Dimethylformamide Market Report Scope & Overview:

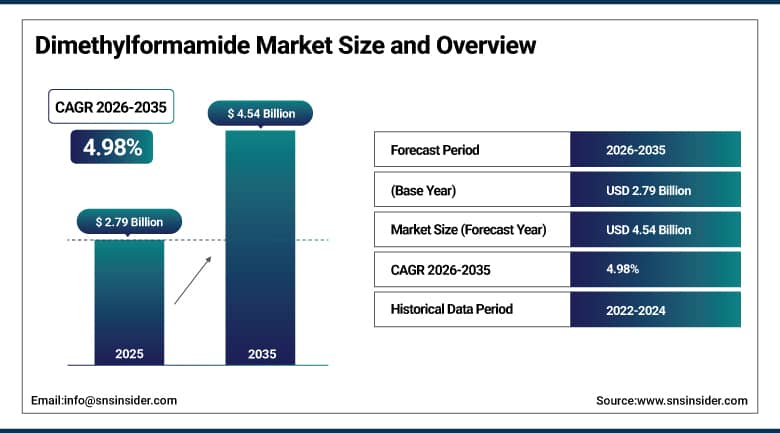

The Dimethylformamide Market was valued at USD 2.79 Billion in 2025 and is expected to reach USD 4.54 Billion by 2035, growing at a CAGR of 4.98% from 2026–2035.

The global dimethylformamide market is advancing across an expanding set of industrial and pharmaceutical applications that leverage the compound’s exceptional solvency characteristics as a dipolar aprotic solvent whose complete miscibility with water, organic solvents, and a broad range of resins, polymers, and active pharmaceutical ingredients makes it the preferred process solvent in pharmaceutical active ingredient synthesis, polyurethane coating formulation, synthetic leather production, and agrochemical manufacturing. DMF’s high boiling point of 153°C, thermal stability, and chemical inertness toward many reagent classes create the process chemistry conditions that pharmaceutical manufacturers require for API crystallization, recrystallization, and reaction control, sustaining pharmaceutical-grade DMF as the highest-value market segment despite its smaller volume relative to industrial grade consumption.

In 2024, Luxi Chemical Group Co. Ltd., one of China’s leading DMF producers, completed a capacity expansion at its Liaocheng production facility adding 50,000 tonnes per year of additional DMF output to serve growing domestic pharmaceutical, textile, and electronics sector demand. The expansion reflected China’s dual role as both the world’s largest DMF consumer and its most significant producer, where domestic demand growth from the expanding pharmaceutical API export industry and the polyurethane synthetic leather production sector creates consistent investment motivation for domestic capacity addition above existing production infrastructure.

Market Size and Forecast:

-

Market Size in 2026E: USD 2.93 Billion

-

Market Size by 2035: USD 4.54 Billion

-

CAGR: 4.98% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Dimethylformamide Market - Request Free Sample Report

Dimethylformamide Market Trends:

-

Pharmaceutical API synthesis demand for high-purity DMF is growing with India and China’s expanding generic and innovative drug active ingredient manufacturing export programmes.

-

Regulatory pressure from REACH and EPA solvent substitution programmes is accelerating green chemistry research into DMF alternatives for applications where substitution is technically feasible.

-

Electronic-grade ultra-high-purity DMF demand is growing with semiconductor advanced node fabrication expansion requiring low-particulate, low-metallic-impurity solvent specifications.

-

Polyurethane synthetic leather production’s shift from solvent-based to water-based processes is progressively reducing DMF consumption per unit of textile output in regulated markets.

-

Agrochemical formulation demand for DMF as a reaction solvent and active ingredient carrier is growing with expanding crop protection chemical production in Asia Pacific.

