Polyphenylene Oxide Market Report Scope & Overview:

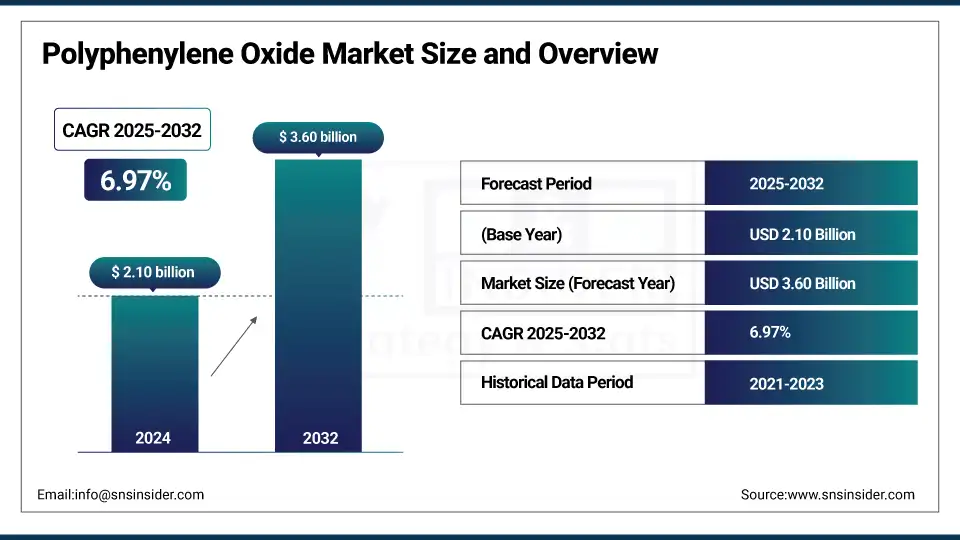

The Polyphenylene Oxide Market Size was valued at USD 2.10 billion in 2024 and is expected to reach USD 3.60 billion by 2032, growing at a CAGR of 6.97% over the forecast period of 2025-2032.

The Polyphenylene Oxide market analysis sheds light on a towering demand for improved polymer blend products in response to an increasing industry demand for materials with excellent mechanical properties, chemical resistance, and thermal stability. Modified PPO (MPPO) blends, especially those modified with polystyrene (PS) or polyamide (PA), are also favored in industries, such as automotive and electronics that require high-performance lightweight plastic. These formulations provide a cost-effective alternative to premium engineering plastics while retaining strength and heat resistance. Elsewhere, OEMs and product designers are specifying modified PPO for its improved moldability and impact resistance, a key reason for its popularity in high-precision applications. This is a trend that is only going to get faster, and manufacturers looking for material solutions that are tunable for more advanced end-use needs, which drive the polyphenylene oxide market growth.

Polyphenylene Oxide Market Size and Forecast:

-

Market Size in 2024: USD 2.10 Billion

-

Market Size by 2032: USD 3.60 Billion

-

CAGR: 6.97% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2023

To Get more information On Polyphenylene Oxide Market - Request Free Sample Report

Polyphenylene Oxide Market Trends:

-

Rising demand for lightweight, high-performance engineering plastics in automotive applications

-

Increasing use of modified PPO blends (MPPO) with polystyrene and polyamide for improved performance

-

Growing adoption of PPO in electronics due to thermal stability and electrical insulation properties

-

Expanding applications in medical and healthcare devices requiring sterilizable and biocompatible materials

-

Increasing investments in advanced polymer manufacturing and high-purity PPO compounds

-

Rising focus on recyclable and sustainable engineering thermoplastics in industrial applications

The U.S. Department of Energy’s Advanced Materials & Manufacturing Technologies Office (AMMTO) has set aside USD 72 million to fund SBIR/STTR projects that target advanced materials, such as reinforced polymer blends, composites, and recyclability-enhanced polymers in the fiscal years 2023 and 2024.

