Latin American ammonium sulfate demand, and UAE’s agricultural and industrial sectors create consistent MEA secondary market procurement.

Market Dynamics:

Growth Drivers: Agricultural nitrogen-sulfur deficiency correction and industrial water treatment expansion

Agricultural soil sulfur depletion from SO₂ emission controls is the ammonium sulfate market’s most structurally certain growth driver in developed markets. The International Fertilizer Association’s documentation that 73% of European and North American soils are sulfur-deficient creates procurement motivation that compounds with each successive year of below-atmospheric-input conditions. Ammonium sulfate’s commercial advantage as a combined nitrogen-sulfur source whose single application corrects both deficiencies creates above-average specification preference over separate urea plus sulfur application in sulfur-deficient farming systems. The global oilseed area’s expansion, whose canola and rapeseed’s above-average sulfur requirement creates per-hectare demand growth, creates procurement that compounds with area expansion.

Industrial water treatment expansion globally is creating the most commercially diversifying ammonium sulfate demand growth vector. Each new biological wastewater treatment facility commissioned, each drinking water plant upgrading to nitrification-denitrification biological treatment, and each industrial process water system adopting nitrogen removal creates ammonium sulfate procurement whose aggregate across global water infrastructure investment creates commercial scale. The progressive tightening of effluent discharge standards whose nitrogen removal requirement creates biological treatment infrastructure investment sustains above-average water treatment procurement growth.

Restraints: Competition from urea and other nitrogen fertilizers and caprolactam byproduct supply dependence creating price volatility

Urea’s dominant nitrogen fertilizer position at above-45% nitrogen content per ton creates cost-per-nitrogen-unit competitive advantage over ammonium sulfate’s 21% nitrogen whose per-ton cost economics create substitution competition in nitrogen-only deficient soils. Each farmer whose soil sulfur adequacy eliminates the dual-nutrient specification motivation creates urea preference over ammonium sulfate whose premium per-unit-nitrogen cost requires sulfur value justification.

Caprolactam production cycle’s commercial volatility creates ammonium sulfate supply fluctuation whose byproduct volume variation creates price instability in caprolactam-supplied markets. Each caprolactam demand reduction from nylon-6 industry slowdown creates ammonium sulfate supply reduction that creates price increase, while caprolactam capacity expansion creates supply surplus that creates price depression whose aggregate creates commercial uncertainty for agricultural procurement planning.

Opportunities: Premium granular ammonium sulfate market development and emerging market first-time agricultural adoption

Premium granular ammonium sulfate represents the most commercially value-accretive market development direction whose handling efficiency, precision application compatibility, and controlled release formulation potential create per-ton commercial value substantially above commodity crystalline alternatives. Each precision agriculture programme that adopts variable rate granular ammonium sulfate application creates premium procurement whose commercial scale grows with precision agriculture adoption.

Emerging market first-time agricultural adoption in Africa, Southeast Asia, and South Asia represents the most commercially scalable volume growth opportunity whose food security investment creates structured fertilizer procurement growth. Each new smallholder farming programme that introduces ammonium sulfate as the recommended nitrogen-sulfur fertilizer creates adoption that compounds with programme expansion and farmer knowledge transfer.

Recent Developments:

-

2025: AdvanSix completed the expansion of its ammonium sulfate granulation capacity at its Hopewell, Virginia facility, adding premium granular production whose integrated caprolactam byproduct production economics create commercially advantaged cost structure for specialty fertilizer market development.

-

2025: Fibrant B.V. and UBE Corporation continued caprolactam capacity expansion in Asia and Europe during 2025–2026 is increasing ammonium sulfate byproduct availability.

-

2025: Nutrien Ltd. and Yara International ASA expanded nitrogen-sulfur fertilizer portfolios, increasing ammonium sulfate integration in blended fertilizer systems.

Ammonium Sulfate Market key players are:

-

BASF SE

-

Nutrien Ltd.

-

OCI Global

-

Sinopec Corporation

-

Sumitomo Chemical Co., Ltd.

-

Gujarat State Fertilizers & Chemicals Ltd. (GSFC)

-

AdvanSix Inc.

-

DOMO Chemicals

-

Evonik Industries AG

-

Lanxess AG

-

Arkema S.A.

-

Fibrant B.V. (DSM-Firmenich)

-

Honeywell International Inc.

-

CF Industries Holdings, Inc.

-

UBE Corporation

-

Nippon Shokubai Co., Ltd.

-

EuroChem Group

-

OCI Nitrogen B.V.

-

Yara International ASA

-

Fertiberia S.A.

Ammonium Sulfate Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.45 Billion |

| Market Size by 2035 | USD 7.06 Billion |

| CAGR | CAGR of 4.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Production Process (Caprolactam Byproduct Process, Synthetic/Saturation Process, Coke Oven Byproduct Process, Others) • By Form (Solid/Granular/Crystalline, Liquid/Solution) • By Application (Fertilizers, Industrial Applications, Pharmaceuticals, Food & Beverage, Water Treatment, Textile Dyeing, Others) • By End Use (Agriculture/Crop Nutrition, Water Treatment, Food Processing, Chemical Industry, Textile Industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Nutrien Ltd., OCI Global, Sinopec Corporation, Sumitomo Chemical Co., Ltd., Gujarat State Fertilizers & Chemicals Ltd. (GSFC), AdvanSix Inc., DOMO Chemicals, Evonik Industries AG, Lanxess AG, Arkema S.A., Fibrant B.V. (DSM-Firmenich), Honeywell International Inc., CF Industries Holdings, Inc., UBE Corporation, Nippon Shokubai Co., Ltd., EuroChem Group, OCI Nitrogen B.V., Yara International ASA, Fertiberia S.A. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 4.73% from 2026 to 2035.

The market was valued at USD 4.45 Billion in 2025.

Widespread use in fertilizers driven by global agricultural demand for combined nitrogen and sulfur nutrition correcting soil deficiencies, and growing industrial applications in water treatment and food processing creating diversified non-agricultural procurement growth.

The caprolactam byproduct process dominated the ammonium sulfate market with 62% share in 2025.

Fertilizers dominated the Ammonium Sulfate Market with 75.4% share in 2025.

Get in Touch