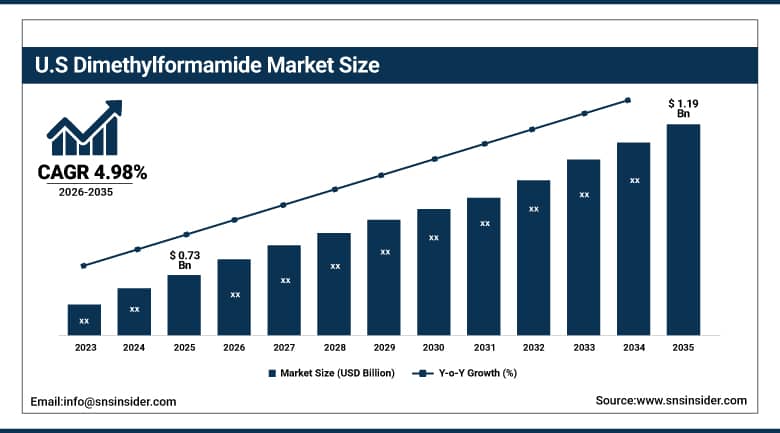

U.S. Dimethylformamide Market Outlook:

The U.S. Dimethylformamide Market was valued at approximately USD 0.73 Billion in 2025 and is expected to grow at a CAGR of approximately 4.98% through 2026-2035 and would value USD 1.19 Billion in 2035.

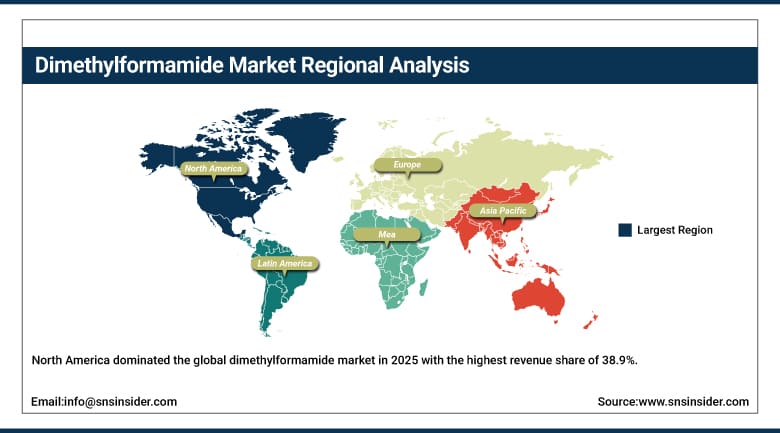

North America held the largest DMF revenue share of 38.9% in 2025, with the United States as the dominant national market through its large pharmaceutical API manufacturing sector’s high-purity DMF consumption, the specialty coatings and adhesives industry’s solvent demand, and the petrochemical sector’s DMF use as a chemical intermediate. BASF Corporation and Eastman Chemical’s North American DMF distribution operations sustain domestic supply chain depth for regulated pharmaceutical-grade procurement.

In 2024, BASF SE expanded its global DMF distribution network to address growing pharmaceutical-grade demand from the North American and European contract drug manufacturing organization sector. Whose API production volume growth is creating above-market pharmaceutical-grade DMF procurement expansion at the high-purity quality specifications that ICH Q7 Good Manufacturing Practice guidelines for active pharmaceutical ingredient manufacturing mandate for solvent quality documentation and impurity profiling.

Dimethylformamide Market Segment Analysis:

-

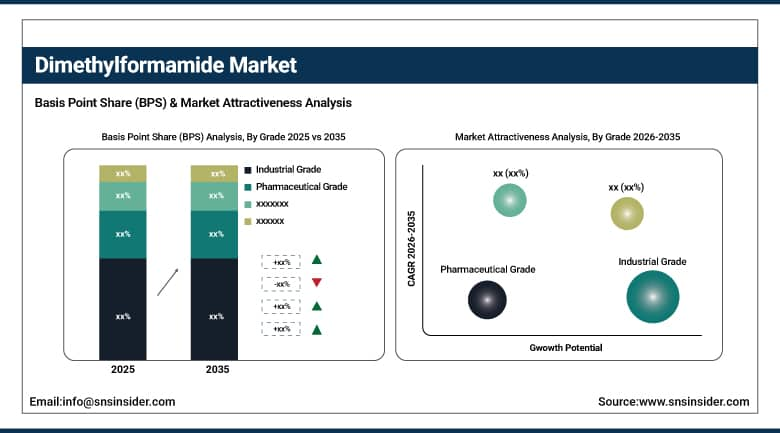

By Grade, industrial grade segment dominated the dimethylformamide market with approximately 58.4% share in 2025, while the pharmaceutical grade segment is the fastest growing with a CAGR of approximately 7.9%.

-

By Process, solvent segment dominated the dimethylformamide market with approximately 51.4% share in 2025, while the Catalyst segment is the fastest growing with a CAGR of approximately 6.8%.

