Railway Telematics Market Report Scope & Overview:

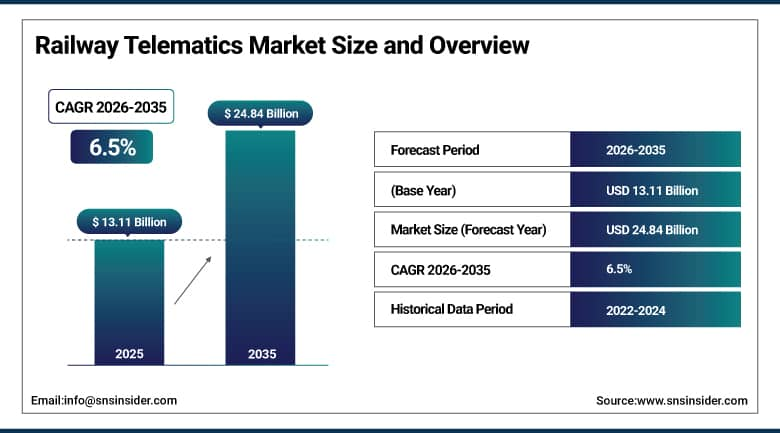

The Railway Telematics Market was valued at USD 13.11 Billion in 2025 and is expected to reach USD 24.84 Billion by 2035, growing at a CAGR of 6.5% from 2026–2035.

The global railway telematics market is undergoing a broad-based transformation as rail operators worldwide invest in connected, data-driven technologies that improve fleet visibility, safety compliance, and operational efficiency across both freight and passenger networks. Telematics integrates telecommunications and informatics into railway systems to enable real-time monitoring of asset location, condition, and performance, generating operational intelligence that modern operators require to reduce unplanned downtime, optimise asset utilisation, and satisfy increasingly stringent safety and emissions regulations. Over 60% of global rail operators now consider telematics a core operational investment, reflecting the technology’s transition from early adopter niche to mainstream rail infrastructure requirement. Freight networks account for approximately 83% of current deployment and are being joined by passenger rail operators whose service reliability ambitions require real-time visibility. Falling sensor and connectivity hardware costs, the maturation of AI-powered predictive analytics, and the availability of satellite-cellular hybrid connectivity are each independently accelerating market growth as rail operators across all geographies and fleet sizes find compelling economic cases for telematics investment.

Wabtec Corporation acquired Frauscher Sensor Technology Group in July 2025 for EUR 675 million, expanding its rail signaling and sensor portfolio across European and Indian markets, and in December 2024 entered a commercial distribution agreement with IMT to deploy its railcar telematics technology across major European freight markets, signalling the accelerating consolidation trend among leading players building integrated end-to-end telematics platforms for global rail operations.

Market Size and Forecast

-

Market Size in 2026E: USD 13.95 Billion

-

Market Size by 2035: USD 24.84 Billion

-

CAGR: 6.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Railway Telematics Market - Request Free Sample Report

Railway Telematics Market Trends

-

Growing adoption of AI-powered predictive maintenance is reducing unplanned rail downtime and extending asset lifespan across freight and passenger networks globally.

-

Rising 5G and satellite-cellular hybrid connectivity deployment is extending real-time telematics coverage across remote and cross-border rail corridors beyond cellular reach.

-

Increasing government investment in Positive Train Control mandates and ERTMS implementation is accelerating standardised telematics deployment across national rail networks.

-

Expanding digital twin technology adoption is enabling rail operators to simulate network performance and optimise maintenance scheduling with greater precision and reduced cost.

-

Growing freight digitalisation and cross-border logistics demands are driving standardised railcar tracking and condition monitoring platform adoption across interoperable rail networks.

The U.S. Railway Telematics Market Outlook

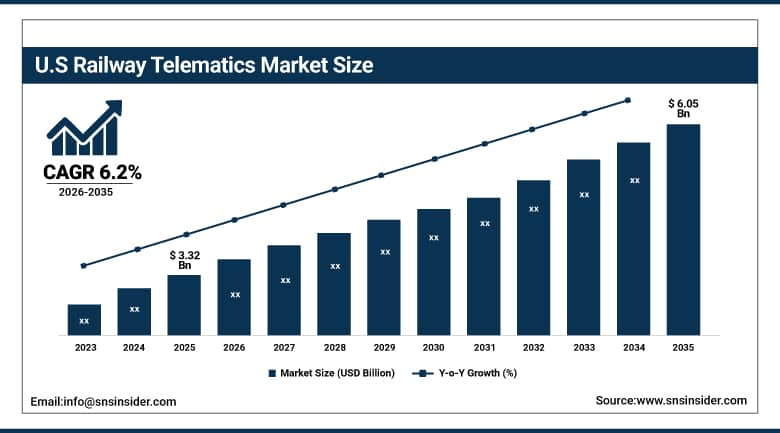

The U.S. Railway Telematics Market was valued at approximately USD 3.32 Billion in 2025 and is expected to reach approximately USD 6.05 Billion by 2035, growing at a CAGR of approximately 6.2%.

