Purpose-built Backup Appliance (PBBA) Market Size Analysis:

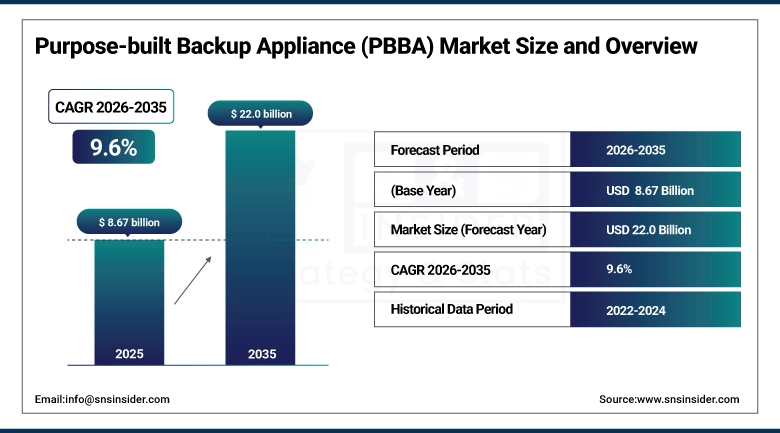

The Purpose Built Backup Appliance (PBBA) Market was valued at USD 8.67 billion in 2025 and is expected to reach USD 22.0 billion by 2035, growing at a CAGR of 9.6% from 2026–2035.

Purpose-built backup appliances are integrated hardware and software systems specifically designed for enterprise backup, recovery and disaster recovery. While there are many different types of storage systems, and even cloud-only solutions PBBAs introduce optimized hardware (such high-capacity storage, dedicated processors) and purpose-built software that allows incredibly fast backup speeds with efficient dedupe, plus quick recoverability of enterprise data. A perfect storm of explosive enterprise data growth, increasing cybersecurity threats (including ransomware that targets backups specifically) and growing regulations about data protection in multiple industries creates strong demand for reliable, dedicated backup infrastructure. More organizations are realizing underpowered backup systems represent a serious business risk that can convert a cyberattack into an existential threat.

Backups from the perspective of ransomware attacks Ransomware attack has change enterprise view on backup infrastructure fundamentally. In the past, backup was often considered a low-priority IT function before ransomware emerged. Now as ransomware is particularly designed to encrypt or delete backup repositories prior to a main attack, organizations realize development that a purpose-built, immutable backup appliance may indeed be the last line of defense between an incident capable of being recovered without any serious impact on their business and complete commercial catastrophe.

This is where cloud-integrated backup appliances appear, providing local high-speed backup while automatically tiering data to the cloud for longer term retention and disaster recovery, solving some of the issues with both purely on-premises and single-cloud approaches. This hybrid approach provides the best of both worlds, and is emerging as a leading enterprise backup model..

Purpose Built Backup Appliance (PBBA) Market Size and Forecast

-

Market Size in 2025: USD 8.67 Billion

-

Market Size by 2035: USD 22.0 Billion

-

CAGR: 9.6% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Purpose Built Backup Appliance (PBBA) Market - Request Free Sample Report

Purpose Built Backup Appliance (PBBA) Market Trends

-

Ransomware resilience features including immutable backup copies and air-gapped repositories becoming standard requirements in PBBA procurement.

-

Cloud integration with automated tiering from local appliance to cloud storage for long-term retention and off-site disaster recovery.

-

AI-powered anomaly detection identifying unusual backup activity patterns that could indicate a ransomware attack in progress.

-

SaaS application data protection becoming a mandatory capability as organizations move workloads to Office 365, Salesforce, and Google Workspace.

-

Hardware appliances featuring purpose-built deduplication engines delivering 10-50x data reduction ratios that significantly lower storage costs.

-

Backup appliance consolidation with primary storage in converged or hyperconverged infrastructure designs.

-

Environmental sustainability requirements driving lower-power backup appliances with improved power usage effectiveness (PUE) metrics.