-

By Application, pharmaceuticals segment dominated the dimethylformamide market with the largest share in 2025, while the textile segment is the fastest growing application.

By Grade, industrial grade dominates, pharmaceutical grade grows fastest

Industrial grade retained the dominant position with approximately 58.4% of the dimethylformamide market in 2025. Its commercial primacy reflects the volume concentration of DMF consumption in bulk industrial applications whose cost sensitivity and throughput scale create specification preference for industrial purity grades over the tighter impurity limits and GMP documentation requirements of pharmaceutical and electronic grades. Synthetic leather and polyurethane coating manufacture using DMF as the primary polyurethane dissolution and wet coagulation solvent represents the single largest individual industrial grade DMF application category, where each square metre of synthetic leather fabric processed consumes proportional DMF that is partially recovered and recycled but whose make-up demand sustains consistent procurement.

Pharmaceutical grade is growing fastest at approximately 7.9% CAGR because the global pharmaceutical API manufacturing expansion in India, China, and Europe is creating above-baseline high-purity DMF demand whose per-kilogram price premium over industrial grade reflects the GMP manufacturing documentation, metallic impurity specification, and controlled substance-compliant supply chain that pharmaceutical manufacturers require from their critical process solvent suppliers. Each new pharmaceutical molecule whose synthesis route specifies DMF as a reaction or crystallization solvent creates a multi-tonne annual pharmaceutical-grade procurement relationship whose quality continuity requirements sustain long-term supplier relationships.

By Application, pharmaceuticals dominate, textile grows fastest

Pharmaceuticals retained the dominant application position with the largest share of the dimethylformamide market in 2025. DMF’s exceptional solvency for pharmaceutical active ingredients, reagents, and catalysts makes it the preferred solvent across numerous API synthesis routes including beta-lactam antibiotic synthesis, antifungal agent crystallization, oncology drug intermediate processing, and anti-inflammatory compound formulation whose combined global pharmaceutical manufacturing volume creates the largest individual application demand for pharmaceutical-grade DMF. The ICH Q3C solvent classification’s Category 2 designation for DMF, which imposes maximum daily exposure limits in finished drug products rather than prohibiting its use, sustains DMF’s specification in pharmaceutical synthesis while creating residual solvent testing requirements that define the quality standard for pharmaceutical-grade DMF procurement.

Textile is growing fastest as the expanding synthetic leather and polyurethane textile production in Asia Pacific, particularly in China, Vietnam, and India, driven by growing domestic consumer goods demand and footwear export market growth creates above-market DMF consumption growth in the region’s manufacturing cluster. Each new synthetic leather production facility commissioned to serve growing footwear, automotive interior, and furniture upholstery markets in Asia creates substantial DMF procurement whose industrial grade specification and high volume per production line create commercial relationships with regional DMF suppliers.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

52.4% |

|

Middle East & Africa |

Saudi Arabia |

28.4% |

|

Latin America |

Brazil |

43.8% |

North America Dimethylformamide Market Insights

North America dominated the global dimethylformamide market in 2025 with the highest revenue share of 38.9%, driven by its large pharmaceutical manufacturing sector’s high-purity DMF consumption, the specialty chemicals industry’s solvent demand, and the advanced coatings and adhesives sector’s industrial grade procurement. The United States accounts for approximately 82.5% of North American revenues through its pharmaceutical API manufacturing and the commercial distribution presence of BASF, Eastman Chemical, and Merck KGaA’s North American operations that sustain domestic pharmaceutical-grade supply chain depth.

Canada contributes supplementary North American revenues through its pharmaceutical and specialty chemical sectors’ DMF consumption, the growing Canadian generic pharmaceutical API manufacturing investment whose solvent procurement includes pharmaceutical-grade DMF, and the industrial coatings and adhesives sector’s solvent demand from construction and automotive manufacturing applications whose growth tracks Canadian industrial sector activity.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Dimethylformamide Market Insights

Europe is a technically sophisticated DMF market where REACH regulation’s Substance of Very High Concern authorization requirement for DMF creates compliance-driven supply chain documentation investment and progressive substitution pressure in applications where technically feasible alternatives exist. Germany accounts for approximately 28.5% of European revenues through its large pharmaceutical API manufacturing sector, the specialty coatings industry’s solvent procurement, and the commercial presence of BASF SE’s European DMF distribution network whose quality documentation capabilities serve regulated industry requirements.

