Rayon fibers Market Report Scope & Overview:

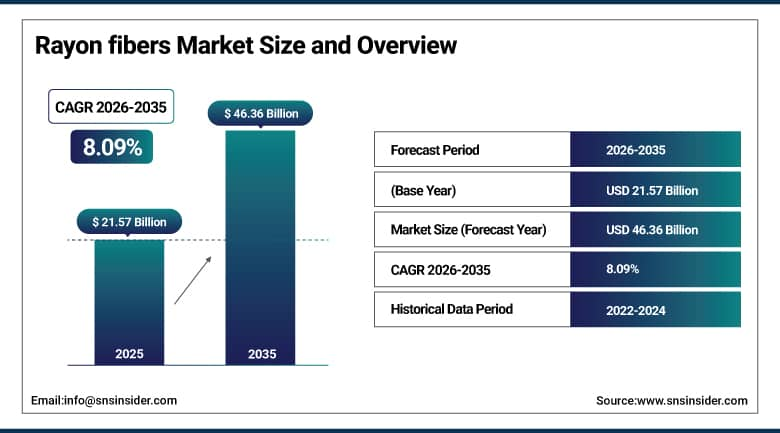

The Rayon Fibers Market was valued at USD 21.57 billion in 2025 and is projected to reach around USD 46.36 billion by 2035, growing at a CAGR of 8.09% from 2026–2035.

The global market for Rayon Fibers is undergoing a consistent growth trajectory owing to the growing trend towards using sustainable and biodegradable fabric types globally, replacing synthetic fibers with regenerated cellulose fiber types, and high demand from the fast fashion & apparel manufacturing segment. Increased consumer preference for comfortable and eco-friendly fabrics is highly aiding in the adoption of viscose, modal, and specifically lyocell fibers on a worldwide basis. Additionally, rising applications in home textiles, hygiene products, and nonwoven medical fabrics are supporting market penetration efforts.

Recent developments include major capacity expansions by leading producers such as Lenzing AG and Aditya Birla Group, focused on scaling lyocell and sustainable viscose production lines. Strategic partnerships between cellulose fiber manufacturers and global fashion brands are increasing to secure traceable and certified sustainable fiber supply chains.

Additionally, advancements in bio-based feedstock sourcing, circular textile recycling initiatives, and low-emission pulp processing technologies are reshaping the competitive landscape, positioning rayon fibers as a key material in the global transition toward sustainable textiles.

Rayon fibers Market Size and Forecast

-

Market Size in 2025: USD 21.57 Billion

-

Market Size by 2035: USD 46.36 Billion

-

CAGR: 8.09% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Rayon fibers Market - Request Free Sample Report

Rayon fibers Market Trends

-

Rising demand for sustainable and biodegradable fibers is accelerating adoption of viscose, modal, and lyocell across textile industries.

-

Growing shift toward eco-friendly and comfort-driven fabrics is boosting rayon usage in apparel and home textiles.

-

Expanding adoption of lyocell and closed-loop production technologies is driving sustainable fiber innovation.

-

Increasing use of rayon in hygiene and medical non-woven applications is widening market scope.

-

Rising regulatory pressure on chemical-based textile production is pushing manufacturers toward greener processes.

-

Growing brand focus on certified and traceable sustainable supply chains is strengthening rayon fiber demand globally.

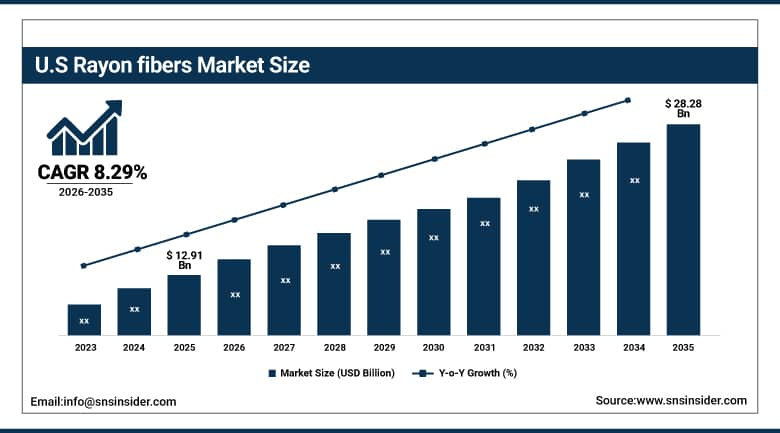

The U.S Rayon Fibers Market was valued at USD 12.91 billion in 2025 and is expected to reach around USD 28.28 billion by 2035, growing at a CAGR of 8.29% from 2026–2035. The market is influenced by the global trend towards sustainability and biodegradability of textile materials, higher usage of regenerated cellulosic fibers like viscose, modal, and lyocell in place of synthetic fibers, and high demand from segments like apparel, household textiles, and hygiene products. The increase in fast fashion manufacturing, consumers’ inclination towards environmentally friendly textiles, and usage of comfort-oriented breathable textiles are also driving the global demand.

