Purified Terephthalic Acid Market Report Scope & Overview

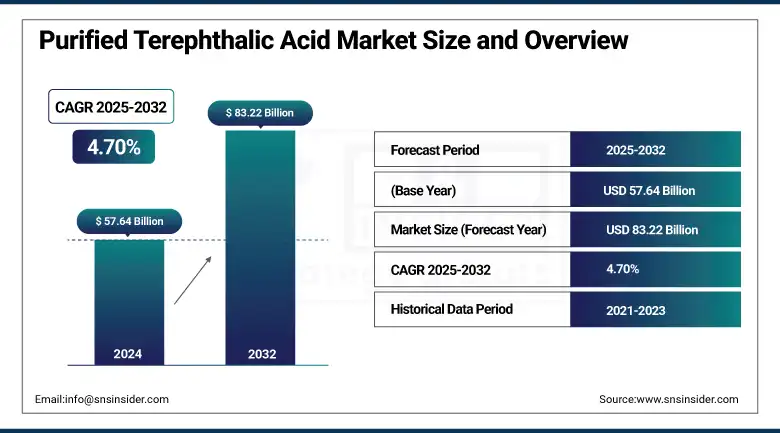

The Purified Terephthalic Acid (PTA) market size was USD 57.64 billion in 2024 and is expected to reach USD 83.22 billion by 2032, growing at a CAGR of 4.70% over the forecast period of 2025-2032.

Purified terephthalic acid market analysis indicates that the increasing demand for polyester fibers drives the market growth. Polyester fibers, the main application of PTA, are used in the textile industry in the production of a wide range of durable, crease-resistant, low-cost clothing, home furnishings, and other industrial fabrics.

Due to rising global populations, as well as increasing disposable incomes, particularly in emerging economies, the demand for textile products has risen rapidly, which, in turn, has led to an uptick in polyester demand. Furthermore, due to the strength, stretchiness, and ability of polyester to resist moisture better than cotton, it is preferred in many uses. With the rise of fast fashion, this need only increases, especially with the expansion of the global apparel industry itself.

To Get more information On Purified Terephthalic Acid Market - Request Free Sample Report

The U.S. International Trade Commission (USITC) found that the importation of fine denier polyester staple fiber has risen significantly, causing the domestic industry to suffer serious injury. As a result, the USITC did recommend tariffs and tariff-rate quota measures to support domestic producers from what they then concluded was a surge of imports.

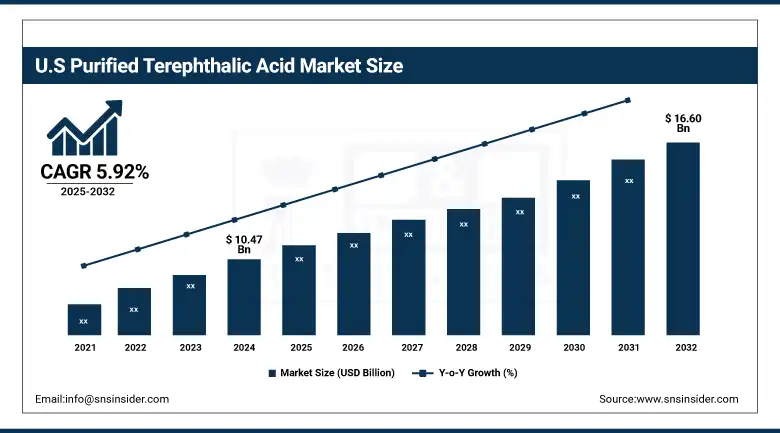

U.S Purified Terephthalic Acid market size was USD 10.47 billion in 2024 and is expected to reach USD 16.60 billion by 2032 and grow at a CAGR of 5.92% over the forecast period of 2025-2032. It is owing to the established packaging sector, with a continuous requirement for a critical feedstock, PTA, due to demand for PET bottles and containers, primarily used in beverage, household, consumer, and personal care products. Further, polyester fibers and resins are consumed in huge volumes by the textile and automotive industries in the U.S., stimulating the demand for PTA, contributing to the industry's growth. Key local petrochemical players that have value-added production facilities in one complex represent a rational basis for PTA manufacturing, pure terephthalic acid as there is a cheap and domestic availability for PTA building blocks, including paraxylene.

