Hexamethylenediamine Market Report Scope & Overview:

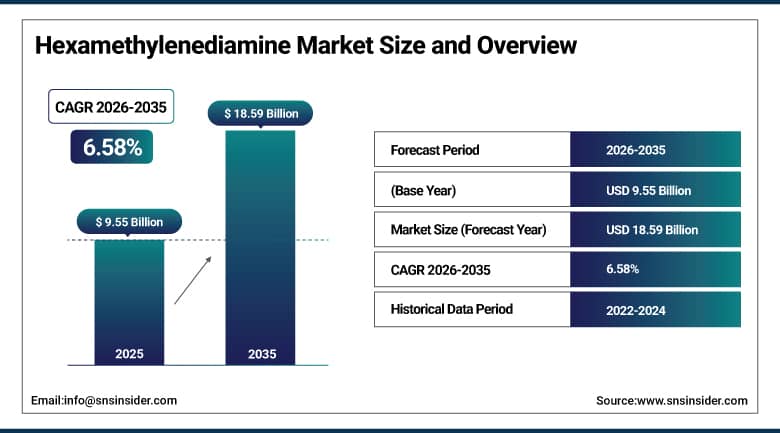

The Hexamethylenediamine Market was valued at USD 9.55 Billion in 2025 and is expected to reach USD 18.59 Billion by 2035, growing at a CAGR of 6.58% from 2026 to 2035.

Hexamethylenediamine, referred to alternatively as HMDA or 1,6-diaminohexane, is a diamine organic compound possessing the chemical formula C6H16N2. The two amino functional groups at the terminal ends and six-carbon atom backbone chain structure render hexamethylenediamine a critical component in the synthesis of nylon 6,6 polyamide through polycondensation reactions in combination with adipic acid. As such, hexamethylenediamine forms an integral part in the global nylon and engineering plastics production value chain, where its downstream products find diverse applications in automobiles, textile fibers, coatings, adhesives, and chemicals formulations; the total demand from all these downstream applications provides the underlying structure for hexamethylenediamine market growth. Besides being a key material in the synthesis of nylon 6,6, hexamethylenediamine also acts as a curing agent for epoxies and corrosion inhibitors in lubricants and water treatment formulations.

In March 2022, Asahi Kasei signed a strategic agreement with Genomatica, Inc. to produce bio-based hexamethylenediamine from renewable biomass feedstocks instead of traditional petroleum-based adiponitrile precursors to meet the rising need for sustainable nylon 6,6 production with lower carbon footprint that meets the ever more rigorous sustainability procurement requirements of automotive and textiles producers. This was evident from the technology development by the strategic partnership for bio-HMDA production, which highlighted the rising significance of renewable feedstock chemistry in the larger nylon value chain whose commercialization would enable the automotive and textile producers to have a sustainable alternative to traditional nylon 6,6 without compromising on its performance properties.

Market Size and Forecast

-

Market Size in 2026E: USD 10.18 Billion

-

Market Size by 2035: USD 18.59 Billion

-

CAGR: 6.58% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Hexamethylenediamine Market - Request Free Sample Report

Hexamethylenediamine Market Trends

-

Bio-based hexamethylenediamine (HMDA) is gaining traction as manufacturers pursue sustainable nylon 6,6 production using renewable feedstocks.

-

Electric vehicle production growth is driving demand for HMDA-based nylon 6,6 in lightweight, heat-resistant, and electrically insulating automotive components.

-

Vertical integration strategies are increasing among HMDA manufacturers to strengthen feedstock security and reduce raw material price volatility.

-

HMDA adoption in specialty coatings and adhesives is expanding due to its superior crosslinking performance, durability, and chemical resistance.

-

Production capacity expansion across Asia Pacific is accelerating as China and India increase domestic HMDA manufacturing to support growing automotive and textile industries.