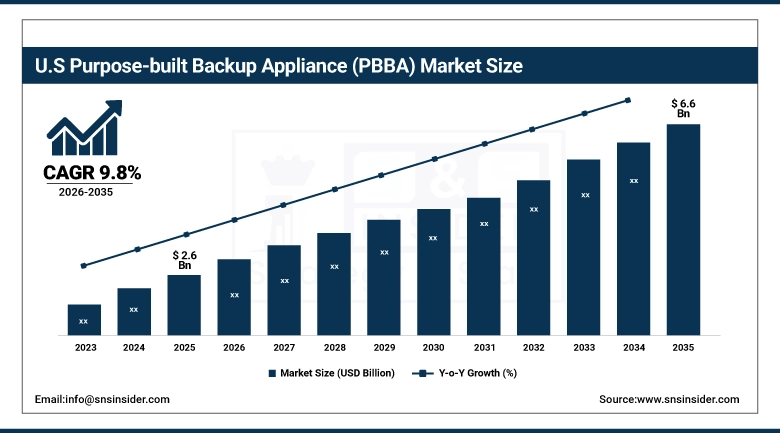

U.S. Purpose Built Backup Appliance Market was valued at USD 2.6 billion in 2025 and is expected to reach USD 6.6 billion by 2035, at a CAGR of 9.8% from 2026 to 2035.

The United States accounts for the largest market share of purpose built backup appliances due to the highest density of enterprise data centers in the world, strong data protection regulations including HIPAA, SOX and SEC cyber disclosure requirements as well as a high prevalence of ransomware attacks that drive organizations to prioritize budget spend on backup infrastructure. The American technology firms such as Dell Technologies, Veritas, IBM and CommVault are worldwide leaders in PBBA research and development as well as sales. Enterprise backup appliances end-users by industry in the U.S.

Long story short, the SEC's 2023 cybersecurity disclosure rules and your new obligation to disclose material cybersecurity incidents occurring within 4 business days have given backup and recovery capabilities a fresher focus. If companies cannot show they can recover quickly from a ransomware attack, there are both regulatory costs to be incurred and reputational damage done, hence boardroom level investment in backup infrastructure.

Purpose Built Backup Appliance (PBBA) Market Segment Insights:

-

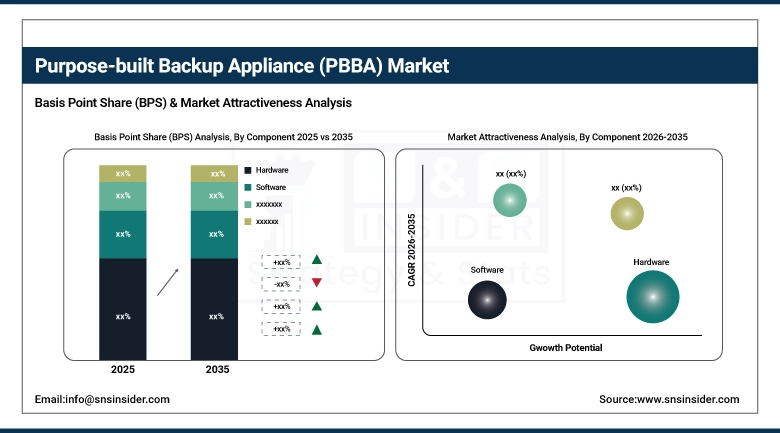

Based on Component, Hardware dominated with the largest revenue share in 2025; Services segment is growing at the highest CAGR.

-

Based on System, Open Systems dominate over proprietary closed systems due to greater flexibility and cloud integration capabilities.

-

Based on Enterprise Size, Large Enterprises hold the largest market share; SMEs are the fastest-growing segment as affordable PBBA solutions become available.

-

Based on Industry Vertical, BFSI and Healthcare hold the largest shares; IT & Telecommunications is expected to grow at the highest CAGR.

Purpose Built Backup Appliance (PBBA) Market Segment Analysis

By Component: Complete Segment Analysis

Hardware forms the basis of the PBBA market with the physical appliance made up of compute nodes, storage arrays, network interfaces and hardware acceleration elements for deduplication along with encryption. Unlike generic, purpose servers, purpose-built hardware provides an order of magnitude better backup throughput, deduplication performance and reliability. Top hardware backup appliances from companies like Dell PowerProtect DD and Veritas Flex Appliance add in-house deduplication hardware that can scour hundreds of terabytes an hour. The revenue still remains primarily with hardware, because in most cases the physical appliance is the majority of the total solution cost.