Recent developments include Lenzing AG scaling up its lyocell (TENCEL™) production capacity in 2025 to meet rising demand from global fashion brands, strengthening supply of certified sustainable fibers.

Additionally, Aditya Birla Group expanded its eco-efficient viscose manufacturing initiatives and circular fiber programs, enhancing sustainability performance and reinforcing long-term contracts with leading apparel and textile manufacturers worldwide.

Rayon fibers Market Segment Highlights

-

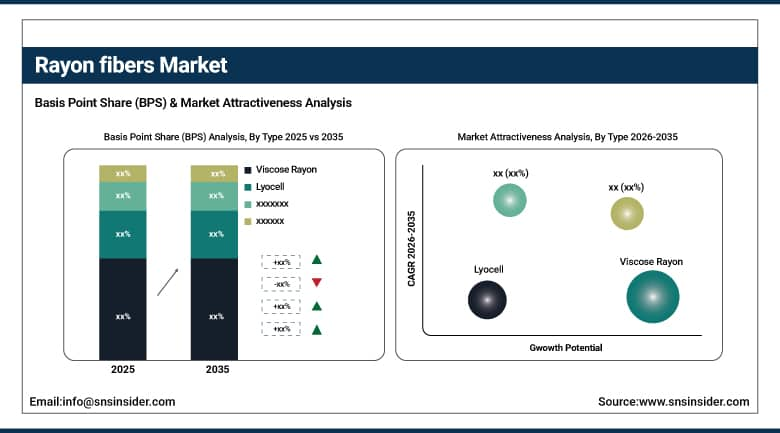

By Type, Viscose Rayon dominated the Rayon Fibers Market with 52.36% share in 2025; Lyocell fastest growing CAGR

-

By Application, Apparel & Fashion Textiles dominated the Rayon Fibers Market with 45.15% share in 2025; Hygiene & Medical Products fastest growing CAGR

-

By End-Use Industry, Textile & Apparel Industry dominated the Rayon Fibers Market with 60.85% share in 2025; Healthcare & Hygiene fastest growing CAGR

-

By Form, Staple Fiber dominated the Rayon Fibers Market with 78.24% share in 2025; Filament Fiber fastest growing CAGR

-

By Distribution Channel, Direct Sales (B2B manufacturers / textile mills) dominated the Rayon Fibers Market with 57.51% share in 2025; Online B2B Platforms fastest growing CAGR

By Type, Viscose Rayon segment dominates the Rayon Fibers Market, Lyocell segment expected to grow fastest

In 2025, the Viscose Rayon segment maintained its dominant position in the Rayon Fibers Market, accounting for 52.36% of total revenue. This leadership is primarily driven by its cost-effectiveness, large-scale availability, and strong adoption across mass-market apparel and home textile manufacturing.

From 2026 to 2035, the Lyocell segment is projected to record the highest CAGR .This rapid growth is driven by the strong global shift toward sustainable and eco-friendly fibers, along with increasing demand for closed-loop production processes and low-impact manufacturing technologies.

By Application, Apparel & Fashion Textiles segment dominates the Rayon Fibers Market, Hygiene & Medical Products segment expected to grow fastest

In 2025, the Apparel & Fashion Textiles segment held the dominant position in the Rayon Fibers Market, accounting for 45.15% of total revenue. This dominance is driven by the large-scale consumption of rayon fibers in fast fashion, casual wear, ethnic wear, and blended textile production, supported by strong demand from global apparel manufacturing hubs.

From 2026 to 2035, the Hygiene & Medical Products segment is projected to record the highest CAGR. Growth is fueled by the increasing use of rayon in non-woven medical textiles, wipes, sanitary products, and absorbent hygiene applications, supported by rising healthcare awareness and demand for disposable, biodegradable materials.

