Prefilled Syringes Market Report Scope & Overview:

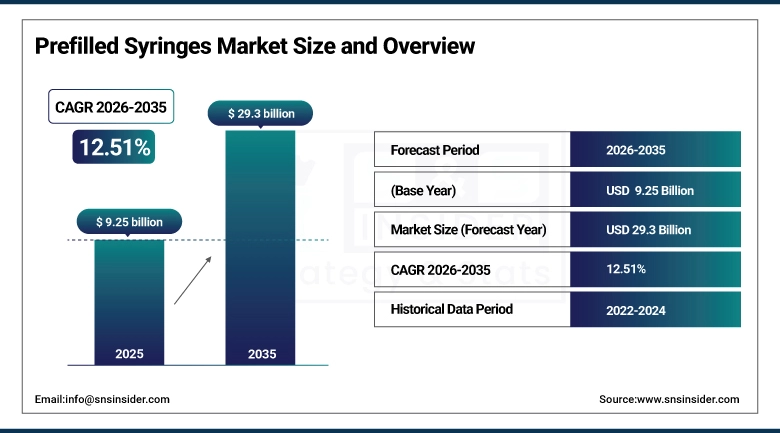

The Prefilled Syringes Market was estimated at USD 9.25 billion in 2025 and is expected to reach USD 29.3 billion by 2035 and grow at a CAGR of 12.51% over the forecast period of 2026-2035.

Prefilled syringes are single-dose drug delivery devices into which a manufacturer has already loaded the drug, eliminating the need for the patient or health care provider to draw up and measure the dose from a vial. Another advantage of this design is that it reduces dosing errors, contamination risk, significantly reduce time for drug administration, and increase patient self-administration convenience. One of the main reasons driving this change within the pharmaceutical industry is their focus on biologic drugs such as monoclonal antibodies, vaccines, and insulin analogs since these complex protein-based drugs need to be formulated carefully and are best suited for delivry via prefilled syringes. The large and rapidly expanding self-administration market, in which patients administer biological therapies to themselves at home instead of receiving injections in a clinical setting, has an especially high demand for easy-to-use prefilled syringe formats.

The Asia Pacific Prefilled Syringes market is expected to witness the fastest growth and register a notable CAGR of 13.66%, due to the rapidly increasing pharmaceutical and biotechnology industries in China, India, and Japan along with rising healthcare spending; and growing burden of chronic diseases that leads to increased use of injectable biologics during the forecast period

Market Size and Forecast:

-

Market Size in 2025: USD 9.25 Billion

-

Market Size by 2035: USD 29.3 Billion

-

CAGR: 12.51% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Prefilled Syringes Market - Request Free Sample Report

Prefilled Syringes Market Trends:

-

Growing biologic and biosimilar drug pipeline driving sustained demand for prefilled syringe formats compatible with complex biologics.

-

Integration of passive and active safety devices into prefilled syringe systems to prevent needlestick injuries to healthcare workers.

-

Auto-injector devices building on prefilled syringes to enable easier self-injection for patients with limited dexterity.

-

Dual-chamber prefilled syringes enabling reconstitution of lyophilized biologics at point of use, extending shelf life.

-

Rising adoption of home healthcare and self-injection driving demand for user-friendly prefilled syringe formats.

-

Glass prefilled syringe alternatives using COP/COC plastic reducing breakage risk and enabling more complex device integration.

-

Digital health integration with smart prefilled syringes incorporating sensors for adherence monitoring and injection tracking.

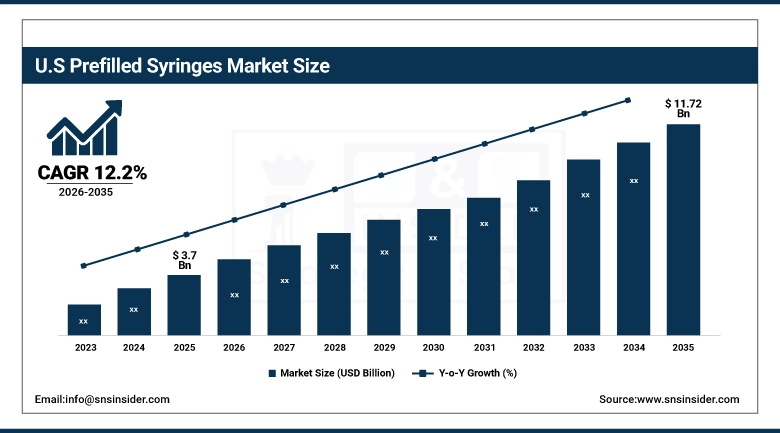

The U.S. Prefilled Syringes Market was valued at USD 3.7 billion in 2025 and is expected to reach USD 11.72 billion by 2035, at a CAGR of 12.2% from 2026 to 2035.