The U.S. Hexamethylenediamine Market Outlook

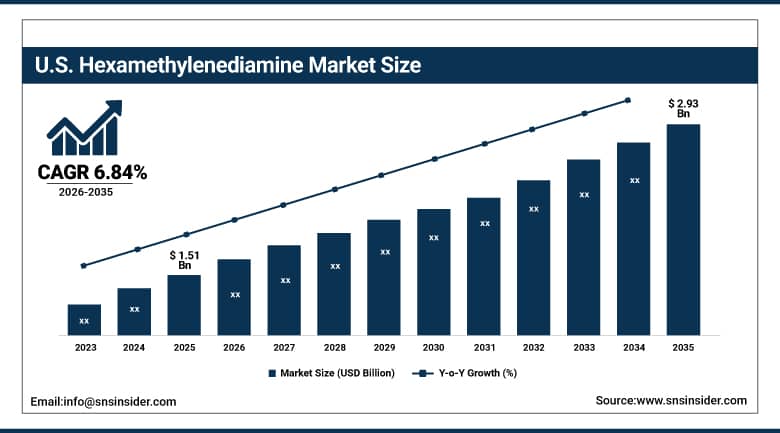

The U.S. Hexamethylenediamine Market was valued at approximately USD 1.51 Billion in 2025 and is expected to reach approximately USD 2.93 Billion by 2035, growing at a CAGR of approximately 6.84%.

The United States HMDA industry enjoys the benefit of its existing network of nylon 6,6 production systems, developed industrial infrastructure and significant demand from end user industries like automotive, textile and coating industries. This is possible due to the existence of ample availability of raw materials such as adiponitrile and butadiene with the help of advanced petrochemical and refining infrastructure available in the United States. Presence of large-scale HMDA producers such as INVISTA and Ascend Performance Materials, who also have large scale nylon 6,6 production plants in the country, makes this country compete effectively in the global HMDA market. This is because of their continuous innovations, large scale production efficiencies and supply chain integration.

In 2025, Ascend Performance Materials Company announced the capacity expansion for their intermediates that included hexamethylenediamine for nylon 6,6 plastics in order to fulfill the rising demands in the automotive and industrial sectors. This decision was based on their faith in the future increase in the demand of HMDA due to the increased tendency towards lightweighting in the automotive sector and the displacement of metal and low performance plastic components in various sectors where nylon 6,6 is used.

Hexamethylenediamine Market Segment Analysis

-

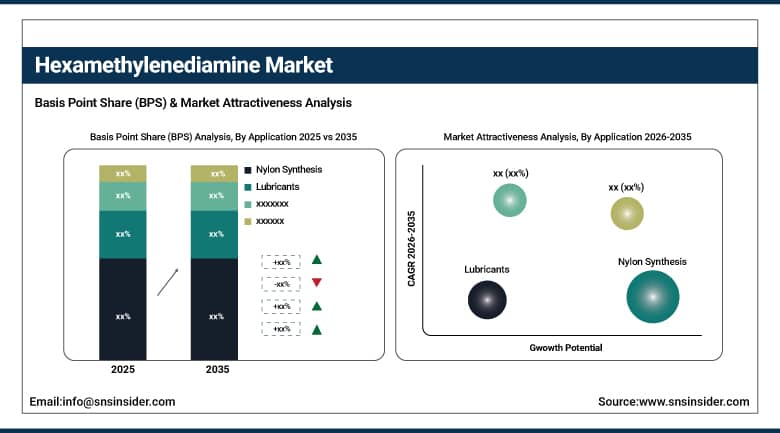

By Application, nylon synthesis dominated the hexamethylenediamine market with a 42% market share in 2025, while the lubricants segment is anticipated to grow at a significant CAGR over the forecast period.

-

By End Use Industry, automotive dominated the hexamethylenediamine market with a 32% market share in 2025, while the textile segment is expected to grow at a significant CAGR over the forecast period.