The services segment, which includes implementation and integration services (the largest share), training, extended warranty and support contracts, and managed backup services to organizations that would rather outsource the management of backup implementations, is the fastest growing component. Modern backup environments are complex, requiring immutability, air-gapping, cloud integration and ransomware detection to be configured properly in order for a business continuity plan to succeed; therefore there is high demand for professional services/implementation. Similarly, lots of organizations also purchase managed backup as a service from system integrators who guarantee successful fulfillment of back backup SLAs.

By System: Complete Segment Analysis

They operate on standard open system operating systems (usually Linux) and integrate with various IT infrastructures from physical servers to VMware & Hyper-V VMs, Kubernetes containers, cloud workloads, databases. Their openness provides integration across the myriad of applications and platforms in use in enterprise IT environments. Market share: The market is ruled by open systems since modern enterprises operate extremely heterogeneous IT infrastructures with different industries not only focusing on the vendor but rather having solutions able to protect all workload types.

Closed (or integrated) backup appliance: Purpose-engineered solutions with hardware and software tightly integrated by one vendor, typically offering optimized performance in that vendor's ecosystem. Co-engineered hardware and Oracle database backup like the Oracle Zero Data Loss Recovery Appliance is an example of such a scenario. Such systems can provide optimal performance in their use cases, but are unable to cover heterogeneous environments robustly.

By Enterprise Size: Complete Segment Analysis

With large enterprises being the largest buyer segment for PBBAs, it is due to their volume of data owned/manipulated; their IT environments are that most complex in terms of what needs protection (understanding all types and layers of applications running), plus they have budgets that allow them to purchase an infrastructure designed specifically for backup. The prospective buyers of enterprise-grade backup appliances include financial institutions, large healthcare systems, government agencies, and multinational corporations. Because the organization needs more than one backup appliance in different locations for geographic redundancy and disaster recovery.

With the price of purpose built backup appliances descending into affordable levels for organizations with smaller IT budgets, SMEs represent the fastest growing segment. The ransomware threat applies to SMEs as much as larger enterprises, and the business impact of backup failure for a smaller organization that cannot recover from failure can be more devastating than at one with more financial flexibility. Backup management platform as a service and smaller-form-factor backup appliances are betting on SMEs, helping make enterprise-grade backup protection attainable..

By Industry Vertical: Complete Segment Analysis

Banking, financial services and insurance is one of the most active vertical for PBBA purchases due to regulatory requirements for data retention, zero tolerance for data loss, and high sensitivity of financial data. Financial regulators (including both SEC vs CFTC, FINRA, and their international equivalents) all have specific data retention windows and prescribed continuity of backing up. Ransomware incursions into financial players displayed that backup integrity is a financial stability issue and led to continuous investment in solid backup infrastructure.

IT service providers and telecom companies are the fastest growing vertical, due to having immense amounts of customer data under their management, while being frequently targeted by ransomware. In order to fulfil SLA promises, cloud service providers require backup infrastructural solutions for their customers. The telecommunications industry operates unique information systems that keep track of every configuration data, subscriber details and call detail record, which needs to be backed up reliably in order for operations to run smoothly and avoid regulatory penalties

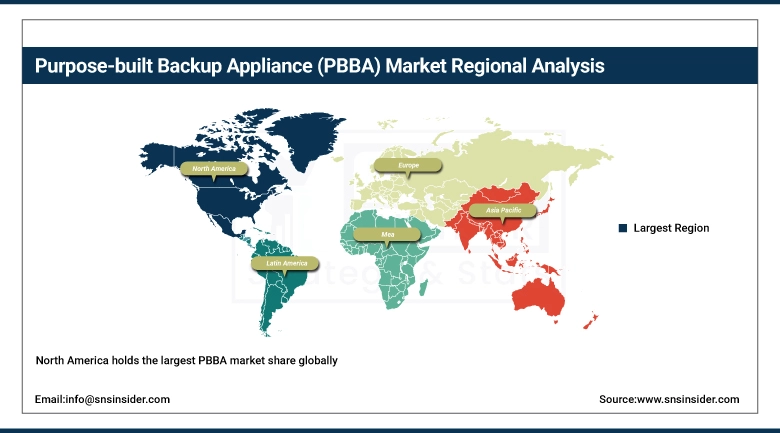

Purpose Built Backup Appliance (PBBA) Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