USA accounts for the largest worldwide market for prefilled syringes owing to being the worlds biggest pharmaceutical market, high levels of uptake from biologic agents such as monoclonal antibodies and insulin analogues as well strong patient demand for self-injection presentations. Sustained demand growth is being fueled in part by the FDA approval of a number of biologic drugs in prefilled syringe format as well as the growing biosimilar market. Key demand drivers are the expected convenience of home selfadministration of therapies for chronic diseases, in the USA.

The U.S. biosimilar market is rapidly growing and at the same time expanding its basket of products with multiple biologic drugs such as Humira, Enbrel, Rituxan facing biosimilar competition. The competition between biosimilar manufacturers is not only based on price but also the convenience of formulation, and prefilled auto-injector pens have become an essential competitive advantage for gaining market share from the original branded products.

Prefilled Syringes Market Segmentation Analysis:

-

Based on Type, Disposable prefilled syringes dominate the market; Reusable systems serve niche applications with frequent dosing requirements.

-

Based on Material, Glass dominates due to established compatibility data for biologics; Plastic (COP/COC) is growing for shock-resistant applications.

-

Based on Design, Single-Chamber leads; Dual-Chamber is growing rapidly for lyophilized biologics requiring reconstitution.

-

Based on Application, Biologics & Biosimilars is the largest and fastest-growing application; Vaccines represent a large volume segment.

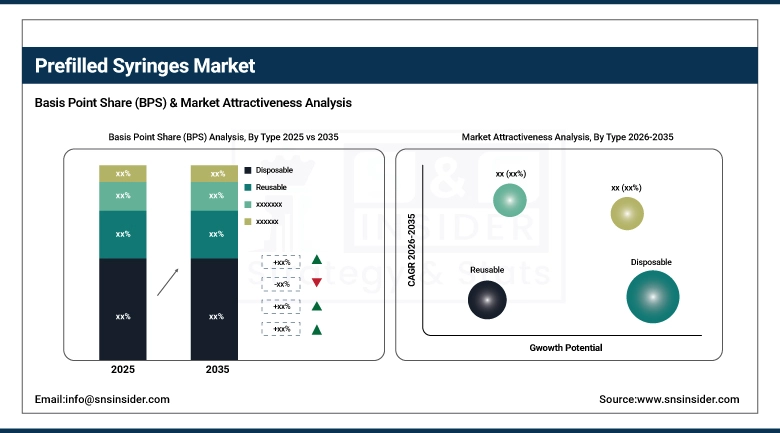

By Type: Disposable Dominates, Reusable Growing Fastest

Disposable prefilled syringes however, account for the largest market globally owing to their widespread usage in vaccine delivery and biologics but mainly if they must be employed as first line drug delivery through insulin or emergency medications since single use administration plays a crucial role in maintaining sterility and decreasing cross contamination ultimately contributing to patient safety. They continue to see rapid uptake driven by increasingly stringent regulatory guidelines, growing immunization efforts and rising demand for ready-to use injectable drug formats that reduce preparation time in the clinical setting. This is because pharmaceutical companies and healthcare providers favour disposable formats since they enhance dosage accuracy and reduce the risk of medication errors, making them the standard for hospitals and clinics globally.

Reusable prefilled syringes represents the fastest growing segment owing to increased focus on cost-efficiency in long term therapies and increasing attention towards sustainability aspect of the healthcare systems. These syringes are getting popular in diseases where repeated dosing is needed, e.g. Diabetes and Autoimmune disorders as they help to reduce overall treatment costs/midical waste generation. The developments in sterilization technologies and material authentication are further bolstering adoption, although healthcare systems in developed regions are increasingly assessing reusable solutions as part of wider eco-friendly programs or resource-efficiency objectives.