Switzerland’s pharmaceutical multinational sector’s API manufacturing, France’s specialty chemical industry, and the United Kingdom’s pharmaceutical and fine chemical sector collectively sustain European DMF demand. European ECHA’s progressive REACH restrictions on DMF in consumer and professional products are creating market transition toward water-based coating alternatives in some textile and coatings applications, while sustaining pharmaceutical and specialty chemical industrial demand where authorization documentation supports continued use.

Asia Pacific Dimethylformamide Market Insights

Asia Pacific is the fastest-growing regional dimethylformamide market, driven by China’s world-leading synthetic leather production, the rapidly expanding Indian pharmaceutical API export industry, and the growing agrochemical and electronics manufacturing sectors across the region. China accounts for approximately 52.4% of Asia Pacific revenues through its dominant position as both the world’s largest DMF producer and consumer, where Luxi Chemical Group, Jiutian Chemical Group, and Zhejiang Realsun Chemical collectively supply domestic demand from textile, pharmaceutical, and electronics applications.

India is the most commercially dynamic emerging DMF market within Asia Pacific, where the pharmaceutical API manufacturing sector’s 600-plus US FDA-registered production sites create large-scale pharmaceutical-grade DMF procurement from both domestic and import sources. The growing Indian synthetic leather production for footwear export and the expanding agrochemical formulation sector create additional industrial-grade demand that is progressively creating domestic DMF production capacity investment. South Korea’s electronics sector and Japan’s specialty chemical industry contribute premium secondary regional demand.

MEA & Latin America Dimethylformamide Market Insights

Saudi Arabia leads MEA revenues through its growing petrochemical and specialty chemical sector’s DMF consumption, the pharmaceutical sector’s import demand for high-purity pharmaceutical-grade DMF, and the industrial coatings sector’s growing procurement as Vision 2030’s manufacturing sector development creates new domestic industrial solvent demand. Egypt and South Africa contribute regional secondary demand through their pharmaceutical and chemical manufacturing sectors.

Brazil leads Latin American revenues through its pharmaceutical manufacturing sector’s API production solvent demand, the agricultural chemical formulation industry’s DMF procurement, and the specialty chemicals and coatings sector’s industrial grade consumption. Mexico and Argentina contribute growing secondary demand through their pharmaceutical and chemical manufacturing expansion.

Market Dynamics:

Growth Drivers: Pharmaceutical API manufacturing expansion in Asia and electronics-grade purity demand from semiconductor fabrication creating above-baseline DMF market growth

The dimethylformamide market’s growth is driven by the structural expansion of the pharmaceutical API manufacturing sector in India and China whose growing global export share of branded and generic drug active ingredients creates proportional pharmaceutical-grade DMF solvent procurement. That grows with each new API manufacturing facility commissioned and each new drug synthesis route that specifies DMF as a critical process solvent. India’s pharmaceutical export growth targeting USD 130 billion in exports by 2030 under the national pharmaceutical policy creates a compounding annual DMF demand driver whose commercial scale is largest in Asia Pacific but whose export-quality production standards require pharmaceutical-grade DMF specification that sustains premium-grade market growth above commodity industrial grade dynamics.

Restraints: REACH regulatory pressure and health risk reclassification driving substitution in European consumer applications and creating compliance cost burden for producers

The European Chemicals Agency’s classification of DMF as a Substance of Very High Concern under REACH due to its reproductive toxicity category 1B designation creates regulatory substitution pressure across European applications where the authorization requirement’s administrative burden and sunset date management create incentive for substitution with less restricted solvent alternatives wherever technically feasible. Each European application that successfully transitions from DMF to N-methyl-2-pyrrolidone alternatives, bio-based aprotic solvents, or water-based processing reduces European DMF procurement and creates a permanent market segment reduction that offsets pharmaceutical and electronics demand growth. Worker occupational exposure limit tightening across multiple jurisdictions creates engineering control investment requirements for DMF-using facilities whose ventilation, enclosed process, and biological monitoring requirements add production cost above chemical procurement.