Demand in the U.S. market is driven by the federal Positive Train Control mandate that created a structural telematics hardware and software deployment requirement across the country’s Class I freight and regulated passenger rail networks, combined with the industry’s voluntary investments in freight corridor digitisation that are advancing beyond PTC compliance toward operational efficiency and shipper visibility improvements. The U.S. accounts for approximately 85% of North American revenues through the world’s most extensive Class I freight railroad network operated by BNSF, Union Pacific, CSX, Norfolk Southern, and Canadian National’s U.S. operations. RailPulse, the open technology consortium advancing railcar telematics standardisation, expanded its membership with CSX joining in July 2024, accelerating interoperable real-time visibility across North American multi-operator freight corridors. Advanced IoT, satellite, and 5G-based telematics adoption by U.S. freight operators is enabling fuel consumption reductions of up to 15%, real-time cargo monitoring for hazardous and high-value shipments, and the data transparency that logistics customers now contractually require from rail carriers competing for freight business against trucking alternatives.

Railway Telematics Market Segment Analysis

-

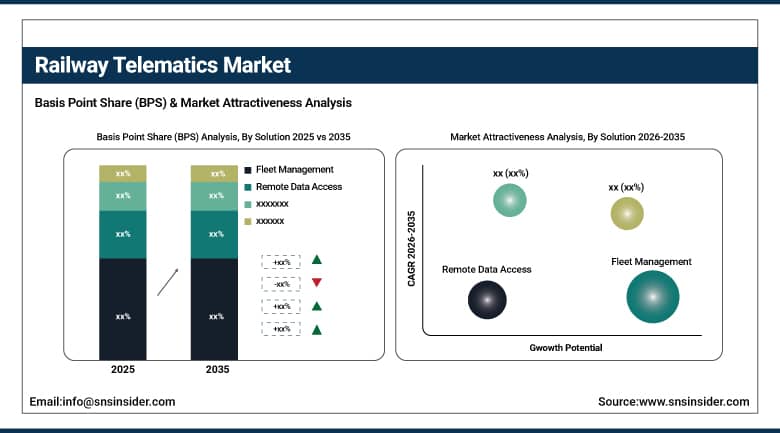

By Solution, fleet management dominated with approximately 41.33% share in 2025 owing to its foundational role in real-time asset tracking and freight visibility. Remote data access is the fastest-growing solution, expanding at a CAGR of 8.46% through 2035.

-

By Railcar, tank cars led the market with approximately 33.15% revenue share in 2025 through their hazardous cargo monitoring compliance requirements. Hoppers are the fastest-growing railcar type, driven by expanding agricultural and mining bulk commodity freight volumes across North American and Asian networks.

-

By Component, telematics control units dominated with approximately 49.21% share in 2025 as the core hardware enabling data acquisition and transmission across railcar fleets. Sensors are the fastest-growing component at a CAGR of 8.16%, driven by multi-function condition and load monitoring adoption.

-

By Train Type, freight dominated with approximately 83.11% of market share in 2025, underpinned by commercial asset tracking, cargo monitoring, and regulatory compliance requirements across Class I and regional freight operations. Passenger rail is the fastest-growing train type at a CAGR of 9.14%.

By Solution, fleet management dominates, remote data access grows fastest

Fleet management retained the dominant solution position with approximately 41.33% of the railway telematics market in 2025, reflecting its foundational role in providing rail operators with the real-time asset visibility and utilisation analytics that freight and passenger network operations require for commercial performance and regulatory compliance. The solution encompasses GPS-based location tracking, railcar dwell time monitoring, route optimisation, and asset utilisation reporting that collectively enable operators to reduce empty car miles, improve cycle times, and satisfy the shipper visibility demands that have become contractual expectations across competitive freight logistics markets. Fleet management’s dominance is further reinforced by the mandatory nature of its core reporting functions, as regulatory filings, safety compliance documentation, and interoperability requirements with industry clearinghouse systems depend on the continuous location and status tracking that fleet management platforms generate across operational networks at all times.