By Design: Single-Chamber Dominates, Dual-Chamber Growing Fastest

Marketed single-chamber prefilled syringes are prevailing in the market, especially for standard injectable drugs, vaccines and biologics because of their simple structure, simpler manufacture and delivery systems with a lower drug product development cost and high reliability. They are widely embraced because of their compatibility with a large number of pharmaceutical formulations and strong integration into mass immunization and routine health care programs. Furthermore, single-chamber systems are efficient at high-volume production, which is important for large-scale deployment of vaccines and emergency health care.

dual-chamber prefilled syringes segment is estimated to account for the largest growth rate during 2023-2030 owing to rising demand for complex biologics and advanced pharmaceutical formulations that need long-term separation of active ingredients and solvents until they are needed. Recently, these types of syringes are being extensively employed for lyophilized drugs, combination therapies and sensitive biologics that will be reconstituted before injectable. Adoption among oncology, rare disease treatment, and specialty pharmaceuticals where formulation integrity and precision are critical to facilitating drug stability improvement, shelf life extension, and enhanced treatment efficiency..

By Material: Glass Dominates, Plastic Growing Fastest

Glass prefilled syringes dominate the market owing to their excellent chemical inertness, superior barrier properties, and long-established acceptance in pharmaceutical packaging. These are widely used for biologics, vaccines, and high-value injectables to provide stability of the drug, act as a barrier against contaminates and protect formulation integrity over prolonged periods. Regulatory bodies and drug manufacturers still gravitate towards glass because of its excellent compatibility properties with a wide range of drug molecules as well as regulatory approval of injectable delivery systems that meet the relevant safety and quality standards.

The fastest-growing segment is plastic prefilled syringes, owing to their lightweight characteristics with much higher break resistance and the growing demands in advanced drug delivery systems. They are particularly gaining prevalence in home health care and self-administration therapies, where portability and safety is essential. Continuous polymer material innovations with better drug-coating properties overcome absorption problems, allowing greater implementation for biologics and chronic disease therapies and treatments in the sectors. Moreover, increased need for user-friendly and patient-centric drug delivery devices is propelling the demand towards a shift from chemically treated glass syringe systems to polymeric-based alternative..

By Application: Vaccines & Immunizations Dominate, Oncology Growing Fastest

Vaccines and immunizations represent the largest application segment due to large-scale global immunization programs, routine childhood vaccination schedules, and heightened focus on pandemic preparedness. Governments and healthcare organizations worldwide are investing heavily in vaccine distribution infrastructure, which has significantly increased demand for prefilled syringe formats that ensure dosage accuracy, reduce preparation time, and enhance safety in mass vaccination campaigns. The growing need for rapid response during infectious disease outbreaks further strengthens this segment’s dominance in the market.

The fastest growing application segment has been oncology as a result of the increasing incidences of cancer globally and rising penetration of injectable biologics and targeted therapies, among others. Cancer treatment frequently demands exact dosing with the minimal yield in controlled drug delivery, these opportunities make prefilled syringes an ideal possible solution for more effective patient solutions and minimizing medication errors. The rise of personalized medicine and an expanding pipeline of parenteral oncology agents are continuing to spur that demand. Secondly, rising number of hospital-based & home healthcare cancer care referral models helped in promoting convenient and reliable injectable medication delivery systems.

By Distribution Channel: Hospitals Dominate, Mail Order Pharmacies Growing Fastest

hospitals represent the largest share of the market because they are considered to be a primary point for drug administration via injection, emergency care, surgeries and inpatient services. They administer the bulk of complicated therapies–biologics, vaccines and life-saving drugs–where pre-filled syringes are favored for their precision, sterility and ease of use. High patient inflow along with the presence of strong institutional procurement systems also allows hospitals to remain at the top in terms of order volumes received by healthcare systems globally for prefilled syringe products.