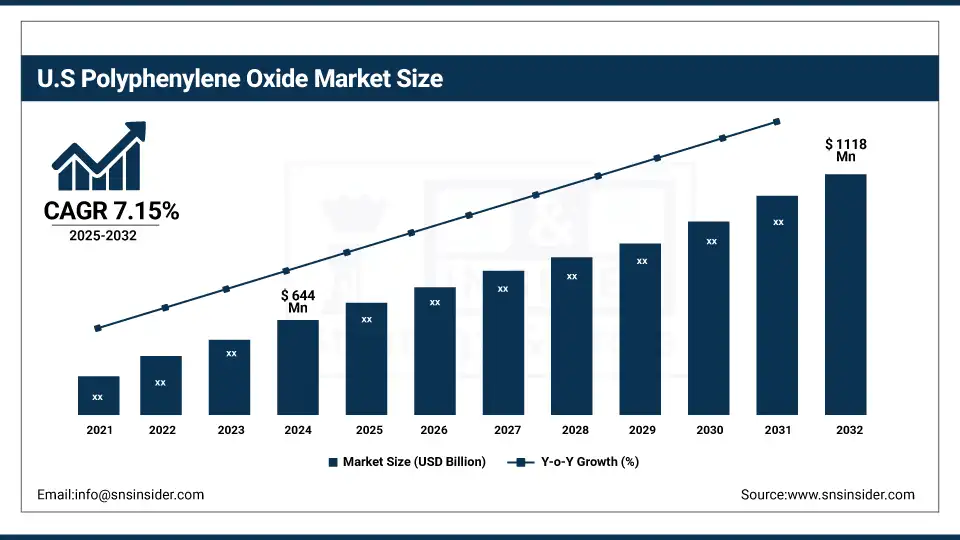

The U.S. Polyphenylene Oxide market size was USD 644 million in 2024 and is expected to reach USD 1118 million by 2032 and grow at a CAGR of 7.15% over the forecast period of 2025-2032. The region’s growth is driven by the advanced materials industry and as it uses heavy amounts of PPO in healthcare, defence, and electrical sectors. PPO is being used more in diagnostic apparatus and sterilizable components as a result of its compliance with U.S. FDA and USP Class VI regulations. RTP Company introduced a new line of high-purity PPO-based compounds targeting reusable medical devices at its Minnesota facility in 2023 to reinforce the U.S.-based material supply chains for hospital-grade components.

Market Dynamics:

Key Drivers:

-

Rising Demand in Automotive Lightweighting Initiatives Drive the Market Growth

The low density, dimensional stability and heat resistance of polyphenylene oxide make it appropriate for automotive parts at a time when motorists are attempting to cut down the weight of their vehicles and increase fuel efficiency. Automotive OEMs are migrating more and more to PPO-based products for under-the-hood, [electric] vehicle and structural components. The push to meet emissions standards and save gas is helping drive demand for thermoplastic materials that substitute for metal components without sacrificing strength or thermal performance.

for instance, in 2023, General Motors revealed a USD 500 million investment to upgrade its Electric Vehicle manufacturing lines in Ohio, which involved adding higher levels of light-weight PPO-based polymers within vehicle components to meet greater energy efficiency and range goals.

Restraints:

-

High Production Cost and Limited Material Compatibility May Hamper the Market Growth

The properties of PPO are also relatively expensive to make and process, primarily due to its poor compatibility with some common polymers. This reduces its blending potential and enhances the cost of compounding so as to confining its use in price-driven markets. Small and medium-sized manufacturers do not typically find it cost-effective when compared to lower-cost engineering thermoplastics, such as ABS or polypropylene. The demand is often, therefore it is particularly focused on luxury or specialist markets. It has sometimes involved clashes as countries and powerful individuals have sought to control these elements for their power.

Opportunities:

-

Technological Advancements in On-site and Mobile Water Treatment Solutions Create an Opportunity for the Market

High-performance polymers, such as Polyphenylene Oxide (PPO) are of growing interest in the medical industry with increasing demand for tough, biocompatible, and sterilizable materials. PPO is desirable for reusable medical products due to its excellent hydrolytic stability, low moisture absorption, high-performance plastics, and chemical/heat resistance. Applications are diagnostic housings, blood filtration systems, and valve assemblies that require dimensional stability and reliability after repeated sterilization cycles (autoclaving, irradiation, gamma, or ethylene oxide), which drive the polyphenylene oxide market trends.

In 2022, SABIC, a leading producer of engineering thermoplastics for global medical device OEMs, invested USD 150 Million to boost its production capacity and enhance the manufacturing capabilities of LNP™ PPO resins at an Indiana, U.S. plant in the wake of tiering demands put on it by North American medical device manufacturers.