75% |

|

Europe |

United Kingdom |

29% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

UAE |

37% |

|

Latin America |

Brazil |

50% |

Purpose Built Backup Appliance (PBBA) North America Market Insights:

North America holds the largest PBBA market share globally. The U.S. encompasses the largest concentration of enterprise data in the world, along with a dynamic, sophisticated cyber threat environment. Mandatory backup investments are driven by data protection regulations across healthcare, finance and government. Leading vendors of PBBA from the region such as Dell, Veritas, Commvault and IBM — focused on domestic customers first in development and innovation.

Get Customized Report as per Your Business Requirement - Enquiry Now

Purpose Built Backup Appliance (PBBA) Europe Market Insights:

The European demand for PBBA is largely driven by the GDPR data-protection regulations, which require businesses that process personal data of EU citizens to have capabilities to meet certain retention, protection and recovery requirements. IMF rankings for world: UK, Germany and France have the largest markets. The EU NIS2 directive and DORA regulation for financial services are tightening demands upon cyber resilience, backup, recovery infrastructure. European organizations unable to satisfy local data sovereignty are steering towards on premises or locally deployed backup appliances versus those based in the U.S..

Purpose Built Backup Appliance (PBBA) Asia Pacific Market Insights:

The PBBA market in Asia Pacific is expected to grow at the highest pace during 2023–2028 with rapid digitalization, a rise in the number of cybersecurity threats, increasing regulatory compliances, and growing awareness regarding ransomware risk. In the Region: The largest market in the region is China, where state-owned and private technology companies are investing resources into data protection. The PBBA market is already a mature market in Japan and South Korea as well. The quickly growing enterprise IT sector in India is generating increasing demand for backup infrastructure.

Purpose Built Backup Appliance (PBBA) Middle East & Africa Market Insights:

Increasing digitalization of banking, healthcare, and government services in countries like Saudi Arabia, UAE and Qatar is driving the Middle East PBBA market. Large amounts of new digital data that must be protected is being generated as a result of government e-transformation programs. The region has also been home to numerous high-profile cyberattacks that have put executives in the region on alert regarding backup infrastructure importance. Market in Africa is still early stage but growing with the growth of mobile banking, e-government and enterprise IT.

Purpose Built Backup Appliance (PBBA) Latin America Market Insights:

Increasing digitalization of banking, healthcare, and government services in countries like Saudi Arabia, UAE and Qatar is driving the Middle East PBBA market. Large amounts of new digital data that must be protected is being generated as a result of government e-transformation programs. The region has also been home to numerous high-profile cyberattacks that have put executives in the region on alert regarding backup infrastructure importance. Market in Africa is still early stage but growing with the growth of mobile banking, e-government and enterprise IT.

Purpose Built Backup Appliance (PBBA) Market Growth Drivers

-

The ransomware epidemic and exponential data growth are the primary market drivers

Regardless of business size or industry, firms are now facing insider threats from ransomware attacks. Modern ransomware attacks are no longer just going after anything, they now actively target backup infrastructure and try to encrypt or delete the available backup data before performing the primary encryption event rendering any recovery impossible other than by paying some ransom. That is why immutable storage and air-gap are features inherent to purpose-built backup appliances that are made for surviving these attacks. Digital transformation, IoT, and AI are driving another tsunami of enterprise data growth -- the sheer volume of data to protect, more sophisticated and scalable backup infrastructure.

Ransomware attacks are reportedly costing U.S. businesses more than USD 30 billion per year according to an FBI report in 2023, and SEC rules mandating the public disclosure of material cybersecurity incidents have elevated backup and recovery infrastructure from a back-office IT decision into a boardroom-level agenda item. It is this promotion of backup from an operations to a strategy priority that is leading to larger budgets and premium products being deployed.