Remote data access is the fastest-growing solution at a CAGR of 8.46% through 2035, driven by the progressive shift of railway operations management toward cloud-based analytics platforms that enable maintenance teams, network operations centres, and management to access real-time and historical fleet performance data from any location without requiring physical terminal access at operational sites. The growing sophistication of cloud-delivered rail analytics, encompassing predictive maintenance alerts, network performance dashboards, and regulatory compliance reporting generated automatically from telematics data streams, is simultaneously improving the operational value of remote access and expanding the range of organisational roles that use telematics data as a standard decision-making input. Each improvement in connectivity reliability and cloud platform capability makes remote data access a more commercially compelling solution category for operators seeking to extend their telematics investment beyond the railcar-level hardware into enterprise-level operational intelligence.

By Component, telematics control units dominate, sensors grow fastest

Telematics control units retained the dominant component position with approximately 49.21% of the railway telematics market in 2025. The TCU is the central hardware node of every railcar telematics installation, combining GPS positioning, cellular and satellite communication, onboard data processing, and power management in a ruggedised unit engineered to survive the vibration, temperature extremes, and electromagnetic environment of railway operations over multi-year deployment lifetimes without frequent maintenance intervention. Its market dominance reflects the universal requirement for a reliable data acquisition and transmission device as the foundational element of any telematics deployment, regardless of the specific monitoring application, connectivity technology, or analytics platform that the broader system incorporates. The TCU’s commercial importance grows proportionally with the fleet digitisation investments that operators across North America, Europe, and Asia Pacific are currently executing at scale.

Sensors are the fastest-growing component in the railway telematics market, driven by the expanding range of monitoring applications that multi-function sensor integration enables beyond the location tracking that TCUs natively provide. Modern railway telematics deployments increasingly incorporate vibration sensors for bearing and wheelset condition monitoring, temperature sensors for cargo integrity verification in refrigerated and hazardous material cars, load sensors for fill-level measurement in hopper and tank car applications, door and seal sensors for security monitoring of high-value freight, and shock detection sensors for impact event recording that supports damage claim management and liability documentation. Each additional sensing capability added to a railcar installation increases both the hardware revenue per unit and the operational data value delivered, expanding the commercial justification for telematics investment across a broader range of railcar types, operators, and geographic markets than location-only telematics could previously reach.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.0% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

UAE |

32.1% |

|

Latin America |

Brazil |

44.2% |

North America Railway Telematics Market Insights

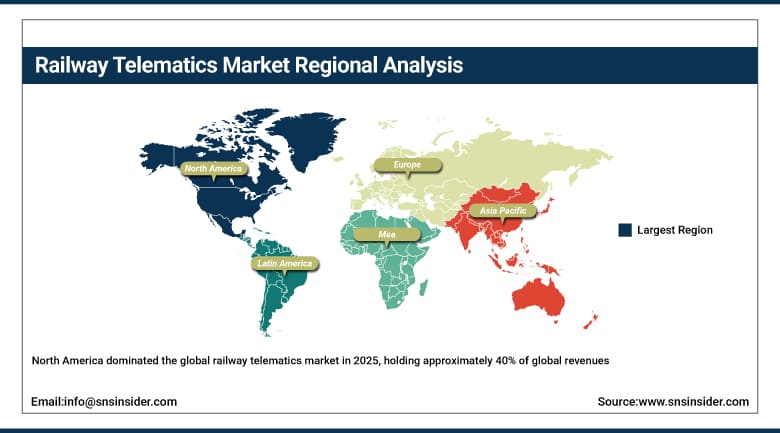

North America dominated the global railway telematics market in 2025, holding approximately 40% of global revenues, with the United States accounting for approximately 85% of North American revenues. The region’s leadership is grounded in the world’s most extensive Class I freight railroad network whose commercial operators have made freight corridor digitisation a strategic investment priority, combined with the federal PTC mandate creating a structural baseline requirement for telematics hardware across regulated routes and the active RailPulse consortium whose open technology standardisation is accelerating interoperable deployment across multi-operator freight networks simultaneously. Over 50% of U.S. rail operators now integrate telematics into environmental performance strategies, using connectivity and analytics to reduce fuel consumption and comply with emissions tracking requirements imposed by federal and state regulatory authorities.