Segmentation Analysis:

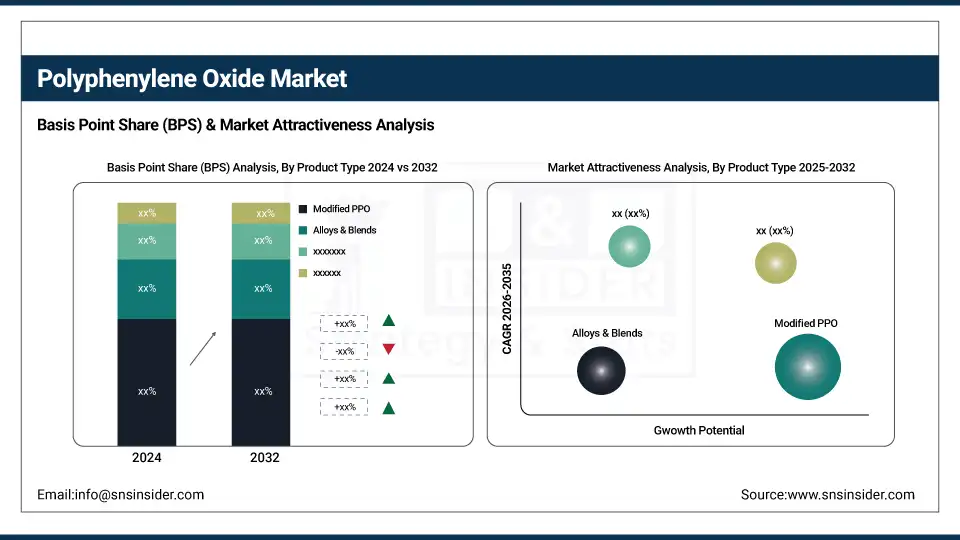

By Product Type

Modified PPO accounts for the highest share of 41% in the market due to its improved thermal and mechanical characteristics, making it a suitable structural component used in automotive and electronics gainshare substitute. Due to its compatibility with other polymers, it can be partly blended to meet certain performance requirements.

Alloys & Blends is the largest and fastest-growing market by type, owing to rising demand for hybrid materials in lightweight products such as healthcare and industrial machinery.

By Processing Technique

Injection Molding dominates with over 48% market share due to its precision, scalability, and suitability for complex part manufacturing, especially in electronics and healthcare devices.

Blow Molding is witnessing the fastest growth as it enables the production of hollow and lightweight parts, gaining traction in fluid-handling components and healthcare packaging innovations.

By Distribution Channel

Direct Sales account for around 50% of the market share, as OEMs and large-volume buyers prefer direct procurement for customized grades and bulk supply contracts.

Online Retail is the fastest-growing segment, supported by increasing digitalization and accessibility to engineering thermoplastics through e-commerce platforms catering to SMEs and research institutions.

By Application

Automotive remains the leading application segment with nearly 35% market share, driven by the need for high-performance and heat-resistant polymers in under-the-hood components and electrical systems.

Medical & Healthcare Devices is the fastest-growing segment due to PPO’s ability to withstand sterilization processes and meet biocompatibility standards, making it ideal for diagnostics and reusable instruments.

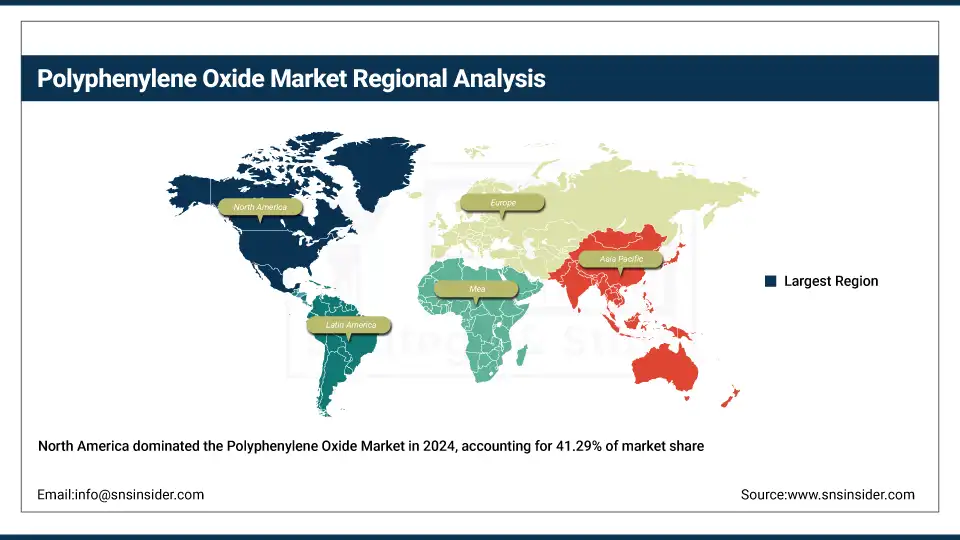

Regional Analysis:

North America held the Polyphenylene Oxide market share largest market 2024, around 41.29% 2024. It is due to its strong industrial base, particularly automobile, electrical, and medical. Pile players and focus on high-performance engineering plastics fuels demand for PPO. Furthermore, the area has strong R&D capabilities and strict regulations promoting flame-retardant and long-lasting materials.