By Application, nylon synthesis dominates, lubricants and coatings grow fastest

Nylon synthesis dominated the hexamethylenediamine market with a 42% market share in 2025, attributable to HMDA's essential role in producing Nylon 6,6, a polyamide heavily utilized across automotive, electronics, and textiles for its exceptional strength, heat resistance, and durability characteristics that few alternative engineering materials can match at comparable cost points. The growing demand for lightweight, high-performance materials in vehicles and industrial components is a major driver sustaining nylon synthesis's commercial dominance, with companies including INVISTA and Ascend Performance Materials having ramped up nylon production capacity to meet global demand growth across both established and emerging automotive markets. Sustainable alternatives such as bio-based nylon continue to rely on hexamethylenediamine as their fundamental chemical building block.

Lubricants represent a growing application segment as HMDA serves important functions as a corrosion inhibitor and synthetic lubricant additive component whose protective film formation on metal surfaces reduces friction and wear between moving mechanical parts while extending lubricant service life through oxidative degradation prevention. The expanding global automotive fleet and industrial equipment base, whose maintenance lubricant consumption grows proportionally with vehicle and machinery population, sustains structural demand growth for HMDA-based lubricant additives whose corrosion protection performance is particularly valued in demanding industrial and automotive applications. Coatings and adhesives applications, where HMDA serves as a crosslinking agent and chemical intermediate, are similarly growing as construction and industrial coating formulators seek high-performance curing agents whose chemical resistance properties support premium protective and decorative coating system specifications.

By End Use Industry, automotive dominates, textile grows fastest

Automotive dominated the hexamethylenediamine market with a 32% market share in 2025, driven by the growing adoption of lightweight nylon parts whose HMDA-based materials are used for components including radiator tanks and air intake manifolds that are progressively replacing heavier traditional metal alternatives as automotive manufacturers pursue vehicle weight reduction for fuel efficiency and emissions compliance objectives. Nylon 6,6's exceptional combination of mechanical strength, thermal stability up to operating temperatures that exceed 150 degrees Celsius, and chemical resistance to automotive fluids makes it the preferred engineering plastic for under-hood components whose performance environment would degrade lower-performance alternative materials, sustaining automotive's position as the dominant HMDA end-use industry across both internal combustion and electric vehicle platforms.

Textile is expected to grow at a significant CAGR over the forecast period, attributable to the rising usage of hexamethylenediamine in the textile industry for manufacturing apparel and carpets whose nylon fibre content benefits from nylon 6,6's excellent strength, durability, and abrasion resistance characteristics that support premium textile product performance specifications. Nylon 6,6's combination of high tensile strength, elastic recovery, and resistance to abrasion makes it particularly valued in performance apparel, technical textiles, and durable carpet applications whose growing consumer demand across both developed and emerging textile markets is sustaining structural HMDA demand growth from the textile end-use category.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

38.47% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

Asia Pacific Hexamethylenediamine Market Insights

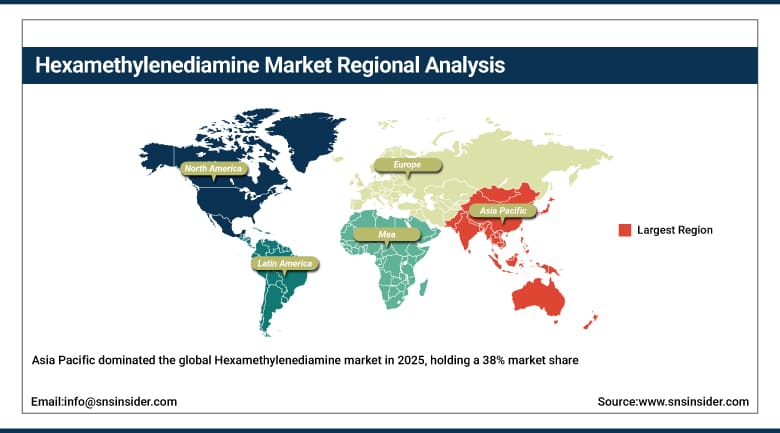

Asia Pacific dominated the global Hexamethylenediamine market in 2025, holding a 38% market share, with China and India serving as key growth drivers due to rapid industrialization, urbanization, and expansion in automotive and textile manufacturing sectors. The increasing production of nylon and HMDA-derived products, coupled with the rise in consumer goods demand, is further boosting market growth across the region. Government initiatives to enhance domestic chemical manufacturing capabilities, including HMDA production, support this regional dominance, with China's position as a major producer of automotive parts and textiles continuing to expand HMDA applications across these growing manufacturing sectors. China accounts for approximately 38.47% of Asia Pacific revenues through its expanding nylon production capacity and large automotive and textile manufacturing base.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Hexamethylenediamine Market Insights