Market Dynamics

Drivers

-

Growth in automotive and electronics applications drives the market growth.

The increase in automotive and electronics applications is a major factor driving the growth of the purified terephthalic acid (PTA) market. PTA is a basic material for engineering plastics, e.g., polybutylene terephthalate (PBT) that is used in automotive components and electronic devices because of its high strength and toughness, thermal stability, and chemical resistance properties. These kinds of plastics are finding more applications in the automotive industry, it is more and more often replacing metals and glass as an automotive material to lower car weight, improve fuel economy, and assist in meeting strict emission standards. In the electronics sector, likewise, the materials derived from PTA are employed in connectors, housings, and insulating components, driving demand for miniaturisation, weight and volume reduction, and improved device reliability, and driving the purified terephthalic acid market growth.

According to the International Trade Administration (ITA), U.S. plastic material and product exports were USD 44.7 billion to the 20 U.S. Free Trade Agreement (FTA) partners in 2023. The high export volume highlights the importance of the U.S. in the worldwide plastics market, PTA, and derivatives. In an updated release of its 2024 Plastics Guide, ITA details U.S. export information of PTA in several applications, emphasizing the significance of PTA for the U.S.

Restrain

-

Trade tariffs and import restrictions may hamper the market growth.

The Purified Terephthalic Acid (PTA) market is experiencing a big difficulty with the aid of changing exchange tariffs and import restrictions. By applying tariffs on imports and exports, these trade barriers can hinder the smooth flow of PTA across borders and, in turn, can raise the cost of raw materials and end products. Tariffs tend to repeatedly increase the price of feedstocks or PTA products for manufacturers situated in countries that heavily source feedstock via imports- such increased costs are eventually passed down to consumers hurts demand at a macro level. Moreover, import restrictions can restrict PTA availability in specific regions, leading to supply shortages and production delays of downstream sectors such as textiles and packaging.

Opportunities

-

The growing PET recycling industry creates opportunities in the market.

The expanding PET recycling industry is a key opportunity for the purified terephthalic acid (PTA) market. With growing global environmental concerns and stringent regulations against plastic waste, recycling old PET end products is now becoming a high priority for the economic and ecological success of low low-landfill and low-carbon-footprint society. Specifically, rPET can be depolymerized to yield recycled PTA that may replace virgin PTA as a sustainable alternative. Not only does this align with the transition of the circular economy, but it also caters to the growing demand of consumers for sustainable and green products. In addition, new technologies in recycling have allowed for improved recycling efficiency and higher quality of recycled PTA, appealing to purified terephthalic acid companies in textiles, packaging, and other applications, and driving the purified terephthalic acid market trends.

In 2023, SK Chemicals also acquired a chemical recycling plant from Shuye Environmental Technology for 99 million to create 50,000 tons per year of PET that will be chemically recycled.

Additionally, Indorama Ventures has been increasing its recycling capacity in Brazil from 9,000 tons to 25,000 tons a year, showing that it is keen to ramp up rPET output to meet demand.