Mail order pharmacies hold the fastest CAGR throughout the forecast period owing to rapid development of home healthcare, growing prevalence of chronic diseases and increasing drug delivery convenience. Patients are moving to self- administration solutions aided by prefilled syringe formats which also supports simple use away from a clinical setting. Digital healthcare platforms along with online pharmacy networks are streamlining access where injectable medications can be delivered to patients' homes in time, allowing for better medication adherence in a longer course of treatment.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

76% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

51% |

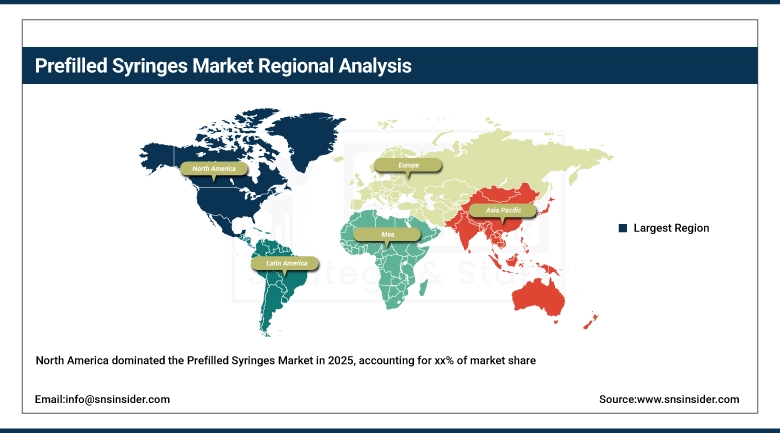

North America Prefilled Syringes Market Insights:

North America dominates the prefilled syringes market, with the U.S. as the primary market driven by its world-leading biopharmaceutical industry, high biologic drug adoption, and patient preference for home self-administration. North America's advanced healthcare system, with strong insurance coverage for biologic drugs, supports premium prefilled delivery formats. The large and growing U.S. biosimilar market is creating new demand as multiple manufacturers compete in prefilled syringe formats.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Prefilled Syringes Market Insights:

Asia Pacific is the fastest-growing prefilled syringe market with a CAGR of 13.66%. China's rapidly growing pharmaceutical manufacturing industry focused on meeting domestic demand and international exports. In India, prefilled syringe manufacturing capacity is being more adopted within the massive and increasing generic and biosimilar pharmaceutical industry. It benefits from demand driven by Japan's aging population with high rates of chronic disease requiring injectable treatments..

Europe Prefilled Syringes Market Insights:

Europe is a sizeable, mature prefilled syringe market. Biologic Drugs in Prefilled Syringe (European). The largest markets are in Germany, France and the UK. The European biosimilar space is more advanced than in the U.S. and national health systems actively encourage substitution of both drug cost reducing biosimilars creating consistent demand for prefilled syringe biosimilars products.

Middle East & Africa Prefilled Syringes Market Insights:

Growing demand for prefilled syringes in the Middle East is driven by a developing pharmaceutical market and growing healthcare infrastructure segments. Today, rising chronic disease burden such as diabetes, cardiovascular disease and cancer is fuelling the demand for injectable biologic therapies. Child immunization campaigns in the Middle East and Africa use high quantities of Vials containing single-dose vaccine presentations. Overseas pharmaceutical firms are extending their distribution of prefilled biologics within GCC.

Latin America Prefilled Syringes Market Insights:

Latin America's prefilled syringe market is growing with increasing biologic drug adoption and diabetes management. Brazil has the largest pharmaceutical market in the region and is building domestic biosimilar manufacturing capacity. The region's growing middle class and improving healthcare coverage are expanding access to biologic treatments. Local manufacturing of insulin pens and biosimilar prefilled syringes is developing in Brazil and Mexico.

Prefilled Syringes Market Growth Drivers

-

The biologic drug revolution and home self-injection trend are the core growth drivers

Biologic agents, among them monoclonal antibodies, insulin analogs, and biosimilars, are the fastest growing class of medication in the pharmacy marketplace and largely delivered by injectable route. Biologics are favoured for prefilled syringes and auto-injectors because they improve dosing accuracy, ease preparation via antibiotic delivery of drug solutions as needed, and enable self injection at home. There are many thousands of molecules under clinical development in the global biologic pipeline, each necessitating a drug delivery device . At home self-injections with other drugs like adalimumab (Humira) is commercially proven and has created a patient preference for this format.t.

Converting biologic drugs from intravenous infusion (which necessitates clinical visits) to subcutaneous self-injection (administered by the patient at home) deliver significant savings for healthcare systems. Research has demonstrated that subcutaneous formulations (compared with IV alternatives) lower treatment administration costs by 30–50% while improving patient satisfaction and adherence. This economic rationale is the engine pushing manufacturer-driven systematic initiatives to create subcutaneous alternatives for their biologic product portfolios..