Purpose Built Backup Appliance (PBBA) Market Restraints

-

Cloud-native backup services and hyperconverged infrastructure integration create competitive pressure

The continued emergence of cloud native backup services from AWS (Backup), Microsoft Azure Backup, Google Cloud Backup and others continues to put price pressure on hardware backup appliances in certain scenarios. Cloud backup with changing data volumes or unstructured data — Cloud backup can be a more affordable option for data that does not require rapid restoration and organizations whose data volumes are variable or continue to rise. Moreover, hyperconverged infrastructure platforms from Nutanix, VMware among others have integrated baseline backup functionalities into their solutions that could eliminate standalone PBBA opportunities in certain segments.

Purpose Built Backup Appliance (PBBA) Market Opportunities

-

Ransomware-resilient immutable backup and cloud-integrated tiering create premium value propositions

The most valuable product category in the market is that with backup appliances and proven immutable storage that even attackers who obtain administrator credentials cannot delete or encrypt. The combination of clean room recovery and hardware-based write-once-read-many (WORM) storage that enables organizations to wipe out ransomware from backups before restoring will make a powerful premium offering. Economics that will appeal to CFOs as well as CIOs are found in cloud-integrated appliances that automatically tier cold backup data from hardware to low-cost cloud object storage.

Recent Developments

-

2025: Commvault Systems and Microsoft expanded their integration between Commvault Cloud and Microsoft Azure, enabling seamless orchestration of backup and recovery across on-premises and Azure cloud environments through a single management interface, representing the next generation of hybrid cloud backup.

-

2024 (March): Veritas Technologies launched NetBackup 10 with AI-driven analytics that automatically identify backup anomalies suggesting ransomware activity, provide predictive storage capacity management, and generate automated compliance reports for GDPR, HIPAA, and SOX.

-

2023 (January): Dell Technologies launched PowerProtect Data Manager with enhanced immutability features including CyberLock technology that prevents backup deletion or modification for a user-defined period even by administrators with full system access, directly addressing the ransomware threat to backup repositories.

Leading companies in the Purpose Built Backup Appliance Market:

-

Dell Technologies Inc

-

Veritas Technologies LLC

-

IBM Corporation

-

Oracle Corporation

-

Hewlett Packard Enterprise

-

Commvault Systems Inc

-

Barracuda Networks

-

Arcserve LLC

-

Quantum Corporation

-

ExaGrid Systems Inc

-

Veeam Software

-

Cohesity Inc

-

Rubrik Inc

-

Druva Inc

-

Zerto (HPE)

-

NetApp Inc

-

Hitachi Vantara LLC

-

Huawei Technologies Co., Ltd

-

Lenovo Group Limited

-

StoneFly Inc

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.67 Billion |

| Market Size by 2035 | USD 22.0 Billion |

| CAGR | CAGR of 9.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By System (Open System, Closed/Integrated System) • By Enterprise Size (Large Enterprises, SMEs) • By Industry Vertical (BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Government & Public Sector, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Dell Technologies Inc, Veritas Technologies LLC, IBM Corporation, Oracle Corporation, Hewlett Packard Enterprise, Commvault Systems Inc, Barracuda Networks, Arcserve LLC, Quantum Corporation, ExaGrid Systems Inc, Veeam Software, Cohesity Inc, Rubrik Inc, Druva Inc, Zerto (HPE), NetApp Inc, Hitachi Vantara LLC, Huawei Technologies Co., Ltd, Lenovo Group Limited, StoneFly Inc |

Frequently Asked Questions

North America leads globally, with the United States being the dominant market due to its high data density and sophisticated cyber threat environment.

BFSI and Healthcare together account for the largest shares due to strict regulatory requirements and zero tolerance for data loss in these sectors.

The ransomware epidemic forcing backup modernization, exponential enterprise data growth, and tightening regulatory data protection requirements are the primary growth drivers.

The Purpose Built Backup Appliance Market was valued at USD 8.67 billion in 2025.

The market is expected to grow at a CAGR of approximately 9.6% from 2026 to 2035.

Get in Touch