Segmentation Analysis

By Application

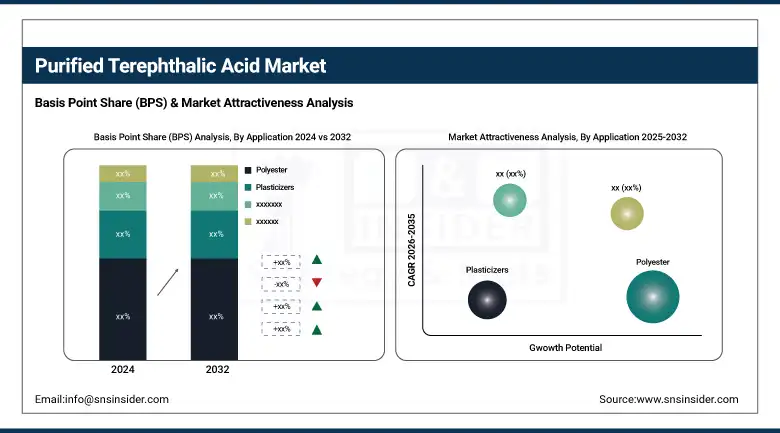

The polyester segment held the largest purified terephthalic acid market share, around 48%, in 2024. It is due to its large applications in the textile & apparel industry. Natural long long-lasting polyester fibers are manufactured from PTA because of good strength, resistance to creasing, and cost effectiveness, along with cleaning convenience compared to cotton and woolen fibers. This quality has made polyester the most popular synthetic fiber in the world. High consumption of polyester has also been driven by the increasing global demand for fast fashion and activewear, which are heavily made from polyester. Polyester is also used for home furnishings, industrial fabrics, and packaging materials.

Plasticizers held a significant purified terephthalic acid market share because they can be essential in improving the flexibility, toughness, and processability of plastics. Plasticizers are important in the production of polyvinyl chloride (PVC) in construction materials, automotive interiors, electrical cables, medical devices, and consumer goods. The global demand for flexible PVC products is on the rise due to the rapid pace of infrastructure development and urbanization taking place across the world, particularly across emerging economies, driving the demand for high-performance plasticizers.

By End User

Textile held the largest market share, around 42%, in 2024. It mostly relies on polyester fibers, which are primarily manufactured through PTA. Textiles Polyester is the most popular kind of artificial fibre in the textile business, appreciating its critical strength, elasticity, wrinkle-resistance, and affordable price. In addition, the rapid growth of the world population, accelerating urbanization, and expanding purchasing power of the middle classes have substantially fuelled demand for cheap and hard-wearing textiles, especially in developing economies like China, India, and Bangladesh. Additionally, with the growing popularity of fast fashion, an increased use of home textiles, such as curtains, bed linens, and other types of upholstery and other fabric supplies, polyester fibers are in more demand than ever and drive the purified terephthalic acid industry.

PET Bottles hold a significant market share in the purified terephthalic acid market owing to the increasing scope of bottle application in the packaging market, which includes use for drinks, personal care, household products, and other use cases. Polyethylene terephthalate (PET), which is known for its strength, clarity, lightweight nature, and excellent barrier properties, is a major end-use of PTA. Because of these attributes, PET bottles are used for packaging carbonated beverages, water, juices, and other consumable products. As the need for consumer-friendly, portable packaging solutions across the globe has driven the demand for PET bottles in urban areas, the consumption of these bottles has increased significantly.

Regional Analysis

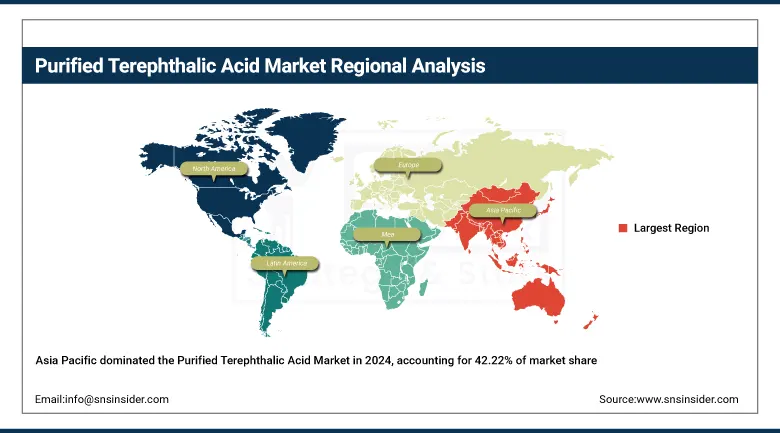

Asia Pacific held the largest market share, around 42.22%, in 2024. It is owing to the development of the polyester industry, increasing industrialization, and, high demand from the packaging and textile industries in the region. China, India, and South Korea are some of the global centers for textile manufacturing whose polyester fibers and resins are primarily produced using PTA as feedstock. The availability of manufacturing infrastructure on a large scale, sufficient availability of raw material (especially paraxylene), and cheap labor make the region highly competitive for PTA production. The rising middle-class population in the Asia Pacific region is also propelling the demand for clothing, home textiles, PET bottles, and food packaging, which are some of the major end-use segments of PTA. In China, where PTA is now also produced, integrated PTA production has taken place not only to realize the economies of scale but also to reduce dependence on PTA imports.