Opportunities: Pharmaceutical grade expansion in emerging markets and electronic-grade ultra-high-purity DMF for advanced semiconductor applications creating premium market development

The pharmaceutical manufacturing sector’s progressive capacity expansion in emerging markets including India, China, Brazil, and Southeast Asia creates a growing addressable market for pharmaceutical-grade DMF. Whose regulatory quality documentation, supply chain traceability, and impurity specification requirements create commercial differentiation for established pharmaceutical-grade DMF producers whose GMP manufacturing certification sustains premium pricing above industrial grade commodity markets. Each new pharmaceutical manufacturing facility built in India, China, or Southeast Asia for API production whose synthesis routes specify DMF creates a multi-year pharmaceutical-grade DMF supply relationship whose quality continuity requirements and regulatory file linkage to specific DMF supplier specifications create switching barriers that sustain commercial relationships independent of spot market pricing. Electronic-grade ultra-high-purity DMF whose metallic ion and particle contamination specifications target parts-per-trillion levels for advanced semiconductor process node compatibility create a technically challenging and premium-priced product tier.

Recent Developments:

-

2024: Luxi Chemical Group completed a 50,000 tonne per year DMF capacity expansion at its Liaocheng production facility to serve growing domestic pharmaceutical, textile, and electronics sector demand in China, reinforcing its position as one of the world’s leading DMF producers.

-

2024: BASF SE expanded its global pharmaceutical-grade DMF distribution network to serve growing contract drug manufacturing organisation demand in North America and Europe, addressing increasing API synthesis solvent procurement requirements under ICH Q7 GMP quality standards.

-

2023: Eastman Chemical Company launched enhanced pharmaceutical-grade DMF with improved metal ion certificate of analysis documentation and supply chain traceability features meeting new ICH Q7 elemental impurities guidance requirements for pharmaceutical solvent qualification.

Dimethylformamide Market Key Players are:

-

BASF SE

-

Eastman Chemical Company

-

Luxi Chemical Group Co. Ltd.

-

Jiutian Chemical Group Co. Ltd.

-

Zhejiang Realsun Chemical Co. Ltd.

-

HELM AG

-

Merck KGaA

-

Solvay SA

-

Thermo Fisher Scientific Inc.

-

Hubei Sanonda Co. Ltd. (ADAMA)

-

Gansu Yinguang Chemical Industry Co. Ltd.

-

Inner Mongolia Yuanxing Energy Co. Ltd.

-

Triveni Chemicals

-

Archer Daniels Midland Company

-

Huaqiang Chemical Group

-

Tokyo Chemical Industry Co. Ltd.

-

Sigma-Aldrich Corporation (Merck)

-

LANXESS AG

-

Dongyue Group Ltd.

-

Quzhou Runtu Co. Ltd.

Dimethylformamide Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.79 Billion |

| Market Size by 2035 | USD 4.54 Billion |

| CAGR | CAGR of 4.98% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade) • By Process (Solvent, Catalyst, Raw Material) • By Application (Pharmaceuticals, Chemical Manufacturing, Paints & Coatings, Textile, Agriculture, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Eastman Chemical Company, Luxi Chemical Group Co. Ltd., Jiutian Chemical Group Co. Ltd., Zhejiang Realsun Chemical Co. Ltd., HELM AG, Merck KGaA, Solvay SA, Thermo Fisher Scientific Inc., Hubei Sanonda Co. Ltd. (ADAMA), Gansu Yinguang Chemical Industry Co. Ltd., Inner Mongolia Yuanxing Energy Co. Ltd., Triveni Chemicals, Archer Daniels Midland Company, Huaqiang Chemical Group, Tokyo Chemical Industry Co. Ltd., Sigma-Aldrich Corporation (Merck), LANXESS AG, Dongyue Group Ltd., and Quzhou Runtu Co. Ltd. |

Frequently Asked Questions

The Dimethylformamide Market is expected to grow at a CAGR of 4.98% from 2026 to 2035.

The Dimethylformamide Market was valued at USD 2.79 Billion in 2025.

Pharmaceutical API manufacturing expansion in India and China creating pharmaceutical-grade DMF demand, electronics-grade ultra-high-purity DMF demand from semiconductor fabrication expansion are the primary growth factors.

The Industrial Grade segment dominated the Dimethylformamide Market with approximately 58.4% share in 2025

North America dominated the Dimethylformamide Market in 2025 with the highest revenue share of 38.9%.

Get in Touch