North America emerged as the fastest growing region in the hexamethylenediamine market with a significant growth rate over the forecast period, driven by its well-established nylon 6,6 manufacturing ecosystem and growing automotive light weighting trends. The United States accounts for approximately 82.47% of regional revenue through the increase in demand for durable and lightweight automotive components, a key HMDA application, and the compound's use in synthetic fibres for textiles. The presence of major global HMDA producers including INVISTA and Ascend Performance Materials, whose abundant feedstock availability and advanced petrochemical infrastructure support cost-competitive production, sustains the region's structural growth advantage and growing export competitiveness in global HMDA markets.

Europe Hexamethylenediamine Market Insights

Hexamethylenediamine had a considerable share of the total world revenues in Europe in 2025, with its growth being fueled by increased expenditure on research and development activities of HMDA and increased production in the automotive industry. Germany was the largest market in Europe, thanks to the country's status as the largest automobile producer in the region and because it hosts some of the major HMDA manufacturers such as Covestro, BASF SE, and Evonik. These manufacturers have manufacturing plants in Europe, which support the production in the region. Germany represents about 28.47% of the revenue in Europe thanks to its robust automobile industry and the chemical industry in the country.

MEA & Latin America Hexamethylenediamine Market Insights

Middle East and Latin America are growing Hexamethylenediamine markets, expected to witness steady growth due to investments in infrastructure and industrialization. The UAE leads MEA revenues at approximately 22.84% of the regional total through its growing petrochemical manufacturing sector and expanding automotive and industrial coating applications. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its significant domestic automotive manufacturing and refinishing sector, growing textile industry, and chemical manufacturing infrastructure whose HMDA consumption across nylon synthesis, coatings, and lubricant applications creates consistent regional demand.

Market Dynamics

Growth Driver: Growing automotive light weighting trends and expanding nylon 6,6 demand across automotive, textile, and industrial applications are the primary structural growth drivers of the hexamethylenediamine market.

The growth in the market of hexamethylenediamine is due to the structural effect on account of the ongoing shift towards light weighting within the automobile industry with its progressive utilization of the nylon 6,6 segment for applications like radiator tanks and air intake manifolds, among others, replacing the use of more expensive and heavier metals as it seeks to achieve goals of fuel efficiency and compliance with regulations that are being increasingly introduced in major automotive markets. An increase of one percent in the total global output of automobiles, together with an increase in the nylon 6,6 segment usage per car, leads to an increase in demand for HMDA in line with the structural effect.

Restraint: Feedstock price volatility for adiponitrile and butadiene and tightening environmental regulations create cost pressure and compliance challenges that constrain hexamethylenediamine market growth.

The manufacture of hexamethylenediamine relies on petrochemical-based raw materials like adiponitrile and butadiene, whose prices are highly correlated with trends in the crude oil industry, which results in the volatility of raw material prices, thereby impacting the cost of manufacture for HMDA and reducing manufacturer margins in instances when raw material prices rise above the final goods prices. The environmental laws concerning the emission of chemicals in the manufacturing processes and waste disposal practices are becoming stricter in major areas of HMDA production, necessitating manufacturers to adopt more environmentally friendly methods and document their compliance, a practice that is more likely to be costly for smaller regional manufacturers compared to large chemical companies.

Opportunity: Bio-based hexamethylenediamine development and electric vehicle nylon 6,6 demand growth represent significant commercial opportunities rewarding sustainability innovation and material performance differentiation.