Get Customized Report as per Your Business Requirement - Enquiry Now

In particular, China reported robust growth in its PTA production capacity, with large installations operational, including a facility by the Sinopec Yizheng Chemical Fiber Company with an annual capacity of 3 million tons expected to start in 2024. Also, the growth of PTA production and consumption has been boosted by the government initiatives like the 13th Five-Year Plan in China and the National Petrochemical Policy in India.

North America Purified Terephthalic Acid market held a significant market share and is the fastest-growing segment in the forecast period. It owing to the well-established packaging, textile, and automotive sectors, which are end-use markets for PTA-based products, such as polyethylene terephthalate (PET) and polyester fibers. Moreover, stable demand for PET bottles and containers from the food and beverage industry and rising consumption of lightweight and durable polyester materials for automotive parts and household goods also create lucrative growth avenues for market players in this region. Finally, the U.S. and Canada consist of an established supply chain, a basic set of advanced manufacturing technologies, and numerous producers who are key players within the PTA contest, which makes the availability of PC consistent.

Europe held a significant market share in the forecast period. It is owing to the high focus on sustainability, matched with established recycling infrastructure, coupled with well-established end-use industries such as packaging, automotive, and textiles. An increase in demand for eco-friendly packaging materials within this region has led to greater consumption of PTA, mostly for recycling PET (rPET) utilized in containers and bottles. The transition to PTA-based sustainable solutions has also been accelerated by European Union policies like the Circular Economy Action Plan and tough plastic recycling targets. Furthermore, polyester fibers based on PTA are used in the automotive and home textile markets in Europe and represent the main source of lightweight, high-performance materials. Strong production standards and significant investment in green technologies have continued to push PTA demand from regional players, who benefit from the proximity of leading global manufacturers.

Key Players

British Petroleum (BP), Reliance Industries Limited, Sinopec Corporation, Indorama Ventures Public Company, SABIC, Alpek, Eastman Chemical Company, Indian Oil Corporation, Lotte Chemical Corporation, Mitsubishi Chemical Corporation.

Recent Development:

-

In April 2024, Sinopec commissioned the largest PTA plant in the world with an annual capacity of 3 million tons in China. This includes short-process, smart-manufacturing, and green production technologies for the updated needs of clothing, food, housing, transportation, and environmental health.

-

In October 2023, GAIL bought a 1.25 million metric tons per annum (MMTPA) PTA plant from JBF Petrochemical Ltd, which will now be called GAIL Mangalore Petrochemicals Ltd. The move is an attempt by GAIL to bolster its petchem position in line with PTA's rising domestic demand, according to sources.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 57.64 Billion |

| Market Size by 2032 | USD83.22 Billion |

| CAGR | CAGR of4.70% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Application (Polyester, (Fiber & Yarn Grade, Polybutylene terephthalate (PET) Grade, Film Grade), Polybutylene Terephthalate (PBT), Plasticizers, Others) • By End User (Textile, PET Bottles, Packaging, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | British Petroleum (BP), Reliance Industries Limited, Sinopec Corporation, Indorama Ventures Public Company, SABIC, Alpek, Eastman Chemical Company, Indian Oil Corporation, Lotte Chemical Corporation, Mitsubishi Chemical Corporation. |

Frequently Asked Questions

Asia Pacific led the Purified Terephthalic Acid Market in the region with the highest revenue share in 2024.

Growth in automotive and electronics applications drives the market growth.

Textile will grow rapidly in the Purified Terephthalic Acid Market from 2025 to 2032.

The expected CAGR of the global Purified Terephthalic Acid Market during the forecast period is 4.70%

The Purified Terephthalic Acid Market was valued at USD 57.64 billion in 2024.

Get in Touch