By End-Use Industry, Textile & Apparel Industry segment dominates the Rayon Fibers Market, Healthcare & Hygiene segment expected to grow fastest

In 2025, the Textile & Apparel Industry segment maintained its dominant position in the Rayon Fibers Market, accounting for 60.85% of total revenue. The driving force behind such leadership emanates from the extensive application of rayon fibers in bulk garment production within textile mills and international apparel chains, which still have significant demands for inexpensive bulk fiber supply.

From 2026 to 2035, the Healthcare & Hygiene segment is projected to record the highest CAGR. This increase is driven by the increased application of rayon-based non-woven fabric in the medical, surgical, and hygiene sectors, as well as the growing demand for biodegradable fiber materials that can be safely used in healthcare facilities. The expansion of healthcare facilities worldwide is also fueling the demand.

By Form, Staple Fiber segment dominates the Rayon Fibers Market, Filament Fiber segment expected to grow fastest

The Staple Fiber segment maintained the highest share of 78.24% in 2025. This dominance It is driven by the popularity of the fiber as an industrial textile, excellent affinity for cotton and polyester fiber mixes, and low cost processing during fabric production. Staple rayon continues to be the lifeblood of world textiles because of its applicability in spinnability, weaving, and non-wovens.

The Filament Fiber segment is projected to register the highest CAGR of during 2026–2035.

By Distribution Channel, Direct Sales segment dominates the Rayon Fibers Market, Online B2B Platforms segment expected to grow fastest

The Direct Sales (B2B manufacturers / textile mills) segment held the largest share of 57.51% in 2025. Such domination is due to the existence of effective long-term supply agreements made by suppliers of rayon fibers and the major textile firms, providing reliable bulk supply, effective costs, and guaranteed quality of the raw material. Direct purchase prevails for bulk orders in the production of clothing and home textiles.

The Online B2B Platforms segment is projected to register the highest CAGR during 2026–2035.

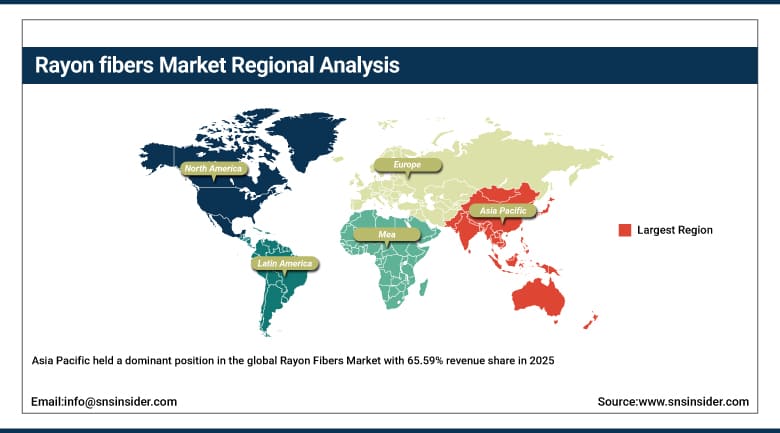

Rayon fibers Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

16.03% |

|

Europe |

Germany |

14.44% |

|

Asia Pacific |

China |

65.59% |

|

Middle East & Africa |

UAE |

2.04% |

|

Latin America |

Brazil |

1.90% |

Asia Pacific Rayon Fibers Market Insights

Asia Pacific held a dominant position in the global Rayon Fibers Market with 65.59% revenue share in 2025, and it is projected to register the highest CAGR of 8.36% from 2026–2035, These are being propelled by massive textile manufacturing industries, robust export-driven apparel manufacturing, and rapid growth in sustainable fiber production capacity. Nations like China, India, Indonesia, Bangladesh, and Vietnam are spearheading the adoption trend, with China and India leading the pack owing to their advanced manufacturing facilities for viscose and lyocell fibers, growing fast-fashion demands, and increased investment in sustainable cellulose fiber manufacturing systems.

Supporting this dominance, textile manufacturers across China and India are increasingly investing in vertically integrated viscose and lyocell production facilities, improving supply chain efficiency and reducing dependency on imports. In addition, the rapid expansion of export-driven apparel clusters and strong penetration of cost-efficient manufacturing infrastructure are reinforcing Asia Pacific’s leadership in global rayon fiber production.

Additionally, recent developments such as large-scale capacity expansion of lyocell production lines by leading Chinese fiber manufacturers and India’s increasing adoption of sustainable viscose manufacturing supported by circular pulp sourcing initiatives are significantly strengthening the region’s position in next-generation eco-friendly fiber production.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Rayon Fibers Market Insights

North America operates under a consumption-driven framework supported by strong demand for sustainable textiles, premium apparel, and hygiene applications, along with increasing adoption of eco-friendly and certified cellulose-based fibers. The region is characterized by advanced retail ecosystems, strong brand presence, and growing preference for biodegradable and comfort-oriented fabrics in both fashion and healthcare textiles.