Canada contributes approximately 15% of North American revenues through Canadian National and Canadian Pacific Kansas City’s cross-border freight operations, whose telematics infrastructure extends across U.S.-Canada transboundary corridors and whose investment in predictive maintenance and real-time fleet visibility reflects the same operational efficiency and safety compliance imperatives that drive U.S. market growth, supplemented by Transport Canada’s Safety Management System regulatory requirements for licensed rail operators across the country’s extensive national freight and passenger network.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Railway Telematics Market Insights

Europe is the world’s second-largest railway telematics market, holding approximately 30% of global revenues, characterised by the progressive continental-scale implementation of the European Rail Traffic Management System whose ERTMS/ETCS standards are creating a standardised telematics deployment framework across national rail networks from Norway to Spain. Germany accounts for approximately 28.4% of European revenues as the region’s largest national market, driven by Deutsche Bahn’s extensive network modernisation programme, the country’s commitment to Industry 4.0 digitalisation of transport infrastructure, and the active presence of German rail technology manufacturers including Siemens Mobility and Knorr-Bremse developing and deploying the next generation of railway telematics hardware and analytics platforms for European and global markets.

The United Kingdom, France, and the Nordic countries are significant secondary European markets where government rail infrastructure investment, freight telematics mandates, and passenger rail modernisation programmes are each independently driving telematics adoption. Siemens Mobility’s November 2024 activation of ERTMS on Norway’s Gjøvik Line North, the first Norwegian line to operate the latest standard, exemplifies the continent-wide implementation programme that is progressively upgrading signalling and telematics infrastructure across European national rail networks over the current decade as the EU single European railway area programme advances.

Asia Pacific Railway Telematics Market Insights

Asia Pacific represents approximately 20% of the global railway telematics market and is the fastest-growing region, driven by India’s extraordinary rail network expansion and modernisation under the National Rail Plan, China’s continued development of the world’s largest high-speed rail network alongside freight digitisation, and Southeast Asian countries including Indonesia, Vietnam, and Thailand whose urban rail and inter-city passenger network development is creating new telematics deployment opportunities across emerging market infrastructure being built to modern digital standards from inception.

China accounts for approximately 48.6% of Asia Pacific revenues through the combination of the world’s most extensive high-speed passenger rail network requiring sophisticated telematics and condition monitoring infrastructure, and a rapidly growing freight network whose bulk commodity and containerised logistics operations are adopting telematics for operational efficiency and visibility. India represents the most commercially significant emerging market within the region, as Indian Railways’ electrification programme, dedicated freight corridor development across the country’s most congested logistics routes, and the Kavach automatic train protection system deployment are collectively generating structural telematics procurement demand at a scale whose commercial significance for global vendors is growing rapidly with each year of programme execution and budget commitment.

MEA & Latin America Railway Telematics Market Insights

The Middle East and Africa and Latin America collectively represent approximately 10% of the global railway telematics market and are growing through a combination of new rail infrastructure development incorporating modern digital standards, freight network digitalisation investments by private operators, and the entry of global telematics platform providers extending commercial reach into markets where rail network expansion and safety modernisation programmes create structured procurement demand. Saudi Arabia leads MEA revenues at approximately 32.1% of the regional total through Vision 2030’s ambitious rail development programme, whose new passenger and freight network construction incorporates modern telematics infrastructure as a standard system requirement alongside the Saudi Railway Company’s investment in asset monitoring for its existing freight operations.

Brazil leads Latin American railway telematics revenues at approximately 44.2% of the regional total through its large private freight railroad sector, whose major operators including Rumo Logística, Vale, and VLI operate extensive bulk commodity freight networks across agricultural and mining export corridors where GPS tracking, cargo condition monitoring, and fleet management telematics deliver direct operational cost savings and shipper visibility improvements. Mexico and Argentina represent secondary markets where passenger rail modernisation and freight network efficiency programmes are creating incremental telematics demand alongside the commodity export freight networks that have historically represented the region’s primary deployment driver.

Market Dynamics:

Growth Drivers: Rising safety regulations, government smart rail investment, and growing freight digitisation demand driving global telematics adoption

The increasing enforcement of rail safety compliance requirements, encompassing PTC mandates in the U.S., ERTMS implementation across Europe, and equivalent safety standards in Asia Pacific, is creating regulatory-driven baseline telematics demand that operators must satisfy regardless of discretionary investment appetite. Over 50% of global rail operators integrate telematics into environmental performance strategies, using connectivity to reduce fuel consumption by up to 15% and comply with emissions tracking requirements. Government infrastructure investment programmes in India, Saudi Arabia, and Southeast Asia are directly creating new procurement requirements as modern digital standards are incorporated into new network construction from project inception, expanding the addressable market with each major infrastructure programme launched.