Prefilled Syringes Market Restraints

-

Glass breakage, drug-device compatibility challenges, and high manufacturing costs create barriers

Glass prefilled syringes are brittle and can easily break when inserted into transport trays, or during patient handling processes that use mechanical force such as auto-injector devices. Container compatibility studies to validate that the container materials do not leach toxic compounds into the drug are laborious and time-consuming. Development time and cost are added as these studies have to be performed again for each drug-device combination. Generating prefilled syringes calls for specialized fill-finish manufacturing, which can be much costlier than traditional vial filling.

Prefilled Syringes Market Opportunities

-

Smart connected prefilled syringes and new biologics in subcutaneous formulations

Patients of all ages have indicated that they would be comfortable with these types of devices, and as patients become more familiar with connected solutions the market will emerge from a high-value opportunity into a significant business problem Smart prefilled syringe, or PFSs, containing sensors that log injection completion status, along with time & GPS data to transmit adherence information to caregivers. These interconnected devices enhance adherence to costly biologic therapies while yielding real-world data on drug use for clinical teams. The continual approach to using recombinant hyaluronidase technology to convert established intravenous biologics into subcutaneous formulations is still contributing the high-value drug reformulation conversion pipeline in the prefilled syringe addressable market.

Recent Developments:

-

2025: BD (Becton, Dickinson) launched the Intevia 1mL Autoinjector platform with enhanced dose accuracy, visual injection completion confirmation, and an optional connectivity module for adherence monitoring, targeting the growing home self-injection market for biologic therapies.

-

2024: West Pharmaceutical Services announced a capacity expansion of its SmartDose electronic wearable injector platform, responding to pharmaceutical customer demand for high-volume subcutaneous drug delivery devices capable of delivering viscous biologics in doses up to 10 mL.

-

2023: Gerresheimer AG expanded its plastic COP prefilled syringe manufacturing capacity at its facilities, responding to growing pharmaceutical customer interest in the superior breakage resistance of cyclic olefin polymer syringes for auto-injector applications.

Prefilled Syringes Market Key Players:

-

Becton, Dickinson and Company

-

Gerresheimer AG

-

Catalent Inc.

-

Nipro Corporation

-

Schott AG

-

Stevanato Group

-

Owen Mumford Ltd.

-

SHL Medical

-

Ypsomed AG

-

Haselmeier GmbH

-

West Pharmaceutical Services

-

Enable Injections Inc.

-

Credence Medical Technologies

-

Bespak

-

Duoject Medical Systems

-

Terumo Corporation

-

Baxter International Inc.

-

Fresenius Kabi AG

-

Weigao Group

-

AptarGroup Inc.

Prefilled Syringes Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.25 Billion |

| Market Size by 2035 | USD 29.3 Billion |

| CAGR | CAGR of 8.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Disposable, Reusable) • By Design (Single-chamber Prefilled Syringes, Dual-chamber Prefilled Syringes, Customized Prefilled Syringes) • By Material (Glass, Plastic) • By Application (Vaccines and Immunizations, Anaphylaxis, Rheumatoid Arthritis, Diabetes, Autoimmune Diseases, Oncology, Others) • By Distribution Channel (Hospitals, Mail Order Pharmacies, Ambulatory Surgery Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Becton, Dickinson and Company; Gerresheimer AG; Catalent Inc.; Nipro Corporation; Schott AG; Stevanato Group; Owen Mumford Ltd.; SHL Medical; Ypsomed AG; Haselmeier GmbH; West Pharmaceutical Services; Enable Injections Inc.; Credence Medical Technologies; Bespak; Duoject Medical Systems; Terumo Corporation; Baxter International Inc.; Fresenius Kabi AG; Weigao Group; AptarGroup Inc. |

Frequently Asked Questions

The Prefilled Syringes Market is expected to grow at a CAGR of 12.51% from 2026 to 2035.

The Prefilled Syringes Market was valued at USD 9.25 billion in 2025.

Ans: Biologics & Biosimilars is both the largest and fastest-growing application, driven by the booming biologic drug pipeline and growing biosimilar market.

North America dominates the Prefilled Syringes Market, with the United States as the primary market due to its world-leading biopharmaceutical industry.

Asia Pacific is the fastest-growing region with a CAGR of 13.66%, driven by rapidly expanding pharmaceutical and biotechnology industries in China, India, and Japan.

Get in Touch