Supporting this demand, organizations across the United States and Canada are increasingly prioritizing sustainable sourcing of regenerated cellulose fibers, accelerating the use of lyocell and modal in premium apparel and home textile segments. Additionally, growing demand from hygiene and non-woven applications is strengthening rayon fiber utilization beyond traditional apparel markets.

Recent developments include major fashion brands in the U.S. expanding sustainable fiber sourcing commitments toward lyocell-based textiles, and increasing collaboration between global textile suppliers and North American apparel companies to develop low-impact, traceable cellulose fiber supply chains.

Europe Rayon Fibers Market Insights

Europe is an important region for the Rayon Fibers Market because of its emphasis on sustainable laws, circular economy policies, and eco-friendly standards for fabric manufacturing. Nations like Germany, France, Italy, and the United Kingdom are pioneers in the use of superior regenerated cellulose fibers, especially for high-end apparel and technical fabrics.

Supporting this position, European textile and fashion companies are increasingly integrating FSC-certified pulp sourcing and closed-loop fiber production systems, accelerating the transition toward low-emission and environmentally responsible textile manufacturing. Demand for lyocell and modal fibers is particularly strong in premium apparel and home textile applications.

Additionally, rising adoption of eco-label certified fabrics and strict environmental compliance requirements in textile production are reinforcing Europe’s role as a sustainability-driven innovation hub in the global rayon fiber industry.

LAMEA Rayon Fibers Market Insights (Latin America, Middle East & Africa)

In LAMEA, the Rayon Fibers Market is experiencing consistent growth due to an increase in the production of textiles, increased imports of cellulose fibers, and investment in the apparel and home textile sectors. Brazil, Mexico, UAE, Saudi Arabia, and South Africa are playing a role in boosting the demand for rayon fibers in applications related to apparel and hospitality.

Supporting this growth, governments in the Middle East are actively investing in industrial diversification and smart manufacturing initiatives, which are gradually increasing adoption of modern textile materials, including rayon fibers. Latin America is also experiencing rising demand from cost-sensitive apparel production hubs.

Additionally, increasing partnerships between global fiber suppliers and regional textile distributors are improving supply chain accessibility, enabling wider penetration of viscose-based and blended rayon fiber products across emerging markets.

Rayon fibers Market Growth Drivers:

-

Rising global shift toward sustainable and biodegradable textile materials, coupled with strong demand for soft, breathable, and eco-friendly fabrics, is driving robust adoption of rayon fibers across apparel, home textiles, and hygiene applications

A primary factor contributing to the Rayon Fibers Market is the growing shift from traditional man-made fibers to regenerated cellulose fibers like viscose, modal, and lyocell. This shift is motivated by rising environmental policies, sustainable initiatives in fast fashion, and changing customer preferences for comfort-driven natural feel fibers. As major apparel companies pay greater attention to sustainability, rayon fibers have found a place in blended fiber products for their softness, moisture retention, and biodegradability.

Additionally, recent developments such as Lenzing AG expanding its TENCEL™ lyocell production footprint in Asia and Europe to meet rising global demand for sustainable fibers, along with Aditya Birla Group scaling up eco-efficient viscose manufacturing and circular pulp sourcing initiatives, are reinforcing long-term market transformation toward high-performance, low-environmental-impact cellulose fiber systems.

Rayon fibers Market Restraints:

-

Rising environmental compliance pressures, high chemical-intensive processing requirements, and supply chain volatility in cellulose pulp sourcing are increasing production complexity and limiting margin expansion across the rayon fibers industry

The primary structural constraint affecting the Rayon Fibers Market is the environmental and regulatory scrutiny that accompanies the manufacturing process of viscose rayon fibers because it relies heavily on chemicals such as carbon disulfide. The environmental issues surrounding this production process have resulted in stringent sustainability laws, increased compliance costs, and more difficult operations for producers, especially those located in Europe and North America. Moreover, this market is plagued by various issues pertaining to unstable availability of wood pulp and fluctuations in the prices of raw cellulose materials.