Restraints: High installation costs and legacy infrastructure integration complexity limiting adoption pace among smaller and regional rail operators

The deployment of railway telematics systems across legacy rolling stock fleets requires substantial capital investment in ruggedised hardware retrofitting, connectivity infrastructure, and systems integration with existing operational management platforms whose proprietary architectures were not designed for open API connectivity with modern cloud-based telematics platforms. Smaller regional and short-line railroad operators face particular economic barriers, as per-railcar installation costs represent a proportionally larger share of their capital budgets than for Class I operators whose fleet scale enables cost amortisation and procurement leverage that makes telematics economics compelling. Remote corridor coverage gaps in developing markets compound the challenge by limiting the value proposition of telematics in corridors where cellular connectivity is absent and satellite alternatives carry higher subscription costs.

Opportunities: AI-powered predictive maintenance, digital twin integration, and satellite connectivity expansion creating new value pools across global railway operations

Rapid advances in AI-powered predictive maintenance analytics are creating a commercially significant expansion opportunity beyond the location tracking and fleet management applications that have historically defined railway telematics deployment, as the demonstrated ability to predict bearing failures, wheel defects, and brake system degradation weeks before failure events translates directly into avoided derailment risk, reduced emergency maintenance cost, and improved asset availability quantifiable in direct financial terms. The growing commercial viability of satellite-cellular hybrid connectivity from providers including Iridium, Starlink, and Inmarsat is simultaneously addressing the remote corridor coverage limitation that has constrained telematics deployment value in the mining, agricultural, and mountain route rail corridors where unplanned equipment failures carry the highest safety and commercial consequences.

Recent Developments:

-

2025: Wabtec Corporation completed its EUR 675 million acquisition of Frauscher Sensor Technology Group in July 2025, significantly expanding its railway sensor and signaling technology portfolio across European and Indian markets and advancing its integrated end-to-end telematics and safety system platform strategy for both freight and passenger rail operators across global markets.

-

2024: Siemens Mobility activated the European Rail Traffic Management System on Norway’s Gjøvik Line North in November 2024, the first Norwegian line to operate the latest ERTMS standard, demonstrating Siemens’ leadership in continental ERTMS implementation that is progressively upgrading signalling and telematics infrastructure across European national networks under the EU single railway area programme.

-

2024: RailPulse expanded its North American freight railcar telematics standardisation initiative through CSX joining the open technology coalition in July 2024, adding one of the largest U.S. Class I railroads to the infrastructure enabling real-time railcar visibility across interoperable freight networks and accelerating industry-wide standardisation of telematics data formats and connectivity protocols.

Railway Telematics Market Key Players are:

-

Siemens AG

-

Alstom SA

-

Wabtec Corporation

-

Thales Group

-

Hitachi Rail Limited

-

Robert Bosch GmbH

-

Knorr-Bremse AG

-

IBM Corporation

-

Nokia Corporation

-

Trimble Inc.

-

SAP SE

-

ORBCOMM Inc.

-

Railnova SA

-

Bombardier Inc. (Alstom)

-

SAVVY Telematics Systems AG

-

Amsted Industries Inc.

-

A1 Digital International GmbH

-

Toshiba Corporation

-

General Electric (Wabtec)

-

Intermodal Telematics BV

Railway Telematics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 13.11 Billion |

| Market Size by 2035 | USD 24.84 Billion |

| CAGR | CAGR of 6.5% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Solution (Fleet Management, Automatic Stock Control, Remote Data Access, Railcar Tracking & Tracing, Others) •By Railcar (Hoppers, Tank Cars, Well Cars, Boxcars, Refrigerated Boxcars, Others) •By Component (Telematics Control Unit, Sensors) •By Train Type (Passenger, Freight) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG, Alstom SA, Wabtec Corporation, Thales Group, Hitachi Rail Limited, Robert Bosch GmbH, Knorr-Bremse AG, IBM Corporation, Nokia Corporation, Trimble Inc., SAP SE, ORBCOMM Inc., Railnova SA, Bombardier Inc. (Alstom), SAVVY Telematics Systems AG, Amsted Industries Inc., A1 Digital International GmbH, Toshiba Corporation, General Electric (Wabtec), Intermodal Telematics BV |

Frequently Asked Questions

Get in Touch