Get Customized Report as per Your Business Requirement - Enquiry Now

In 2022, SABIC announced a USD 150 million investment in its Indiana site to increase capacity for production of LNP PPO resins to address heightened demand in the medical and automotive markets, serving local OEMs with FDA-compliant, sterilizable materials.

The Asia Pacific region is the fastest-growing market due to the increase in manufacturing sector with a robust electronic and automotive industry across China, Japan, South Korea, and India. The growing requirement for heat-resistant, lightweight polymers, and the surging production of consumer electronics are driving PPO use.

Mitsubishi Chemical increased its capacity for PPO compounding in Japan during late 2023 to support local needs and bolster supply reliability, especially for EV parts, high-efficiency electronic components.

Europe maintains a significant share of the Polyphenylene Oxide market. Europe has a strong presence in the PPO market, driven by strict environmental norms, energy-efficient automobile design, and increasing advanced medical equipment. Germany and France are the front-runners in precision engineering and sustainable use of plastic.

In 2023, LyondellBasell launched a recyclable PPO-based compound at its Germany plant through a circular economy program targeting lower carbon emissions for the automotive and consumer goods market.

Key Players:

Major Polyphenylene Oxides companies are SABIC, Mitsubishi Chemical Group, Asahi Kasei Corporation, RTP Company, Ensinger GmbH, Evonik Industries AG, Sumitomo Chemical Co., Ltd., LyondellBasell Industries, Solvay S.A., Toray Industries, Inc., Polyplastics Co., Ltd., LG Chem, Chi Mei Corporation, Teknor Apex, Celanese Corporation, RadiciGroup, Daicel Corporation, Arkema, Kingfa Sci. & Tech. Co., Ltd., Kumho Petrochemical Co., Ltd.

Recent Development:

-

In 2024, Solvay launched an R&D partnership focused on next-generation PPO-based materials for electrification and battery safety applications in Europe.

-

In 2023, Techmer PM introduced color and additive masterbatches compatible with PPO resins to improve UV resistance and aesthetics in consumer electronics.

| Report Attributes | Details |

| Market Size in 2024 | USD 2.10 Billion |

| Market Size by 2032 | USD 3.60 Billion |

| CAGR | CAGR of6.97% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Virgin PPO, Modified PPO, Alloys & Blends, and Others) • By Processing Technique (Injection Molding, Extrusion, Blow Molding, Compression Molding, and Others) • By Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Retail, Specialty Stores) • By Application (Automotive, Electrical & Electronics, Healthcare & Medical Devices, Industrial Machinery, Consumer Goods, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | SABIC, Mitsubishi Chemical Group, Asahi Kasei Corporation, RTP Company, Ensinger GmbH, Evonik Industries AG, Sumitomo Chemical Co., Ltd., LyondellBasell Industries, Solvay S.A., Toray Industries, Inc., Polyplastics Co., Ltd., LG Chem, Chi Mei Corporation, Teknor Apex, Celanese Corporation, RadiciGroup, Daicel Corporation, Arkema, Kingfa Sci. & Tech. Co., Ltd., Kumho Petrochemical Co., Ltd. |

Frequently Asked Questions

Ans Trends like rising use in electric vehicles, recyclable blends, and growing medical-grade PPO innovations are shaping the market's future.

Ans Key players include SABIC, Mitsubishi Chemical, Asahi Kasei, LyondellBasell, RTP Company, and Ensinger GmbH.

Ans PPO compounds are widely used in connectors, pump housings, medical device casings, and under-the-hood automotive components.

Ans Automotive, electrical & electronics, and healthcare are the primary consumers of PPO due to its thermal and mechanical properties.

Ans Increasing demand for lightweight, heat-resistant polymers in automotive, electronics, and medical sectors is driving global PPO market growth.

Get in Touch