Rayon fibers Market Opportunities:

-

Expansion of sustainable textile demand, eco-certified apparel growth, and rising adoption of next-generation cellulose fibers are creating strong opportunities for rayon fiber manufacturers

The major opportunity in the market for Rayon Fibers is the rapidly growing trend of sustainable and circular textile systems in which viscose, modal, and lyocell are replacing artificial fibers in clothing and household textiles. The demand generated by international fashion companies for sustainable, traceable, and eco-friendly fibers has motivated companies to invest in the latest technologies for the production of cellulose fibers. Moreover, closed loop production system, sustainable source of bio-pulp, and sustainable chain systems allow manufacturers to follow high environmental standards and venture into premium and technical textiles as well.

Recent Developments:

-

2026: Lenzing AG expanded its lyocell (TENCEL™) production capacity across Asia and Europe, strengthening supply of sustainable cellulose fibers to meet rising demand from global apparel brands focused on low-impact and certified textile sourcing.

-

2026: Aditya Birla Group (Grasim Industries) advanced its eco-efficient viscose manufacturing initiatives by scaling circular pulp sourcing and low-emission production technologies, improving sustainability performance across its global rayon fiber supply chain.

-

2025: Sateri Holdings increased production efficiency across its viscose rayon facilities through upgraded closed-loop chemical recovery systems, enhancing environmental compliance and reducing overall manufacturing footprint.

Rayon fibers Market Key Players

Some of the Rayon fibers Market Companies

-

Lenzing AG

-

Aditya Birla Group (Grasim Industries Ltd.)

-

Sateri Holdings Limited

-

Tangshan Sanyou Group Xingda Chemical Fibre Co. Ltd.

-

Sinar Mas Group

-

Kelheim Fibres GmbH

-

Zhejiang Fulida Co. Ltd.

-

Yibin Grace Group Co. Ltd.

-

Jiangsu Aoyang Technology Co. Ltd.

-

Shandong Helon Co. Ltd.

-

Birla Cellulose

-

Eastman Chemical Company (Tencel operations legacy alignment)

-

Xinxiang Bailu Chemical Fibre Group Co. Ltd.

-

Thai Rayon Public Company Limited

-

Sappi Limited (Cellulose Specialties division)

-

Bracell (Royal Golden Eagle Group)

-

Acelon Chemicals & Fibre Corporation

-

Weiqiao Textile Company Limited

-

Domsjö Fabriker AB (Aditya Birla-owned specialty cellulose unit ecosystem)

-

Guangdong Xinhui Meida Nylon Co. Ltd.

Rayon fibers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.57 Billion |

| Market Size by 2035 | USD 46.36 Billion |

| CAGR | CAGR of 8.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Viscose Rayon, Modal Rayon, Lyocell, Cuprammonium Rayon, Others) • By Application (Apparel & Fashion Textiles, Home Textiles, Industrial Textiles, Hygiene & Medical Products, Non-woven Fabrics) • By End-Use Industry (Textile & Apparel Industry, Healthcare & Hygiene, Automotive Textiles, Industrial Manufacturing, Others) • By Form (Staple Fiber, Filament Fiber, Others) • By Distribution Channel (Direct Sales (B2B manufacturers / textile mills), Distributors & Traders, Online B2B Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lenzing AG, Aditya Birla Group (Grasim Industries Ltd.), Sateri Holdings Limited, Tangshan Sanyou Group Xingda Chemical Fibre Co. Ltd., Sinar Mas Group, Kelheim Fibres GmbH, Zhejiang Fulida Co. Ltd., Yibin Grace Group Co. Ltd., Jiangsu Aoyang Technology Co. Ltd., Shandong Helon Co. Ltd., Birla Cellulose, Eastman Chemical Company (Tencel operations legacy alignment), Xinxiang Bailu Chemical Fibre Group Co. Ltd., Thai Rayon Public Company Limited, Sappi Limited (Cellulose Specialties division), Bracell (Royal Golden Eagle Group), Acelon Chemicals & Fibre Corporation, Weiqiao Textile Company Limited, Domsjö Fabriker AB (Aditya Birla-owned specialty cellulose unit ecosystem), Guangdong Xinhui Meida Nylon Co. Ltd. |

Frequently Asked Questions

Asia Pacific dominated the Rayon fibers Market in 2025.

The Viscose Rayon segment dominated the Rayon fibers Market in 2025.

Rapid global shift toward sustainable textiles, increasing adoption of biodegradable regenerated cellulose fibers, and rising demand for eco-friendly apparel and hygiene products is the primary growth driver of the Rayon Fibers Market

The Rayon fibers Market was valued at USD 21.57 billion in 2025.

The Rayon fibers Market is expected to grow at a CAGR of 8.09% from 2026 to 2035.

Get in Touch