The development of commercially viable bio-based hexamethylenediamine from renewable biomass feedstocks, exemplified by Asahi Kasei's partnership with Genomatica, represents a transformative product innovation opportunity whose successful commercialization would provide automotive and textile manufacturers with verified sustainable nylon 6,6 precursors that satisfy increasingly stringent corporate sustainability procurement criteria without compromising material performance characteristics. Each automotive or textile manufacturer adopting bio-based nylon 6,6 specifications creates premium market demand for verified bio-HMDA production whose sustainability documentation commands meaningful price premiums above conventional fossil-derived alternatives. The electric vehicle transition's growing demand for lightweight, thermally stable, and electrically insulating engineering plastics in battery housing, electrical connector, and structural component applications represents an emerging high-growth HMDA demand vector whose magnitude will scale proportionally with global EV production volume growth through the forecast period.

Recent Developments:

-

2025: Ascend Performance Materials announced expanded production capacity for its nylon 6,6 intermediate chemicals including hexamethylenediamine at integrated U.S. manufacturing facilities to meet growing automotive and industrial demand for high-performance engineering plastics.

-

2023: BASF SE and Evonik Industries continued investment in European HMDA production capacity expansion to support growing automotive and industrial coating demand across Germany's established automotive manufacturing sector and the broader European chemical industry infrastructure.

-

2022: Asahi Kasei entered into a strategic partnership with Genomatica, Inc. to develop bio-based hexamethylenediamine from renewable biomass feedstocks, targeting sustainable nylon 6,6 production for automotive and textile manufacturers with sustainability procurement commitments.

Hexamethylenediamine Market Key Players are:

-

INVISTA

-

Ascend Performance Materials LLC

-

BASF SE

-

Evonik Industries AG

-

DuPont de Nemours Inc.

-

Asahi Kasei Corporation

-

Toray Industries Inc.

-

UBE Industries Ltd.

-

Shandong Haili Chemical Industry Co. Ltd.

-

Liaoning Shuangyi Chemical Co. Ltd.

-

Hengshui Haoye Chemical Co. Ltd.

-

Henan Shenma Nylon Chemical Co. Ltd.

-

Huafeng (China) Co. Ltd.

-

LANXESS AG

-

Domo Chemicals GmbH

-

Genomatica Inc.

-

Covestro AG

-

Merck KGaA

-

Rennovia Inc.

-

China National Bluestar (Group) Co. Ltd

Hexamethylenediamine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.55 Billion |

| Market Size by 2035 | USD 18.59 Billion |

| CAGR | CAGR of 6.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Nylon Synthesis, Coatings, Adhesives, Lubricants, Polyurethane Production, Others) • By End Use Industry (Automotive, Textile, Paints & Coatings, Petrochemical, Electrical & Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | INVISTA, Ascend Performance Materials LLC, BASF SE, Evonik Industries AG, DuPont de Nemours Inc., Asahi Kasei Corporation, Toray Industries Inc., UBE Industries Ltd., Shandong Haili Chemical Industry Co. Ltd., Liaoning Shuangyi Chemical Co. Ltd., Hengshui Haoye Chemical Co. Ltd., Henan Shenma Nylon Chemical Co. Ltd., Huafeng (China) Co. Ltd., LANXESS AG, Domo Chemicals GmbH, Genomatica Inc., Covestro AG, Merck KGaA, Rennovia Inc., and China National Bluestar (Group) Co. Ltd. |

Frequently Asked Questions

Asia Pacific dominated the Hexamethylenediamine Market in 2025, holding a 38% share.

The Hexamethylenediamine Market is expected to grow at a CAGR of 6.58% from 2026 to 2035.

The nylon synthesis segment dominated the Hexamethylenediamine Market in 2025 with a 42% market share.

Growing automotive lightweighting trends driving nylon 6,6 component adoption, expanding global textile and consumer goods manufacturing, rising demand for high-performance engineering plastics in electric vehicle applications.

The Hexamethylenediamine Market was valued at USD 9.55 Billion in 2025.

Get in Touch